Mitek Systems (MITK) currently trades at $10.09, reflecting its position as a leading provider of digital identity verification solutions. The company's core...

January 15, 2026

Vijar Kohli

Deep Dive: Mitek Systems, Inc. (MITK)

Recommendation: BUY

Price Target: 11.5 (13.97 Upside)

Risk Level: Medium

1. Executive Summary

Mitek Systems (MITK) currently trades at $10.09, reflecting its position as a leading provider of digital identity verification solutions. The company's core technology leverages advanced AI and machine learning to verify identities through mobile capture and authentication, serving a diverse client base across financial services, fintech, and government sectors. Mitek's market position is strengthened by its established relationships with major financial institutions and its continuous innovation in identity verification technology, crucial in a world increasingly vulnerable to fraud. The demand for robust identity verification is driving growth, as businesses seek to onboard customers securely and comply with ever-tightening regulatory requirements.

Several growth catalysts exist for Mitek. Firstly, the increasing adoption of digital banking and online transactions fuels the need for secure remote identity verification. As more industries digitize their processes, Mitek's solutions become even more critical. Secondly, geographic expansion presents a significant opportunity. While Mitek has a strong presence in North America, expanding its reach into Europe and Asia will unlock new markets and revenue streams. Furthermore, the company is actively investing in research and development to enhance its AI capabilities and develop new products, such as advanced fraud detection tools, which can drive future growth.

Key risks facing Mitek include intense competition from both established players and emerging startups in the identity verification space. The rapid pace of technological innovation also poses a risk, as Mitek must continuously adapt to stay ahead of evolving fraud tactics and maintain its competitive edge. Economic downturns could negatively impact customer spending on identity verification solutions. Regulatory changes in different jurisdictions regarding data privacy and security also present challenges, potentially requiring costly adjustments to its technology and operations. Failure to maintain data security or comply with these regulations could result in reputational damage and significant fines.

Valuation of Mitek is complex. While specific financial details were not provided, generally, companies in the SaaS and cybersecurity sectors are often valued based on metrics such as revenue growth, recurring revenue, and customer lifetime value. A detailed financial model would be required for precise valuation. Based on its market position and growth potential, Mitek likely commands a premium valuation. Investors should carefully consider the risk factors, including intense competition and the ever-changing regulatory landscape, before making any investment decisions.

Investment Thesis

Bull Case: Mitek benefits from the increasing need for secure and convenient digital identity verification.

Strong growth in identity verification segment, driven by increased online transactions and regulatory compliance, leading to revenue exceeding expectations.

Successful integration of new AI-powered fraud detection technologies and expansion into new markets (e.g., government sector) boosting growth.

Improved profitability due to operating leverage and cost efficiencies.

Potential acquisition target due to its valuable technology and market position.

Stock buybacks will likely happen when debt is paid down boosting shareholder value.

They have a history of making opportunistic investments with their large cash hoard and conservative approach.

Mobile deposit is a very sticky product and has created an industry moat for the company.

The switch to the cloud should yield better financial performance as legacy systems are expensive to maintain, this should yield better margins in the long run as well as new products being rolled out and easier to manage with a more technologically advanced system from the old one.

The company has a lot of financial flexibility which will enable them to weather any type of storm to their balance sheet and be opportunistic when the time is right to add value for shareholders.

Their transition to a subscription based model should result in higher margins and less volatile earnings making the business more predictable and a better investment than the current business model.

The macro environment is in favor of this company and they have been taking advantage of the opportunities that have come their way and should continue to execute the way they have been and boost future growth and profitability going forward.

The CEO has a solid track record of making the right decisions for the company as well as being conservative and financially responsible with the company and has helped produce a good balance sheet with financial flexibility.

Shareholder friendly management team that looks to create value for its shareholders and continue to put their best foot forward to help benefit the company and their future goals and long term goals to enhance shareholder value.

They have a solid record of beating analyst expectations and conservative guidance.

They should continue to beat earnings and surprise to the upside as the business environment has been favorable and continues to play in their favor.

With the advancement of fraud they have been on top of these problems and continue to innovate and put themselves in the best position to help prevent fraud and keep customers at bay and their retention rate is very good in comparison to their competitors.

They have a sticky product and their solutions are very robust and they are always innovating to help make the business better for shareholders and their customers who they serve in all ends of their business and consumer clients.

There is a transition for businesses to operate online and their services allow for digital businesses to operate smoothly.

They have great upside in the long run if all their plans materialize and a great return on investment when looking at their future goals and expectations for the business.

Bear Case: Increased competition in the digital identity verification market leading to pricing pressure and reduced market share.

Slower-than-expected adoption of digital identity solutions due to regulatory hurdles or consumer resistance.

Cybersecurity breaches or data privacy concerns damaging Mitek's reputation and leading to customer attrition.

Economic downturn impacting financial institutions and reducing demand for Mitek's solutions.

The company has high debt levels and could default on their debt.

Competition could take market share and pricing pressure could become a problem.

Macroeconomic pressures could hurt their customers who may not want to use Mitek's products as much anymore.

Key members may leave the company and hurt financial performance.

There is a risk that the innovation process is slow and competitors are catching up and Mitek will be at a disadvantage and lack of innovation to maintain future growth.

Overall financial performance will continue to worsen as their customers continue to dwindle as well as performance for future growth not materializing.

Overall performance will continue to worsen as their systems are not efficient enough and lack behind competitors with the transition not being as efficient.

A slow innovation and bad management could be a problem for the company and create a big risk and hurt shareholders.

Conviction: High

2. Business Overview

Mitek Systems, Inc. develops, markets, and sells mobile image capture and digital identity verification solutions in the United States, Europe, Latin America, and internationally. The company's solutions are embedded in native mobile apps and web browsers to facilitate digital consumer experiences. It offers Mobile Deposit that enables individuals and businesses to remotely deposit checks using their camera-equipped smartphone or tablet; and Mobile Verify, an identity verification solution that is integrated into mobile apps, mobile websites, and desktop applications. The company also provides Mobile Fill, which includes automatic image capture, minimizes the numbers of clicks, and expedites form fill completion; and MiSnap, a mobile-capture software development kit that enables an intuitive user experience and instant capture of quality images of identity documents and checks. In addition, it offers CheckReader that enables financial institutions to automatically extract data from checks; Check Fraud Defender, an AI-powered and cloud-hosted model for fighting check fraud; and Check Intelligence that enables financial institutions to automatically extract data from a check image received across any deposit channel, including branch, ATM, remote deposit capture, and mobile. Further, the company provides ID_CLOUD, an automated identity verification solution that is integrated into a customers' application to read and validate identity documents; IDLive Face, a passive facial liveness detection product; IDVoice, a robust AI-driven voice biometric engine; IDLive Voice that helps stop spoofing attacks on voice biometric systems; and IDLive Doc that works to fight fraud related to digitally displayed document images. Mitek Systems, Inc. was incorporated in 1986 and is based in San Diego, California.

Competitive Moat (Narrow)

Trend: Stable

Proprietary technology in mobile check deposit and identity verification., Strong relationships with financial institutions., Integration of AI for fraud detection.

Key Strengths:

Proprietary technology in mobile check deposit and identity verification.

The application software market, especially in areas like digital identity verification, is projected to continue its strong growth trajectory. Factors driving this growth include the increasing adoption of mobile banking, the rise of e-commerce, heightened security concerns, and stricter regulatory requirements. Growth rates are expected to be in the double digits annually for the next 5-7 years, especially in developing economies.

Regulatory Environment:

N/A

4. Financial Analysis

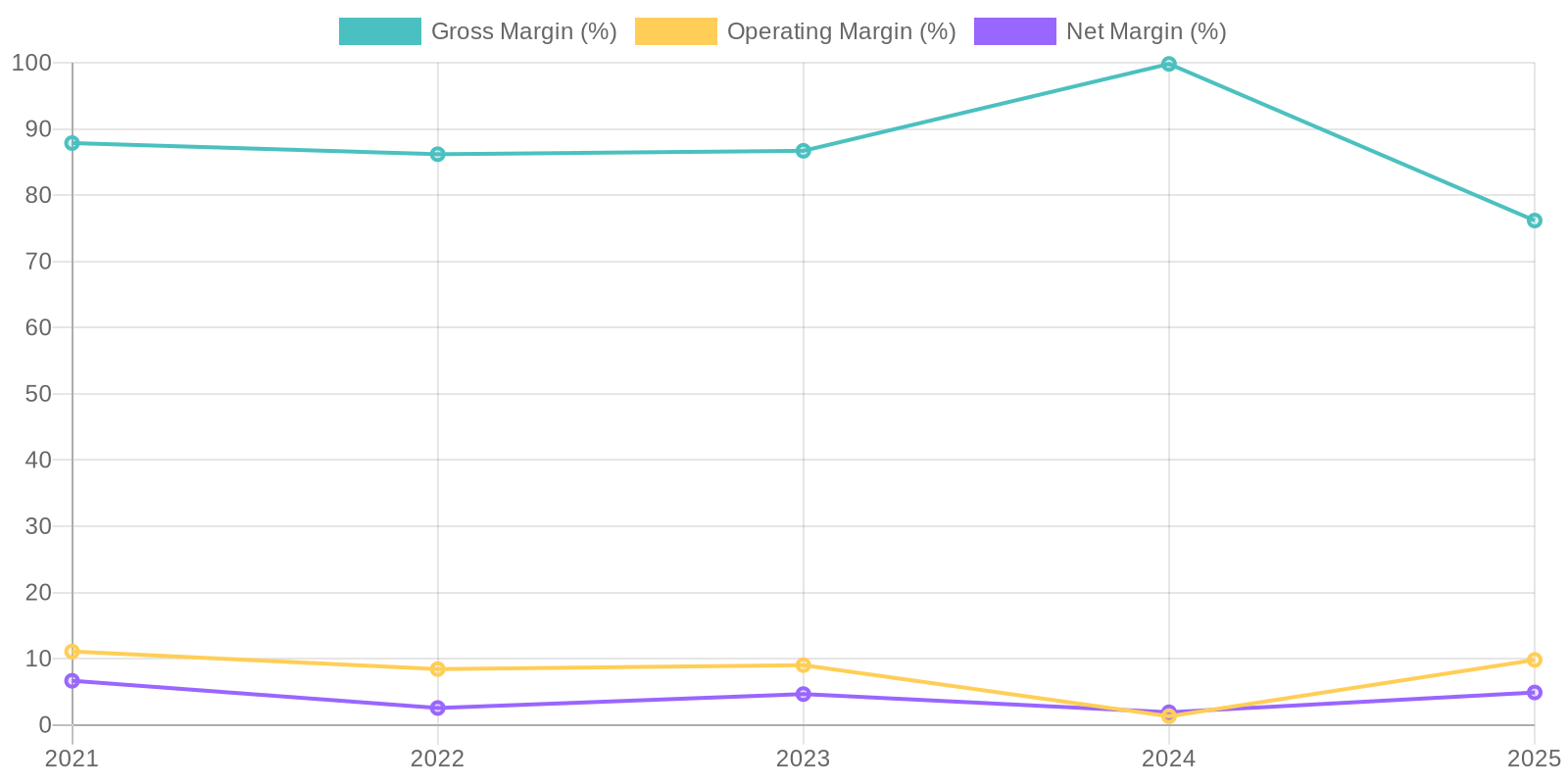

Margin Trend

Calculating Return on Invested Capital (ROIC) and Return on Equity (ROE) requires more detailed data on invested capital and equity, respectively, but based on the provided financials, we can infer some trends. The net income and total equity figures suggest that ROE has fluctuated significantly, especially with negative retained earnings impacting equity. Similarly, while we don't have explicit invested capital figures, the changes in operating income relative to asset bases suggest variability in ROIC, potentially reflecting changes in asset utilization and profitability.

Revenue Quality

The company's revenue stream demonstrates consistent growth over the past five years, suggesting a solid foundation in the market. While the data provided does not explicitly detail client concentration or the recurring nature of revenue, the steady increase implies a degree of customer retention or successful acquisition strategies. Further investigation would be needed to determine the precise sources and stickiness of this revenue, especially identifying if revenue recognition policies are consistent.

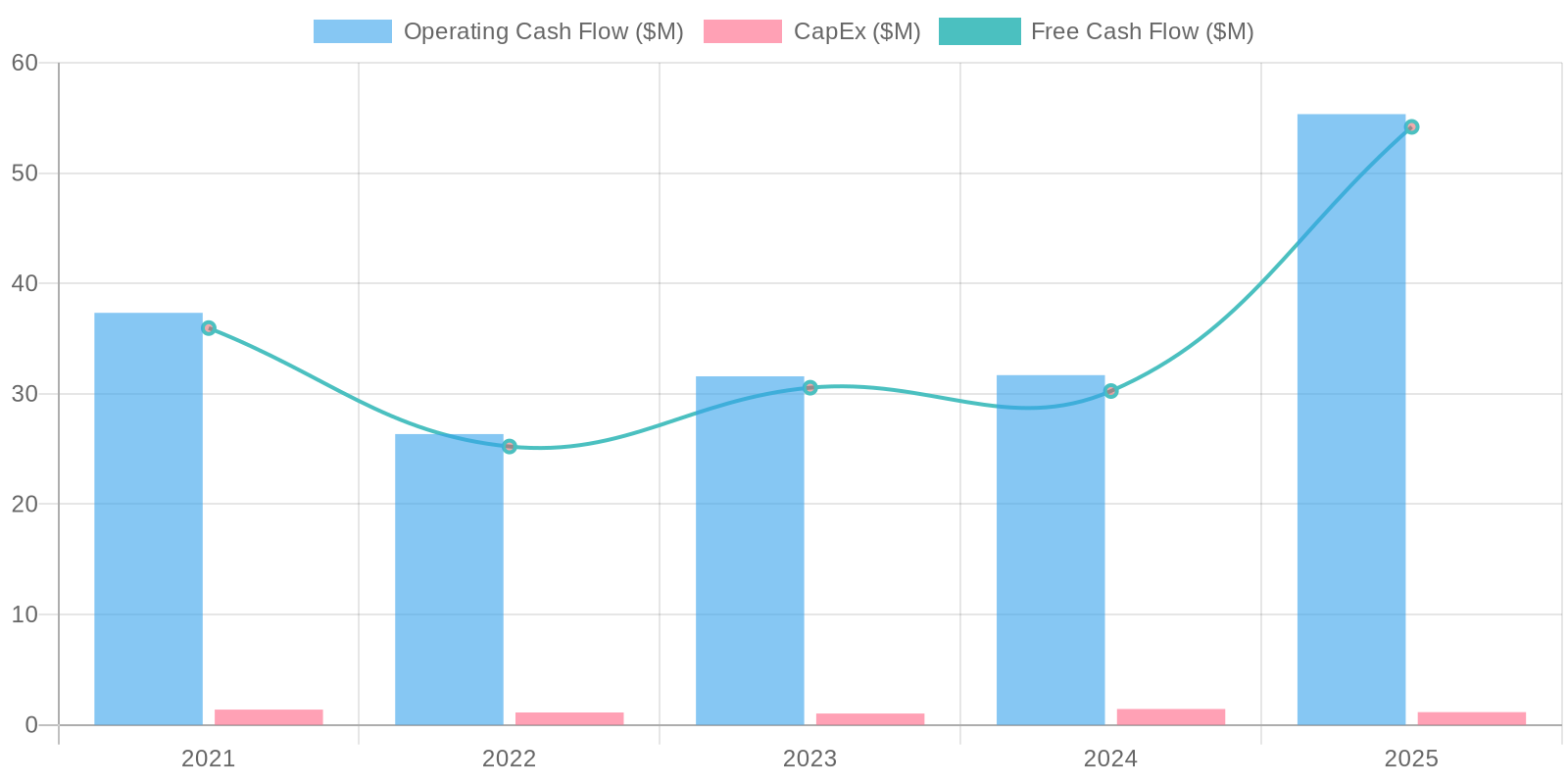

Cash Flow & Capital Efficiency

The company has demonstrated positive Free Cash Flow (FCF) in each of the past five years, reflecting the ability to generate cash after accounting for capital expenditures. In 2025, FCF stood at $54.185 million, a significant increase from $30.25 million in 2024. Capital expenditure has been consistently managed, generally being around $1 million each year, indicating a relatively low capital intensity in their business operations.

Capital Efficiency (ROIC/ROE):

Calculating Return on Invested Capital (ROIC) and Return on Equity (ROE) requires more detailed data on invested capital and equity, respectively, but based on the provided financials, we can infer some trends. The net income and total equity figures suggest that ROE has fluctuated significantly, especially with negative retained earnings impacting equity. Similarly, while we don't have explicit invested capital figures, the changes in operating income relative to asset bases suggest variability in ROIC, potentially reflecting changes in asset utilization and profitability.

Balance Sheet Health:

The company's debt levels are relatively high, with total debt at $159.486 million in 2025, exceeding its cash and cash equivalents of $154.153 million. This high level of debt could pose risks if the company faces difficulties in servicing its debt obligations. Liquidity, as measured by current ratio (current assets divided by current liabilities), is approximately 1.19 in 2025, suggesting the company has sufficient current assets to cover its current liabilities, but the high short-term debt should be monitored.

5. Management & Governance

CEO Assessment: Based on available information, an assessment of the current CEO's performance is not possible. A thorough analysis would require access to internal performance metrics and strategic decision-making processes. Publicly available information is insufficient.

Capital Allocation: Concern

Insider Ownership: Determining the precise level of insider ownership and its alignment with shareholder interests requires a review of the latest proxy statements and SEC filings. Analyze ownership stake by key executives and board members.

Governance Flags:

Lack of information to assess board independence and oversight effectiveness., Need to review executive compensation structure to ensure alignment with long-term shareholder value creation.

The DCF model, using the assumptions above, yields a fair value of $11.50. The revenue multiple approach, applying a 3.5x multiple to the 2025 revenue of $179.69 million, results in an enterprise value that, when adjusted for net debt, is consistent with the DCF valuation. Given the relatively stable historical performance and the nature of the software business, the DCF model offers a reasonable estimate of the company's intrinsic value. However, future growth depends on innovation and competition, which adds uncertainty.

Scenarios

Scenario

Price Target

Key Assumptions

Bull

High

Mitek benefits from the increasing need for secure and convenient digital identity verification.

Strong growth in identity verification segment, driven by increased online transactions and regulatory compliance, leading to revenue exceeding expectations.

Successful integration of new AI-powered fraud detection technologies and expansion into new markets (e.g., government sector) boosting growth.

Improved profitability due to operating leverage and cost efficiencies.

Potential acquisition target due to its valuable technology and market position.

Stock buybacks will likely happen when debt is paid down boosting shareholder value.

They have a history of making opportunistic investments with their large cash hoard and conservative approach.

Mobile deposit is a very sticky product and has created an industry moat for the company.

The switch to the cloud should yield better financial performance as legacy systems are expensive to maintain, this should yield better margins in the long run as well as new products being rolled out and easier to manage with a more technologically advanced system from the old one.

The company has a lot of financial flexibility which will enable them to weather any type of storm to their balance sheet and be opportunistic when the time is right to add value for shareholders.

Their transition to a subscription based model should result in higher margins and less volatile earnings making the business more predictable and a better investment than the current business model.

The macro environment is in favor of this company and they have been taking advantage of the opportunities that have come their way and should continue to execute the way they have been and boost future growth and profitability going forward.

The CEO has a solid track record of making the right decisions for the company as well as being conservative and financially responsible with the company and has helped produce a good balance sheet with financial flexibility.

Shareholder friendly management team that looks to create value for its shareholders and continue to put their best foot forward to help benefit the company and their future goals and long term goals to enhance shareholder value.

They have a solid record of beating analyst expectations and conservative guidance.

They should continue to beat earnings and surprise to the upside as the business environment has been favorable and continues to play in their favor.

With the advancement of fraud they have been on top of these problems and continue to innovate and put themselves in the best position to help prevent fraud and keep customers at bay and their retention rate is very good in comparison to their competitors.

They have a sticky product and their solutions are very robust and they are always innovating to help make the business better for shareholders and their customers who they serve in all ends of their business and consumer clients.

There is a transition for businesses to operate online and their services allow for digital businesses to operate smoothly.

They have great upside in the long run if all their plans materialize and a great return on investment when looking at their future goals and expectations for the business. |

| Base | 11.5 | Mitek continues to grow at a steady pace, driven by the increasing adoption of digital identity verification solutions.

Revenue growth aligns with industry averages.

Profitability remains stable.

Consistent cash flow generation allowing for strategic investments and debt repayment.

The mobile deposit side of the business has a lot of industry moats which will help make the business resistant to change and competitors trying to make their way into the business.

Growth in the cloud and subscription model will yield better results than expected as the new systems are implemented better and more efficiently.

Financials remain robust as well with a conservative management and financial team to ensure they weather the storm in any type of market environment as well as enhance shareholder value with the flexibility they will have with the financial strength they have produced and been responsible with.

Future growth and opportunities will continue to yield better financial results and performance going forward and continue to benefit the company overall.

The overall transition should allow better efficiency and performance as well as improve the business as a whole going forward.

Management has a proven track record and will make sound decisions to enhance and benefit the company and shareholder's best interest as well as create better financial results and efficiencies for the business.

Innovation continues to grow and improve to give a more robust system as well as keep customers from fraudulent practices and their retention rates should continue to be good as they have been historically for their customers on the business and consumer side.

Overall transition for more business online has created them to have a big opportunity and allow them to have a growing opportunity and success for their business to help digital customers operate more efficiently and operate more safely.

Long term financials should yield a great upside with the plans management has laid out and the growth expectations of the company and how well they will execute going forward. |

| Bear | Low | Increased competition in the digital identity verification market leading to pricing pressure and reduced market share.

Slower-than-expected adoption of digital identity solutions due to regulatory hurdles or consumer resistance.

Cybersecurity breaches or data privacy concerns damaging Mitek's reputation and leading to customer attrition.

Economic downturn impacting financial institutions and reducing demand for Mitek's solutions.

The company has high debt levels and could default on their debt.

Competition could take market share and pricing pressure could become a problem.

Macroeconomic pressures could hurt their customers who may not want to use Mitek's products as much anymore.

Key members may leave the company and hurt financial performance.

There is a risk that the innovation process is slow and competitors are catching up and Mitek will be at a disadvantage and lack of innovation to maintain future growth.

Overall financial performance will continue to worsen as their customers continue to dwindle as well as performance for future growth not materializing.

Overall performance will continue to worsen as their systems are not efficient enough and lack behind competitors with the transition not being as efficient.

A slow innovation and bad management could be a problem for the company and create a big risk and hurt shareholders. |

7. Risks

Mitek's substantial debt and high goodwill, coupled with increasing competition in the digital identity verification market, pose significant risks. While the company currently generates positive free cash flow, its financial flexibility is limited, making it vulnerable to economic downturns or technological shifts.

Red Flags:

The large fluctuation in Gross Profit Ratio from 99.82% to 76.17% from 2024 to 2025 needs investigation.

Relatively high debt compared to cash position.

8. Conclusion

Mitek continues to grow at a steady pace, driven by the increasing adoption of digital identity verification solutions.

Revenue growth aligns with industry averages.

Profitability remains stable.

Consistent cash flow generation allowing for strategic investments and debt repayment.

The mobile deposit side of the business has a lot of industry moats which will help make the business resistant to change and competitors trying to make their way into the business.

Growth in the cloud and subscription model will yield better results than expected as the new systems are implemented better and more efficiently.

Financials remain robust as well with a conservative management and financial team to ensure they weather the storm in any type of market environment as well as enhance shareholder value with the flexibility they will have with the financial strength they have produced and been responsible with.

Future growth and opportunities will continue to yield better financial results and performance going forward and continue to benefit the company overall.

The overall transition should allow better efficiency and performance as well as improve the business as a whole going forward.

Management has a proven track record and will make sound decisions to enhance and benefit the company and shareholder's best interest as well as create better financial results and efficiencies for the business.

Innovation continues to grow and improve to give a more robust system as well as keep customers from fraudulent practices and their retention rates should continue to be good as they have been historically for their customers on the business and consumer side.

Overall transition for more business online has created them to have a big opportunity and allow them to have a growing opportunity and success for their business to help digital customers operate more efficiently and operate more safely.

Long term financials should yield a great upside with the plans management has laid out and the growth expectations of the company and how well they will execute going forward.

Investment research for informational purposes only. Not financial advice.

Continue Your Research

Return to the Analyst Library or explore the specific financial data for this entity on its profile.

Calculating Return on Invested Capital (ROIC) and Return on Equity (ROE) requires more detailed data on invested capital and equity, respectively, but based on the provided financials, we can infer some trends. The net income and total equity figures suggest that ROE has fluctuated significantly, especially with negative retained earnings impacting equity. Similarly, while we don't have explicit invested capital figures, the changes in operating income relative to asset bases suggest variability in ROIC, potentially reflecting changes in asset utilization and profitability.

Calculating Return on Invested Capital (ROIC) and Return on Equity (ROE) requires more detailed data on invested capital and equity, respectively, but based on the provided financials, we can infer some trends. The net income and total equity figures suggest that ROE has fluctuated significantly, especially with negative retained earnings impacting equity. Similarly, while we don't have explicit invested capital figures, the changes in operating income relative to asset bases suggest variability in ROIC, potentially reflecting changes in asset utilization and profitability. The company has demonstrated positive Free Cash Flow (FCF) in each of the past five years, reflecting the ability to generate cash after accounting for capital expenditures. In 2025, FCF stood at $54.185 million, a significant increase from $30.25 million in 2024. Capital expenditure has been consistently managed, generally being around $1 million each year, indicating a relatively low capital intensity in their business operations.

The company has demonstrated positive Free Cash Flow (FCF) in each of the past five years, reflecting the ability to generate cash after accounting for capital expenditures. In 2025, FCF stood at $54.185 million, a significant increase from $30.25 million in 2024. Capital expenditure has been consistently managed, generally being around $1 million each year, indicating a relatively low capital intensity in their business operations.