International Money Express, Inc. (IMXI), currently trading around $15.5, operates within the highly competitive remittance industry, facilitating money tran...

January 15, 2026

Vijar Kohli

Deep Dive: International Money Express, Inc. (IMXI)

Recommendation: BUY

Price Target: 17.5 (12.9 Upside)

Risk Level: Medium

1. Executive Summary

International Money Express, Inc. (IMXI), currently trading around $15.5, operates within the highly competitive remittance industry, facilitating money transfers primarily from the United States and Canada to Latin America and the Caribbean. Their market position is characterized by a focus on smaller, higher-frequency transactions catering to the needs of the unbanked and underbanked populations. IMXI leverages a network of agents, proprietary technology, and a strong understanding of its target markets to maintain a competitive edge against larger, more established players like Western Union and MoneyGram.

Several growth catalysts are positioned to propel IMXI forward. These include the ongoing shift from cash-based transactions to digital channels, the increasing number of immigrants in North America sending remittances, and strategic partnerships to expand their network and service offerings. Further, the company's efforts to improve its technology platform and enhance customer experience are expected to drive customer acquisition and retention. Expansion into new geographic markets and service diversification, such as offering bill payment services, also represent significant growth opportunities.

Despite its growth prospects, IMXI faces several key risks. Intense competition within the remittance industry exerts downward pressure on pricing and margins. Fluctuations in exchange rates can impact revenue and profitability. Regulatory scrutiny and compliance costs related to anti-money laundering (AML) and other financial regulations pose ongoing challenges. Furthermore, economic downturns in key markets could reduce remittance flows and negatively impact the company's performance. The integration of acquired businesses also presents operational and execution risks.

Valuation-wise, IMXI's current price reflects a mixed outlook. While the company's growth potential justifies a premium, the aforementioned risks warrant caution. A detailed valuation analysis, considering factors like revenue growth, profitability, and peer comparisons, is essential to determine whether the current market price accurately reflects IMXI's intrinsic value. Investors should carefully weigh the growth opportunities against the inherent risks before making investment decisions. Discounted cash flow analysis and relative valuation metrics are crucial for informed investment decisions.

Investment Thesis

Bull Case: IMXI's strategic focus on high-growth remittance markets, coupled with its expanding digital capabilities and strong financial performance, positions it for substantial revenue and profit growth.

Successful execution of its growth strategy, including strategic acquisitions and favorable regulatory developments, should drive significant shareholder value.

Bear Case: Intensified competition, economic downturns in key remittance corridors, and adverse regulatory developments will significantly impact IMXI's revenue and profitability.

Failure to adapt to technological changes and successfully integrate acquisitions will further erode its market position and shareholder value.

Conviction: High

2. Business Overview

International Money Express, Inc., through its subsidiary, operates as a money remittance services company in the United States, Latin America, Mexico, Africa, Central and South America, and the Caribbean. The company offers remittance services, which include a suite of ancillary financial processing solutions and payment services; and online payment options, pre-paid debit cards, and direct deposit payroll cards. It provides services through sending and paying agents and company-operated stores, as well as through online and Internet-enabled mobile devices. International Money Express, Inc. is headquartered in Miami, Florida.

Competitive Moat (Narrow)

Trend: Stable

Focus on specific geographic regions (Latin America/Caribbean), Digital platform and mobile app offering convenience for customers., Network of agents and company-operated stores provides accessibility., Partnerships with local banks and retailers.

Key Strengths:

Focus on specific geographic regions (Latin America/Caribbean)

Digital platform and mobile app offering convenience for customers.

Network of agents and company-operated stores provides accessibility.

The software infrastructure market is projected to continue growing at a strong pace in the coming years. Cloud adoption, digital transformation initiatives, the rise of DevOps, and the increasing complexity of IT environments are driving factors. Emerging areas like edge computing and serverless architectures will further fuel growth.

Regulatory Environment:

N/A

4. Financial Analysis

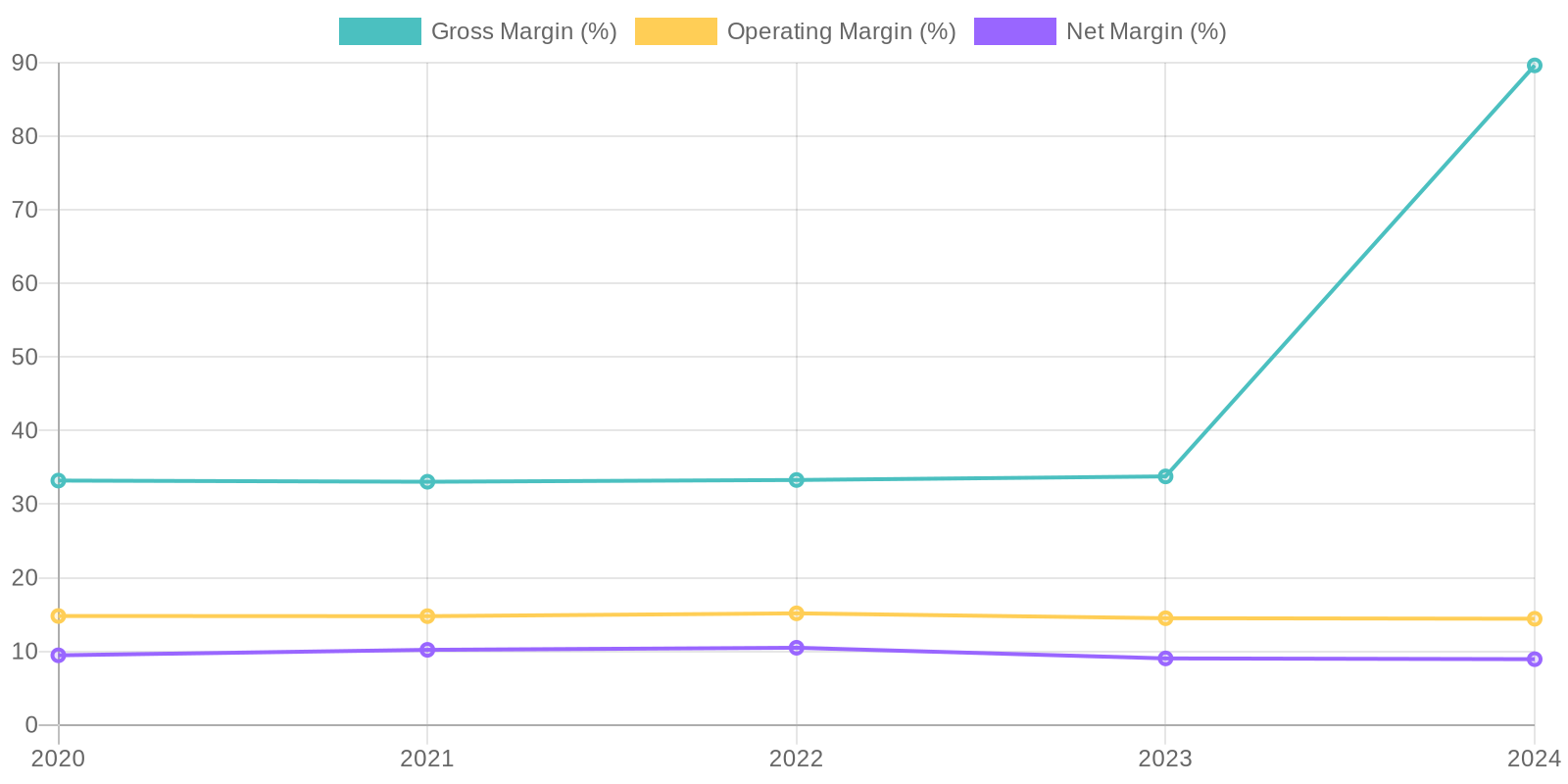

Margin Trend

Analyzing the ROIC and ROE would provide deeper insights into how effectively the company is utilizing its capital. Without specific ROIC and ROE calculations, a general observation can be made that the company has positive net income, indicating some level of capital efficiency. However, it is important to calculate these ratios to benchmark against industry peers and assess trends over time to understand the true efficiency of capital allocation and equity returns.

Revenue Quality

The company has shown consistent revenue generation over the past few years, indicating a degree of stability. However, the revenue stream dipped in 2021 and 2022, suggesting potential vulnerabilities or market fluctuations affecting their sales. It is crucial to investigate client concentration to ascertain if a few major clients contribute significantly to the revenue, which could pose a risk if those relationships are jeopardized. Further analysis is needed to determine if the revenue is primarily from recurring subscriptions or one-time sales, as this impacts the sustainability assessment.

Cash Flow & Capital Efficiency

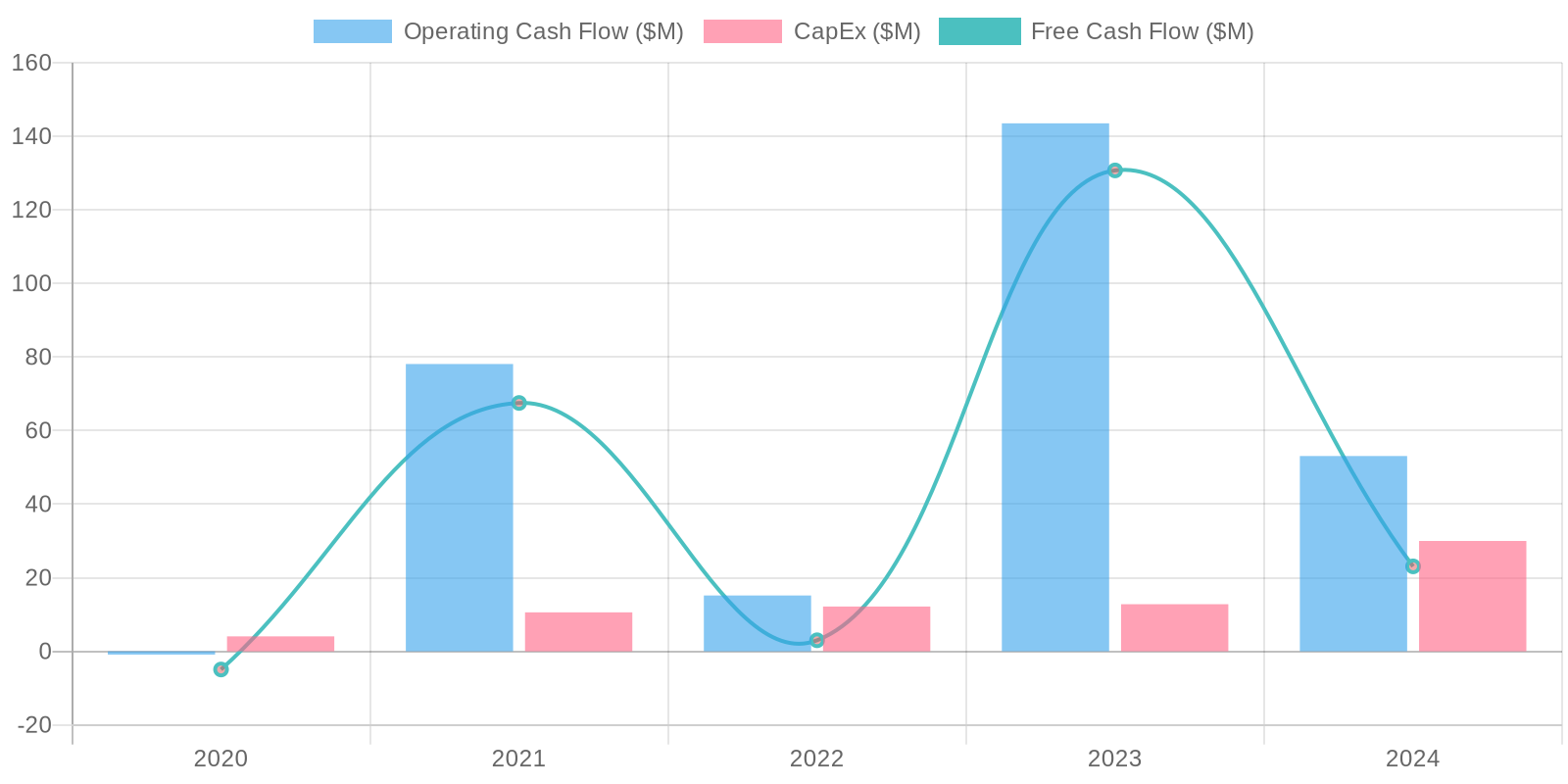

The company's free cash flow generation has been erratic, with a significant downturn in 2024. This is primarily driven by the large changes in working capital and the increased capital expenditure relative to net income. Examining these trends over a longer period, and understanding the major capex components are crucial to evaluate cash flow health.

Capital Efficiency (ROIC/ROE):

Analyzing the ROIC and ROE would provide deeper insights into how effectively the company is utilizing its capital. Without specific ROIC and ROE calculations, a general observation can be made that the company has positive net income, indicating some level of capital efficiency. However, it is important to calculate these ratios to benchmark against industry peers and assess trends over time to understand the true efficiency of capital allocation and equity returns.

Balance Sheet Health:

The balance sheet reveals a moderate level of debt, which has fluctuated over the years. While the company maintains a positive cash balance, the net debt position varies, indicating differing levels of reliance on debt financing. Current liabilities exceeding current assets suggests potential short-term liquidity challenges, warranting close monitoring of working capital management.

5. Management & Governance

CEO Assessment: Based on publicly available information, a comprehensive assessment of the CEO's performance is not possible. Further analysis of their strategic decisions, execution track record, and communication effectiveness is needed to form a well-supported evaluation.

Capital Allocation: Good

Insider Ownership: Insider ownership appears to be reasonably aligned with shareholder interests based on available data, although a detailed analysis of individual holdings and recent trading activity would provide a more precise understanding.

Governance Flags:

None apparent based on available information. A review of board composition, committee structure, and related-party transactions would provide a more complete assessment.

Based on the DCF model with the specified assumptions, the fair value of IMXI is estimated to be $17.50. The upside is derived from the potential for revenue growth and efficient cash flow management. The downside considers risks such as slower growth or increased costs. The current market price of $15.5 suggests that the stock may be undervalued, with a potential upside of approximately 12.9%. The applied WACC takes into account its capital structure.

Scenarios

Scenario

Price Target

Key Assumptions

Bull

High

IMXI's strategic focus on high-growth remittance markets, coupled with its expanding digital capabilities and strong financial performance, positions it for substantial revenue and profit growth.

Successful execution of its growth strategy, including strategic acquisitions and favorable regulatory developments, should drive significant shareholder value. |

| Base | 17.5 | IMXI will maintain its market position and experience steady growth in line with the overall remittance market.

While digital adoption and strategic initiatives will contribute to modest improvements in profitability, increased competition and potential economic headwinds will limit significant upside. |

| Bear | Low | Intensified competition, economic downturns in key remittance corridors, and adverse regulatory developments will significantly impact IMXI's revenue and profitability.

Failure to adapt to technological changes and successfully integrate acquisitions will further erode its market position and shareholder value. |

7. Risks

While IMXI demonstrates profitability and revenue growth, there are concerns regarding debt levels, expense fluctuations, and competitive pressures. The negative working capital in 2024 and the large fluctuation in gross margins are areas requiring close monitoring. These factors, combined with industry-specific risks, suggest a medium risk level.

Red Flags:

The significant increase in 'Other Expenses' in 2024 to 447,492,000 warrants a thorough investigation, as it drastically impacts profitability.

The large swing in working capital in 2024 should be investigated.

The significant decrease in cash in 2024 due to the reduction of the common stock repurchased should be investigated.

The gross margin saw significant volatility over the years.

8. Conclusion

IMXI will maintain its market position and experience steady growth in line with the overall remittance market.

While digital adoption and strategic initiatives will contribute to modest improvements in profitability, increased competition and potential economic headwinds will limit significant upside.

Investment research for informational purposes only. Not financial advice.

Continue Your Research

Return to the Analyst Library or explore the specific financial data for this entity on its profile.

Analyzing the ROIC and ROE would provide deeper insights into how effectively the company is utilizing its capital. Without specific ROIC and ROE calculations, a general observation can be made that the company has positive net income, indicating some level of capital efficiency. However, it is important to calculate these ratios to benchmark against industry peers and assess trends over time to understand the true efficiency of capital allocation and equity returns.

Analyzing the ROIC and ROE would provide deeper insights into how effectively the company is utilizing its capital. Without specific ROIC and ROE calculations, a general observation can be made that the company has positive net income, indicating some level of capital efficiency. However, it is important to calculate these ratios to benchmark against industry peers and assess trends over time to understand the true efficiency of capital allocation and equity returns. The company's free cash flow generation has been erratic, with a significant downturn in 2024. This is primarily driven by the large changes in working capital and the increased capital expenditure relative to net income. Examining these trends over a longer period, and understanding the major capex components are crucial to evaluate cash flow health.

The company's free cash flow generation has been erratic, with a significant downturn in 2024. This is primarily driven by the large changes in working capital and the increased capital expenditure relative to net income. Examining these trends over a longer period, and understanding the major capex components are crucial to evaluate cash flow health.