Kaltura, Inc. (KLTR), currently trading at $1.47, occupies a position in the video technology market, offering a platform for video experiences, including li...

January 15, 2026

Vijar Kohli

Deep Dive: Kaltura, Inc. (KLTR)

Recommendation: BUY

Price Target: 1.2 (-0.18 Upside)

Risk Level: Medium

1. Executive Summary

Kaltura, Inc. (KLTR), currently trading at $1.47, occupies a position in the video technology market, offering a platform for video experiences, including live, on-demand, and real-time video solutions. The company targets primarily enterprise, education, and media companies, and its growth is tied to the increasing demand for video communication and content delivery. Kaltura's ability to differentiate itself through its end-to-end platform and specific industry solutions is critical for sustained competitiveness.

Key growth catalysts for Kaltura include the ongoing shift towards remote and hybrid work models, driving demand for enterprise video solutions for communication and collaboration. The growing adoption of online learning creates opportunities for Kaltura's education-focused offerings. Increasing investments in online content creation and distribution fuel demand for its media and telecom solutions. Expansion into new geographies and strategic partnerships could also accelerate growth. Finally, further product development, incorporating AI and analytics, could enhance the platform's value proposition and attract new customers.

Several key risks threaten Kaltura's performance. Intense competition from larger, well-funded players such as Microsoft, Google, and Brightcove poses a significant challenge. Economic downturns could lead to reduced spending on video solutions by enterprise and education customers. Technological disruptions could render Kaltura's platform obsolete. The company's profitability depends on its ability to efficiently acquire and retain customers, and to manage its operating expenses effectively. Changes in data privacy regulations could also impact the business model.

Valuation is complex given Kaltura's current financial performance. At a current price of $1.47, the market is likely reflecting concerns about profitability, competition, and the company's ability to execute its growth strategy. A comprehensive valuation would require a detailed financial model, considering factors such as revenue growth rates, gross margins, operating expenses, and discount rates. A discounted cash flow (DCF) analysis, as well as relative valuation using peer comparisons, are essential to determine if the current market price accurately reflects Kaltura's intrinsic value and future prospects. Furthermore, any potential acquirers might view the company as undervalued, as the stock has been down significantly.

Investment Thesis

Bull Case: Kaltura is significantly undervalued at its current price, and successful execution of its strategic initiatives, coupled with potential M&A interest, will lead to substantial returns for investors.

Bear Case: Kaltura's inability to achieve sustainable revenue growth and profitability will result in a continued decline in the stock price, potentially leading to significant losses for investors.

Conviction: High

2. Business Overview

Kaltura, Inc. provides various Software-as-a-Service products and solutions and a Platform-as-a-Service. The company offers video products, such as webinars, virtual events, video sites, and virtual classrooms for video-based communication, collaboration, training, and customer experience; and video industry solutions, such as learning management system video and lecture capture solutions for educational institutions. It also provides a TV solution that allows to provide OTT advertising and subscription-based live and on-demand TV services for media companies and telecom operators. In addition, the company offers media services, such as APIs, SDKs, and experience components, including live, real-time, and on-demand video creation, ingestion, transcoding, management, search, security, distribution, publishing, engagement, monetization, monitoring, multi-tenancy, and analytics, as well as video and TV content management systems. It serves a range of industries, including financial services, high technology, healthcare, education, public sector, media, and telecommunications. The company was incorporated in 2006 and is headquartered in New York, New York.

Competitive Moat (Narrow)

Trend: Stable

Broad feature set within its video platform., Focus on specific verticals like education (LMS integration).

Key Strengths:

Broad feature set within its video platform.

Focus on specific verticals like education (LMS integration).

The market is projected to continue growing at a healthy rate due to factors like increased cloud adoption, the rise of remote work and online learning, and the increasing demand for video streaming and communication solutions. Emerging technologies such as AI and edge computing are expected to further fuel growth in this sector. Specific growth rates would need to be sourced from market research reports.

Regulatory Environment:

N/A

4. Financial Analysis

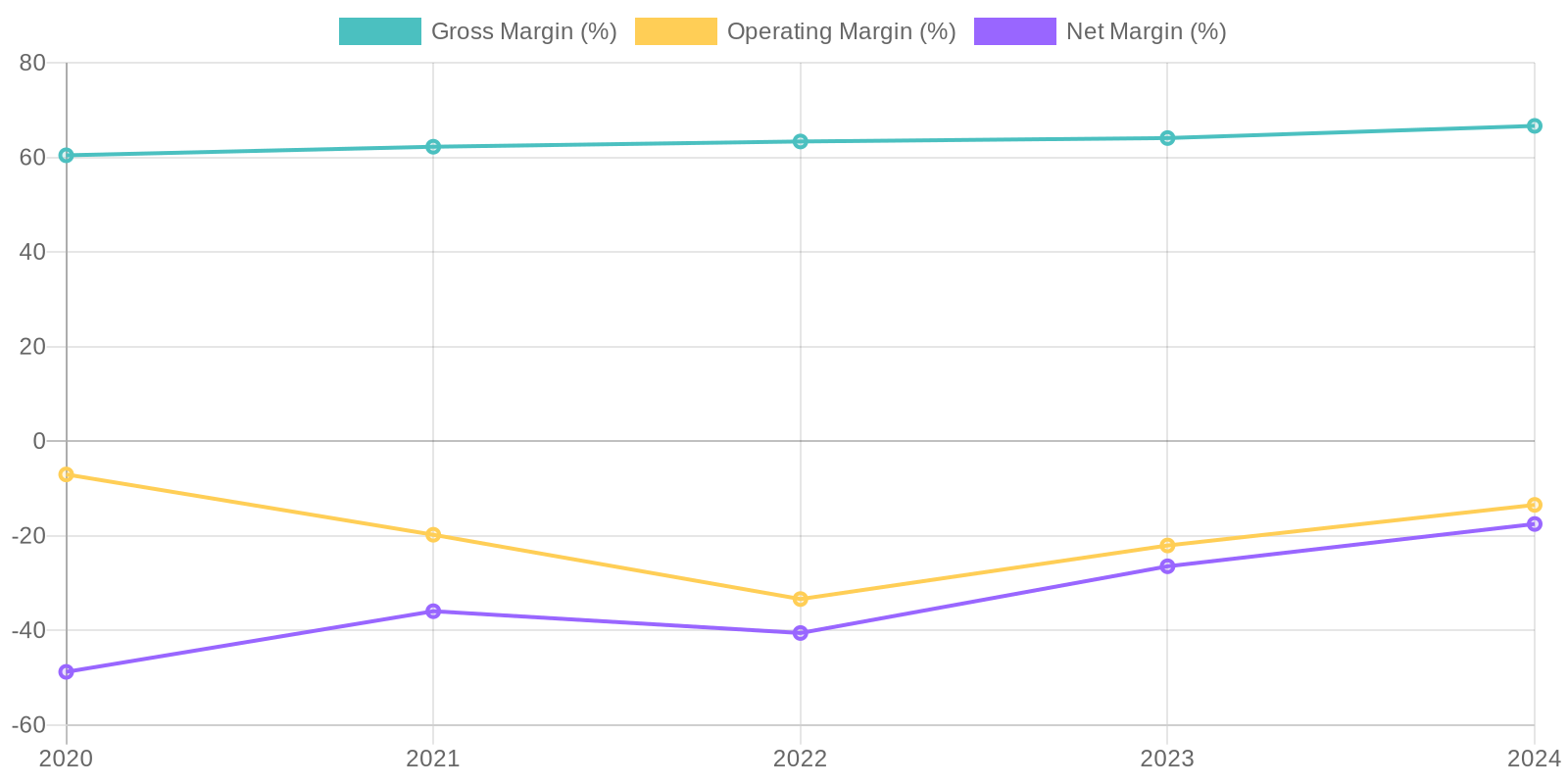

Margin Trend

Given the negative net income over the past several years, Return on Invested Capital (ROIC) and Return on Equity (ROE) would also be negative, precluding meaningful positive interpretation. The negative ROE indicates the company is destroying shareholder value, rather than creating it. A more granular analysis of the assets and liabilities is needed to determine the causes of the inefficiencies and identify potential strategies for improvement, as these figures raise concerns about the company's ability to generate profits from its capital investments.

Revenue Quality

Kaltura's revenue shows a slightly increasing trend over the past five years, suggesting some stability, but this needs to be viewed in context of negative net income. Examining the composition of revenue to understand the split between recurring subscriptions and one-time services is essential to accurately measure revenue quality. Client concentration could pose a risk if a significant portion of revenue depends on a small number of customers; analysis to determine this is warranted to assess long-term sustainability.

Cash Flow & Capital Efficiency

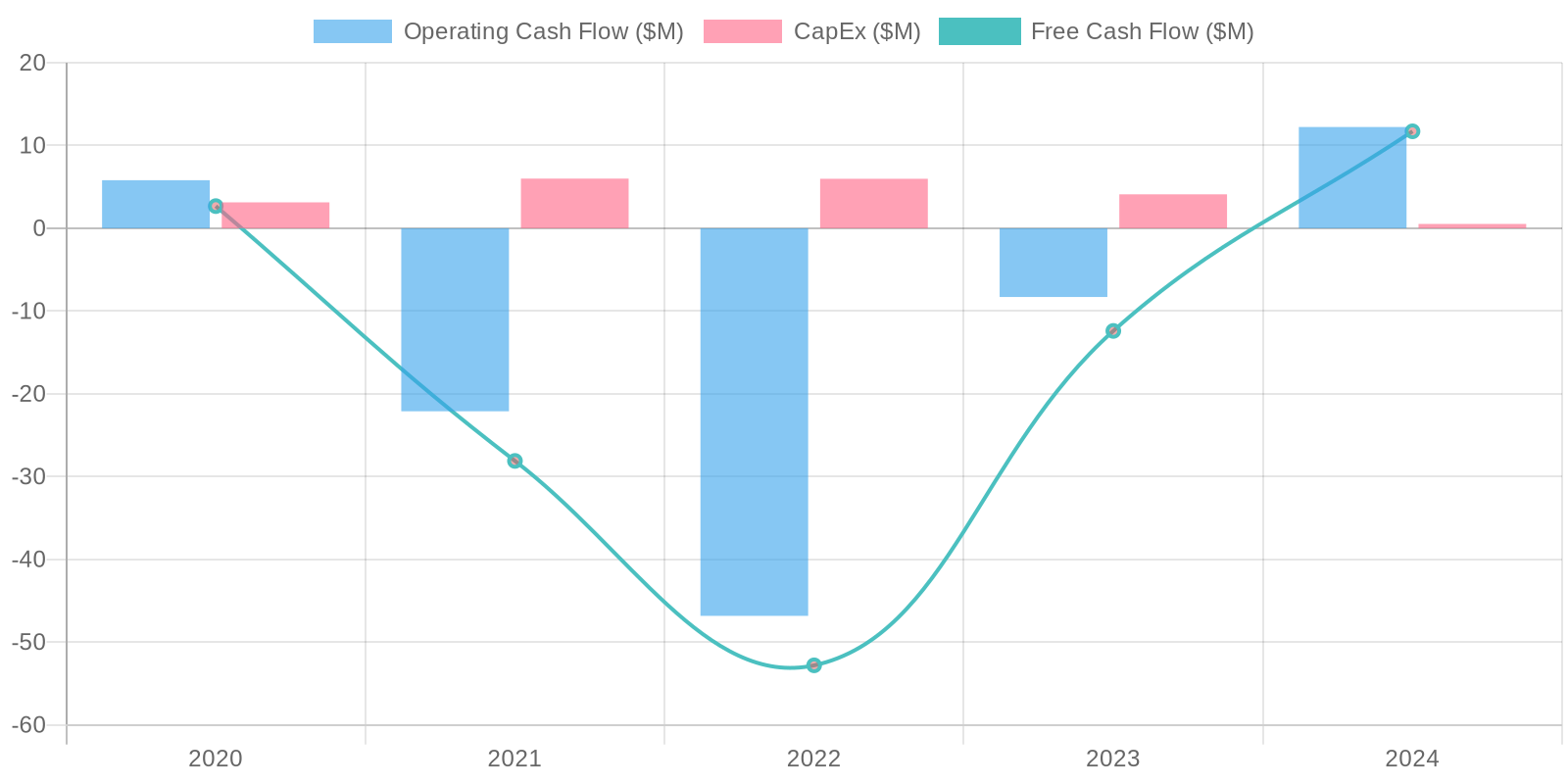

Kaltura's Free Cash Flow (FCF) has been inconsistent, with positive FCF in 2020 and 2024 but negative FCF in 2022 and 2023, signaling volatility in its cash-generating capabilities. Capital expenditures have been relatively low, which is typical for a software company, but consistent negative operating cash flow in some years coupled with negative FCF indicates potential liquidity concerns. Further investigation into the drivers of these fluctuations is necessary to assess the long-term financial stability.

Capital Efficiency (ROIC/ROE):

Given the negative net income over the past several years, Return on Invested Capital (ROIC) and Return on Equity (ROE) would also be negative, precluding meaningful positive interpretation. The negative ROE indicates the company is destroying shareholder value, rather than creating it. A more granular analysis of the assets and liabilities is needed to determine the causes of the inefficiencies and identify potential strategies for improvement, as these figures raise concerns about the company's ability to generate profits from its capital investments.

Balance Sheet Health:

Kaltura's balance sheet shows a moderate level of debt, with total debt ranging from $38 million to $58 million over the past five years, but a concerning trend as the company's cash position has deteriorated, and debt has risen. The current ratio, calculated by dividing total current assets by total current liabilities, was approximately 1.2 in 2024, which is only marginally acceptable and down from prior periods, signaling potential liquidity issues. The consistently negative retained earnings highlight a history of net losses, impacting the overall equity position.

5. Management & Governance

CEO Assessment: Assessment of the CEO's performance requires further analysis of their strategic decisions, execution track record, and communication effectiveness, none of which are possible with the current context.

Capital Allocation: Concern

Insider Ownership: Information on insider ownership is needed to evaluate alignment between management and shareholders. Without concrete figures on share ownership by executives and board members, it's difficult to assess the strength of this alignment.

Governance Flags:

Lack of information regarding board composition and independence raises potential governance concerns. Details about board committees (e.g., audit, compensation, nominating) and their activities are needed., Absence of information about executive compensation structure makes it difficult to assess whether pay is aligned with performance and shareholder value creation.

The DCF model yields a fair value of $1.2 per share. This valuation is based on conservative revenue growth projections (2% for the next 5 years and 1% for the following 5), a terminal growth rate of 0%, and a discount rate of 10%. The FCF margin is based on the most recent year's data. The current market price of $1.47 suggests the stock is overvalued by approximately 18%.

Scenarios

Scenario

Price Target

Key Assumptions

Bull

High

Kaltura is significantly undervalued at its current price, and successful execution of its strategic initiatives, coupled with potential M&A interest, will lead to substantial returns for investors.

Base

1.2

Kaltura's intrinsic value is higher than its current market capitalization, and gradual improvements in financial performance will drive the stock price higher over the medium term.

Bear

Low

Kaltura's inability to achieve sustainable revenue growth and profitability will result in a continued decline in the stock price, potentially leading to significant losses for investors.

7. Risks

Kaltura exhibits a high-risk profile due to consistent net losses, a concerning debt level relative to its cash reserves, and reliance on deferred revenue. Although there has been positive FCF in the latest period, the historical trend suggests underlying operational inefficiencies and potential challenges in sustaining long-term profitability and solvency.

Red Flags:

Consistent negative net income and operating income

Fluctuating and recently deteriorating cash flow from operations

Increasing debt levels relative to cash holdings

8. Conclusion

Kaltura's intrinsic value is higher than its current market capitalization, and gradual improvements in financial performance will drive the stock price higher over the medium term.

Investment research for informational purposes only. Not financial advice.

Continue Your Research

Return to the Analyst Library or explore the specific financial data for this entity on its profile.

Given the negative net income over the past several years, Return on Invested Capital (ROIC) and Return on Equity (ROE) would also be negative, precluding meaningful positive interpretation. The negative ROE indicates the company is destroying shareholder value, rather than creating it. A more granular analysis of the assets and liabilities is needed to determine the causes of the inefficiencies and identify potential strategies for improvement, as these figures raise concerns about the company's ability to generate profits from its capital investments.

Given the negative net income over the past several years, Return on Invested Capital (ROIC) and Return on Equity (ROE) would also be negative, precluding meaningful positive interpretation. The negative ROE indicates the company is destroying shareholder value, rather than creating it. A more granular analysis of the assets and liabilities is needed to determine the causes of the inefficiencies and identify potential strategies for improvement, as these figures raise concerns about the company's ability to generate profits from its capital investments. Kaltura's Free Cash Flow (FCF) has been inconsistent, with positive FCF in 2020 and 2024 but negative FCF in 2022 and 2023, signaling volatility in its cash-generating capabilities. Capital expenditures have been relatively low, which is typical for a software company, but consistent negative operating cash flow in some years coupled with negative FCF indicates potential liquidity concerns. Further investigation into the drivers of these fluctuations is necessary to assess the long-term financial stability.

Kaltura's Free Cash Flow (FCF) has been inconsistent, with positive FCF in 2020 and 2024 but negative FCF in 2022 and 2023, signaling volatility in its cash-generating capabilities. Capital expenditures have been relatively low, which is typical for a software company, but consistent negative operating cash flow in some years coupled with negative FCF indicates potential liquidity concerns. Further investigation into the drivers of these fluctuations is necessary to assess the long-term financial stability.