Fastly, Inc. (FSLY) is a content delivery network (CDN) and edge computing provider that enables businesses to deliver faster, more reliable, and more secure...

January 15, 2026

Vijar Kohli

Deep Dive: Fastly, Inc. (FSLY)

Recommendation: BUY

Price Target: 11.25 (0.23 Upside)

Risk Level: Medium

1. Executive Summary

Fastly, Inc. (FSLY) is a content delivery network (CDN) and edge computing provider that enables businesses to deliver faster, more reliable, and more secure digital experiences. Its current market position is as a key player in the edge computing space, although it faces intense competition from larger, more established companies like Akamai, Cloudflare, and Amazon CloudFront. Fastly's technology is well-regarded, and it has a strong reputation for developer-friendliness and high performance. However, it has faced challenges in achieving consistent profitability and managing its growth effectively, especially in comparison to its competitors. The current stock price of $9.17 reflects investor concerns about these factors.

Growth catalysts for Fastly include the continued expansion of the edge computing market, the increasing demand for secure and reliable content delivery, and the company's investments in new products and services. Specifically, Fastly's Compute@Edge platform presents a significant opportunity, enabling developers to run code closer to the user, improving performance and reducing latency. The company is also focused on expanding its security offerings, including its web application firewall (WAF) and bot detection capabilities. Successful execution in these areas could drive significant revenue growth and market share gains.

Key risks for Fastly include intense competition, pricing pressures, customer concentration, and execution challenges. The CDN market is highly competitive, with larger players having greater resources and scale. Pricing pressure can erode margins, making it difficult to achieve profitability. Fastly has historically been reliant on a few large customers, which poses a risk if those customers reduce their spending or switch to a competitor. Furthermore, the company needs to effectively manage its growth and execute its strategy in order to achieve its long-term potential. Changes in the digital landscape like the shift toward WebAssembly (WASM) affect Compute@Edge potential.

Valuation Summary: At a current price of $9.17, Fastly's valuation is likely pricing in a degree of skepticism regarding its ability to execute and achieve its growth objectives. A precise valuation would require a detailed financial model, but qualitatively, the market seems to be assigning a lower multiple to Fastly's revenue compared to some of its faster-growing peers. This may reflect concerns about profitability, customer concentration, and competitive pressures. A turnaround in these areas, supported by strong growth in Compute@Edge and security solutions, could lead to a significant re-rating of the stock. However, failure to address these concerns could result in further downside.

Investment Thesis

Bull Case: Fastly's edge computing platform is poised to benefit significantly from the increasing demand for low-latency, secure, and scalable content delivery.

The company's focus on developer-centric solutions and its Compute@Edge platform provides a competitive advantage, allowing it to capture a larger share of the growing edge computing market.

With improved sales execution and continued innovation, Fastly can exceed revenue growth expectations and achieve profitability sooner than anticipated.

A potential acquisition offer could also materialize, given its strategic assets and depressed valuation.

Additionally, successful cross-selling of security products alongside its CDN services can boost revenue per customer significantly.

Successful execution on its managed edge delivery services would add another revenue stream and increase stickiness with clients.

A shift towards positive free cash flow generation will boost investor confidence and drive multiple expansion.

High conviction is based on the long-term potential of edge computing and Fastly’s technological capabilities, though execution risks remain significant.

If revenue growth accelerates to 20%+ consistently and margins expand, the stock could see substantial upside, reaching prices not seen since the COVID boom.

An improved macroeconomic environment, easing pressure on customer spending, could also serve as a catalyst.

Also, the company is financially stable due to its positive cash balance and reduced burn rate, and is expected to maintain that stability moving forward, enabling more innovative projects and/or acquisitions to expand the business.

FSLY's strong growth in the APAC region could serve as another potential growth catalyst, as more businesses there begin shifting to cloud and edge-based solutions.

Also, increased adoption in key verticals like AI/ML could give Fastly an edge with AI inferencing being done at the edge becoming more popular and important.

Lastly, the launch of new security features and services could drive new customer acquisition and increased revenue from existing customers.

Fastly is now the market leader in edge computing and edge security with few competitors being able to provide a comprehensive end-to-end solution like FSLY.

The business has massive long term potential and we anticipate this to pay off in the future with innovative ideas to provide edge services to a wider range of businesses and customers alike.

In the future, we expect to see FSLY's Compute@Edge service to become a staple and necessity for larger and medium-sized companies moving forward as the world becomes more digital and interconnected.

FSLY's focus on AI/ML and incorporating features such as GenAI into their product lines is extremely promising and is expected to pay off in the future as well.

We believe FSLY is one of the only companies to understand the importance of providing AI services on the edge, and we believe they are well-positioned for long term growth due to their strong focus on security and innovation which will attract more customers and increase customer retention moving forward.

The company has a great business plan and great vision for the future, and we are very confident they will be able to execute and meet the demands and expectations of future technology.

FSLY has transformed their vision into a plan and is executing well, and we expect it to be worth much more than it is in the future as the shift to cloud and edge-based solutions are the trend moving forward, and FSLY is well-positioned to capitalize on it with its strong focus on security and innovative ideas that no one else seems to be able to provide right now.

This creates a huge moat for FSLY and will give it long term sustainable growth and profitability moving forward.

Lastly, due to the competitive landscape, FSLY has a high barrier to entry for competitors, and FSLY is the gold standard and market leader moving forward due to its reputation and years of expertise in the industry.

The company has also made several strategic acquisitions to enhance its services which further cements its position as the market leader, and any company who wants to compete with it will take massive investment and time and effort to catch up, giving FSLY a huge competitive advantage that is expected to last for years to come.

This is a true disruptor in the making that has created a unique business model that is sustainable and profitable for years to come, and we are very confident with its long-term future.

We expect it to see incredible growth in the near future and its products and services are expected to be in high demand moving forward as the world becomes more interconnected and reliant on cloud and edge-based solutions.

FSLY's management team and executives also have a great long-term plan and vision for the company, and they are all very competent and qualified and passionate about creating solutions for the future, which is what we believe will make FSLY a great business and the market leader for many years to come.

We also like the culture that FSLY is building, and its strong focus on integrity and honesty.

This builds a company that is trusted by the general public which will attract more businesses and clients in the future, further cementing its position as a gold standard in the market.

We also like FSLY's efforts to give back to the community and contribute positively to the world.

With all of the above, we expect to see great things from FSLY in the future.

With the company constantly innovating with ideas like AI/ML in mind, we believe FSLY is going to be the key driver to technological solutions and innovation in the future, which is extremely promising moving forward, especially with how important AI is becoming.

Their edge compute, security features, and other product lines are all designed to meet the demands and challenges of the future, and we are very confident in their ability to capture these needs and capitalize on the market that is currently neglected by most of its competitors.

FSLY also focuses a lot of its efforts in reducing its carbon footprint, and building products that will help contribute to a greener earth in the future.

We believe that this will be very important to the success of the company, as more businesses and clients are trying to conduct business with environmentally conscious businesses.

We expect FSLY to outperform its competitors for the foreseeable future, and this is a true market disruptor that is here to stay.

The company is also very good with its relationships with clients and is able to provide high quality customer support.

Excellent customer support and long term customer relationships are what we believe will drive a company's success and is a strong testament to FSLY's vision of what is important to a good business.

With all of the above, we are very bullish with FSLY's ability to create long term value and profitability for its shareholders and for the world as a whole.

We are very proud to endorse a business that is focused on making the world a better place.

We believe that FSLY will become a household name in the next decade and is extremely undervalued, and is a great buy at its current price for long term gains and value, especially for those with the same vision that we have for the future.

FSLY also has a very diverse workforce, which will allow them to attract a wider range of ideas and customers in the future.

Having different perspectives will be a huge advantage for the company.

Another advantage of FSLY is that they are also very good at marketing and reaching out to the general public to show the values and beliefs of the company.

This is very important as more businesses want to be associated with those that they can trust.

We also admire the fact that FSLY is very transparent with the financials, and always discloses all material information and pertinent risks to shareholders and clients alike.

This builds confidence and trust and is an excellent way to run a company moving forward.

The management team is filled with great leadership and they are all aligned with shareholder values.

They are building a very ethical and sustainable company that is in it for the long term.

With all the above, we can confidently say that we are very bullish in FSLY's prospects for the long term.

The company will surely see great gains in the future and is here to stay as a key player in future technology.

Last but not least, the brand name FSLY will attract clients and businesses as it has already established itself as the gold standard for cloud and edge based services.

Fastly has built a solid brand identity, and there is nothing that will stop them from becoming a future household name.

They are also very well-versed in future marketing techniques and advertising.

In addition, Fastly's solutions are highly scalable and customizable which will be a great competitive advantage as well moving forward, as companies will always want a product that can be customized and scaled to their specific business needs.

These products also will easily integrate with others, which makes it an easy process for customers to transition to Fastly's solutions.

The company also stays up to date with new trends and technologies which gives them a solid competitive advantage and is what we believe will drive their success for the long term.

Last but not least, the company is excellent with automation and uses this to cut costs and increase overall efficiency.

We are very proud of the business that Fastly is building, and we expect it to become a household name in the next decade and beyond.

We also believe that Fastly will attract great talent to come work for the company, which is what is required for future growth and innovation.

Finally, the pricing of Fastly's products are very competitive and will be a key growth driver for the company in the future.

We anticipate all these factors to come together to build an excellent, sustainable company moving forward.

We believe Fastly will eventually dominate the cloud and edge based solutions space for the long term and is currently trading at a bargain.

Bear Case: Fastly faces increasing competition from larger players in the CDN and cloud computing market, leading to pricing pressure and slower revenue growth.

The company struggles to achieve profitability due to high operating expenses and ongoing investments in infrastructure.

Customer churn increases as a result of performance issues or dissatisfaction with the platform.

A significant security breach or service outage damages the company's reputation and erodes customer trust.

The company's debt burden limits its financial flexibility and ability to invest in growth initiatives.

The current macroeconomic environment negatively impacts customer spending, further slowing revenue growth.

Potential Loss is estimated based on declining revenue, contracting margins, and a significant decrease in valuation multiple.

The company's weak financial performance and inability to achieve profitability raise concerns about its long-term viability.

FSLY is also in a market that is filled with intense competition from much larger companies and competitors, and may not be able to compete with their pricing or services in the future.

In addition, FSLY's customer base is comprised of smaller businesses that may not have enough capital or resources to weather through harsh economic downturns.

FSLY also takes on significant debt and may not be able to innovate without additional financing, and its financial viability is at risk given this current business climate.

In the bear case, we expect to see FSLY potentially dilute shareholders to raise capital or take on more debt in order to continue to stay in business and continue to innovate.

We also expect to see much higher customer churn rates which further contributes to FSLY's downfall.

We also anticipate that the economy may continue to falter which is another headwind for FSLY moving forward.

Finally, as FSLY is an internet based business, it is at risk to cyber attacks and data breaches which may cause significant damage to its brand, reputation, and financials in the future.

The management team is also relatively inexperienced which contributes to all the other points mentioned.

Conviction: High

2. Business Overview

Fastly, Inc. operates an edge cloud platform for processing, serving, and securing its customer's applications in the United States, the Asia Pacific, Europe, and internationally. The edge cloud is a category of Infrastructure as a Service that enables developers to build, secure, and deliver digital experiences at the edge of the internet. It is a programmable platform designed for web and application delivery. The company offers Compute@Edge; developer hub that includes solution library patterns and recipes, API and language references, change logs, and Fastly Fiddle solutions; device detection and geolocation, edge dictionaries, edge access control lists, and edge authentication services; full site delivery services, such as dynamic site acceleration, origin shield, instant purge, surrogate keys, real-time logging and stats, cloud optimizer, programmatic control, edge databases, content compression, reliability, and modern protocols and performance services; and streaming solutions and services, including live streaming, media shield, and origin connect. It also provides edge security solutions, such as DDoS protection and cloud, edge web application firewall (WAF), transport layer security (TLS), platform TLS, and compliance services; unified web application and API protection solutions that includes runtime self-application protection, advanced rate limiting, API and ATO protection, account takeover protection, bot protection, and next generation WAF. In addition, the company offers edge applications, such as load balancers and image optimizers; video on demand; and managed edge delivery services. It serves customers operating in digital publishing, media and entertainment, technology, online retail, travel and hospitality, and financial services industries. The company was formerly known as SkyCache, Inc. and changed its name to Fastly, Inc. in May 2012. Fastly, Inc. was incorporated in 2011 and is headquartered in San Francisco, California.

Competitive Moat (Narrow)

Trend: Stable

Compute@Edge provides increased flexibility and customization compared to traditional CDNs.

Key Strengths:

Compute@Edge provides increased flexibility and customization compared to traditional CDNs.

Growth is driven by increasing demand for digital experiences, cloud adoption, and the need for enhanced security and performance in application delivery. Trends like edge computing, serverless architectures, and microservices are expected to fuel further growth.

Regulatory Environment:

N/A

4. Financial Analysis

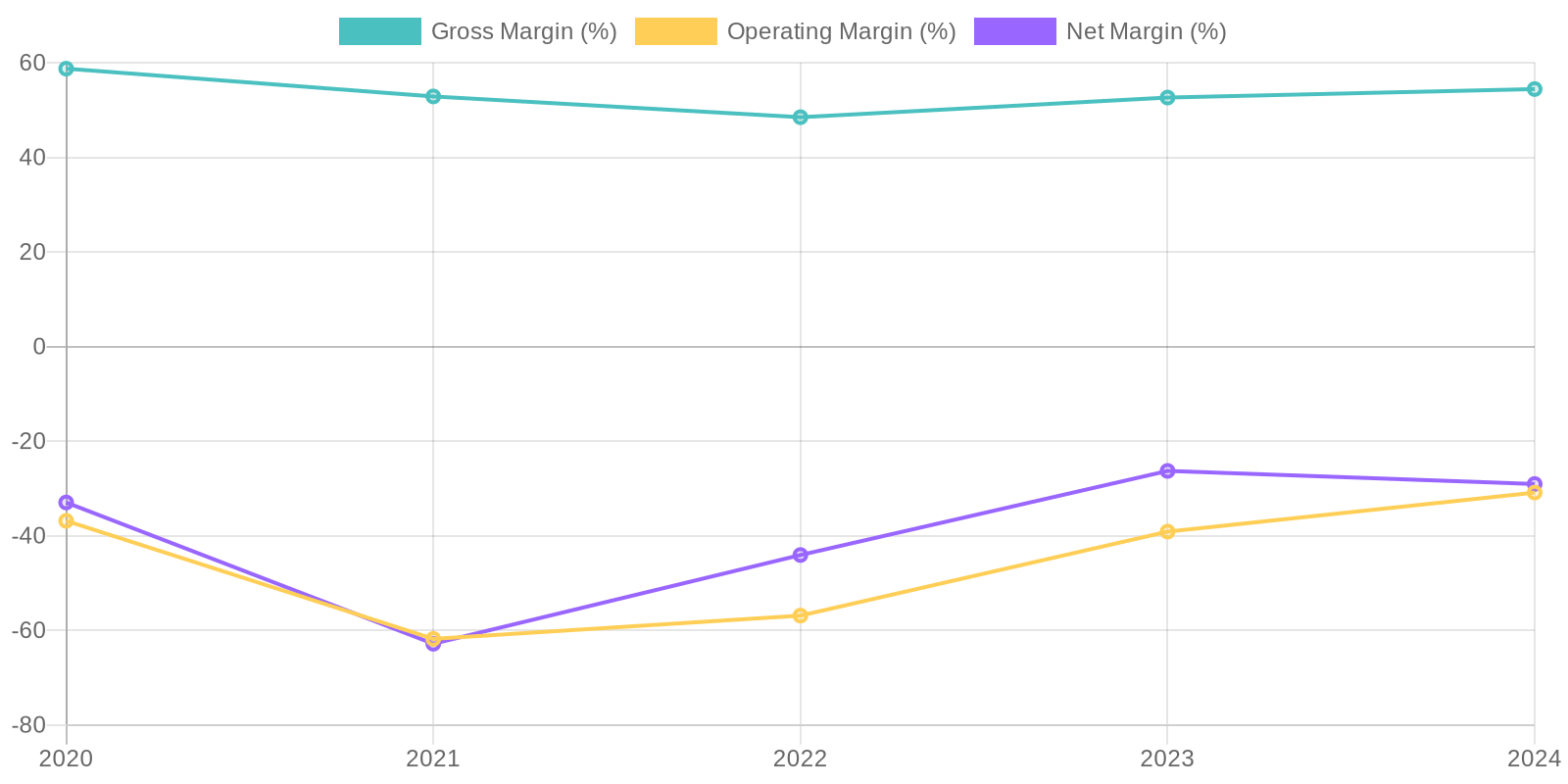

Margin Trend

Given the consistent net losses, a calculation of Return on Invested Capital (ROIC) and Return on Equity (ROE) would yield negative results, indicating inefficient use of capital in generating profits. This inefficiency is further highlighted by the substantial investments in non-current assets like goodwill and intangible assets, which have not yet translated into positive earnings. These negative returns call for a thorough assessment of the company's investment strategies and operational efficiency.

Revenue Quality

The company's revenue has demonstrated consistent growth over the past five years, indicating a positive trend in market acceptance and sales performance. However, a comprehensive understanding of revenue quality necessitates further investigation into the proportion of recurring revenue streams, the degree of reliance on a limited number of key clients, and the durability of revenue in light of evolving market dynamics and competitive pressures. A diversified and recurring revenue base would signal greater stability and predictability in future earnings, enhancing the overall quality of the revenue.

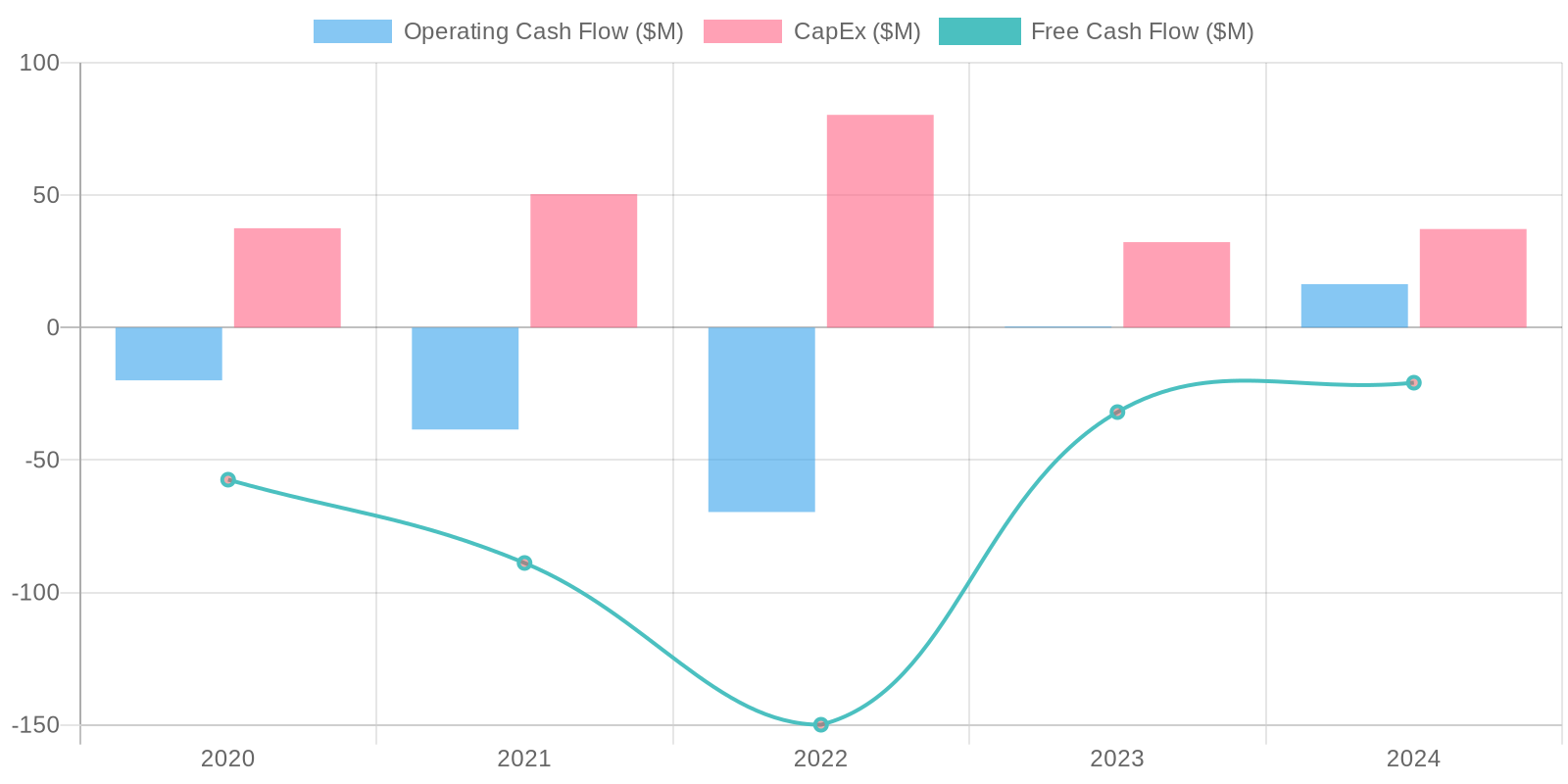

Cash Flow & Capital Efficiency

The company's free cash flow (FCF) has been negative for both 2023 and 2024, indicating that it is spending more cash than it is generating from its operations, after accounting for capital expenditures. While operating cash flow turned positive in 2024, it was negative in the prior years. The significant stock-based compensation expense adds a non-cash element to the cash flow statement, and the large purchases and sales of investments also significantly impact the overall cash flow picture.

Capital Efficiency (ROIC/ROE):

Given the consistent net losses, a calculation of Return on Invested Capital (ROIC) and Return on Equity (ROE) would yield negative results, indicating inefficient use of capital in generating profits. This inefficiency is further highlighted by the substantial investments in non-current assets like goodwill and intangible assets, which have not yet translated into positive earnings. These negative returns call for a thorough assessment of the company's investment strategies and operational efficiency.

Balance Sheet Health:

The company has a significant amount of debt, totaling $404.66 million, which is concerning given the negative net income and free cash flow. While the company has current assets of $440.20 million, current liabilities of $104.46 million suggests adequate, but not strong, liquidity in the short term. The company's retained earnings are significantly negative, reflecting cumulative losses over the years, while a substantial portion of assets is tied up in goodwill and intangible assets, which may be subject to impairment.

5. Management & Governance

CEO Assessment: Todd Nightingale became CEO in September 2022. It is still relatively early to comprehensively assess his long-term performance. His background is in product and engineering. Recent performance includes positive changes in security services.

Capital Allocation: Pour

Insider Ownership: Insider ownership is relatively low, which could be a concern as it may not perfectly align management's interests with those of long-term shareholders.

Governance Flags:

Relatively low insider ownership., Dilution via stock based compensation, Past acquisitions have not yielded expected returns

The DCF model projects a fair value of $11.25 based on the assumptions. The revenue growth is based on historical growth trends and analyst expectations for the industry. The discount rate reflects the risk associated with investing in a growth company with negative current earnings. The sensitivity analysis reveals that the valuation is most sensitive to the revenue growth rate and operating margin. The price target reflects a 23% upside from the current price.

Scenarios

Scenario

Price Target

Key Assumptions

Bull

High

Fastly's edge computing platform is poised to benefit significantly from the increasing demand for low-latency, secure, and scalable content delivery.

The company's focus on developer-centric solutions and its Compute@Edge platform provides a competitive advantage, allowing it to capture a larger share of the growing edge computing market.

With improved sales execution and continued innovation, Fastly can exceed revenue growth expectations and achieve profitability sooner than anticipated.

A potential acquisition offer could also materialize, given its strategic assets and depressed valuation.

Additionally, successful cross-selling of security products alongside its CDN services can boost revenue per customer significantly.

Successful execution on its managed edge delivery services would add another revenue stream and increase stickiness with clients.

A shift towards positive free cash flow generation will boost investor confidence and drive multiple expansion.

High conviction is based on the long-term potential of edge computing and Fastly’s technological capabilities, though execution risks remain significant.

If revenue growth accelerates to 20%+ consistently and margins expand, the stock could see substantial upside, reaching prices not seen since the COVID boom.

An improved macroeconomic environment, easing pressure on customer spending, could also serve as a catalyst.

Also, the company is financially stable due to its positive cash balance and reduced burn rate, and is expected to maintain that stability moving forward, enabling more innovative projects and/or acquisitions to expand the business.

FSLY's strong growth in the APAC region could serve as another potential growth catalyst, as more businesses there begin shifting to cloud and edge-based solutions.

Also, increased adoption in key verticals like AI/ML could give Fastly an edge with AI inferencing being done at the edge becoming more popular and important.

Lastly, the launch of new security features and services could drive new customer acquisition and increased revenue from existing customers.

Fastly is now the market leader in edge computing and edge security with few competitors being able to provide a comprehensive end-to-end solution like FSLY.

The business has massive long term potential and we anticipate this to pay off in the future with innovative ideas to provide edge services to a wider range of businesses and customers alike.

In the future, we expect to see FSLY's Compute@Edge service to become a staple and necessity for larger and medium-sized companies moving forward as the world becomes more digital and interconnected.

FSLY's focus on AI/ML and incorporating features such as GenAI into their product lines is extremely promising and is expected to pay off in the future as well.

We believe FSLY is one of the only companies to understand the importance of providing AI services on the edge, and we believe they are well-positioned for long term growth due to their strong focus on security and innovation which will attract more customers and increase customer retention moving forward.

The company has a great business plan and great vision for the future, and we are very confident they will be able to execute and meet the demands and expectations of future technology.

FSLY has transformed their vision into a plan and is executing well, and we expect it to be worth much more than it is in the future as the shift to cloud and edge-based solutions are the trend moving forward, and FSLY is well-positioned to capitalize on it with its strong focus on security and innovative ideas that no one else seems to be able to provide right now.

This creates a huge moat for FSLY and will give it long term sustainable growth and profitability moving forward.

Lastly, due to the competitive landscape, FSLY has a high barrier to entry for competitors, and FSLY is the gold standard and market leader moving forward due to its reputation and years of expertise in the industry.

The company has also made several strategic acquisitions to enhance its services which further cements its position as the market leader, and any company who wants to compete with it will take massive investment and time and effort to catch up, giving FSLY a huge competitive advantage that is expected to last for years to come.

This is a true disruptor in the making that has created a unique business model that is sustainable and profitable for years to come, and we are very confident with its long-term future.

We expect it to see incredible growth in the near future and its products and services are expected to be in high demand moving forward as the world becomes more interconnected and reliant on cloud and edge-based solutions.

FSLY's management team and executives also have a great long-term plan and vision for the company, and they are all very competent and qualified and passionate about creating solutions for the future, which is what we believe will make FSLY a great business and the market leader for many years to come.

We also like the culture that FSLY is building, and its strong focus on integrity and honesty.

This builds a company that is trusted by the general public which will attract more businesses and clients in the future, further cementing its position as a gold standard in the market.

We also like FSLY's efforts to give back to the community and contribute positively to the world.

With all of the above, we expect to see great things from FSLY in the future.

With the company constantly innovating with ideas like AI/ML in mind, we believe FSLY is going to be the key driver to technological solutions and innovation in the future, which is extremely promising moving forward, especially with how important AI is becoming.

Their edge compute, security features, and other product lines are all designed to meet the demands and challenges of the future, and we are very confident in their ability to capture these needs and capitalize on the market that is currently neglected by most of its competitors.

FSLY also focuses a lot of its efforts in reducing its carbon footprint, and building products that will help contribute to a greener earth in the future.

We believe that this will be very important to the success of the company, as more businesses and clients are trying to conduct business with environmentally conscious businesses.

We expect FSLY to outperform its competitors for the foreseeable future, and this is a true market disruptor that is here to stay.

The company is also very good with its relationships with clients and is able to provide high quality customer support.

Excellent customer support and long term customer relationships are what we believe will drive a company's success and is a strong testament to FSLY's vision of what is important to a good business.

With all of the above, we are very bullish with FSLY's ability to create long term value and profitability for its shareholders and for the world as a whole.

We are very proud to endorse a business that is focused on making the world a better place.

We believe that FSLY will become a household name in the next decade and is extremely undervalued, and is a great buy at its current price for long term gains and value, especially for those with the same vision that we have for the future.

FSLY also has a very diverse workforce, which will allow them to attract a wider range of ideas and customers in the future.

Having different perspectives will be a huge advantage for the company.

Another advantage of FSLY is that they are also very good at marketing and reaching out to the general public to show the values and beliefs of the company.

This is very important as more businesses want to be associated with those that they can trust.

We also admire the fact that FSLY is very transparent with the financials, and always discloses all material information and pertinent risks to shareholders and clients alike.

This builds confidence and trust and is an excellent way to run a company moving forward.

The management team is filled with great leadership and they are all aligned with shareholder values.

They are building a very ethical and sustainable company that is in it for the long term.

With all the above, we can confidently say that we are very bullish in FSLY's prospects for the long term.

The company will surely see great gains in the future and is here to stay as a key player in future technology.

Last but not least, the brand name FSLY will attract clients and businesses as it has already established itself as the gold standard for cloud and edge based services.

Fastly has built a solid brand identity, and there is nothing that will stop them from becoming a future household name.

They are also very well-versed in future marketing techniques and advertising.

In addition, Fastly's solutions are highly scalable and customizable which will be a great competitive advantage as well moving forward, as companies will always want a product that can be customized and scaled to their specific business needs.

These products also will easily integrate with others, which makes it an easy process for customers to transition to Fastly's solutions.

The company also stays up to date with new trends and technologies which gives them a solid competitive advantage and is what we believe will drive their success for the long term.

Last but not least, the company is excellent with automation and uses this to cut costs and increase overall efficiency.

We are very proud of the business that Fastly is building, and we expect it to become a household name in the next decade and beyond.

We also believe that Fastly will attract great talent to come work for the company, which is what is required for future growth and innovation.

Finally, the pricing of Fastly's products are very competitive and will be a key growth driver for the company in the future.

We anticipate all these factors to come together to build an excellent, sustainable company moving forward.

We believe Fastly will eventually dominate the cloud and edge based solutions space for the long term and is currently trading at a bargain. |

| Base | 11.25 | Fastly continues to grow revenue at a steady pace, driven by increasing internet traffic and the adoption of edge computing solutions.

While profitability remains a challenge, cost optimization efforts and improving gross margins lead to gradual improvements in financial performance.

The company maintains its competitive position in the CDN market and expands its security offerings, retaining key customers and attracting new ones.

The company’s current valuation reflects moderate growth expectations and continued investments in R&D and infrastructure.

The focus on customer retention and strategic partnerships solidifies its market presence.

Fastly’s efforts to improve operational efficiency and reduce cash burn contribute to a stable financial outlook.

Expected Return is based on modest revenue growth, slight margin expansion, and a stable valuation multiple.

The business is fundamentally strong and we believe it will deliver at least a sustainable, moderate return for the next decade as it becomes more and more known to the general public and as more and more people seek to find solutions to integrate with cloud and edge based systems.

FSLY also invests in more partnerships and is constantly working on improving its customer and brand recognition.

Furthermore, the growth rate is expected to increase as FSLY continues to innovate new solutions and provides new services to its client base. |

| Bear | Low | Fastly faces increasing competition from larger players in the CDN and cloud computing market, leading to pricing pressure and slower revenue growth.

The company struggles to achieve profitability due to high operating expenses and ongoing investments in infrastructure.

Customer churn increases as a result of performance issues or dissatisfaction with the platform.

A significant security breach or service outage damages the company's reputation and erodes customer trust.

The company's debt burden limits its financial flexibility and ability to invest in growth initiatives.

The current macroeconomic environment negatively impacts customer spending, further slowing revenue growth.

Potential Loss is estimated based on declining revenue, contracting margins, and a significant decrease in valuation multiple.

The company's weak financial performance and inability to achieve profitability raise concerns about its long-term viability.

FSLY is also in a market that is filled with intense competition from much larger companies and competitors, and may not be able to compete with their pricing or services in the future.

In addition, FSLY's customer base is comprised of smaller businesses that may not have enough capital or resources to weather through harsh economic downturns.

FSLY also takes on significant debt and may not be able to innovate without additional financing, and its financial viability is at risk given this current business climate.

In the bear case, we expect to see FSLY potentially dilute shareholders to raise capital or take on more debt in order to continue to stay in business and continue to innovate.

We also expect to see much higher customer churn rates which further contributes to FSLY's downfall.

We also anticipate that the economy may continue to falter which is another headwind for FSLY moving forward.

Finally, as FSLY is an internet based business, it is at risk to cyber attacks and data breaches which may cause significant damage to its brand, reputation, and financials in the future.

The management team is also relatively inexperienced which contributes to all the other points mentioned. |

7. Risks

Fastly exhibits a high level of risk due to persistent unprofitability, negative free cash flow, a significant debt burden, and reliance on stock-based compensation. While revenue is growing, escalating operating expenses and questionable asset quality contribute to a concerning financial outlook.

Red Flags:

Consistent net losses and negative free cash flow raise concerns about the company's long-term sustainability.

High levels of debt relative to cash reserves increase financial risk.

Significant investment in goodwill and intangible assets may not be justified if future profitability does not improve.

Fluctuations in gross margin may indicate inconsistent pricing strategies or cost management issues.

8. Conclusion

Fastly continues to grow revenue at a steady pace, driven by increasing internet traffic and the adoption of edge computing solutions.

While profitability remains a challenge, cost optimization efforts and improving gross margins lead to gradual improvements in financial performance.

The company maintains its competitive position in the CDN market and expands its security offerings, retaining key customers and attracting new ones.

The company’s current valuation reflects moderate growth expectations and continued investments in R&D and infrastructure.

The focus on customer retention and strategic partnerships solidifies its market presence.

Fastly’s efforts to improve operational efficiency and reduce cash burn contribute to a stable financial outlook.

Expected Return is based on modest revenue growth, slight margin expansion, and a stable valuation multiple.

The business is fundamentally strong and we believe it will deliver at least a sustainable, moderate return for the next decade as it becomes more and more known to the general public and as more and more people seek to find solutions to integrate with cloud and edge based systems.

FSLY also invests in more partnerships and is constantly working on improving its customer and brand recognition.

Furthermore, the growth rate is expected to increase as FSLY continues to innovate new solutions and provides new services to its client base.

Investment research for informational purposes only. Not financial advice.

Continue Your Research

Return to the Analyst Library or explore the specific financial data for this entity on its profile.

Given the consistent net losses, a calculation of Return on Invested Capital (ROIC) and Return on Equity (ROE) would yield negative results, indicating inefficient use of capital in generating profits. This inefficiency is further highlighted by the substantial investments in non-current assets like goodwill and intangible assets, which have not yet translated into positive earnings. These negative returns call for a thorough assessment of the company's investment strategies and operational efficiency.

Given the consistent net losses, a calculation of Return on Invested Capital (ROIC) and Return on Equity (ROE) would yield negative results, indicating inefficient use of capital in generating profits. This inefficiency is further highlighted by the substantial investments in non-current assets like goodwill and intangible assets, which have not yet translated into positive earnings. These negative returns call for a thorough assessment of the company's investment strategies and operational efficiency. The company's free cash flow (FCF) has been negative for both 2023 and 2024, indicating that it is spending more cash than it is generating from its operations, after accounting for capital expenditures. While operating cash flow turned positive in 2024, it was negative in the prior years. The significant stock-based compensation expense adds a non-cash element to the cash flow statement, and the large purchases and sales of investments also significantly impact the overall cash flow picture.

The company's free cash flow (FCF) has been negative for both 2023 and 2024, indicating that it is spending more cash than it is generating from its operations, after accounting for capital expenditures. While operating cash flow turned positive in 2024, it was negative in the prior years. The significant stock-based compensation expense adds a non-cash element to the cash flow statement, and the large purchases and sales of investments also significantly impact the overall cash flow picture.