Deep Dive: Five9, Inc. (FIVN)

Recommendation: HOLD Price Target: 21.59 (2.58 Upside) Risk Level: Medium

1. Executive Summary

Five9, Inc. (FIVN) operates in the Customer Experience (CX) market, providing cloud contact center software. Its current market position is that of a significant, though not dominant, player in a rapidly evolving industry, competing with larger, more established companies like NICE, Genesys, and Twilio, as well as smaller, specialized competitors. Five9's focus is primarily on mid-market and enterprise customers, offering a comprehensive suite of applications for inbound and outbound call centers, omnichannel communications, and analytics. The current price of $19.01 reflects recent challenges and uncertainties, potentially presenting a value opportunity depending on one's assessment of future growth and risks.

Growth catalysts for Five9 include the continued migration of contact centers to the cloud, driven by the need for greater flexibility, scalability, and cost-effectiveness. The increasing adoption of AI-powered solutions within contact centers, such as virtual agents and intelligent routing, also presents a significant growth opportunity. Further expansion into international markets, particularly Europe and Latin America, represents another potential avenue for growth. Strategic partnerships and acquisitions could accelerate market penetration and broaden Five9's product offerings.

Key risks facing Five9 include intensifying competition from larger, well-capitalized players who may offer bundled solutions or aggressively price their services. The risk of technological disruption, particularly from emerging AI technologies, necessitates ongoing innovation and adaptation. Economic downturns could negatively impact customer spending on contact center software. Integration risks associated with acquisitions and the potential loss of key personnel also pose challenges. Furthermore, data security and privacy concerns are paramount, and any breaches could damage Five9's reputation and lead to regulatory penalties.

Valuation of Five9 is complex given its high-growth potential but also substantial risks. At the current price of $19.01, the stock may be considered undervalued by some, especially if future growth catalysts materialize and execution is strong. However, a discounted cash flow (DCF) analysis, incorporating realistic growth rates and discount rates that reflect the risks mentioned above, is crucial for determining a fair value. A comparison with peer companies in the cloud communications space, considering factors such as revenue growth, profitability, and market share, should also be considered. Investors need to carefully weigh the potential upside against the inherent risks before making an investment decision.

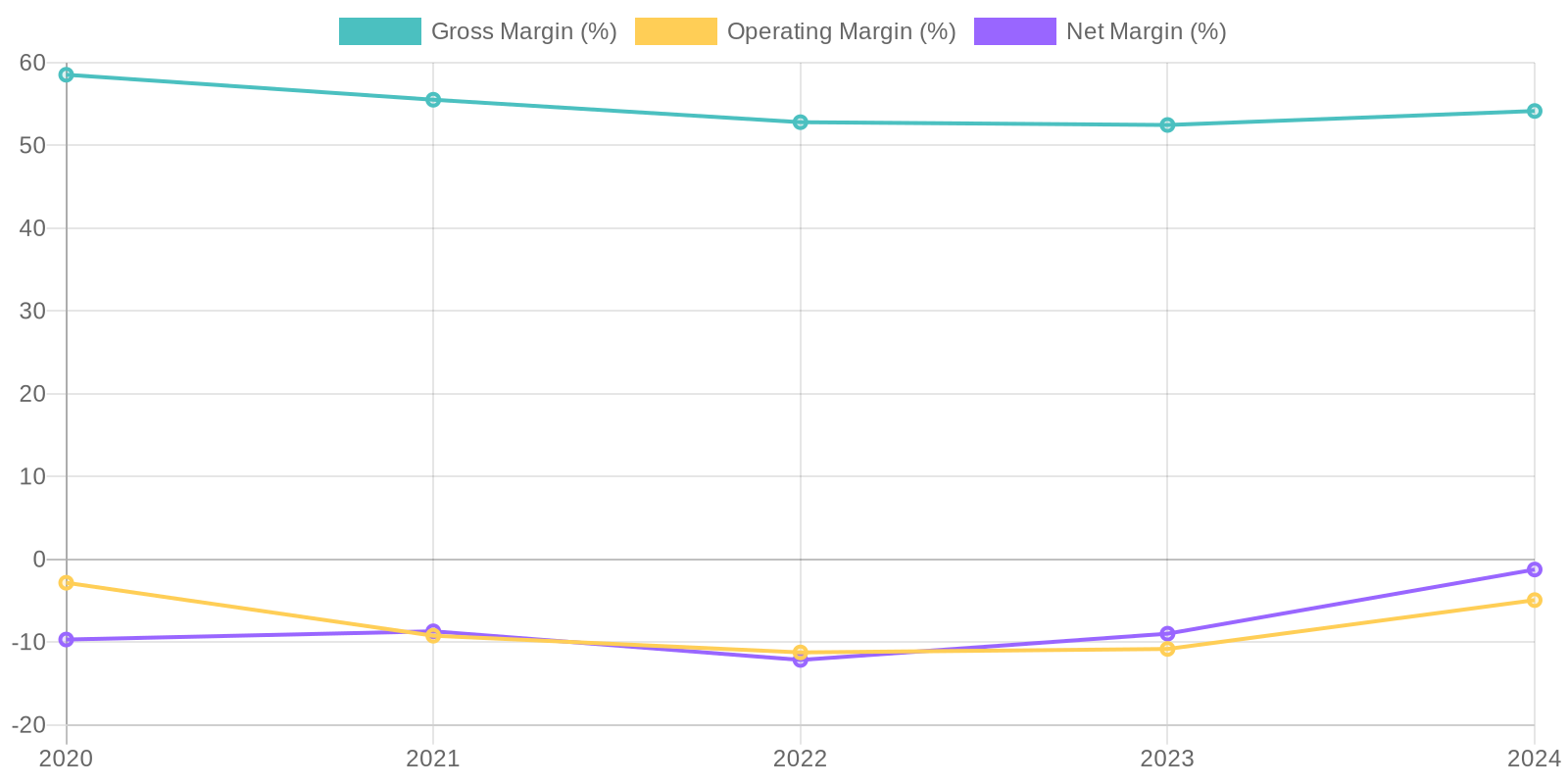

Given the company's negative net income in 2024, a traditional ROE calculation is not meaningful, as it would result in a negative value. Similarly, a standard ROIC calculation will also yield unfavorable figures due to the negative operating income. It is important to note that these profitability ratios are suppressed by continued net losses, signaling an inefficient use of capital to generate profits.

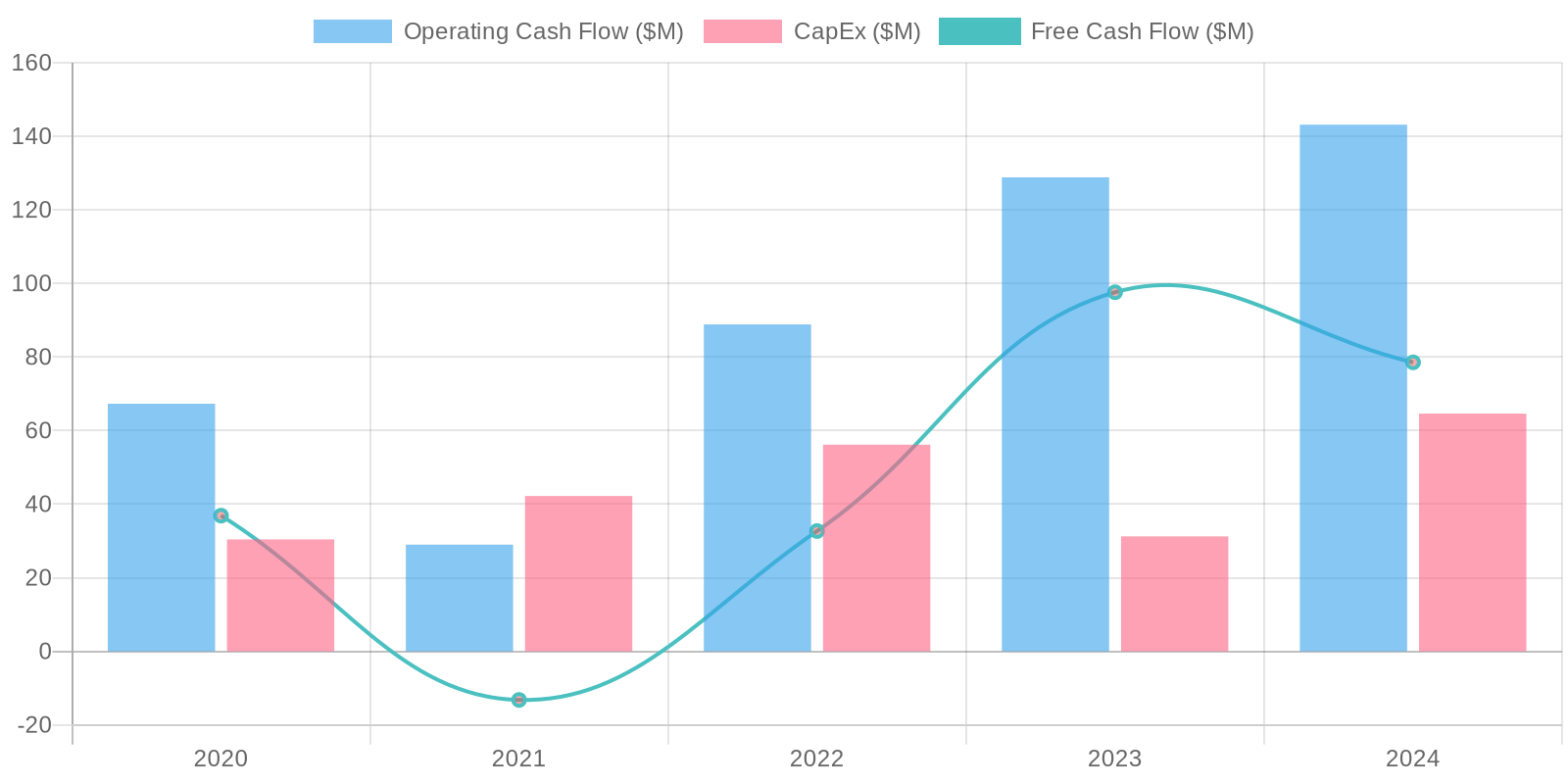

Given the company's negative net income in 2024, a traditional ROE calculation is not meaningful, as it would result in a negative value. Similarly, a standard ROIC calculation will also yield unfavorable figures due to the negative operating income. It is important to note that these profitability ratios are suppressed by continued net losses, signaling an inefficient use of capital to generate profits. The company exhibited a positive Free Cash Flow (FCF) of $78.56 million in 2024, marking a significant improvement compared to previous years where FCF was volatile. This positive cash generation is crucial for reinvestment and debt management. Capital expenditures have generally been consistent, representing a relatively small portion of overall revenue. However, a thorough examination of the sustainability of operating cash flow, along with trends in capital spending will provide a better understanding of the company's long term cash position.

The company exhibited a positive Free Cash Flow (FCF) of $78.56 million in 2024, marking a significant improvement compared to previous years where FCF was volatile. This positive cash generation is crucial for reinvestment and debt management. Capital expenditures have generally been consistent, representing a relatively small portion of overall revenue. However, a thorough examination of the sustainability of operating cash flow, along with trends in capital spending will provide a better understanding of the company's long term cash position.