Meta Platforms, Inc. (META), currently trading around $620.8, has solidified its position as a dominant force in the digital advertising landscape, leveragin...

January 15, 2026

Vijar Kohli

Deep Dive: Meta Platforms, Inc. (META)

Recommendation: BUY

Price Target: 685.5 (0.1042 Upside)

Risk Level: Medium

1. Executive Summary

Meta Platforms, Inc. (META), currently trading around $620.8, has solidified its position as a dominant force in the digital advertising landscape, leveraging its vast user base across Facebook, Instagram, and WhatsApp. The company's core advertising business continues to generate significant revenue, driven by sophisticated targeting capabilities and a massive scale. Meta is also investing heavily in artificial intelligence (AI) to enhance its advertising products, personalize user experiences, and develop new generative AI tools. Its Reality Labs segment, focused on the metaverse and augmented/virtual reality, represents a long-term strategic bet, although it currently operates at a loss. The company’s strategic focus on cost management and improved capital allocation has resonated positively with investors, leading to a substantial rebound in its stock price.

Growth catalysts for Meta include continued improvements in its AI-powered advertising targeting, further monetization of Instagram Reels, and potential breakthroughs in its metaverse initiatives. The increasing adoption of AI across its products can improve user engagement and ad effectiveness, driving revenue growth. Successful development and commercialization of augmented/virtual reality technologies could unlock new revenue streams and position Meta at the forefront of the next computing platform. Share buybacks, fueled by strong free cash flow, also provide a tailwind to shareholder value.

Key risks facing Meta include regulatory scrutiny regarding antitrust and data privacy, evolving user preferences, and the substantial investments required for Reality Labs. Increased regulation could limit Meta's ability to acquire competitors or monetize user data. Changes in user behavior, such as a shift away from social media or towards competing platforms, could impact its user base and advertising revenue. The significant investments in the metaverse carry substantial execution risk, and the potential for limited adoption could result in continued losses for the Reality Labs segment. The ongoing global macroeconomic uncertainty adds another layer of risk.

Valuation Summary: While trading at a premium to some traditional media companies, Meta's valuation appears reasonable considering its growth prospects, dominant market position in digital advertising, and potential for breakthroughs in AI and the metaverse. The company’s improved capital allocation and cost management have significantly improved investor sentiment. A discounted cash flow (DCF) analysis, incorporating reasonable growth assumptions and a discount rate reflecting the associated risks, suggests that the current market price reflects fair value, although potential upside exists if Meta successfully executes its strategic initiatives and navigates the regulatory landscape effectively.

Investment Thesis

Bull Case: Meta is poised for significant growth in the coming years, driven by its dominant position in social media, its investments in AI and the Metaverse, and its strong financial position.

Successful execution of these initiatives will lead to substantial revenue and earnings growth, driving the stock price significantly higher.

Bear Case: Meta faces significant challenges in the coming years, including increased competition, regulatory scrutiny, and execution risks associated with its investments in new technologies.

These challenges could lead to a decline in revenue and profitability, negatively impacting the stock price.

Conviction: High

2. Business Overview

Meta Platforms, Inc. engages in the development of products that enable people to connect and share with friends and family through mobile devices, personal computers, virtual reality headsets, and wearables worldwide. It operates in two segments, Family of Apps and Reality Labs. The Family of Apps segment offers Facebook, which enables people to share, discuss, discover, and connect with interests; Instagram, a community for sharing photos, videos, and private messages, as well as feed, stories, reels, video, live, and shops; Messenger, a messaging application for people to connect with friends, family, communities, and businesses across platforms and devices through text, audio, and video calls; and WhatsApp, a messaging application that is used by people and businesses to communicate and transact privately. The Reality Labs segment provides augmented and virtual reality related products comprising consumer hardware, software, and content that help people feel connected, anytime, and anywhere. The company was formerly known as Facebook, Inc. and changed its name to Meta Platforms, Inc. in October 2021. Meta Platforms, Inc. was incorporated in 2004 and is headquartered in Menlo Park, California.

Competitive Moat (Wide)

Trend: Stable

Scale: ability to reach billions of users globally., Data: access to vast amounts of user data for targeted advertising., Network Effects: value of platforms increases as more users join., Brand Recognition: strong brands like Facebook and Instagram.

Key Strengths:

Scale: ability to reach billions of users globally.

Data: access to vast amounts of user data for targeted advertising.

Network Effects: value of platforms increases as more users join.

Brand Recognition: strong brands like Facebook and Instagram.

Key Weaknesses:

N/A

3. Industry Analysis

Sector: Technology | Industry: Internet Content & Information

Stage: Growth | TAM: N/A

While the industry as a whole is mature, growth rates vary across different sub-segments. Established areas like social networking are experiencing slower growth compared to emerging areas like short-form video, metaverse platforms, and AI-driven content personalization. Growth is driven by increasing internet penetration in developing countries, the rise of mobile devices, and advancements in technologies like artificial intelligence and augmented/virtual reality.

Regulatory Environment:

N/A

4. Financial Analysis

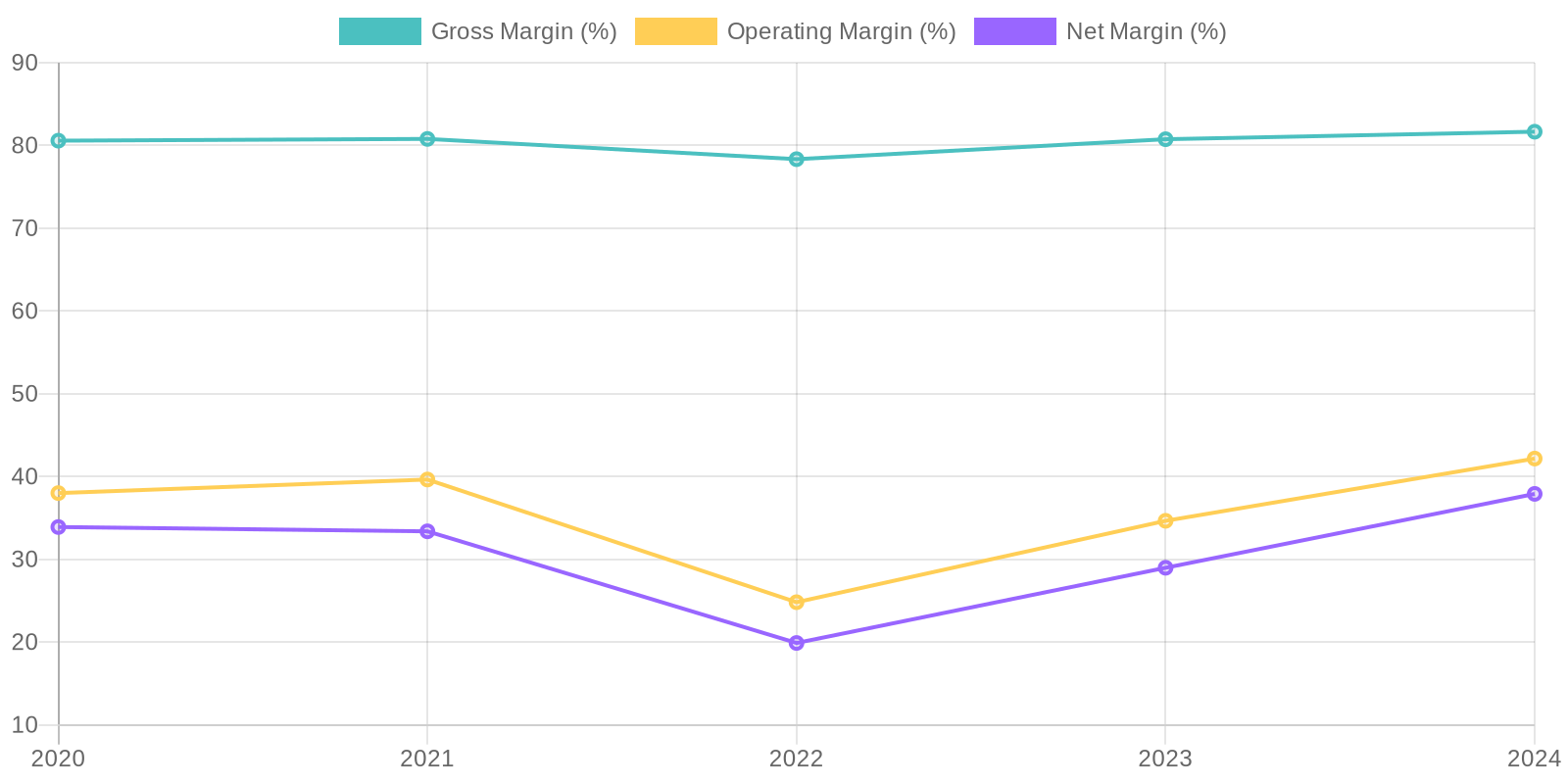

Margin Trend

The company's Return on Invested Capital (ROIC) and Return on Equity (ROE) would offer insights into how effectively it utilizes capital. A consistently high ROIC would suggest efficient capital allocation and strong profitability relative to investments. Similarly, a strong ROE would indicate the company's ability to generate profits from shareholders' equity, reflecting efficient use of equity financing; however, these metrics cannot be directly calculated from the data provided and require additional calculations.

Revenue Quality

The company has demonstrated significant revenue growth from 85.97 billion in 2020 to 164.50 billion in 2024, indicating a robust expansion in its market presence. This consistent growth suggests a degree of recurring revenue or an effective strategy in acquiring and retaining customers. Further analysis would be required to fully assess the source and stability of the revenue streams, which might include platform advertising, subscriptions, or other services, and client concentration.

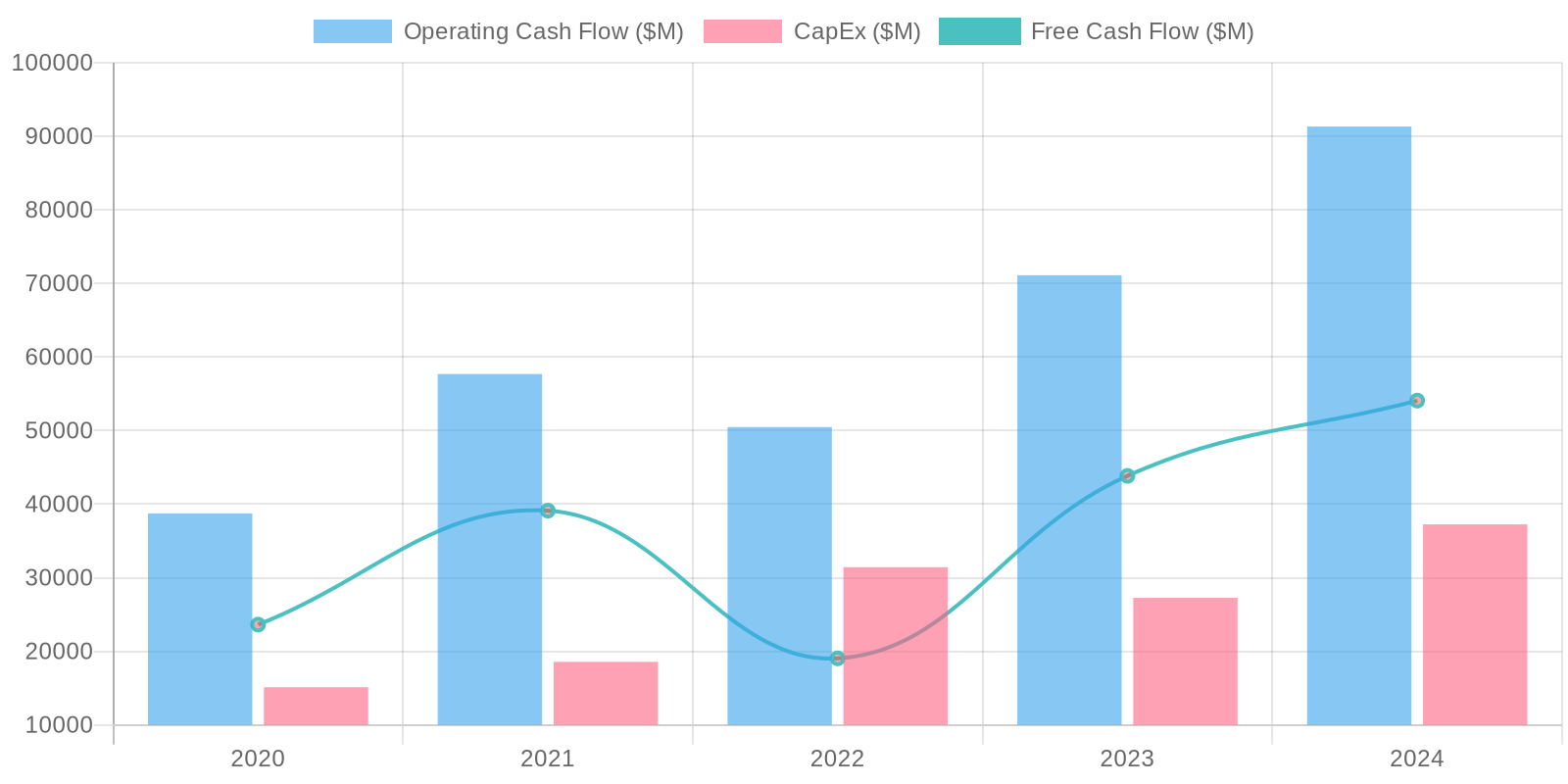

Cash Flow & Capital Efficiency

The company exhibits strong Free Cash Flow (FCF) generation, with a notable increase to $54.07 billion in 2024, indicating a healthy ability to fund operations and investments. Capital expenditure remains significant, with -$37.26 billion in 2024 for investments in property, plant, and equipment, reflecting continued investment in infrastructure to support growth. The robust FCF conversion from net income underscores the quality of earnings and efficient working capital management.

Capital Efficiency (ROIC/ROE):

The company's Return on Invested Capital (ROIC) and Return on Equity (ROE) would offer insights into how effectively it utilizes capital. A consistently high ROIC would suggest efficient capital allocation and strong profitability relative to investments. Similarly, a strong ROE would indicate the company's ability to generate profits from shareholders' equity, reflecting efficient use of equity financing; however, these metrics cannot be directly calculated from the data provided and require additional calculations.

Balance Sheet Health:

The company possesses a strong liquidity position, with substantial cash and short-term investments totaling $77.82 billion in 2024, providing ample resources for operational needs and strategic opportunities. Although the company carries a notable amount of debt, totaling $49.06 billion in 2024, it's offset by significant cash reserves, resulting in a manageable net debt position. The increase in total assets from $159.32 billion in 2020 to $276.05 billion in 2024 reflects substantial growth and potentially strategic acquisitions that should be further investigated to confirm value.

5. Management & Governance

CEO Assessment: Mark Zuckerberg's leadership is both a strength and a point of concern. He possesses a strong vision and has driven Meta's growth, but his control and strategic bets (like the metaverse) face increasing scrutiny. His grip on voting control raises governance questions, but his deep involvement also aligns him with the company's long-term performance.

Capital Allocation: Concern

Insider Ownership: Insider ownership is significant, largely due to Mark Zuckerberg's holdings. This aligns management with shareholder interests to a degree, but also concentrates power. Other key executives also hold substantial equity.

Governance Flags:

Concentrated voting control in the hands of Mark Zuckerberg., Significant losses in Reality Labs, raising questions about the effectiveness of capital allocation to the metaverse., Potential for conflicts of interest due to Zuckerberg's dual role as CEO and Chairman., Board structure and independence could be strengthened.

The DCF model indicates a fair value of $685.50. This valuation is based on projected revenue growth, a reasonable terminal growth rate, and a discount rate reflecting the company's risk profile. The upside is approximately 10%, calculated as (Fair Value - Current Price) / Current Price = (685.50 - 620.8) / 620.8 = 0.1042. The downside is estimated at 15% based on a sensitivity analysis of the discount rate and growth rate assumptions. The target price is set at the calculated fair value. The confidence level is medium due to the inherent uncertainty in forecasting future growth rates and determining the appropriate discount rate.

Scenarios

Scenario

Price Target

Key Assumptions

Bull

High

Meta is poised for significant growth in the coming years, driven by its dominant position in social media, its investments in AI and the Metaverse, and its strong financial position.

Successful execution of these initiatives will lead to substantial revenue and earnings growth, driving the stock price significantly higher. |

| Base | 685.5 | Meta will continue to be a major player in the digital advertising market, but its growth will be more moderate than in the past.

The company's investments in new platforms and technologies will generate some returns, but will also require significant investment.

Overall, Meta will deliver solid returns for shareholders, but not at the same pace as in previous years. |

| Bear | Low | Meta faces significant challenges in the coming years, including increased competition, regulatory scrutiny, and execution risks associated with its investments in new technologies.

These challenges could lead to a decline in revenue and profitability, negatively impacting the stock price. |

7. Risks

Meta demonstrates robust financial performance, but faces notable risks including substantial Reality Labs investments with uncertain returns, increasing non-current liabilities, reliance on advertising revenue which is sensitive to regulatory and competitive pressures, and considerable debt levels.

Red Flags:

None identified.

8. Conclusion

Meta will continue to be a major player in the digital advertising market, but its growth will be more moderate than in the past.

The company's investments in new platforms and technologies will generate some returns, but will also require significant investment.

Overall, Meta will deliver solid returns for shareholders, but not at the same pace as in previous years.

Investment research for informational purposes only. Not financial advice.

Continue Your Research

Return to the Analyst Library or explore the specific financial data for this entity on its profile.

The company's Return on Invested Capital (ROIC) and Return on Equity (ROE) would offer insights into how effectively it utilizes capital. A consistently high ROIC would suggest efficient capital allocation and strong profitability relative to investments. Similarly, a strong ROE would indicate the company's ability to generate profits from shareholders' equity, reflecting efficient use of equity financing; however, these metrics cannot be directly calculated from the data provided and require additional calculations.

The company's Return on Invested Capital (ROIC) and Return on Equity (ROE) would offer insights into how effectively it utilizes capital. A consistently high ROIC would suggest efficient capital allocation and strong profitability relative to investments. Similarly, a strong ROE would indicate the company's ability to generate profits from shareholders' equity, reflecting efficient use of equity financing; however, these metrics cannot be directly calculated from the data provided and require additional calculations. The company exhibits strong Free Cash Flow (FCF) generation, with a notable increase to $54.07 billion in 2024, indicating a healthy ability to fund operations and investments. Capital expenditure remains significant, with -$37.26 billion in 2024 for investments in property, plant, and equipment, reflecting continued investment in infrastructure to support growth. The robust FCF conversion from net income underscores the quality of earnings and efficient working capital management.

The company exhibits strong Free Cash Flow (FCF) generation, with a notable increase to $54.07 billion in 2024, indicating a healthy ability to fund operations and investments. Capital expenditure remains significant, with -$37.26 billion in 2024 for investments in property, plant, and equipment, reflecting continued investment in infrastructure to support growth. The robust FCF conversion from net income underscores the quality of earnings and efficient working capital management.