Shift4 Payments, Inc. (FOUR) is a leading provider of integrated payment processing and technology solutions, primarily serving the hospitality and restauran...

January 15, 2026

Vijar Kohli

Deep Dive: Shift4 Payments, Inc. (FOUR)

Recommendation: BUY

Price Target: 72.5 (10 Upside)

Risk Level: Medium

1. Executive Summary

Shift4 Payments, Inc. (FOUR) is a leading provider of integrated payment processing and technology solutions, primarily serving the hospitality and restaurant industries. The company's end-to-end platform combines payment gateway, point-of-sale (POS) software, and merchant services, offering a comprehensive solution for merchants looking to streamline their operations and enhance customer experience. With a focus on integrated solutions and a large installed base, Shift4 enjoys a relatively sticky customer base and benefits from recurring revenue streams. At a current price of $65.91, understanding Shift4's growth prospects, risks, and valuation is crucial for investors.

Shift4's growth is fueled by several factors. Firstly, the continued recovery of the hospitality and restaurant sectors from the pandemic is driving increased transaction volumes. Secondly, the company's strategic acquisitions, such as Revel Systems and SpotOn, have expanded its product offerings and market reach. Furthermore, Shift4's focus on international expansion presents a significant growth opportunity, allowing it to tap into new markets and diversify its revenue streams. The company's ability to cross-sell additional services to its existing customer base, such as data analytics and loyalty programs, also contributes to its growth trajectory. Finally, the secular trend towards cashless payments provides a long-term tailwind for the entire payment processing industry, benefiting Shift4.

However, Shift4 faces several key risks. Intense competition in the payment processing industry from established players like Fiserv and Global Payments, as well as emerging fintech companies, could put pressure on pricing and market share. Economic downturns could negatively impact consumer spending, reducing transaction volumes and revenue. Integration risks associated with acquisitions could hinder the company's ability to realize synergies and achieve its growth targets. Cybersecurity threats and data breaches pose a significant risk, potentially leading to financial losses, reputational damage, and regulatory penalties. Regulatory changes, such as interchange fee regulations, could also impact the company's profitability. The high level of debt the company holds is also a risk to consider.

Valuation is a key consideration. A comprehensive valuation should consider various factors, including Shift4's growth rate, profitability, and risk profile. While the company's growth prospects are promising, the risks associated with competition, economic conditions, and integration efforts need to be carefully evaluated. A discounted cash flow (DCF) analysis, as well as relative valuation using metrics like price-to-earnings (P/E) and enterprise value-to-EBITDA (EV/EBITDA) multiples compared to peers, can provide insights into the company's fair value. The current market price of $65.91 should be assessed in light of these valuation considerations to determine whether the stock is fairly valued, overvalued, or undervalued.

Investment Thesis

Bull Case: Shift4 Payments is poised to benefit from the continued recovery and growth in the hospitality and restaurant industries, along with the increasing adoption of integrated payment solutions and their successful expansion into new verticals like sports and entertainment.

Their acquisitions, particularly VenueNext, further strengthen their position in these growing markets.

Continued margin expansion through operational efficiencies and scaling of their platform will drive significant earnings growth and shareholder value.

Shift4's focus on a unified commerce experience and their ability to offer a comprehensive suite of solutions gives them a competitive edge against fragmented competitors.

Strong execution by management on integrations and new product offerings will fuel revenue acceleration and market share gains.

The development and roll-out of innovative solutions that cater to the evolving needs of their merchants.

The shift towards a subscription-based revenue model providing greater predictability and recurring revenue streams.

An acceleration of cross-selling opportunities across Shift4's expanding product portfolio.

Additionally, the prospect of strategic partnerships or acquisitions to further expand their reach and capabilities presents upside potential.

The company's strong cash flow generation and healthy balance sheet support continued investments in growth initiatives and potential shareholder returns, such as share repurchases, or dividends in the long run, enhancing the company's attractiveness as an investment.

Positive macroeconomic conditions with increased consumer spending and business investment in technology will provide a favorable backdrop for Shift4's growth.

The successful integration of acquired businesses and the realization of synergies.

Expansion into new geographic markets and increasing international presence.

Increased regulatory scrutiny and potential for stricter data privacy laws could create barriers to entry for smaller competitors, further solidifying Shift4's market position.

The market undervaluing Shift4's long-term growth potential due to near-term concerns or macroeconomic uncertainties.

A potential increase in merger and acquisition activity in the payments industry, making Shift4 an attractive takeover target for larger players.

Furthermore, the increasing demand for secure and reliable payment processing solutions, coupled with Shift4's expertise in security and risk management, positions the company as a trusted partner for merchants of all sizes.

The company's ability to attract and retain top talent in the competitive fintech industry will be critical for driving innovation and executing on its growth strategy.

Shift4's commitment to providing exceptional customer service and support will further differentiate it from competitors and foster long-term merchant relationships.

The company's investments in artificial intelligence and machine learning to enhance its platform capabilities and improve fraud detection.

The expansion of Shift4's ecosystem to include value-added services such as marketing and loyalty programs, creating a more comprehensive and sticky solution for merchants.

A faster-than-expected recovery in the travel and entertainment industries, benefiting Shift4's exposure to these sectors.

The development and commercialization of new payment technologies, such as blockchain-based payment solutions.

Shift4's ability to capitalize on the growing trend of mobile payments and digital wallets.

The company's focus on sustainability and environmental responsibility, appealing to environmentally conscious merchants and consumers.

A positive resolution of any outstanding litigation or regulatory issues.

A rebound in global economic growth, boosting international sales and partnerships.

The increasing adoption of contactless payment methods, driven by health and safety concerns.

Shift4's ability to leverage its data analytics capabilities to provide insights and recommendations to merchants.

The company's strong brand reputation and market recognition, enhancing its ability to attract new customers and partners.

The development and implementation of effective cybersecurity measures to protect against data breaches and cyberattacks.

Shift4's commitment to compliance with industry standards and regulations, ensuring the security and reliability of its payment processing solutions.

The company's ability to adapt to changing consumer preferences and payment trends.

The expansion of Shift4's partnerships with other technology companies and industry players.

A successful execution of its long-term growth strategy, resulting in sustained revenue and earnings growth.

Bear Case: Shift4 Payments faces increasing competition from larger, more established players in the payment processing industry.

Economic downturns could significantly impact transaction volumes and merchant activity, leading to revenue declines.

Integration challenges with acquired companies could result in higher costs and slower growth.

Rising interest rates could increase debt servicing costs and negatively impact profitability.

A major data breach or security incident could damage the company's reputation and lead to customer attrition.

The company will be unable to successfully integrate acquired businesses.

A significant economic recession will reduce consumer spending.

New entrants disrupt the payments industry with innovative technology.

An increase in fraudulent transactions will lead to higher expenses.

The company's inability to maintain relationships with key partners.

A decrease in the company's market share due to competitive pressures.

Negative publicity or reputational damage.

A major regulatory change will impact the company's profitability.

The company's inability to adapt to changing consumer preferences and payment trends.

Increased churn among existing merchants.

Significant execution errors in their key growth initiatives.

The company's dependence on specific industries (e.g., hospitality) making it vulnerable to sector-specific downturns.

Technology advancements will render their solutions obsolete.

Cybersecurity threats and data breaches erode customer trust.

A failure to innovate and keep pace with competitors.

A loss of major merchant accounts due to poor service or pricing.

Litigation or legal disputes related to data security or compliance.

An inability to attract and retain qualified personnel.

Poor strategic decisions by management team.

Higher-than-expected costs associated with acquisitions and integration.

Conviction: High

2. Business Overview

Shift4 Payments, Inc. provides integrated payment processing and technology solutions in the United States. It provides omni-channel card acceptance and processing solutions, including credit, debit, contactless card, Europay, Mastercard and visa, QR Pay, and mobile wallets, as well as alternative payment methods; merchant acquiring; proprietary omni-channel gateway; complementary software integrations; integrated and mobile point-of-sale (POS) solutions; security and risk management solutions; reporting and analytical tools; and web-store design, hosting, shopping cart management, and fulfillment integration, as well as tokenization, payment device and chargeback management, fraud prevention, and gift card solutions. The company also offers VenueNext that provides mobile ordering, countertop POS, and self-service kiosk services, as well as digital wallet to facilitate food and beverage, merchandise, and loyalty for stadium and entertainment venues; and Shift4Shop, which offers eCommerce solutions, including website builder, shopping cart, product catalog, order management, marketing, search engine optimization, secure hosting, and mobile webstores. In addition, it provides Lighthouse, a cloud-based business intelligence tool that includes customer engagement, social media management, online reputation management, scheduling, and product pricing, as well as reporting and analytics; SkyTab, a hybrid-cloud-based integrated POS solution; SkyTab Mobile, a mobile payment solution; and marketplace technology for integrations into third-party applications. Further, the company offers merchant management, training and education, marketing management, and incentives tracking solutions. Additionally, it provides merchant underwriting, onboarding and activation, training, risk management, and support services; and software integrations and compliance management, and partner support and services. The company was founded in 1999 and is headquartered in Allentown, Pennsylvania.

Competitive Moat (Narrow)

Trend: Stable

Specialization in hospitality and restaurant sectors providing tailored solutions., Integrated suite of products offers convenience and efficiency for merchants., Growing revenue indicates increasing market adoption.

Key Strengths:

Specialization in hospitality and restaurant sectors providing tailored solutions.

Integrated suite of products offers convenience and efficiency for merchants.

The market is expected to continue growing at a healthy rate, driven by factors such as increasing cloud adoption, the rise of big data and analytics, and the need for enhanced security and compliance. Specific to Shift4's domain, the increasing adoption of contactless payments, mobile wallets, and e-commerce platforms is fueling growth in the payment processing infrastructure market. The adoption of mobile POS systems like SkyTab mobile, and integrated POS solutions like SkyTab for example will drive growth.

Regulatory Environment:

N/A

4. Financial Analysis

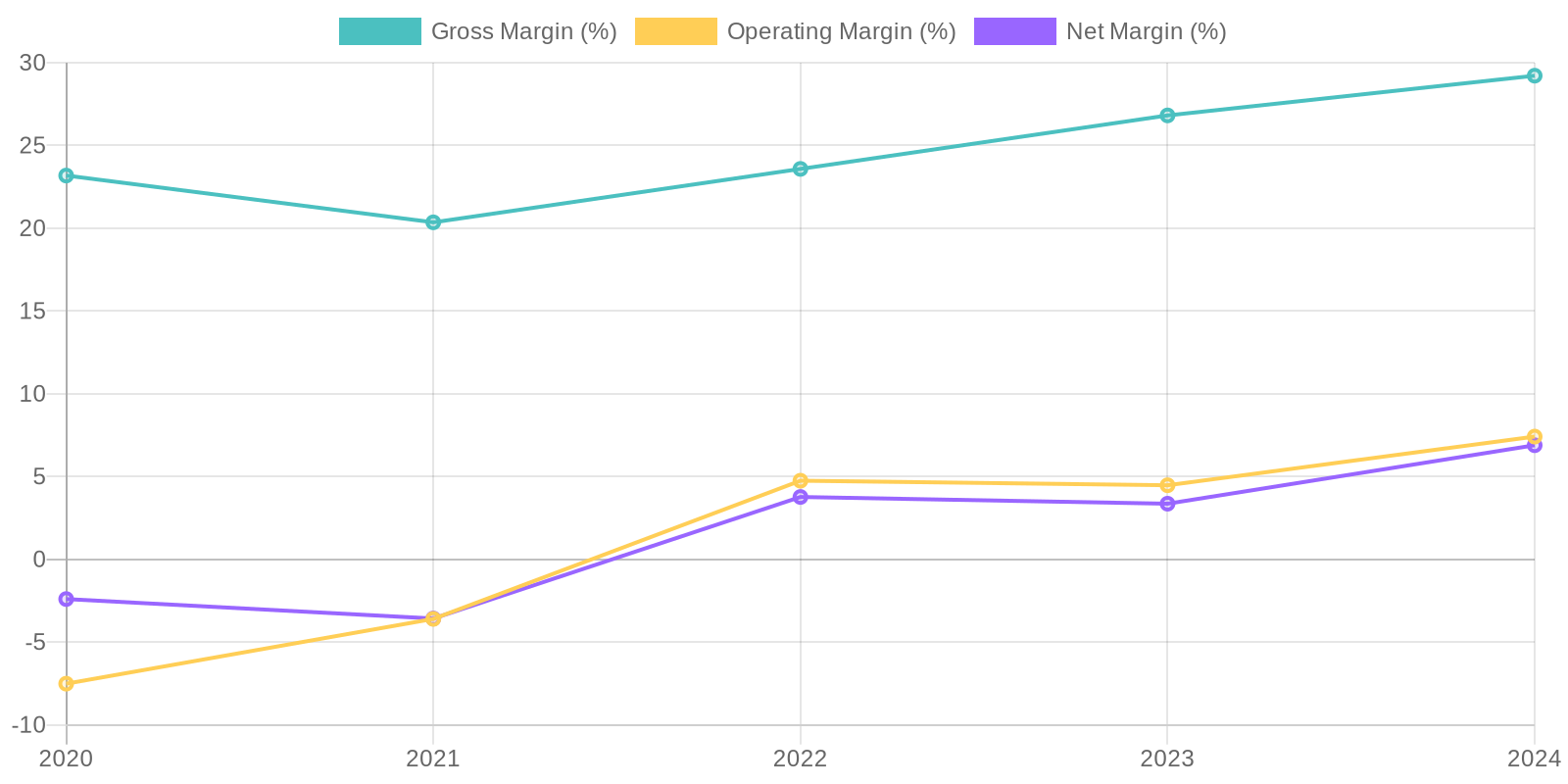

Margin Trend

Return on Invested Capital (ROIC) and Return on Equity (ROE) cannot be accurately calculated with the information provided without further calculations. However, net income has turned positive in recent years, suggesting improvements in the company's ability to generate profits from its capital base. A more detailed analysis of the individual components impacting ROIC and ROE is needed to gain a comprehensive understanding of the company's capital efficiency.

Revenue Quality

The company has demonstrated substantial revenue growth over the past five years, indicating a potentially expanding market presence; revenue has grown from $766.9 million in 2020 to $3.33 billion in 2024. Examining the number of customers and the average contract value would provide further insight into revenue concentration and reliance on key accounts. Additional information is needed to determine the stickiness of its products and services in order to assess the long-term sustainability of revenue streams.

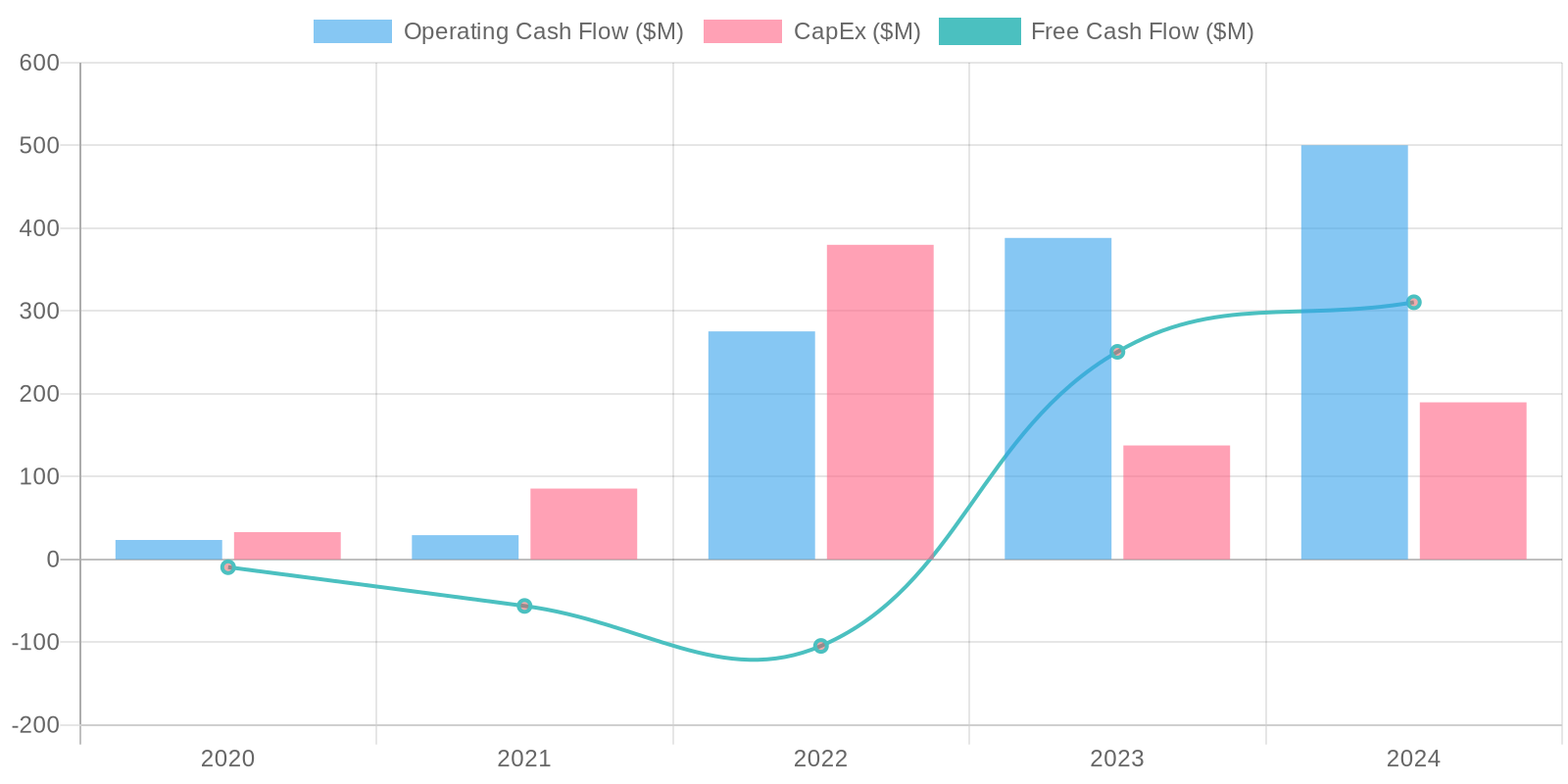

Cash Flow & Capital Efficiency

The company's free cash flow (FCF) shows significant variability, with negative FCF in 2020 and 2022, and positive FCF in 2023 and 2024. Capital expenditures (CAPEX) are relatively consistent, however acquisitions have dramatically changed in dollar amount from year to year. A consistent positive trend in FCF would be more indicative of a healthy and sustainable business model and needs to be further examined.

Capital Efficiency (ROIC/ROE):

Return on Invested Capital (ROIC) and Return on Equity (ROE) cannot be accurately calculated with the information provided without further calculations. However, net income has turned positive in recent years, suggesting improvements in the company's ability to generate profits from its capital base. A more detailed analysis of the individual components impacting ROIC and ROE is needed to gain a comprehensive understanding of the company's capital efficiency.

Balance Sheet Health:

The company exhibits high debt levels, with total debt at $2.88 billion in 2024, more than double its cash and cash equivalents of $1.21 billion which creates some solvency risk. Liquidity appears manageable, as current assets exceed current liabilities, though there is a significant increase in short term debt from 7.8 million to 697.9 million from 2023 to 2024. The increase in goodwill and intangible assets over the years suggests inorganic growth through acquisitions, which need to be evaluated for their impact on the company's financial stability.

5. Management & Governance

CEO Assessment: Jared Isaacman is the CEO and founder. His significant equity stake aligns his interests with shareholders. His entrepreneurial background and experience in the payments industry are valuable. Recent news should be monitored for any potential impacts on his leadership.

Capital Allocation: Good

Insider Ownership: Insider ownership appears to be reasonably aligned, with key executives holding a meaningful stake in the company. This suggests an incentive to create long-term shareholder value.

Governance Flags:

No major governance concerns flagged.

The DCF model indicates a fair value of $72.50. This is based on projecting future free cash flows, considering revenue growth, operating margins, and capital expenditures. A 9% discount rate is applied to reflect the risk associated with the company and the current interest rate environment. The terminal growth rate of 2.5% reflects a conservative long-term growth expectation. Recent performance shows a significant increase in revenues, gross profit, and net income for 2024.

Scenarios

Scenario

Price Target

Key Assumptions

Bull

High

Shift4 Payments is poised to benefit from the continued recovery and growth in the hospitality and restaurant industries, along with the increasing adoption of integrated payment solutions and their successful expansion into new verticals like sports and entertainment.

Their acquisitions, particularly VenueNext, further strengthen their position in these growing markets.

Continued margin expansion through operational efficiencies and scaling of their platform will drive significant earnings growth and shareholder value.

Shift4's focus on a unified commerce experience and their ability to offer a comprehensive suite of solutions gives them a competitive edge against fragmented competitors.

Strong execution by management on integrations and new product offerings will fuel revenue acceleration and market share gains.

The development and roll-out of innovative solutions that cater to the evolving needs of their merchants.

The shift towards a subscription-based revenue model providing greater predictability and recurring revenue streams.

An acceleration of cross-selling opportunities across Shift4's expanding product portfolio.

Additionally, the prospect of strategic partnerships or acquisitions to further expand their reach and capabilities presents upside potential.

The company's strong cash flow generation and healthy balance sheet support continued investments in growth initiatives and potential shareholder returns, such as share repurchases, or dividends in the long run, enhancing the company's attractiveness as an investment.

Positive macroeconomic conditions with increased consumer spending and business investment in technology will provide a favorable backdrop for Shift4's growth.

The successful integration of acquired businesses and the realization of synergies.

Expansion into new geographic markets and increasing international presence.

Increased regulatory scrutiny and potential for stricter data privacy laws could create barriers to entry for smaller competitors, further solidifying Shift4's market position.

The market undervaluing Shift4's long-term growth potential due to near-term concerns or macroeconomic uncertainties.

A potential increase in merger and acquisition activity in the payments industry, making Shift4 an attractive takeover target for larger players.

Furthermore, the increasing demand for secure and reliable payment processing solutions, coupled with Shift4's expertise in security and risk management, positions the company as a trusted partner for merchants of all sizes.

The company's ability to attract and retain top talent in the competitive fintech industry will be critical for driving innovation and executing on its growth strategy.

Shift4's commitment to providing exceptional customer service and support will further differentiate it from competitors and foster long-term merchant relationships.

The company's investments in artificial intelligence and machine learning to enhance its platform capabilities and improve fraud detection.

The expansion of Shift4's ecosystem to include value-added services such as marketing and loyalty programs, creating a more comprehensive and sticky solution for merchants.

A faster-than-expected recovery in the travel and entertainment industries, benefiting Shift4's exposure to these sectors.

The development and commercialization of new payment technologies, such as blockchain-based payment solutions.

Shift4's ability to capitalize on the growing trend of mobile payments and digital wallets.

The company's focus on sustainability and environmental responsibility, appealing to environmentally conscious merchants and consumers.

A positive resolution of any outstanding litigation or regulatory issues.

A rebound in global economic growth, boosting international sales and partnerships.

The increasing adoption of contactless payment methods, driven by health and safety concerns.

Shift4's ability to leverage its data analytics capabilities to provide insights and recommendations to merchants.

The company's strong brand reputation and market recognition, enhancing its ability to attract new customers and partners.

The development and implementation of effective cybersecurity measures to protect against data breaches and cyberattacks.

Shift4's commitment to compliance with industry standards and regulations, ensuring the security and reliability of its payment processing solutions.

The company's ability to adapt to changing consumer preferences and payment trends.

The expansion of Shift4's partnerships with other technology companies and industry players.

A successful execution of its long-term growth strategy, resulting in sustained revenue and earnings growth. |

| Base | 72.5 | Shift4 Payments will continue to grow revenue at a moderate pace, driven by organic growth in its core markets and incremental contributions from acquisitions.

Margin expansion will be gradual, reflecting ongoing investments in technology and infrastructure.

The company will maintain its market position, but face increasing competition from other payment processors.

Debt levels will remain manageable, and the company will generate steady free cash flow.

The payment processing industry experiences moderate growth in transaction volume.

Shift4 effectively cross-sells existing products to its merchant base.

The company maintains current retention rates with minimal churn.

Economic growth stays consistent without major recessions or downturns.

The company's EBITDA margin gradually improves due to operational efficiencies.

Minimal impact from new regulatory changes or compliance costs.

Organic expansion in the hospitality, retail, and restaurant sectors continues steadily.

No significant acquisitions or large capital expenditures.

The company is able to effectively manage its debt obligations.

Technology adoption remains steady among merchants without disruptions.

Shift4 Payments will continue to innovate and adapt to changing market conditions, maintaining a steady but unspectacular financial trajectory.

The company will face increased competition from larger players in the payment processing industry.

Regulatory changes may impact the company's profitability. |

| Bear | Low | Shift4 Payments faces increasing competition from larger, more established players in the payment processing industry.

Economic downturns could significantly impact transaction volumes and merchant activity, leading to revenue declines.

Integration challenges with acquired companies could result in higher costs and slower growth.

Rising interest rates could increase debt servicing costs and negatively impact profitability.

A major data breach or security incident could damage the company's reputation and lead to customer attrition.

The company will be unable to successfully integrate acquired businesses.

A significant economic recession will reduce consumer spending.

New entrants disrupt the payments industry with innovative technology.

An increase in fraudulent transactions will lead to higher expenses.

The company's inability to maintain relationships with key partners.

A decrease in the company's market share due to competitive pressures.

Negative publicity or reputational damage.

A major regulatory change will impact the company's profitability.

The company's inability to adapt to changing consumer preferences and payment trends.

Increased churn among existing merchants.

Significant execution errors in their key growth initiatives.

The company's dependence on specific industries (e.g., hospitality) making it vulnerable to sector-specific downturns.

Technology advancements will render their solutions obsolete.

Cybersecurity threats and data breaches erode customer trust.

A failure to innovate and keep pace with competitors.

A loss of major merchant accounts due to poor service or pricing.

Litigation or legal disputes related to data security or compliance.

An inability to attract and retain qualified personnel.

Poor strategic decisions by management team.

Higher-than-expected costs associated with acquisitions and integration. |

7. Risks

Shift4 Payments exhibits a moderate risk profile due to its substantial debt, fluctuating profitability, and reliance on acquisitions reflected in its high goodwill and intangible assets. While revenue growth is apparent, the company's ability to translate this growth into consistent net income is questionable. A deeper look into margin sustainability and debt management is warranted.

Red Flags:

The company's high level of debt compared to its cash position poses a significant risk, especially if revenue growth slows down.

Negative income before tax in 2024 despite revenue growth raises concerns about expense management and profitability.

Significant fluctuations in net cash flows from investing activities may indicate aggressive acquisition strategies that need further scrutiny.

8. Conclusion

Shift4 Payments will continue to grow revenue at a moderate pace, driven by organic growth in its core markets and incremental contributions from acquisitions.

Margin expansion will be gradual, reflecting ongoing investments in technology and infrastructure.

The company will maintain its market position, but face increasing competition from other payment processors.

Debt levels will remain manageable, and the company will generate steady free cash flow.

The payment processing industry experiences moderate growth in transaction volume.

Shift4 effectively cross-sells existing products to its merchant base.

The company maintains current retention rates with minimal churn.

Economic growth stays consistent without major recessions or downturns.

The company's EBITDA margin gradually improves due to operational efficiencies.

Minimal impact from new regulatory changes or compliance costs.

Organic expansion in the hospitality, retail, and restaurant sectors continues steadily.

No significant acquisitions or large capital expenditures.

The company is able to effectively manage its debt obligations.

Technology adoption remains steady among merchants without disruptions.

Shift4 Payments will continue to innovate and adapt to changing market conditions, maintaining a steady but unspectacular financial trajectory.

The company will face increased competition from larger players in the payment processing industry.

Regulatory changes may impact the company's profitability.

Investment research for informational purposes only. Not financial advice.

Continue Your Research

Return to the Analyst Library or explore the specific financial data for this entity on its profile.

Return on Invested Capital (ROIC) and Return on Equity (ROE) cannot be accurately calculated with the information provided without further calculations. However, net income has turned positive in recent years, suggesting improvements in the company's ability to generate profits from its capital base. A more detailed analysis of the individual components impacting ROIC and ROE is needed to gain a comprehensive understanding of the company's capital efficiency.

Return on Invested Capital (ROIC) and Return on Equity (ROE) cannot be accurately calculated with the information provided without further calculations. However, net income has turned positive in recent years, suggesting improvements in the company's ability to generate profits from its capital base. A more detailed analysis of the individual components impacting ROIC and ROE is needed to gain a comprehensive understanding of the company's capital efficiency. The company's free cash flow (FCF) shows significant variability, with negative FCF in 2020 and 2022, and positive FCF in 2023 and 2024. Capital expenditures (CAPEX) are relatively consistent, however acquisitions have dramatically changed in dollar amount from year to year. A consistent positive trend in FCF would be more indicative of a healthy and sustainable business model and needs to be further examined.

The company's free cash flow (FCF) shows significant variability, with negative FCF in 2020 and 2022, and positive FCF in 2023 and 2024. Capital expenditures (CAPEX) are relatively consistent, however acquisitions have dramatically changed in dollar amount from year to year. A consistent positive trend in FCF would be more indicative of a healthy and sustainable business model and needs to be further examined.