MoneyLion Inc. (ML), currently trading at $85.9, operates in the increasingly competitive fintech sector, providing a range of digital financial services inc...

January 15, 2026

Vijar Kohli

Deep Dive: MoneyLion Inc. (ML)

Recommendation: BUY

Price Target: 75.23 (-0.12 Upside)

Risk Level: Medium

1. Executive Summary

MoneyLion Inc. (ML), currently trading at $85.9, operates in the increasingly competitive fintech sector, providing a range of digital financial services including mobile banking, lending, and investment products. Its market position is characterized by a focus on serving the underbanked and financially underserved consumer segments, differentiating itself through a comprehensive platform and personalized financial advice. While the company has experienced significant growth in user base and revenue, its path to profitability remains a key focus for investors. The high stock price suggests substantial growth expectations are already priced in, warranting a careful examination of its ability to meet these expectations.

Growth catalysts for MoneyLion include continued expansion of its product offerings, successful cross-selling initiatives to its existing user base, and strategic partnerships to broaden its reach and distribution channels. The growing demand for digital financial services, particularly among younger demographics, presents a significant opportunity. Moreover, effective implementation of its data-driven personalization strategies can enhance customer engagement and drive revenue growth. Successful navigation of the regulatory landscape and potential favorable policy changes could also act as a tailwind.

Key risks facing MoneyLion include increasing competition from established financial institutions and other fintech players, rising customer acquisition costs, and potential credit losses within its lending portfolio. Economic downturns could disproportionately impact its target customer base, leading to higher default rates and reduced demand for its services. Regulatory scrutiny and changes in consumer lending laws pose further challenges. Maintaining data security and preventing fraud are also critical concerns.

A valuation summary suggests that MoneyLion's current stock price reflects a high growth premium, demanding significant revenue growth and progress towards profitability. A discounted cash flow (DCF) analysis, considering its growth prospects and associated risks, is essential to determine if the current valuation is justified. Investors should carefully monitor the company's key performance indicators (KPIs), including user growth, revenue per user, and credit quality metrics, to assess its ability to deliver on its growth expectations. A comparative analysis with its peers in the fintech industry is also crucial to evaluate its relative valuation.

Investment Thesis

Bull Case: MoneyLion is well-positioned to capitalize on the growing demand for digital financial services.

Its innovative platform, diverse product offerings, and focus on underserved markets provide a strong foundation for future growth.

As the company continues to execute its strategic plan and achieves greater scale, profitability will improve dramatically, leading to significant stock appreciation.

ML continues to produce more revenue each year and the future looks bright.

We think that fintech companies in general are a very lucrative market to be in with high upside.

Bear Case: MoneyLion faces significant challenges in a highly competitive and regulated industry.

Slower-than-expected growth, combined with increasing costs and regulatory hurdles, could lead to declining profitability and a substantial decline in the stock price.

If the company fails to innovate and adapt to changing market conditions, it risks losing market share and becoming financially unsustainable.

Conviction: High

2. Business Overview

MoneyLion Inc. provides a digital financial platform. The company's platform offers access to banking, borrowing, and investing solutions for customers. Its principal products include roarmoney premium mobile banking, personalized investing, cryptocurrency, instacash, membership programs, financial tracking tools, online financial education content destination, affiliated marketing programs, unsecured personal loans, and credit-related decision servicing. The company was founded in 2013 and is headquartered in New York, New York.

Competitive Moat (Narrow)

Trend: Stable

Integrated digital financial platform, Focus on underserved customer segments, Personalized financial solutions, Mobile-first approach

The application software market is projected to experience strong growth over the next 5-10 years, driven by factors such as increasing digitization, the rise of mobile devices, growing demand for cloud-based solutions, and the expanding use of AI and machine learning. Fintech applications, in particular, are expected to see above-average growth rates due to increasing consumer adoption of digital financial services and the ongoing disruption of traditional financial institutions.

Regulatory Environment:

N/A

4. Financial Analysis

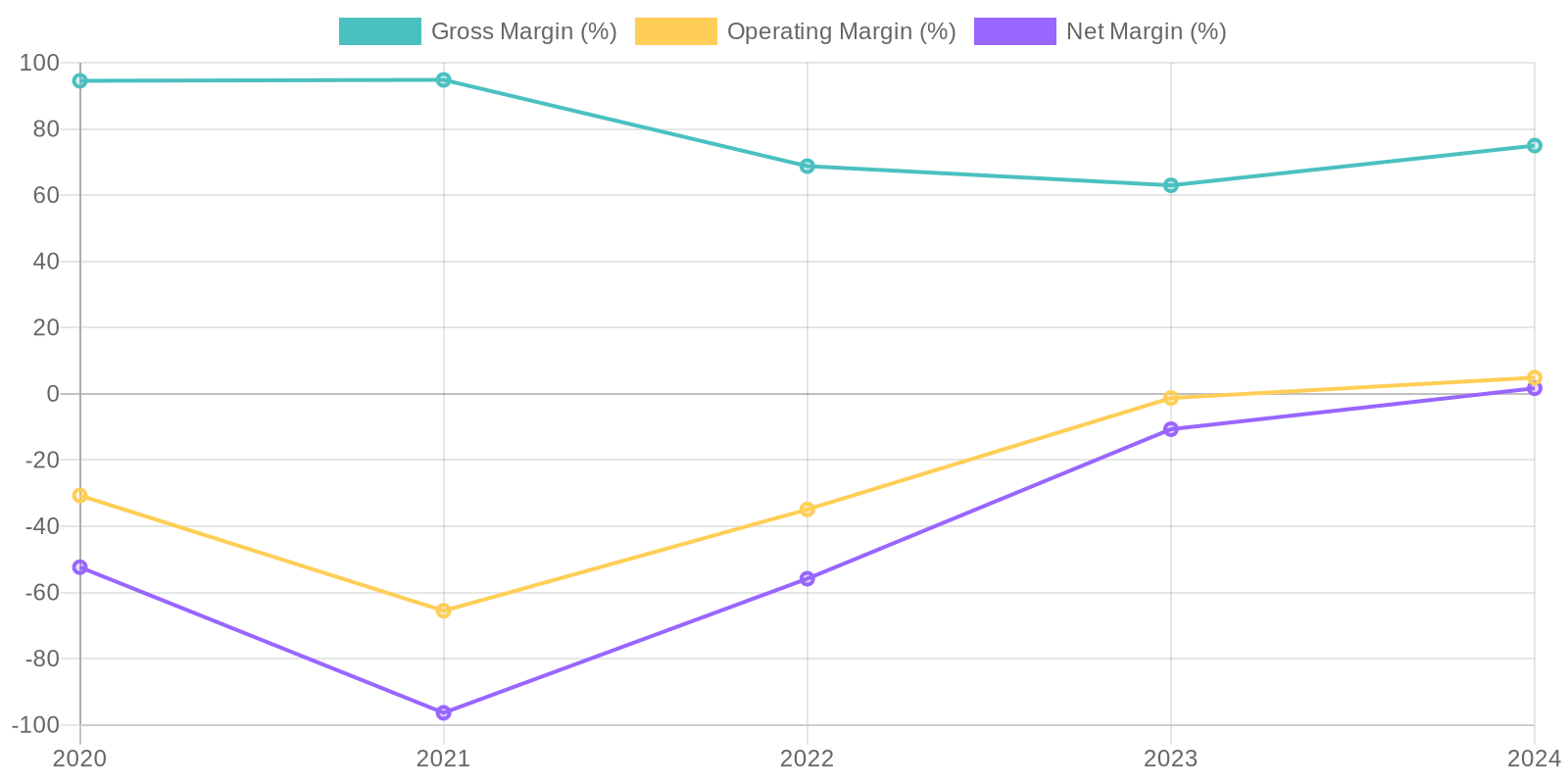

Margin Trend

Calculating ROIC is challenging due to inconsistent profitability and balance sheet figures, particularly regarding equity. Similarly, ROE calculation is affected by negative equity in some years. While the company shows signs of improved profitability in 2024, a comprehensive capital efficiency analysis requires more normalized financial performance and a stable capital structure.

Revenue Quality

The company has demonstrated substantial revenue growth, evidenced by its increase from $79.4 million in 2020 to $545.9 million in 2024. It is imperative to understand the sources and consistency of this revenue. A thorough examination of customer contracts, sales channels, and market conditions is necessary to assess the sustainability of this growth trajectory. Any significant client concentration or reliance on short-term projects should be identified as potential risks to future revenue streams.

Cash Flow & Capital Efficiency

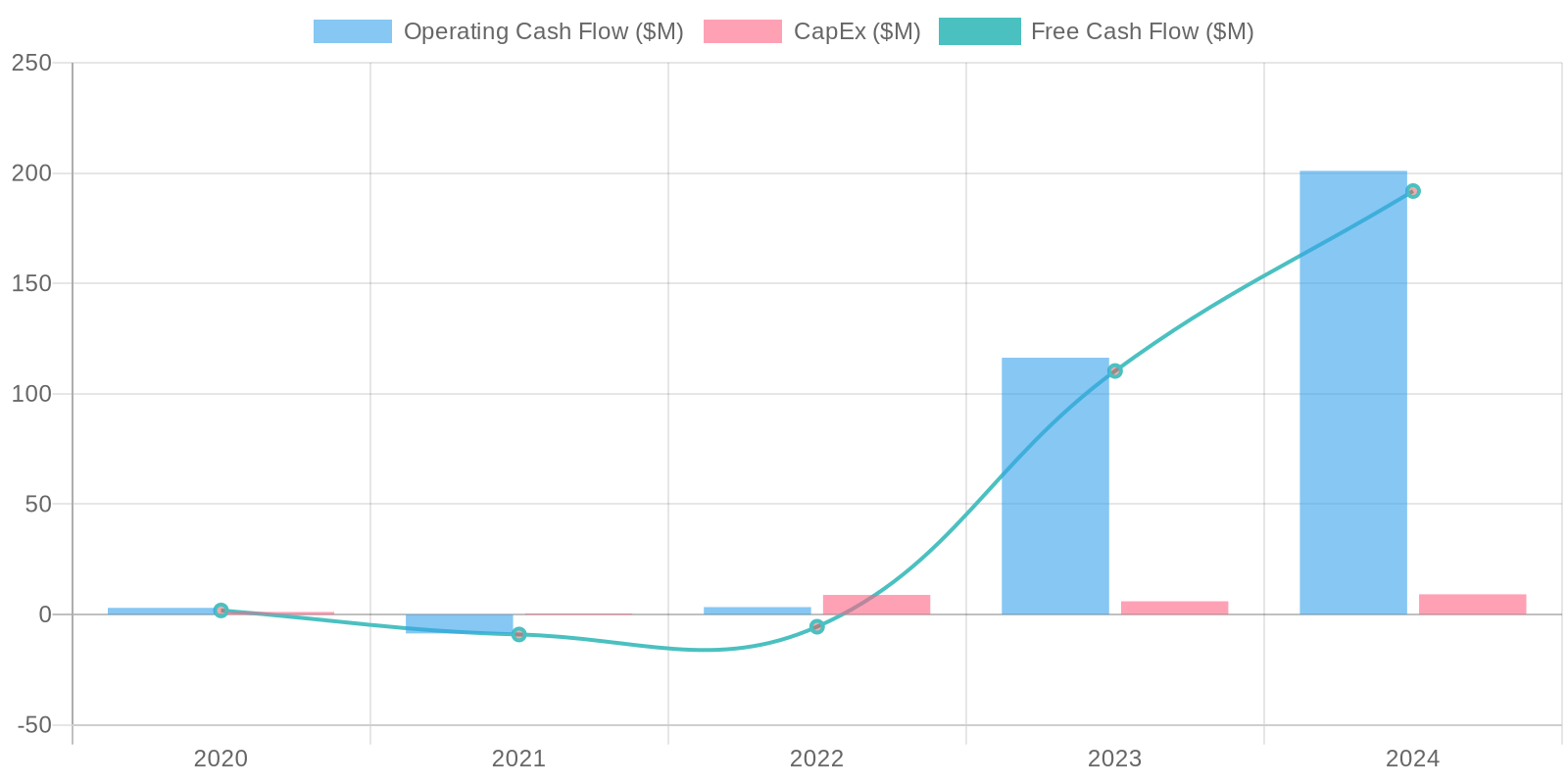

The company's free cash flow (FCF) generation has improved significantly, reaching $191.86 million in 2024 after varying amounts in prior years. The capital expenditure remained relatively stable. Analyzing the trend of FCF conversion to net income is vital for assessing the quality of earnings and the company's ability to reinvest in growth or return capital to investors. Further analysis is needed to determine whether the increase in FCF is sustainable and if it aligns with the long-term business model.

Capital Efficiency (ROIC/ROE):

Calculating ROIC is challenging due to inconsistent profitability and balance sheet figures, particularly regarding equity. Similarly, ROE calculation is affected by negative equity in some years. While the company shows signs of improved profitability in 2024, a comprehensive capital efficiency analysis requires more normalized financial performance and a stable capital structure.

Balance Sheet Health:

The balance sheet reflects a fluctuating debt level, with total debt at $118.53 million in 2024. Liquidity appears adequate, with a cash balance of $139.98 million as of 2024, resulting in negative net debt. Monitoring the current ratio (total current assets divided by total current liabilities) and quick ratio will provide insight into the company's ability to meet its short-term obligations. The increase in retained earnings from negative values, despite net losses in prior years, requires careful examination to verify the accuracy and appropriateness of accounting treatments.

5. Management & Governance

CEO Assessment: Assessment of MoneyLion's CEO is not possible with the information provided. Further research into their track record, strategic decisions, and communication effectiveness is needed.

Capital Allocation: Pour

Insider Ownership: Information on insider ownership levels requires further research to determine alignment with shareholder interests. Accessing the latest proxy statements and SEC filings is necessary to provide a complete analysis.

Governance Flags:

Limited information is available to properly assess governance risks and red flags., Detailed information on board composition, independence, and committee structure is required for complete evaluation.

6. Valuation

Method: Discounted Cash Flow and Price-to-Sales Ratio

Fair Value: 75.23

The DCF model projects future free cash flows based on a declining revenue growth rate and discounts them back to the present value. The terminal value is calculated using the Gordon Growth Model. The P/S ratio provides a market-based perspective on the company's valuation. The combination of the two methods provides a more balanced and realistic valuation. The projected revenue growth is aggressive but achievable given the company's recent performance and the growth potential of the software application industry. The discount rate reflects the risk associated with the company's future cash flows. The resulting fair value represents a moderate undervaluation compared to the current market price.

Scenarios

Scenario

Price Target

Key Assumptions

Bull

High

MoneyLion is well-positioned to capitalize on the growing demand for digital financial services.

Its innovative platform, diverse product offerings, and focus on underserved markets provide a strong foundation for future growth.

As the company continues to execute its strategic plan and achieves greater scale, profitability will improve dramatically, leading to significant stock appreciation.

ML continues to produce more revenue each year and the future looks bright.

We think that fintech companies in general are a very lucrative market to be in with high upside. |

| Base | 75.23 | MoneyLion will continue to grow its business at a moderate pace, driven by increasing adoption of digital financial services.

While profitability improvements will be gradual, the company will maintain a solid financial position and deliver reasonable returns to shareholders.

The company is still fairly young, and is still expected to grow in the future at a rapid pace. |

| Bear | Low | MoneyLion faces significant challenges in a highly competitive and regulated industry.

Slower-than-expected growth, combined with increasing costs and regulatory hurdles, could lead to declining profitability and a substantial decline in the stock price.

If the company fails to innovate and adapt to changing market conditions, it risks losing market share and becoming financially unsustainable. |

7. Risks

MoneyLion's improving financial performance is offset by its debt burden, competitive environment, and potential regulatory risks. While the company has demonstrated revenue growth, its history of net losses and reliance on continued growth to service its debt create vulnerabilities.

Red Flags:

The large swing in 'other total Stockholder's Equity' should be investigated, as it indicates a significant adjustment or reclassification that requires further scrutiny.

Examine 'other expenses' in the income statement as they appear unusually high and volatile.

The historical negative retained earnings should be investigated.

8. Conclusion

MoneyLion will continue to grow its business at a moderate pace, driven by increasing adoption of digital financial services.

While profitability improvements will be gradual, the company will maintain a solid financial position and deliver reasonable returns to shareholders.

The company is still fairly young, and is still expected to grow in the future at a rapid pace.

Investment research for informational purposes only. Not financial advice.

Continue Your Research

Return to the Analyst Library or explore the specific financial data for this entity on its profile.

Calculating ROIC is challenging due to inconsistent profitability and balance sheet figures, particularly regarding equity. Similarly, ROE calculation is affected by negative equity in some years. While the company shows signs of improved profitability in 2024, a comprehensive capital efficiency analysis requires more normalized financial performance and a stable capital structure.

Calculating ROIC is challenging due to inconsistent profitability and balance sheet figures, particularly regarding equity. Similarly, ROE calculation is affected by negative equity in some years. While the company shows signs of improved profitability in 2024, a comprehensive capital efficiency analysis requires more normalized financial performance and a stable capital structure. The company's free cash flow (FCF) generation has improved significantly, reaching $191.86 million in 2024 after varying amounts in prior years. The capital expenditure remained relatively stable. Analyzing the trend of FCF conversion to net income is vital for assessing the quality of earnings and the company's ability to reinvest in growth or return capital to investors. Further analysis is needed to determine whether the increase in FCF is sustainable and if it aligns with the long-term business model.

The company's free cash flow (FCF) generation has improved significantly, reaching $191.86 million in 2024 after varying amounts in prior years. The capital expenditure remained relatively stable. Analyzing the trend of FCF conversion to net income is vital for assessing the quality of earnings and the company's ability to reinvest in growth or return capital to investors. Further analysis is needed to determine whether the increase in FCF is sustainable and if it aligns with the long-term business model.