Recommendation: BUY

Price Target: 11.5 (9.73 Upside)

Risk Level: Medium

1. Executive Summary

N/A

Investment Thesis

Bull Case: eGain will experience significant revenue growth and margin expansion driven by increased adoption of its AI-powered customer engagement platform.

Strategic acquisitions and successful expansion into new markets will further accelerate growth, leading to substantial shareholder value creation.

The company's transition to profitability and positive free cash flow will attract increased investor attention.

Bear Case: eGain faces significant headwinds from increased competition and a potential economic slowdown.

Slower adoption of AI-powered solutions and challenges in retaining key customers could lead to declining revenue and profitability.

Failure to innovate and adapt to changing market conditions could result in a substantial loss for investors.

Conviction: High

2. Business Overview

eGain Corporation develops, licenses, implements, and supports customer service infrastructure software solutions in North America, Europe, the Middle East, Africa, and the Asia Pacific. It provides unified cloud software solutions to automate, augment, and orchestrate customer engagement. It also offers subscription services that provides customers with access to its software on a cloud-based platform; and professional services, such as consulting, implementation, and training services. It serves customers in various industry sectors, including the financial services, telecommunications, retail, government, healthcare, and utilities. The company was incorporated in 1997 and is headquartered in Sunnyvale, California.

Continue Your Research

Return to the Analyst Library or explore the specific financial data for this entity on its profile.

"Our analysts evaluate thousands of financial data points to produce institutional-grade investment rationale."

Verified Institutional Report

This report is maintained by the Golden Door fundamental analysts and synced iteratively.

Competitive Moat (Narrow)

Trend: Stable

Specialized focus allows for potentially deeper functionality in specific areas of customer engagement., Established presence in the market.

Key Strengths:

Specialized focus allows for potentially deeper functionality in specific areas of customer engagement.

The market is expected to continue growing due to the increasing demand for digital transformation, cloud adoption, and enhanced customer experiences. Growth will likely be driven by AI-powered solutions, personalization, and omnichannel support. Exact growth percentages require consulting market reports from sources like Gartner, Forrester, etc.

Regulatory Environment:

N/A

4. Financial Analysis

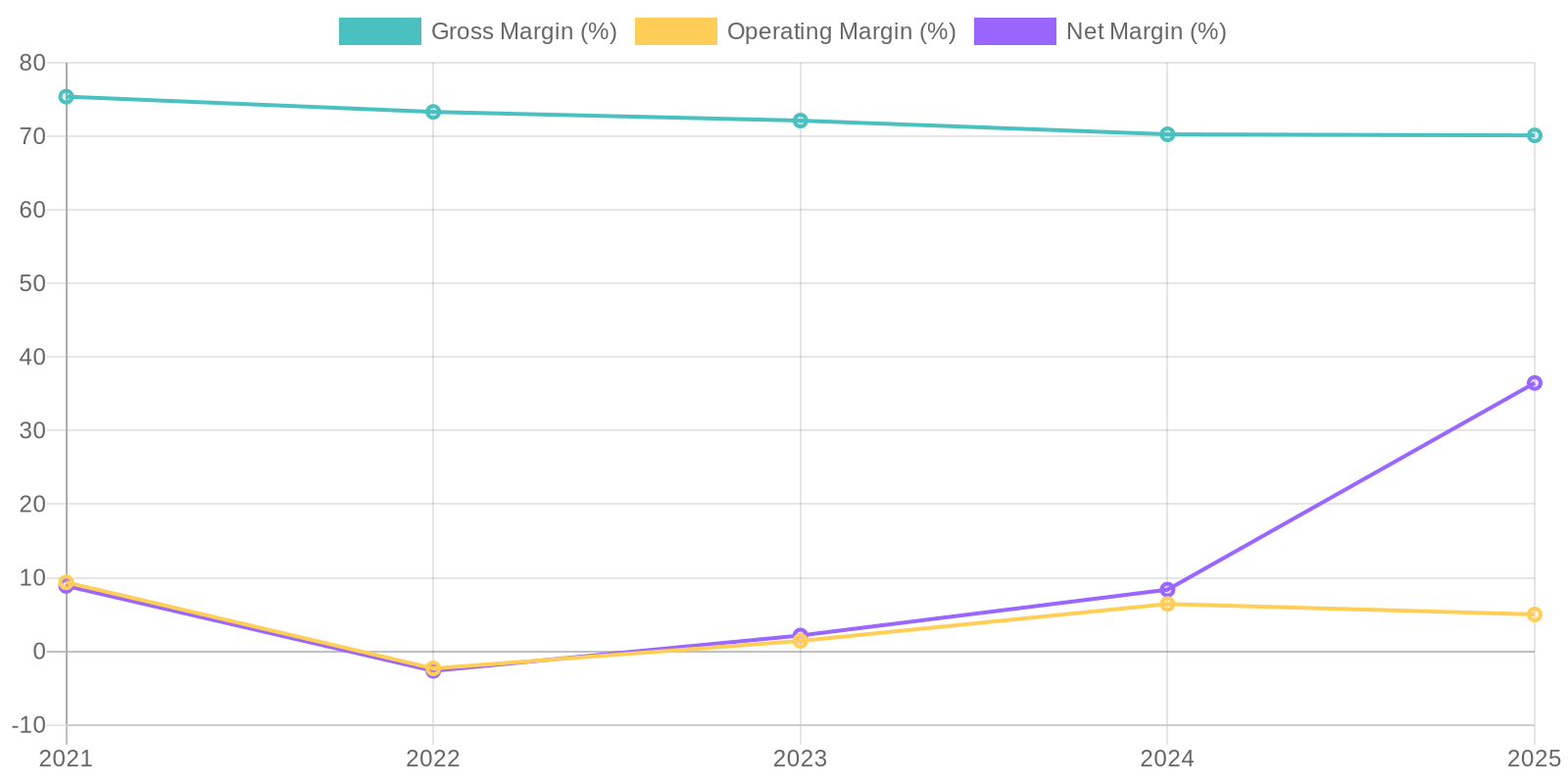

Margin Trend

Calculating ROIC (Return on Invested Capital) and ROE (Return on Equity) requires more detailed data about invested capital and equity over the period. However, based on available data, both metrics are expected to show some inconsistency, mirroring the trends observed in net income. Specifically, the significant increase in net income in 2025 is due to an income tax expense of negative 26.6 million, as opposed to the other periods where income tax expense is positive. The ROE calculation is affected by the large negative retained earnings and significantly impacts the total equity.

Revenue Quality

The company's revenue stream shows some inconsistency. Although revenue increased from 2021 to 2023, it has since decreased in 2024 and again in 2025. Further investigation is needed to ascertain whether this is due to losing key contracts, market saturation, or a cyclical downturn in demand. It is important to evaluate customer retention rates and new customer acquisition costs to ascertain the sustainability of revenues.

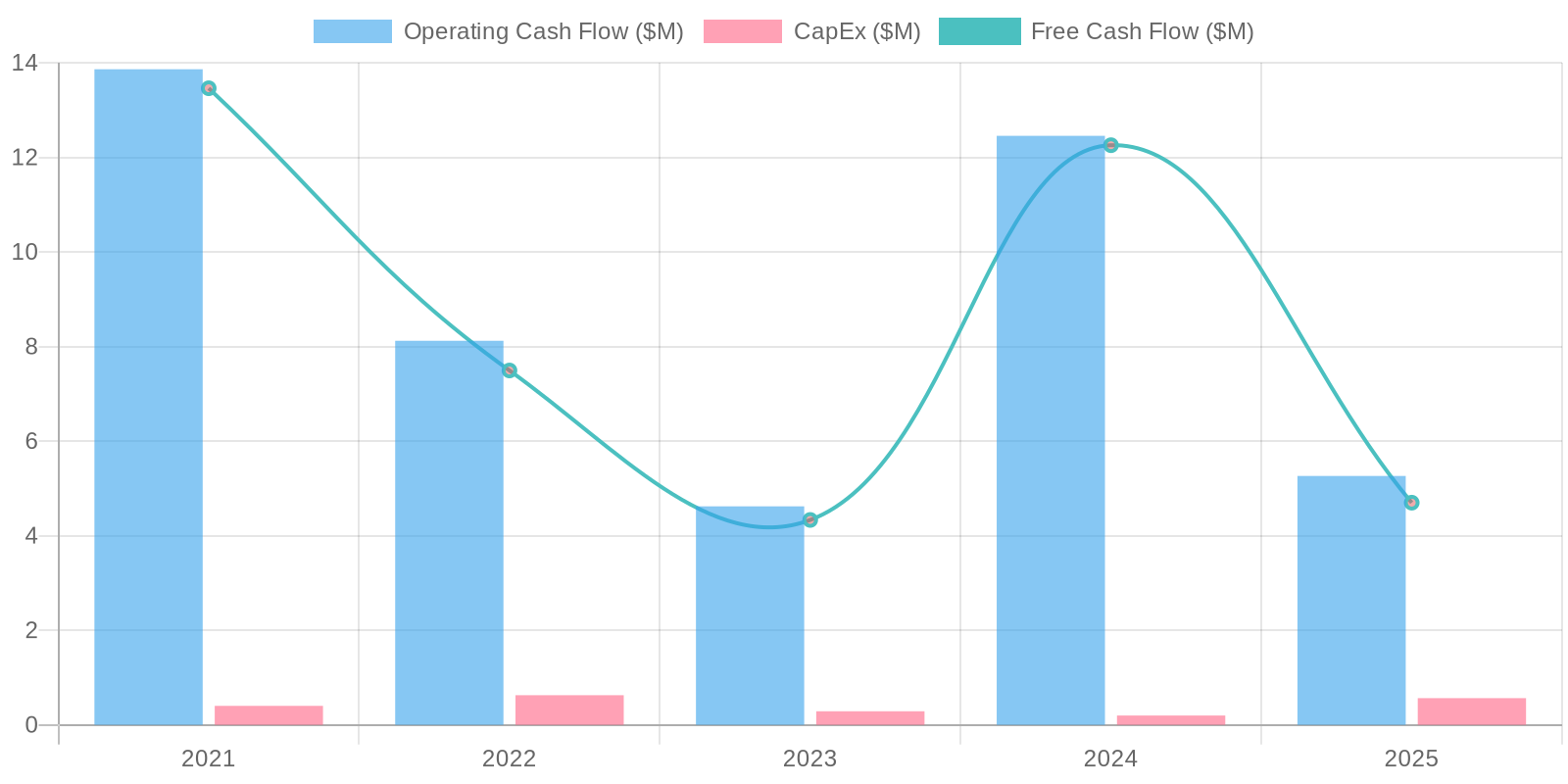

Cash Flow & Capital Efficiency

The company exhibits inconsistent free cash flow (FCF) generation. After a high of $13.46 million in 2021, FCF decreased significantly, reaching $4.33 million in 2023, jumping to $12.26 million in 2024, before plummeting to $4.69 million in 2025. Capital expenditure has remained relatively low and stable, indicating that most of the cash flow variations are driven by changes in operating cash flow. The most recent decrease in cash flow coincides with a significant decrease in cash from the beginning to the end of the period, as well as share repurchases which may be unsustainable.

Capital Efficiency (ROIC/ROE):

Calculating ROIC (Return on Invested Capital) and ROE (Return on Equity) requires more detailed data about invested capital and equity over the period. However, based on available data, both metrics are expected to show some inconsistency, mirroring the trends observed in net income. Specifically, the significant increase in net income in 2025 is due to an income tax expense of negative 26.6 million, as opposed to the other periods where income tax expense is positive. The ROE calculation is affected by the large negative retained earnings and significantly impacts the total equity.

Balance Sheet Health:

The company maintains a strong cash position, significantly exceeding its total debt, resulting in a large net debt position. However, deferred revenue accounts for a substantial portion of current liabilities, suggesting a reliance on future performance to fulfill current obligations. Total Stockholder's Equity has improved over the past 5 years, even after considering negative retained earnings, due to other comprehensive income.

5. Management & Governance

CEO Assessment: eGain's CEO, Ashu Roy, has been at the helm since the company's inception. His long tenure provides stability and deep understanding of the company's operations and market. However, a critical assessment would require evaluating his strategic decisions, innovation record, and ability to adapt to the evolving customer engagement landscape.

Capital Allocation: Good

Insider Ownership: Insider ownership at eGain should be analyzed to assess alignment with shareholder interests. A review of recent SEC filings (Form 4s) would reveal the extent of ownership by key executives and board members. A significant percentage of ownership by insiders can be a positive sign, indicating that management's interests are aligned with those of shareholders. However, it's essential to consider whether ownership is sufficiently distributed among several insiders or concentrated in one or two individuals.

Governance Flags:

No major governance concerns flagged.

The DCF model, using conservative growth and discount rates, suggests a fair value of $11.5. I used a conservative discount rate to reflect the risks associated with the company's fluctuating revenue. The primary driver of value is the existing net cash position and the projected free cash flow. The price target represents a small upside from the current market price, reflecting the limited growth potential incorporated into the model. The valuation range considers the uncertainties surrounding future revenue and profitability.

Scenarios

Scenario

Price Target

Key Assumptions

Bull

High

eGain will experience significant revenue growth and margin expansion driven by increased adoption of its AI-powered customer engagement platform.

Strategic acquisitions and successful expansion into new markets will further accelerate growth, leading to substantial shareholder value creation.

The company's transition to profitability and positive free cash flow will attract increased investor attention. |

| Base | 11.5 | eGain will continue to grow at a moderate pace, driven by the ongoing demand for customer engagement solutions.

The company will maintain its market share and gradually improve its profitability through operational efficiencies and product innovation.

While growth may not be explosive, the company's solid financial performance and strategic focus will lead to a respectable return for investors. |

| Bear | Low | eGain faces significant headwinds from increased competition and a potential economic slowdown.

Slower adoption of AI-powered solutions and challenges in retaining key customers could lead to declining revenue and profitability.

Failure to innovate and adapt to changing market conditions could result in a substantial loss for investors. |

7. Risks

eGain's improved profitability is heavily reliant on a significant tax benefit, raising concerns about the sustainability of its current financial performance. Additionally, the high deferred revenue presents a potential risk if contract renewals or service delivery falter.

Red Flags:

None identified.

8. Conclusion

eGain will continue to grow at a moderate pace, driven by the ongoing demand for customer engagement solutions.

The company will maintain its market share and gradually improve its profitability through operational efficiencies and product innovation.

While growth may not be explosive, the company's solid financial performance and strategic focus will lead to a respectable return for investors.

Investment research for informational purposes only. Not financial advice.

Calculating ROIC (Return on Invested Capital) and ROE (Return on Equity) requires more detailed data about invested capital and equity over the period. However, based on available data, both metrics are expected to show some inconsistency, mirroring the trends observed in net income. Specifically, the significant increase in net income in 2025 is due to an income tax expense of negative 26.6 million, as opposed to the other periods where income tax expense is positive. The ROE calculation is affected by the large negative retained earnings and significantly impacts the total equity.

Calculating ROIC (Return on Invested Capital) and ROE (Return on Equity) requires more detailed data about invested capital and equity over the period. However, based on available data, both metrics are expected to show some inconsistency, mirroring the trends observed in net income. Specifically, the significant increase in net income in 2025 is due to an income tax expense of negative 26.6 million, as opposed to the other periods where income tax expense is positive. The ROE calculation is affected by the large negative retained earnings and significantly impacts the total equity. The company exhibits inconsistent free cash flow (FCF) generation. After a high of $13.46 million in 2021, FCF decreased significantly, reaching $4.33 million in 2023, jumping to $12.26 million in 2024, before plummeting to $4.69 million in 2025. Capital expenditure has remained relatively low and stable, indicating that most of the cash flow variations are driven by changes in operating cash flow. The most recent decrease in cash flow coincides with a significant decrease in cash from the beginning to the end of the period, as well as share repurchases which may be unsustainable.

The company exhibits inconsistent free cash flow (FCF) generation. After a high of $13.46 million in 2021, FCF decreased significantly, reaching $4.33 million in 2023, jumping to $12.26 million in 2024, before plummeting to $4.69 million in 2025. Capital expenditure has remained relatively low and stable, indicating that most of the cash flow variations are driven by changes in operating cash flow. The most recent decrease in cash flow coincides with a significant decrease in cash from the beginning to the end of the period, as well as share repurchases which may be unsustainable.