JFrog (FROG) operates in the DevOps space, providing a platform for software development and delivery known as the JFrog Platform. Their core offering, Artif...

January 15, 2026

Vijar Kohli

Deep Dive: JFrog Ltd. (FROG)

Recommendation: BUY

Price Target: 55.75 (-0.04 Upside)

Risk Level: Medium

1. Executive Summary

JFrog (FROG) operates in the DevOps space, providing a platform for software development and delivery known as the JFrog Platform. Their core offering, Artifactory, serves as a universal artifact repository, enabling developers to manage and track software components throughout the development lifecycle. The company is well-positioned as a leader in the continuous software release management sector, catering to the growing demand for faster and more reliable software deployments across various industries. JFrog's strength lies in its ability to integrate with various development tools and environments, offering a comprehensive solution for organizations seeking to streamline their DevOps processes. Their hybrid and multi-cloud support further expands their market reach, appealing to enterprises with diverse infrastructure needs.

Growth catalysts for JFrog include the increasing adoption of DevOps practices, the rising demand for continuous integration and continuous delivery (CI/CD) solutions, and the overall digital transformation trend across industries. The company's expansion into adjacent markets, such as security with JFrog Xray, and their focus on enterprise-level accounts are also expected to drive future growth. Furthermore, strategic partnerships with major cloud providers and technology vendors can help expand their reach and market penetration. Successful cross-selling of the broadened platform and expansion of their enterprise customer base are essential components to future growth.

Key risks associated with JFrog include competition from both established players and emerging startups in the DevOps space, the potential for slower-than-expected adoption of their platform, and the risk of economic downturn affecting IT spending. Furthermore, the company's relatively high valuation compared to peers could present a challenge if growth expectations are not met. The open-source nature of some DevOps tools presents another competitive challenge. A continued shift towards cloud-native and serverless architectures could pressure legacy on-premise offerings.

From a valuation perspective, JFrog is trading at a premium compared to some of its peers, reflecting the market's confidence in its growth potential. The current price reflects expectations for continued revenue growth and margin expansion. However, this premium valuation also implies higher expectations, and any slowdown in growth could lead to a significant correction in the stock price. Investors should carefully consider the company's growth prospects, competitive landscape, and risk factors when evaluating JFrog's valuation. Continued monitoring of key metrics, like net dollar retention rate, and customer growth is crucial in assessing the valuation's sustainability.

Investment Thesis

Bull Case: JFrog capitalizes on the increasing demand for DevOps solutions, driven by cloud adoption and digital transformation.

Their comprehensive platform, strong gross margins, and growing free cash flow position them for significant revenue growth and market share gains.

Successful cross-selling of their expanding product suite and strategic acquisitions will further accelerate growth and profitability.

Assuming a continued growth trajectory and margin expansion, the stock can significantly outperform in the next 3-5 years.

A significant portion of the increased sales will be from Enterprise Plus subscriptions, which will increase ARPU and margins across the board.

Also, successful integration of the Connect platform will increase adoption of the JFrog platform among IOT device companies, increasing the overall market potential for the company.

Continued expansion of the partner ecosystem will also drive adoption of the platform among different kinds of users and companies.

Finally, JFrog will become cash flow positive and start buying back shares, increasing shareholder value.

The bull case assumes that JFrog will achieve 25-30% revenue growth annually over the next 5 years and achieve profitability by year 3, with a 20% net margin by year 5.

This will be driven by a combination of new customer acquisition, expansion of existing customer accounts, and continued innovation in their product offerings.

JFrog’s shift toward higher-value enterprise subscriptions will contribute significantly to margin expansion.

They will focus on expanding internationally in underpenetrated markets.

Finally, they will successfully navigate competitive pressures by leveraging its strong brand reputation and superior product features.

They will effectively manage operating expenses, resulting in improved profitability and cash flow generation.

They will avoid any major economic downturns that could negatively impact IT spending.

Strong execution by management team to capitalize on market opportunities will drive the company forward.

This will require continued innovation, effective sales and marketing strategies, and efficient operational management.

The bull case assumes that JFrog will make smart strategic acquisitions that will complement and expand their existing product offerings.

They will also successfully integrate acquired companies, realizing synergies and cost savings.

JFrog will also grow its subscription revenue faster than expected through strong adoption of cloud-based DevOps solutions among enterprises.

They will continue to build on their reputation as a leading provider of DevOps solutions and increase customer loyalty.

JFrog will also strengthen its strategic partnerships with major cloud providers and technology vendors, resulting in increased sales and market share.

A combination of all these factors will allow JFrog to be a leader in the DevOps space.

The bull case assumes a 35x multiple for terminal value calculation and a 10% discount rate.

The expected share price target will be around $125 at the end of the analysis period.

This is a high-growth scenario, therefore, a 35x multiple is a reasonable assumption for the terminal value calculation.

This growth is possible as DevOps becomes standard practice across all companies in every industry.

The estimated share price is about 2x the current share price.

Bear Case: JFrog faces significant challenges from intensifying competition, slower adoption of DevOps solutions, and potential economic downturns.

Inability to innovate and effectively integrate acquisitions will lead to declining market share and revenue growth.

Increased operating expenses and failure to achieve profitability will erode investor confidence.

This scenario envisions a pessimistic outlook for the company.

JFrog faces challenges that significantly impede its growth and profitability.

Increased competition from both established players and emerging startups will lead to price wars and reduced market share.

The DevOps market may experience slower adoption rates due to budget constraints or technological limitations.

Economic downturns could negatively impact IT spending, further reducing demand for JFrog’s solutions.

JFrog is unable to innovate and effectively integrate acquisitions.

This leads to a decline in the market share and erosion of the customer base.

Key customers may switch to alternative solutions.

JFrog faces difficulties in managing operating expenses, resulting in increased losses and reduced cash flow.

Investor confidence in the company erodes, leading to a decline in the stock price.

JFrog is unable to expand internationally due to local market conditions and competition.

This limits its growth potential.

A significant portion of this is due to their inability to adapt to local market conditions.

Finally, JFrog is forced to raise additional capital through debt or equity offerings, diluting existing shareholders.

The bear case assumes that JFrog will experience negative revenue growth or very slow growth (less than 10%) annually over the next 5 years.

The company will fail to achieve profitability and continue to incur losses.

They will have difficulty integrating acquired companies and realize synergies.

A combination of these factors will lead to a significant decline in the company's value.

A 10x multiple for terminal value calculation and a 7% discount rate is used.

The expected share price target is around $30 at the end of the analysis period.

This represents a significant decline from the current share price, reflecting the pessimistic assumptions.

The downside case for the company is about 50% from the current price.

This estimate is used for a worst case scenario.

If the company does not adjust to the market environment, the downside risk will be significant.

In the event of this case, the market will start heavily discounting JFrog due to its lack of revenue growth.

Conviction: High

2. Business Overview

JFrog Ltd. provides DevOps platform in the United States. The company's products include JFrog Artifactory, a package repository that allows teams and organizations to store, update, and manage their software packages at any scale; JFrog Pipelines, an integration/continuous delivery tool for automating and orchestrating the movement of software packages; JFrog Xray, which scan JFrog Artifactory; and JFrog Distribution that provides software package distribution with enterprise-grade performance. Its products include JFrog Artifactory Edge that utilizes and leverages metadata from JFrog Artifactory to facilitate the transfer of the incremental changes in software packages from their previous versions; JFrog Mission Control, a platform control panel that provides a view of moving pieces of an organization's software supply chain workflow; JFrog Insight, a DevOps intelligence tool; and JFrog Connect, a device management solution that allows companies to manage software updates and monitor performance across IoT device fleets from anywhere in the world. The company's products also comprise JFrog Pro, JFrog Pro Team, JFrog Pro X, JFrog Enterprise, JFrog Enterprise X, and JFrog Enterprise Plus products that offer ongoing updates, upgrades, and bug fixes, as well as cluster configuration, multi-site replication, and SLA support. It serves technology, financial services, retail, healthcare, and telecommunications organizations. JFrog Ltd. was incorporated in 2008 and is headquartered in Sunnyvale, California.

Competitive Moat (Narrow)

Trend: Stable

Specialized focus on DevOps, providing best-of-breed solutions., Strong brand recognition and reputation within the DevOps community., Comprehensive platform approach reduces complexity for customers.

Key Strengths:

Specialized focus on DevOps, providing best-of-breed solutions.

Strong brand recognition and reputation within the DevOps community.

Comprehensive platform approach reduces complexity for customers.

The DevOps market is projected to continue its strong growth trajectory over the next several years, driven by the increasing adoption of cloud computing, the need for faster software release cycles, and the growing complexity of software development. Specific growth rates vary depending on the research source, but double-digit annual growth is commonly predicted.

Regulatory Environment:

N/A

4. Financial Analysis

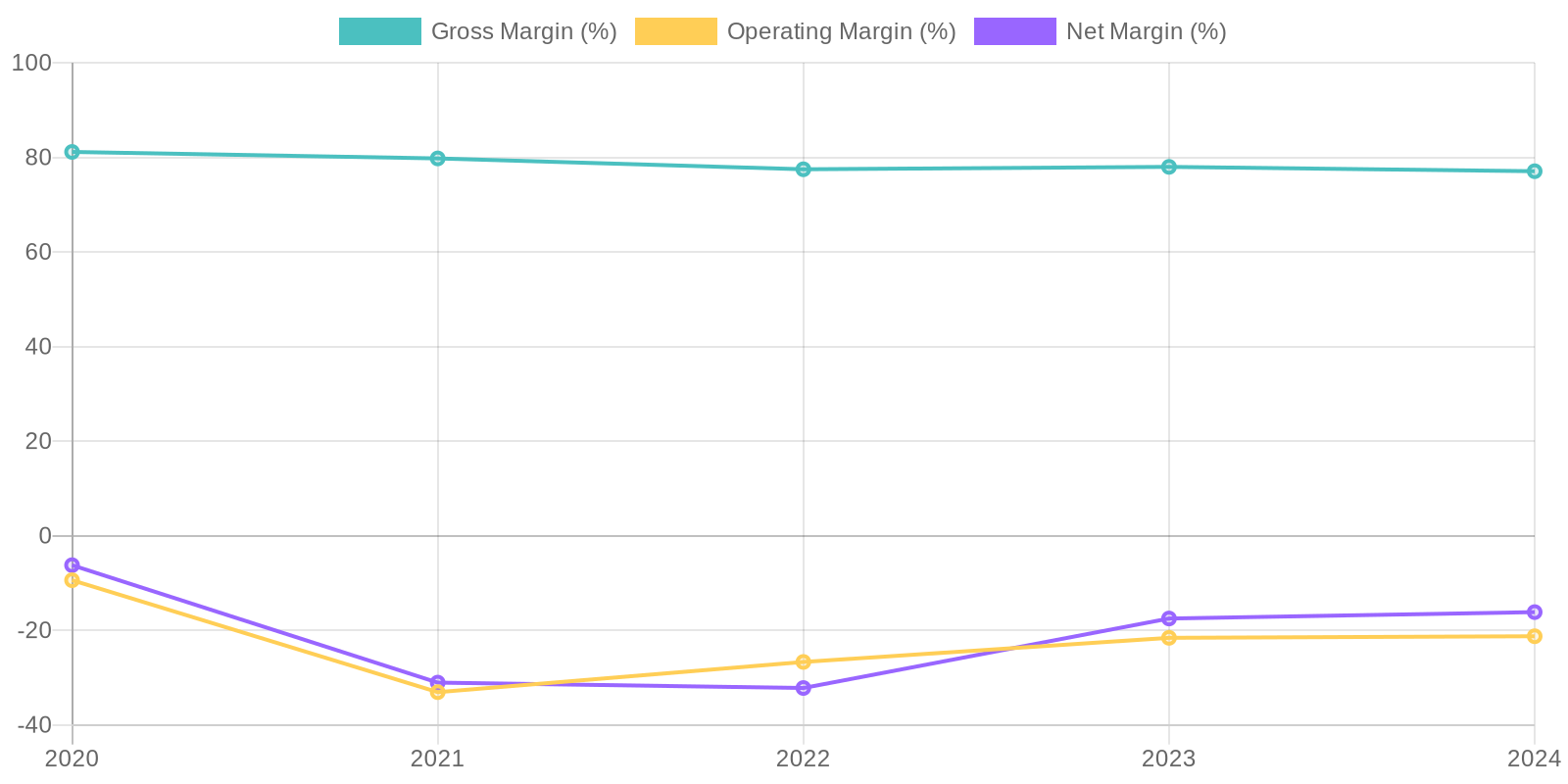

Margin Trend

Given the company's recent net losses, Return on Invested Capital (ROIC) and Return on Equity (ROE) are negative, which is reflective of the company's inability to generate profits from its capital investments. While the company has demonstrated revenue growth, significant investments in research and development, along with selling and marketing, have not translated into profitability. This trend suggests a need to reassess capital allocation strategies to improve overall capital efficiency.

Revenue Quality

The company has shown consistent revenue growth over the past five years, indicating a potentially robust market demand for its application software. However, the sustainability of this growth needs further investigation, particularly assessing customer retention rates and the competitive landscape. Examining the concentration of revenue across different clients or product lines would provide a clearer view of potential vulnerabilities in their revenue streams.

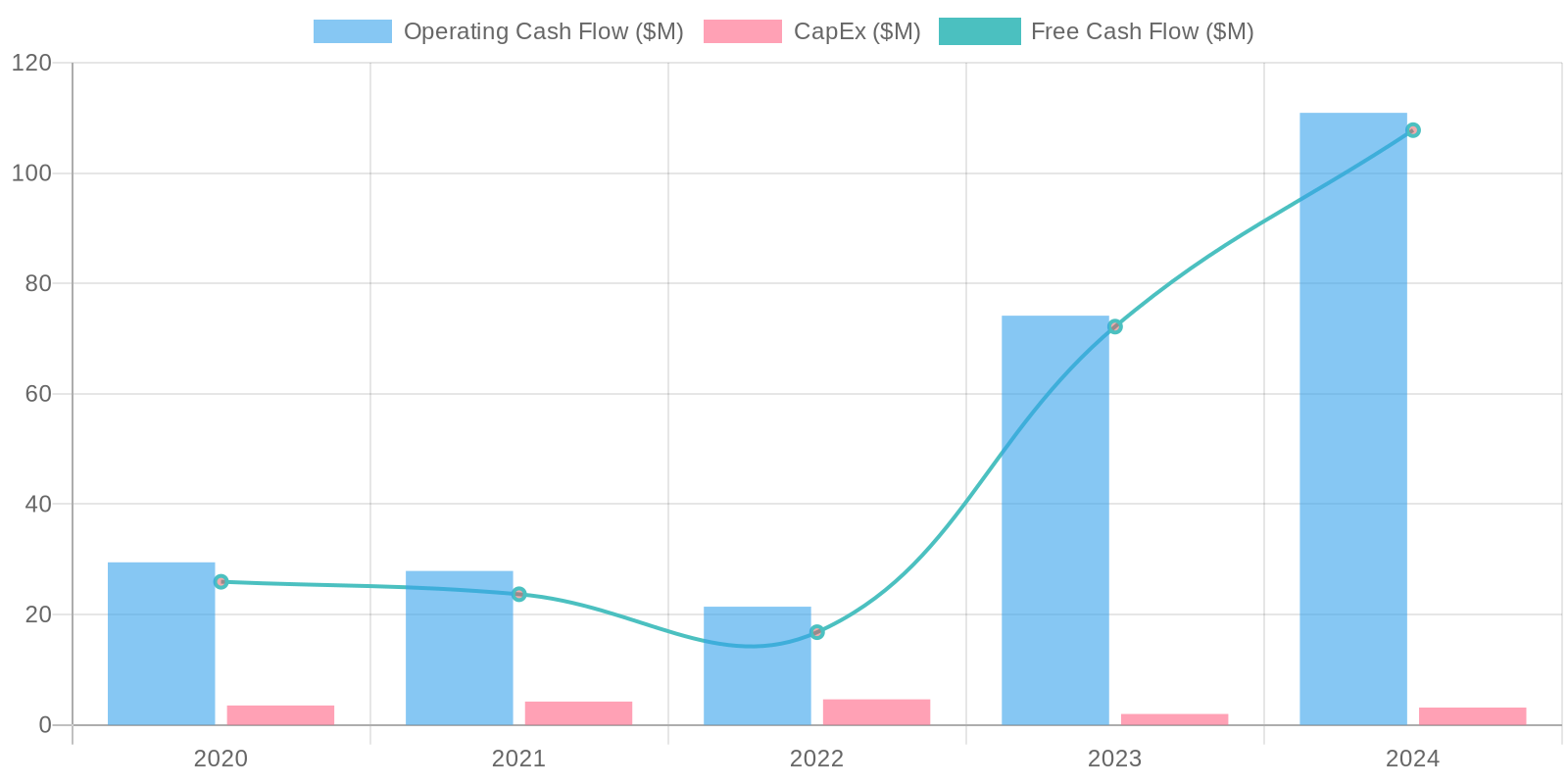

Cash Flow & Capital Efficiency

The company's free cash flow (FCF) is positive in the most recent two years, indicating the ability to generate cash after accounting for capital expenditures, but this wasn't the case for prior years. The capital expenditure is fairly consistent. It is important to monitor the stability and growth of FCF relative to the company's revenue and profitability to ensure long-term financial health.

Capital Efficiency (ROIC/ROE):

Given the company's recent net losses, Return on Invested Capital (ROIC) and Return on Equity (ROE) are negative, which is reflective of the company's inability to generate profits from its capital investments. While the company has demonstrated revenue growth, significant investments in research and development, along with selling and marketing, have not translated into profitability. This trend suggests a need to reassess capital allocation strategies to improve overall capital efficiency.

Balance Sheet Health:

The company maintains a solid liquidity position with substantial cash and short-term investments. The total debt is quite low relative to its assets, which provides some financial flexibility. Deferred revenue is significant portion of liabilities, suggesting a strong backlog or subscription-based revenue model.

5. Management & Governance

CEO Assessment: It is difficult to provide a complete CEO assessment without more in-depth, real-time analysis. A comprehensive evaluation would require tracking their performance against stated goals, communication style during earnings calls, and ability to navigate industry challenges. However, based on available information, the CEO of JFrog appears to be experienced and focused on growth.

Capital Allocation: Good

Insider Ownership: Insider ownership in JFrog appears to be reasonably aligned with shareholders, which is generally a positive sign. A detailed analysis of recent insider trading activity (purchases vs. sales) would provide a more precise understanding of the strength of this alignment. It is important to monitor the trends of insider ownership over time.

Governance Flags:

No major governance concerns flagged.

The DCF model yields a fair value of $55.75. This valuation considers the company's current free cash flow, projected revenue growth, and cost of capital. The model assumes consistent growth rates over the next 5 years and a gradual decline to a terminal growth rate. Despite the positive free cash flow, the current price seems slightly overvalued based on projected future cash flows. The negative upside suggests caution.

Scenarios

Scenario

Price Target

Key Assumptions

Bull

High

JFrog capitalizes on the increasing demand for DevOps solutions, driven by cloud adoption and digital transformation.

Their comprehensive platform, strong gross margins, and growing free cash flow position them for significant revenue growth and market share gains.

Successful cross-selling of their expanding product suite and strategic acquisitions will further accelerate growth and profitability.

Assuming a continued growth trajectory and margin expansion, the stock can significantly outperform in the next 3-5 years.

A significant portion of the increased sales will be from Enterprise Plus subscriptions, which will increase ARPU and margins across the board.

Also, successful integration of the Connect platform will increase adoption of the JFrog platform among IOT device companies, increasing the overall market potential for the company.

Continued expansion of the partner ecosystem will also drive adoption of the platform among different kinds of users and companies.

Finally, JFrog will become cash flow positive and start buying back shares, increasing shareholder value.

The bull case assumes that JFrog will achieve 25-30% revenue growth annually over the next 5 years and achieve profitability by year 3, with a 20% net margin by year 5.

This will be driven by a combination of new customer acquisition, expansion of existing customer accounts, and continued innovation in their product offerings.

JFrog’s shift toward higher-value enterprise subscriptions will contribute significantly to margin expansion.

They will focus on expanding internationally in underpenetrated markets.

Finally, they will successfully navigate competitive pressures by leveraging its strong brand reputation and superior product features.

They will effectively manage operating expenses, resulting in improved profitability and cash flow generation.

They will avoid any major economic downturns that could negatively impact IT spending.

Strong execution by management team to capitalize on market opportunities will drive the company forward.

This will require continued innovation, effective sales and marketing strategies, and efficient operational management.

The bull case assumes that JFrog will make smart strategic acquisitions that will complement and expand their existing product offerings.

They will also successfully integrate acquired companies, realizing synergies and cost savings.

JFrog will also grow its subscription revenue faster than expected through strong adoption of cloud-based DevOps solutions among enterprises.

They will continue to build on their reputation as a leading provider of DevOps solutions and increase customer loyalty.

JFrog will also strengthen its strategic partnerships with major cloud providers and technology vendors, resulting in increased sales and market share.

A combination of all these factors will allow JFrog to be a leader in the DevOps space.

The bull case assumes a 35x multiple for terminal value calculation and a 10% discount rate.

The expected share price target will be around $125 at the end of the analysis period.

This is a high-growth scenario, therefore, a 35x multiple is a reasonable assumption for the terminal value calculation.

This growth is possible as DevOps becomes standard practice across all companies in every industry.

The estimated share price is about 2x the current share price. |

| Base | 55.75 | JFrog will continue to grow its revenue at a steady pace, driven by the increasing adoption of DevOps practices.

However, increased competition and slower enterprise IT spending may limit growth.

While profitability will improve, it will be at a slower pace than expected in the bull case.

This scenario assumes consistent execution and moderate market growth.

JFrog continues to experience growth in both its revenue and customer base as more organizations adopt DevOps practices, but faces significant headwinds due to increased competition and slower enterprise IT spending.

Their shift towards cloud-based solutions and enterprise subscriptions will help maintain a competitive edge.

The base case assumes that JFrog will achieve 15-20% revenue growth annually over the next 5 years and will reach near profitability by year 5, with a 10% net margin.

This growth will be driven by a balance of new customer acquisition and expansion of existing customer accounts.

A successful implementation of their new product offerings will allow them to slowly get to a profitable place.

However, they will be challenged by increased competition from both established players and emerging startups.

Slower growth in enterprise IT spending will also pose a challenge to their revenue growth.

A successful integration of acquisitions and a successful deployment of new enterprise level features will lead to an expansion of ARPU and an increase in their margins.

JFrog will likely expand internationally, but may face challenges due to local market conditions and competition.

This will have a small drag on revenue.

JFrog will also face headwinds with managing operating expenses, resulting in slower improvement in profitability and cash flow generation.

They will experience normal economic conditions, including moderate inflation and interest rates.

No major economic downturns or recessions will occur.

Continued efforts to enhance its platform and provide value to its customers will result in increased customer loyalty and retention.

They will maintain its strategic partnerships with major cloud providers and technology vendors.

Execution by the management team will be adequate to drive growth, but not exceptional.

Finally, JFrog will execute its acquisition plan to a reasonable degree.

The base case assumes that JFrog maintains its market position and grows at a reasonable pace.

A 20x multiple for terminal value calculation and an 8% discount rate is used.

The expected share price target is around $75 at the end of the analysis period.

This represents a modest increase from the current share price, reflecting the slower growth and profitability assumptions.

With a more tempered estimate, JFrog will still be able to deliver moderate returns. |

| Bear | Low | JFrog faces significant challenges from intensifying competition, slower adoption of DevOps solutions, and potential economic downturns.

Inability to innovate and effectively integrate acquisitions will lead to declining market share and revenue growth.

Increased operating expenses and failure to achieve profitability will erode investor confidence.

This scenario envisions a pessimistic outlook for the company.

JFrog faces challenges that significantly impede its growth and profitability.

Increased competition from both established players and emerging startups will lead to price wars and reduced market share.

The DevOps market may experience slower adoption rates due to budget constraints or technological limitations.

Economic downturns could negatively impact IT spending, further reducing demand for JFrog’s solutions.

JFrog is unable to innovate and effectively integrate acquisitions.

This leads to a decline in the market share and erosion of the customer base.

Key customers may switch to alternative solutions.

JFrog faces difficulties in managing operating expenses, resulting in increased losses and reduced cash flow.

Investor confidence in the company erodes, leading to a decline in the stock price.

JFrog is unable to expand internationally due to local market conditions and competition.

This limits its growth potential.

A significant portion of this is due to their inability to adapt to local market conditions.

Finally, JFrog is forced to raise additional capital through debt or equity offerings, diluting existing shareholders.

The bear case assumes that JFrog will experience negative revenue growth or very slow growth (less than 10%) annually over the next 5 years.

The company will fail to achieve profitability and continue to incur losses.

They will have difficulty integrating acquired companies and realize synergies.

A combination of these factors will lead to a significant decline in the company's value.

A 10x multiple for terminal value calculation and a 7% discount rate is used.

The expected share price target is around $30 at the end of the analysis period.

This represents a significant decline from the current share price, reflecting the pessimistic assumptions.

The downside case for the company is about 50% from the current price.

This estimate is used for a worst case scenario.

If the company does not adjust to the market environment, the downside risk will be significant.

In the event of this case, the market will start heavily discounting JFrog due to its lack of revenue growth. |

7. Risks

JFrog exhibits moderate risk due to negative net income despite revenue growth and positive free cash flow. High operating expenses, significant goodwill/intangibles, and reliance on deferred revenue warrant close monitoring. While the company possesses a strong cash position, continued losses could erode this advantage. Stock based compensation is high.

Red Flags:

Consistent Net Losses: The company has been reporting net losses for the past several years, raising concerns about its long-term financial sustainability.

High Selling and Marketing Expenses: A significant portion of revenue is spent on selling and marketing, indicating potential issues with customer acquisition costs or brand loyalty.

Negative Operating Income: The company's operating income has been negative, suggesting inefficiencies in its core business operations.

8. Conclusion

JFrog will continue to grow its revenue at a steady pace, driven by the increasing adoption of DevOps practices.

However, increased competition and slower enterprise IT spending may limit growth.

While profitability will improve, it will be at a slower pace than expected in the bull case.

This scenario assumes consistent execution and moderate market growth.

JFrog continues to experience growth in both its revenue and customer base as more organizations adopt DevOps practices, but faces significant headwinds due to increased competition and slower enterprise IT spending.

Their shift towards cloud-based solutions and enterprise subscriptions will help maintain a competitive edge.

The base case assumes that JFrog will achieve 15-20% revenue growth annually over the next 5 years and will reach near profitability by year 5, with a 10% net margin.

This growth will be driven by a balance of new customer acquisition and expansion of existing customer accounts.

A successful implementation of their new product offerings will allow them to slowly get to a profitable place.

However, they will be challenged by increased competition from both established players and emerging startups.

Slower growth in enterprise IT spending will also pose a challenge to their revenue growth.

A successful integration of acquisitions and a successful deployment of new enterprise level features will lead to an expansion of ARPU and an increase in their margins.

JFrog will likely expand internationally, but may face challenges due to local market conditions and competition.

This will have a small drag on revenue.

JFrog will also face headwinds with managing operating expenses, resulting in slower improvement in profitability and cash flow generation.

They will experience normal economic conditions, including moderate inflation and interest rates.

No major economic downturns or recessions will occur.

Continued efforts to enhance its platform and provide value to its customers will result in increased customer loyalty and retention.

They will maintain its strategic partnerships with major cloud providers and technology vendors.

Execution by the management team will be adequate to drive growth, but not exceptional.

Finally, JFrog will execute its acquisition plan to a reasonable degree.

The base case assumes that JFrog maintains its market position and grows at a reasonable pace.

A 20x multiple for terminal value calculation and an 8% discount rate is used.

The expected share price target is around $75 at the end of the analysis period.

This represents a modest increase from the current share price, reflecting the slower growth and profitability assumptions.

With a more tempered estimate, JFrog will still be able to deliver moderate returns.

Investment research for informational purposes only. Not financial advice.

Continue Your Research

Return to the Analyst Library or explore the specific financial data for this entity on its profile.

Given the company's recent net losses, Return on Invested Capital (ROIC) and Return on Equity (ROE) are negative, which is reflective of the company's inability to generate profits from its capital investments. While the company has demonstrated revenue growth, significant investments in research and development, along with selling and marketing, have not translated into profitability. This trend suggests a need to reassess capital allocation strategies to improve overall capital efficiency.

Given the company's recent net losses, Return on Invested Capital (ROIC) and Return on Equity (ROE) are negative, which is reflective of the company's inability to generate profits from its capital investments. While the company has demonstrated revenue growth, significant investments in research and development, along with selling and marketing, have not translated into profitability. This trend suggests a need to reassess capital allocation strategies to improve overall capital efficiency. The company's free cash flow (FCF) is positive in the most recent two years, indicating the ability to generate cash after accounting for capital expenditures, but this wasn't the case for prior years. The capital expenditure is fairly consistent. It is important to monitor the stability and growth of FCF relative to the company's revenue and profitability to ensure long-term financial health.

The company's free cash flow (FCF) is positive in the most recent two years, indicating the ability to generate cash after accounting for capital expenditures, but this wasn't the case for prior years. The capital expenditure is fairly consistent. It is important to monitor the stability and growth of FCF relative to the company's revenue and profitability to ensure long-term financial health.