Deep Dive: Informatica Inc. (INFA)

Recommendation: HOLD Price Target: 25.41 (2.5 Upside) Risk Level: Medium

1. Executive Summary

N/A

Investment Thesis

Bull Case: N/A Bear Case: N/A Conviction: High

2. Business Overview

Informatica Inc. develops an artificial intelligence-powered platform that connects, manages, and unifies data across multi-cloud, hybrid systems at enterprise scale in the United States. The company's platform includes a suite of interoperable data management products, including data integration products to ingest, transform, and integrate data; API and application integration products that enable users to create and manage APIs and integration processes for app-to-app synchronization, business process orchestration, B2B partner management, application development, and API management; data quality products to profile, cleanse, standardize, and enrich data to deliver accurate, complete, and consistent data sets for analytics, data science, governance, and other initiatives; and master data management products to create an authoritative single source of truth of business-critical data to reduce data related errors and remove redundancies. Its platform also includes customer and business 360 products to create, visualize, and browse comprehensive 360-degree views of business-critical data; data catalog products that enables customers to quickly find, access, and understand enterprise data using a simple Google-like search experience; and governance and privacy products that help users govern data, enable compliance with regulatory and corporate policies, and drive broader data consumption. The company also offers maintenance and professional services. Informatica Inc. was founded in 1993 and is headquartered in Redwood City, California.

Competitive Moat (Narrow)

Trend: Stable Breadth of data integration and management capabilities, Focus on enterprise-scale data challenges, AI-powered features for data quality and governance

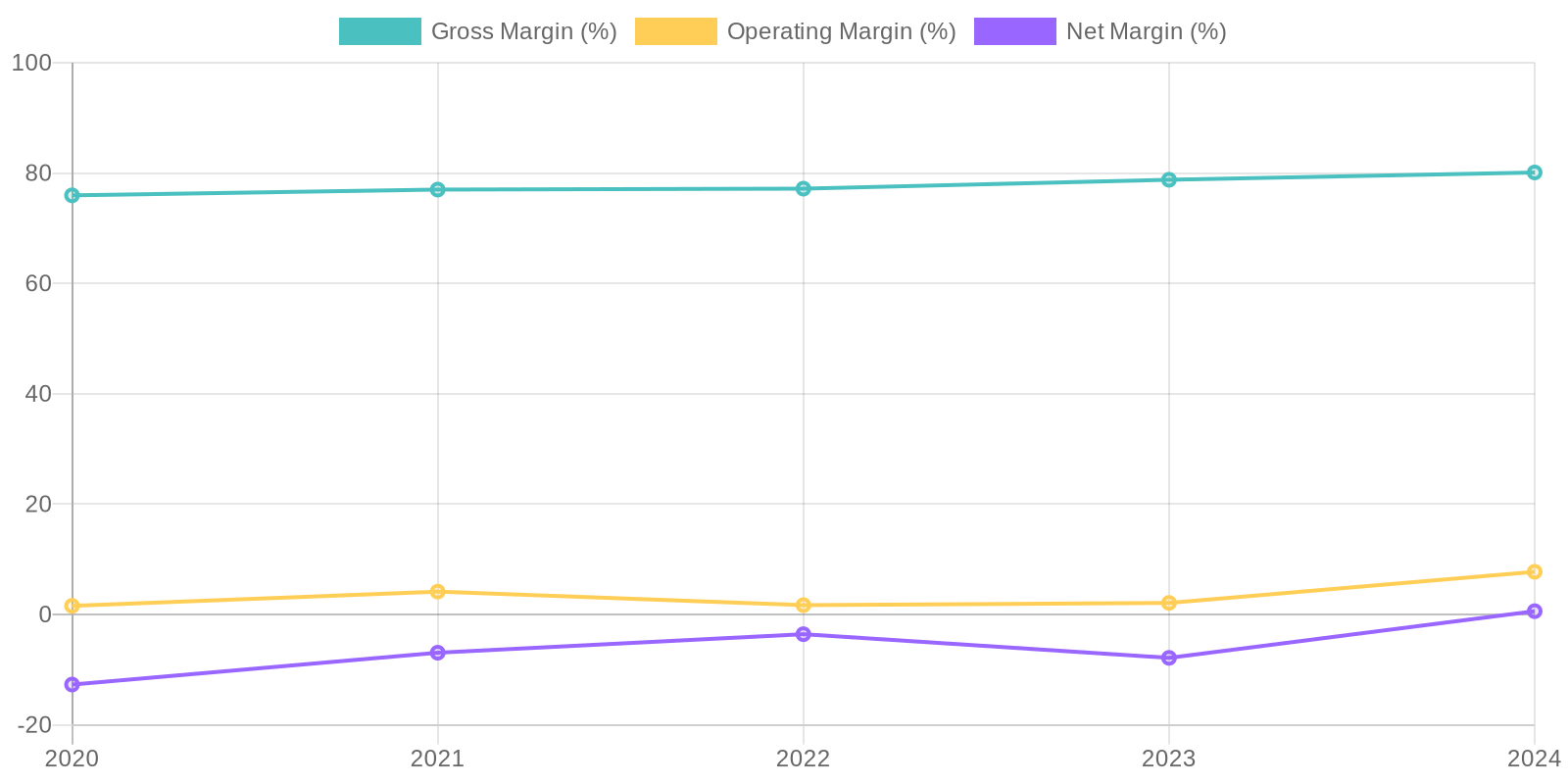

Calculating Return on Invested Capital (ROIC) and Return on Equity (ROE) requires more detailed data on invested capital. However, considering the recent improvements in net income and a relatively stable equity base, both ROIC and ROE likely improved in 2024 compared to prior loss-making years. Further investigation is warranted to confirm these calculations and assess the sustainability of these returns.

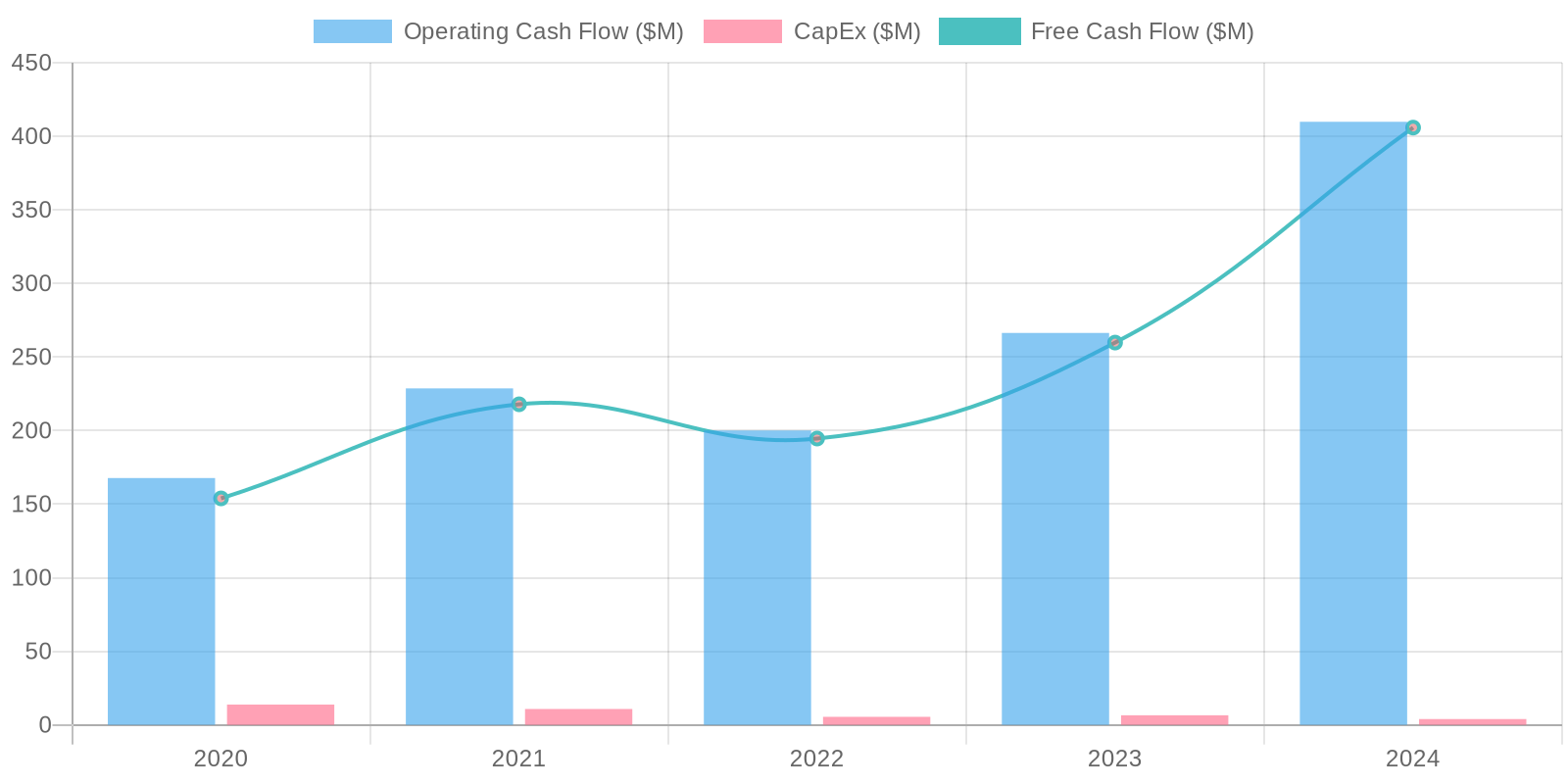

Calculating Return on Invested Capital (ROIC) and Return on Equity (ROE) requires more detailed data on invested capital. However, considering the recent improvements in net income and a relatively stable equity base, both ROIC and ROE likely improved in 2024 compared to prior loss-making years. Further investigation is warranted to confirm these calculations and assess the sustainability of these returns. The company showcases strong Free Cash Flow (FCF) generation, with $405.9 million in 2024 and $259.8 million in 2023, indicating an ability to convert revenue into cash. Capital expenditures (CAPEX) are relatively modest compared to operating cash flow, suggesting that the company does not require significant reinvestment to maintain its operations. Further analysis of the consistency of FCF generation and its relationship to revenue growth could reveal important insights into the company's financial health.

The company showcases strong Free Cash Flow (FCF) generation, with $405.9 million in 2024 and $259.8 million in 2023, indicating an ability to convert revenue into cash. Capital expenditures (CAPEX) are relatively modest compared to operating cash flow, suggesting that the company does not require significant reinvestment to maintain its operations. Further analysis of the consistency of FCF generation and its relationship to revenue growth could reveal important insights into the company's financial health.