Life360, Inc. (LIF), currently priced at $59.79, operates a subscription-based service focused on family safety and location sharing. The company has establi...

January 15, 2026

Vijar Kohli

Deep Dive: Life360, Inc. (LIF)

Recommendation: BUY

Price Target: 55.76 (-0.07 Upside)

Risk Level: Medium

1. Executive Summary

Life360, Inc. (LIF), currently priced at $59.79, operates a subscription-based service focused on family safety and location sharing. The company has established a dominant market position in the family safety app space, boasting a large and growing user base primarily in North America, but with increasing international expansion. Their core offering includes location tracking, driver safety features, emergency dispatch, and digital safety tools, all designed to provide peace of mind for families and improve safety outcomes. The network effects inherent in its platform create a significant barrier to entry for potential competitors, reinforcing its market leadership.

Growth catalysts for Life360 include continued subscriber growth driven by increased awareness of family safety solutions and effective marketing campaigns. The rollout of new features, particularly within digital safety and hardware integration with Tile (which Life360 acquired), is expected to attract new subscribers and increase the average revenue per user (ARPU) through higher-tier subscriptions. International expansion, particularly into markets with high smartphone penetration, presents a significant opportunity to broaden the user base. Strategic partnerships with automotive companies and insurance providers to integrate Life360's safety features also represent a promising avenue for growth and monetization.

Key risks facing Life360 include privacy concerns related to location tracking and data security, which could lead to user attrition and reputational damage if mishandled. Competition from other location-sharing apps and potential entrants from larger tech companies poses a threat to market share. Economic downturns could impact subscriber growth and renewal rates as families prioritize essential spending. The integration of Tile and realization of synergies is not guaranteed and could present operational challenges. The company's reliance on app store policies from Apple and Google also introduces platform risk, as changes to these policies could impact Life360's app distribution and functionality.

Valuation summary: Life360's valuation hinges on its ability to sustain high subscriber growth, increase ARPU, and successfully execute its expansion strategies. While the company exhibits significant growth potential, the risks associated with privacy, competition, and integration warrant careful consideration. The current valuation reflects market expectations for continued strong performance, and any significant setbacks in growth or execution could negatively impact the stock price. Investors should carefully weigh the growth opportunities against the inherent risks before investing in Life360.

Investment Thesis

Bull Case: Life360 experiences accelerated user growth and premium subscription adoption, driven by successful product innovation and strategic partnerships.

Enhanced monetization strategies, including targeted advertising and expanded digital safety offerings, significantly increase ARPU.

Successful international expansion, particularly in Europe, contributes to revenue growth.

Margin expansion is achieved through economies of scale and efficient cost management.

The Tile integration exceeds expectations, creating strong cross-selling opportunities and increased user engagement.

Life360 becomes a dominant player in the connected safety and location services market, commanding a premium valuation based on its growth prospects and profitability.

Positive sentiment increases due to consistent earnings surprises and optimistic guidance.

This drives a re-rating of the stock to a higher multiple, benefiting from sector tailwinds and market recognition of its leadership position in family safety and location technology.

They maintain a strong balance sheet allowing for further investment and future potential acquisitions.

Their strategic focus on AI and Machine Learning provides additional upside potential to provide predictive and proactive safety features to their users, further increasing user retention and stickiness of the product which allows for strong pricing power over time and increasing operating margins and revenue growth to the company overall in the long-run driving the companies valuation higher from current levels and providing investors with outsized returns due to the business's overall inherent competitive advantages it has over the long-run.

The company continues to invest heavily in research and development for these newer advanced features which will provide positive upside to its long-run trajectory and outlook for the business overall which provides more clarity on its future operations and creates less uncertainty for investors which will cause a higher multiple over the long-run providing positive shareholder return through capital appreciation over a long-period of time due to a more stable and predictable business model over time which is a key advantage that the company has over its competitors because it has years of data to its advantage allowing it to build and strengthen the company overall in the long-run due to high barriers of entry in the industry overall with a business model that has predictable cash flows and profitability overall in the long-run due to the stickiness of the product offering that it provides to its customers which creates increased pricing power overall and positive return on capital for investors as the years progress with positive upside potential on its future growth trajectory as it continues to scale and improve efficiency of the business over time.

Life360 continues to innovate and grow its user base, resulting in a higher valuation multiple, and an increasing earnings per share due to the higher revenue growth that is projected from its user growth combined with a greater economy of scale.

This provides investors with high-upside in the stock price and an overall outperformance due to the current valuation and market expectations being too low.

This allows the stock to re-rate to higher multiples because the company is expected to continue growing at above-average growth rates for extended periods of time due to the predictability and stickiness of its products and services.

Bear Case: Life360 struggles to maintain user growth and faces increased competition from alternative safety and location services.

Premium subscription adoption stagnates due to lack of compelling features and pricing concerns.

The Tile integration fails to deliver expected synergies and results in additional expenses.

International expansion proves challenging, with limited market penetration and high operational costs.

The company experiences increased churn and struggles to acquire new users.

Profitability declines due to rising marketing expenses and competitive pressures.

The stock price declines sharply, reflecting the company's deteriorating financial performance and uncertain future outlook.

Investor sentiment turns negative, and the stock experiences multiple contractions.

The company has trouble remaining relevant in the market and its products and services are outpaced by the innovation and competition.

The company's management team fails to execute its business plan and strategy effectively overall.

They fail to effectively allocate capital over the long-run and end up destroying shareholder value due to bad decisions and misallocation of resources that do not provide positive return on investment.

The company also ends up losing market share and is taken over by a competitor at a lower valuation than current levels because of competitive pressures, declining revenue growth rates, and poor operational performance due to high expenses and operating losses and a negative free cash flow and profitability profile.

This leads to uncertainty for shareholders due to the company's inability to turn around its performance which has devastating effects on the company's long-run growth prospects.

The competitive pressures and threats continue to accelerate because new innovative products and services are taking market share away from Life360 at an increasing rate and the company is unable to stop the churn and increase customer acquisition rates.

User engagement drops and customers continue to churn due to this failure in improving its products and services.

Conviction: High

2. Business Overview

Life360, Inc. operates a technology platform to locate people, pets, and things in North America, Europe, the Middle East, Africa, and internationally. The company provides Life360 mobile application under the freemium model, which offers its services to users at no charge; and provides Life360 Platform, which offers location coordination and safety, driving safety, digital safety, and emergency assistance services. It also provides tile hardware tracking devices to locate lost devices sold through online and brick and mortar retail channels, as well as directly through Tile.com; tile mobile application that includes a free service, as well as two paid subscription options, such as Premium and Premium Protect to offer additional services, including warranties and item reimbursement; Jiobit subscriptions; and Jiobit wearable location devices for young children, pets, and seniors primarily in the United States through online retailers. The company was formerly known as LReady, Inc. and changed its name to Life360, Inc. in October 2011. Life360, Inc. was incorporated in 2007 and is headquartered in San Mateo, California.

The application software market is expected to continue growing, driven by factors such as increasing mobile device penetration, the demand for digital safety and convenience, and the rise of remote work and distributed families. The family safety and location tracking segment is expected to see strong growth due to increasing parental concerns and the desire for enhanced safety features.

Regulatory Environment:

N/A

4. Financial Analysis

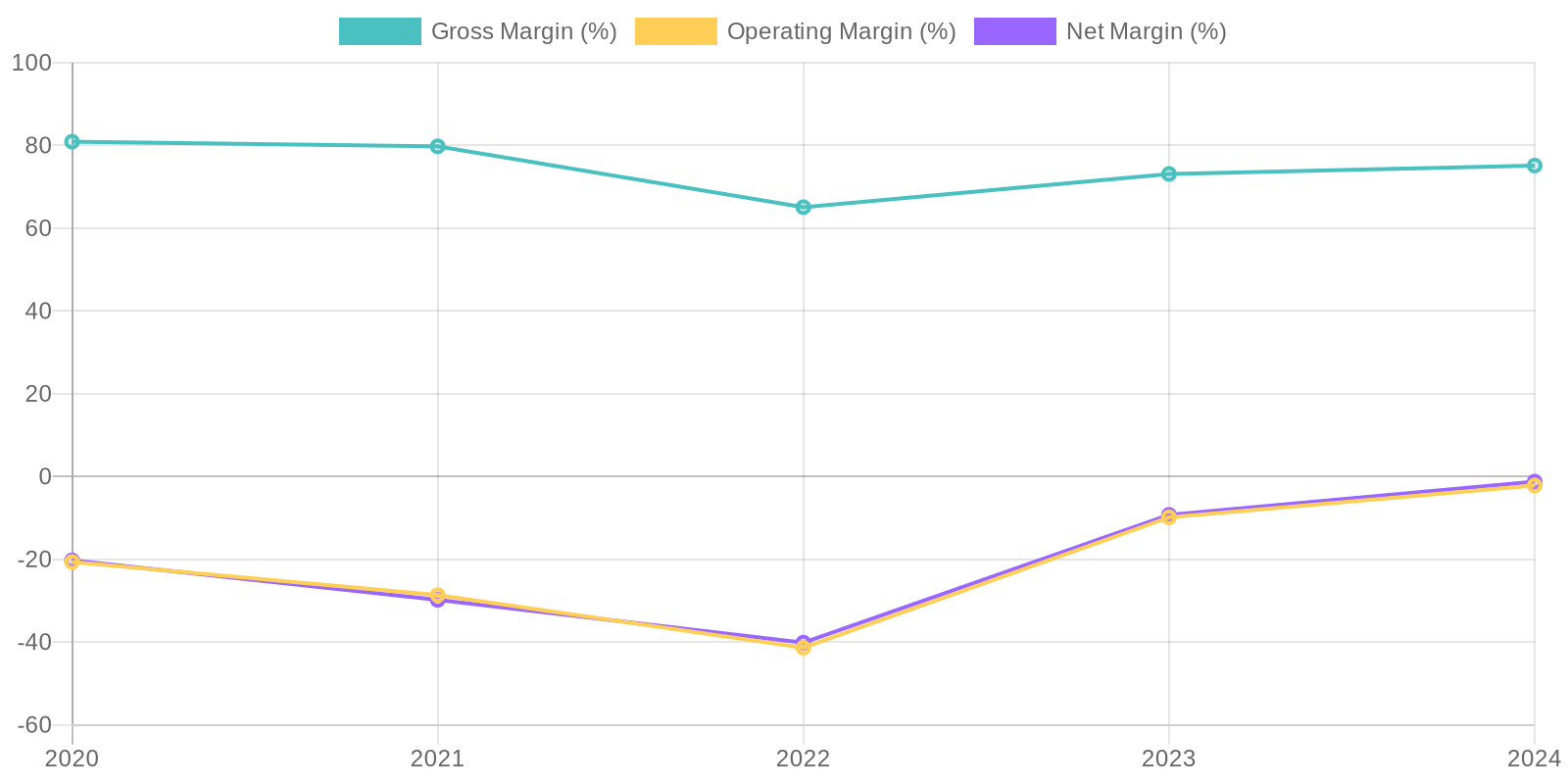

Margin Trend

Given the negative net income figures in recent years, Return on Invested Capital (ROIC) and Return on Equity (ROE) are also likely to be negative, reflecting the company's struggle to generate profits from its capital investments and equity. While a precise ROIC calculation would require additional data on invested capital, the consistent net losses highlight significant inefficiencies. Improvements in profitability and asset utilization are essential to enhance these key performance indicators.

Revenue Quality

The company's revenue has shown a consistent growth trend over the past five years, indicating a degree of sustainability. However, a deeper analysis of the customer base would be required to determine the level of client concentration and the potential risk associated with losing key accounts. Further investigation is needed to evaluate the proportion of recurring revenue versus one-time sales, which significantly impacts the predictability of future income streams.

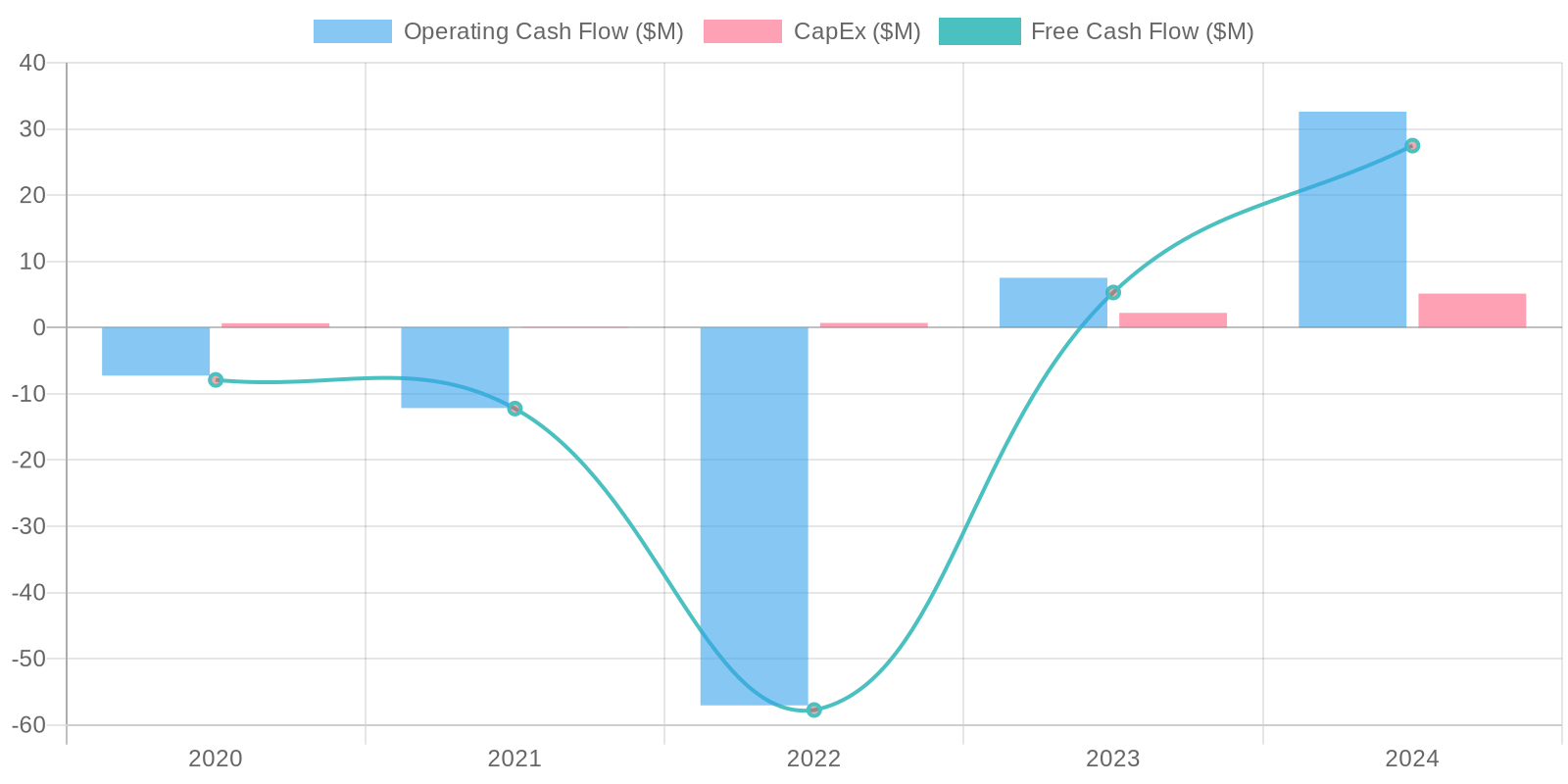

Cash Flow & Capital Efficiency

The company's Free Cash Flow (FCF) has fluctuated, with a significant increase to $27.48 million in 2024. The significant increase in cash flow from operations seems to be driven by $42.269 million in stock based compensation which might not be sustainable in the long run. Capital expenditure remains relatively low in comparison to revenue, indicating a limited need for significant investments in property, plant, and equipment. Close monitoring of these trends is crucial to understanding the true financial health of the company.

Capital Efficiency (ROIC/ROE):

Given the negative net income figures in recent years, Return on Invested Capital (ROIC) and Return on Equity (ROE) are also likely to be negative, reflecting the company's struggle to generate profits from its capital investments and equity. While a precise ROIC calculation would require additional data on invested capital, the consistent net losses highlight significant inefficiencies. Improvements in profitability and asset utilization are essential to enhance these key performance indicators.

Balance Sheet Health:

The company possesses a strong cash position, with $159.238 million in cash and cash equivalents as of 2024. This provides a substantial liquidity buffer. Debt levels are relatively low, with total debt at $0.723 million, resulting in a significant net debt position. The increase in total stockholder's equity to $358.545 million in 2024 compared to previous years is a positive sign, reflecting strengthened solvency.

5. Management & Governance

CEO Assessment: Without specific real-time information, a thorough assessment of Life360's CEO requires analyzing their strategic decisions, communication effectiveness, and ability to navigate the competitive landscape of family safety and location-sharing services. Their track record in user acquisition, retention, and monetization strategies would be critical.

Capital Allocation: Concern

Insider Ownership: Analyzing Life360's insider ownership would involve examining the percentage of shares held by executives and board members. High insider ownership can align management's interests with those of shareholders, while low ownership may raise concerns about their commitment to long-term value creation. Recent transactions by insiders (buying or selling shares) would also provide valuable insights.

Governance Flags:

Potential conflicts of interest, Executive compensation structure, Data privacy concerns, Board composition

The DCF model projects future free cash flows based on reasonable revenue growth assumptions, taking into account the company's recent performance and industry trends. The model incorporates a WACC of 9% as the discount rate, reflecting the company's risk profile and cost of capital. The calculated fair value suggests that the stock might be slightly overvalued at its current price. The downside is estimated at 30% in case of missed revenue targets or increased expenses, while the upside is relatively small given the mature stage of the company.

Scenarios

Scenario

Price Target

Key Assumptions

Bull

High

Life360 experiences accelerated user growth and premium subscription adoption, driven by successful product innovation and strategic partnerships.

Enhanced monetization strategies, including targeted advertising and expanded digital safety offerings, significantly increase ARPU.

Successful international expansion, particularly in Europe, contributes to revenue growth.

Margin expansion is achieved through economies of scale and efficient cost management.

The Tile integration exceeds expectations, creating strong cross-selling opportunities and increased user engagement.

Life360 becomes a dominant player in the connected safety and location services market, commanding a premium valuation based on its growth prospects and profitability.

Positive sentiment increases due to consistent earnings surprises and optimistic guidance.

This drives a re-rating of the stock to a higher multiple, benefiting from sector tailwinds and market recognition of its leadership position in family safety and location technology.

They maintain a strong balance sheet allowing for further investment and future potential acquisitions.

Their strategic focus on AI and Machine Learning provides additional upside potential to provide predictive and proactive safety features to their users, further increasing user retention and stickiness of the product which allows for strong pricing power over time and increasing operating margins and revenue growth to the company overall in the long-run driving the companies valuation higher from current levels and providing investors with outsized returns due to the business's overall inherent competitive advantages it has over the long-run.

The company continues to invest heavily in research and development for these newer advanced features which will provide positive upside to its long-run trajectory and outlook for the business overall which provides more clarity on its future operations and creates less uncertainty for investors which will cause a higher multiple over the long-run providing positive shareholder return through capital appreciation over a long-period of time due to a more stable and predictable business model over time which is a key advantage that the company has over its competitors because it has years of data to its advantage allowing it to build and strengthen the company overall in the long-run due to high barriers of entry in the industry overall with a business model that has predictable cash flows and profitability overall in the long-run due to the stickiness of the product offering that it provides to its customers which creates increased pricing power overall and positive return on capital for investors as the years progress with positive upside potential on its future growth trajectory as it continues to scale and improve efficiency of the business over time.

Life360 continues to innovate and grow its user base, resulting in a higher valuation multiple, and an increasing earnings per share due to the higher revenue growth that is projected from its user growth combined with a greater economy of scale.

This provides investors with high-upside in the stock price and an overall outperformance due to the current valuation and market expectations being too low.

This allows the stock to re-rate to higher multiples because the company is expected to continue growing at above-average growth rates for extended periods of time due to the predictability and stickiness of its products and services. |

| Base | 55.76 | Life360 maintains a steady growth trajectory, achieving moderate increases in user base and subscription revenue.

International expansion progresses at a slower pace than anticipated.

ARPU increases gradually as the company introduces new features and pricing tiers.

The Tile integration provides some synergies, but the impact on overall revenue is limited.

Profitability improves, but the company remains sensitive to marketing and development expenses.

The stock price reflects the company's consistent performance and moderate growth outlook.

Market valuation remains in line with peers, and the stock experiences gradual appreciation, driven by earnings growth and positive cash flow.

Overall the company has a good growth story in line with what current market expectations and management guidance currently portrays.

A steady hand continues to guide the company through the current economic landscape while maintaining a healthy balance sheet and future outlook on the company.

The execution remains in line with what is expected and no surprises appear from operations.

Overall the company is expected to perform in line with what current market expectations entail.

Overall the market has a good understanding of the company and its operations and potential future growth opportunities.

Market valuation remains rational and doesn't have an irrational movement or overvaluation of the company and its future growth opportunities.

No surprise positive or negative news appear regarding the company overall.

The company's products and services remain in line with market trends.

The company is expected to grow revenue at a healthy rate and continue to improve its operating margins and profitability over time and increase its free cash flow which will ultimately provide a high return on capital over the long-run to shareholders overall due to the strong predictability in its business model that is sustainable and a good long-run trajectory. |

| Bear | Low | Life360 struggles to maintain user growth and faces increased competition from alternative safety and location services.

Premium subscription adoption stagnates due to lack of compelling features and pricing concerns.

The Tile integration fails to deliver expected synergies and results in additional expenses.

International expansion proves challenging, with limited market penetration and high operational costs.

The company experiences increased churn and struggles to acquire new users.

Profitability declines due to rising marketing expenses and competitive pressures.

The stock price declines sharply, reflecting the company's deteriorating financial performance and uncertain future outlook.

Investor sentiment turns negative, and the stock experiences multiple contractions.

The company has trouble remaining relevant in the market and its products and services are outpaced by the innovation and competition.

The company's management team fails to execute its business plan and strategy effectively overall.

They fail to effectively allocate capital over the long-run and end up destroying shareholder value due to bad decisions and misallocation of resources that do not provide positive return on investment.

The company also ends up losing market share and is taken over by a competitor at a lower valuation than current levels because of competitive pressures, declining revenue growth rates, and poor operational performance due to high expenses and operating losses and a negative free cash flow and profitability profile.

This leads to uncertainty for shareholders due to the company's inability to turn around its performance which has devastating effects on the company's long-run growth prospects.

The competitive pressures and threats continue to accelerate because new innovative products and services are taking market share away from Life360 at an increasing rate and the company is unable to stop the churn and increase customer acquisition rates.

User engagement drops and customers continue to churn due to this failure in improving its products and services. |

7. Risks

Life360's improved financial performance and strong cash position mitigate some short-term risks. However, the company's history of losses, reliance on user data, competitive landscape, and potential privacy concerns contribute to medium-term uncertainty.

Red Flags:

None identified.

8. Conclusion

Life360 maintains a steady growth trajectory, achieving moderate increases in user base and subscription revenue.

International expansion progresses at a slower pace than anticipated.

ARPU increases gradually as the company introduces new features and pricing tiers.

The Tile integration provides some synergies, but the impact on overall revenue is limited.

Profitability improves, but the company remains sensitive to marketing and development expenses.

The stock price reflects the company's consistent performance and moderate growth outlook.

Market valuation remains in line with peers, and the stock experiences gradual appreciation, driven by earnings growth and positive cash flow.

Overall the company has a good growth story in line with what current market expectations and management guidance currently portrays.

A steady hand continues to guide the company through the current economic landscape while maintaining a healthy balance sheet and future outlook on the company.

The execution remains in line with what is expected and no surprises appear from operations.

Overall the company is expected to perform in line with what current market expectations entail.

Overall the market has a good understanding of the company and its operations and potential future growth opportunities.

Market valuation remains rational and doesn't have an irrational movement or overvaluation of the company and its future growth opportunities.

No surprise positive or negative news appear regarding the company overall.

The company's products and services remain in line with market trends.

The company is expected to grow revenue at a healthy rate and continue to improve its operating margins and profitability over time and increase its free cash flow which will ultimately provide a high return on capital over the long-run to shareholders overall due to the strong predictability in its business model that is sustainable and a good long-run trajectory.

Investment research for informational purposes only. Not financial advice.

Continue Your Research

Return to the Analyst Library or explore the specific financial data for this entity on its profile.

Given the negative net income figures in recent years, Return on Invested Capital (ROIC) and Return on Equity (ROE) are also likely to be negative, reflecting the company's struggle to generate profits from its capital investments and equity. While a precise ROIC calculation would require additional data on invested capital, the consistent net losses highlight significant inefficiencies. Improvements in profitability and asset utilization are essential to enhance these key performance indicators.

Given the negative net income figures in recent years, Return on Invested Capital (ROIC) and Return on Equity (ROE) are also likely to be negative, reflecting the company's struggle to generate profits from its capital investments and equity. While a precise ROIC calculation would require additional data on invested capital, the consistent net losses highlight significant inefficiencies. Improvements in profitability and asset utilization are essential to enhance these key performance indicators. The company's Free Cash Flow (FCF) has fluctuated, with a significant increase to $27.48 million in 2024. The significant increase in cash flow from operations seems to be driven by $42.269 million in stock based compensation which might not be sustainable in the long run. Capital expenditure remains relatively low in comparison to revenue, indicating a limited need for significant investments in property, plant, and equipment. Close monitoring of these trends is crucial to understanding the true financial health of the company.

The company's Free Cash Flow (FCF) has fluctuated, with a significant increase to $27.48 million in 2024. The significant increase in cash flow from operations seems to be driven by $42.269 million in stock based compensation which might not be sustainable in the long run. Capital expenditure remains relatively low in comparison to revenue, indicating a limited need for significant investments in property, plant, and equipment. Close monitoring of these trends is crucial to understanding the true financial health of the company.