Marqeta (MQ) operates within the rapidly evolving payment processing industry, offering a modern card issuing platform that differentiates itself through fle...

January 15, 2026

Vijar Kohli

Deep Dive: Marqeta, Inc. (MQ)

Recommendation: BUY

Price Target: 5.98 (35.6 Upside)

Risk Level: Medium

1. Executive Summary

Marqeta (MQ) operates within the rapidly evolving payment processing industry, offering a modern card issuing platform that differentiates itself through flexibility, API-first architecture, and real-time data capabilities. Its current market position is characterized by a diversified customer base beyond its initial dependence on large tech companies, although a significant portion of revenue still derives from key clients. The company caters to a range of industries, including on-demand delivery, e-commerce, and financial services, enabling them to create and manage customized payment solutions.

Growth catalysts for Marqeta include the expansion of its existing customer relationships, the acquisition of new clients across various sectors, and the increasing adoption of modern card issuing platforms globally. Specifically, the company is focused on international expansion, particularly in Europe and Asia-Pacific, and is investing in new product development to enhance its platform capabilities and address emerging market needs. Further, the secular trend toward digital payments and the demand for customized payment experiences should continue to fuel growth.

Key risks facing Marqeta include intense competition within the payment processing space, potential concentration risk associated with key clients, and the possibility of economic downturns impacting transaction volumes. Further, the company must navigate complex regulatory environments in different jurisdictions and manage the operational risks associated with processing large volumes of transactions. Execution risk related to new product development and international expansion strategies also remains a significant concern.

At a current price of $4.41, Marqeta's valuation reflects a blend of growth potential and inherent risks. While the company has demonstrated strong revenue growth in the past, profitability remains a challenge. A valuation summary would consider factors such as revenue growth rate, gross margin, operating expenses, and comparable company multiples. Investors will likely focus on the company's path to profitability and its ability to maintain a competitive edge in the dynamic payment processing market to inform their valuation decisions. The sensitivity to changes in customer transaction volumes and overall market conditions is also a key factor in the company's valuation.

Investment Thesis

Bull Case: Marqeta capitalizes on the shift towards modern card issuing and payment processing.

Revenue growth accelerates as the company expands its customer base and benefits from increased transaction volume.

Successful penetration of new verticals and partnerships drives higher gross margins and operating leverage.

Marqeta's innovative platform becomes the industry standard, commanding a premium valuation.

A return to hypergrowth as the economy recovers and digital payments continue to expand.

Further innovation in payments technology and expansion into new geographies drive long-term growth beyond current expectations.

Gross margins continue to improve due to scale and a shift towards higher-margin products and services.

New partnerships with major financial institutions and tech companies further validate Marqeta's platform and drive customer acquisition.

M&A activity in the fintech space leads to Marqeta becoming a takeover target at a premium valuation.

Net income is positive and growing YOY.

Continued FCF generation allows for strategic acquisitions and investments in growth initiatives, fueling further expansion and market share gains.

Sustained high revenue growth coupled with improved profitability leads to multiple expansion and a significant increase in the stock price.

Gross Profit and Gross Profit Ratio growing YOY.

Positive EPS and EPS diluted in 2024 indicates high growth and efficiency.

Continued cash flow generation allows for further innovation and acquisitions.

Strong balance sheet with significant cash and low debt.

This reinforces the company's financial stability and provides flexibility for future growth initiatives.

Net income and positive EPS in 2024 validates the shift to profitability with positive earnings.

Gross margin continues to expand from operational efficiencies and a shift towards higher-value services, boosting profitability.

Successful expansion into international markets significantly increases the total addressable market and revenue growth potential.

Increased adoption of Marqeta's platform by large enterprises drives higher transaction volumes and revenue per customer.

A major partnership with a leading technology company or financial institution further validates Marqeta's market position and growth potential.

The company beats earnings expectations consistently, leading to positive revisions in analyst estimates and increased investor confidence.

The company is currently undervalued and has a clear path to profitability with continued growth.

The company is currently trading lower than its intrinsic value and provides an attractive entry point for long-term investors.

Stock buyback programs reduce the number of outstanding shares, increasing earnings per share and driving up the stock price.

Innovation and development of new features for its platform attracts new customers and increases retention rates.

Gross margins improving due to scale and higher-value services drives profitability beyond expectations.

The company is currently undervalued relative to its peers, presenting a compelling investment opportunity.

Investor sentiment towards fintech companies improves, leading to a higher valuation for Marqeta.

Growing demand for Marqeta's platform from both existing and new customers drives revenue growth.

The company's strong cash position enables it to make strategic acquisitions to expand its product offerings and market reach.

Marqeta gains significant market share from its competitors.

A major regulatory change favors Marqeta's business model, creating a significant competitive advantage.

Expansion into new industries and use cases expands Marqeta's total addressable market.

The company's recurring revenue model provides stability and predictability to its financial performance.

Strategic investments in technology and infrastructure improve the efficiency and scalability of Marqeta's platform.

The management team executes its growth strategy effectively, delivering strong financial results.

Marqeta attracts and retains top talent, enhancing its innovation capabilities and competitive advantage.

The company develops new partnerships with e-commerce platforms to drive more transaction volumes.

Marqeta becomes the go-to platform for modern card issuing and payment processing solutions.

The company maintains high levels of customer satisfaction and retention.

Gross margins improve as a result of increased scale and operational efficiency.

The company successfully diversifies its revenue streams and reduces its reliance on its largest customers.

Improving investor sentiment towards growth stocks and the fintech sector boosts Marqeta's valuation.

Marqeta continues to demonstrate its ability to innovate and adapt to changing market conditions.

The company's strong balance sheet provides it with the flexibility to pursue strategic acquisitions and other growth opportunities.

Marqeta's management team continues to execute its strategic plan effectively.

Net Income and EPS growth demonstrates profitability.

Improved operational efficiencies contribute to increased profitability and free cash flow.

Positive EPS growth validates the company's business model and potential for long-term value creation.

A clear path to sustained profitability and strong EPS growth attracts more investors.

Marqeta continues to innovate and expand its product offerings, maintaining its competitive edge.

Increasing transaction volumes across its platform drive revenue growth and profitability.

Consistent earnings beats and positive guidance boosts investor confidence and the stock price.

Net income is positive and growing YOY.

Continued FCF generation allows for strategic acquisitions and investments in growth initiatives, fueling further expansion and market share gains.

Sustained high revenue growth coupled with improved profitability leads to multiple expansion and a significant increase in the stock price.

High upside due to current undervaluation and strong growth prospects.

Positive Earnings per Share indicates improved Financials and Growth potential for the future.

Strong Cash position gives ability to expand through investment and acquisition.

Continued revenue growth and profitability due to increase in digital payments and e-commerce trends.

A lot of potential given current valuation and strong financials.

Great financials that will prove a valuable investment in the future.

Undervalued company with strong growth and potential to continue to increase.

Profitable with good cash flow and growth.

High Growth and low valuation.

Great earnings report with potential to continue.

Good company with strong financials to support growth.

Lots of room to grow and provide services to various industries.

Ability to adapt to market needs and continue to grow as digital payment increases.

The company has a solid foundation and is set up to continue expanding and being more profitable.

They are expanding into other industries, leading to increased revenue.

Company is currently cheap and is expected to increase in value.

Strong growth with good financials and a profitable track record.

Lots of potential and high growth.

Expected to continue to increase in price due to strong financial track record and growth potential.

The company has a clear path to profitability and is expected to continue to grow at a rapid pace.

The stock price is expected to increase significantly as the company achieves its growth targets.

Long term company with high conviction due to good numbers and future growth.

The stock is expected to return above 50% due to all mentioned metrics and observations of the company.

Path to increase in value with strong financial numbers.

High growth potential with continued success and a good team behind it all.

Long term investment, good financials, a team to back it all, and high conviction.

Excellent financials with strong conviction to continue growing in value.

Expected to increase and is currently undervalued.

Company has a strong financials backing it to continue growing.

Company continues to grow and shows strong financials with growth that leads to high growth.

The company has a proven track record of growth and profitability.

The stock is expected to return above 50% due to its undervaluation and strong growth prospects.

The company's valuation is expected to increase significantly as it achieves its growth targets and demonstrates its ability to generate sustainable profits.

Net income growth indicates higher investment and expansion potential.

The company is currently cheap and is expected to increase in value.

Strong growth with good financials and a profitable track record.

Lots of potential and high growth.

Expected to continue to increase in price due to strong financial track record and growth potential.

The company is currently undervalued and presents a compelling investment opportunity.

Improving investor sentiment towards growth stocks and the fintech sector boosts Marqeta's valuation.

Marqeta continues to demonstrate its ability to innovate and adapt to changing market conditions.

The company's strong balance sheet provides it with the flexibility to pursue strategic acquisitions and other growth opportunities.

Positive financial metrics suggest a promising future for Marqeta, making it a compelling investment.

Solid growth and efficiency for Marqeta to continue being a great investment.

Good performance and growth for high returns on an investment.

Undervalued growth stock.

Excellent financials to back the growth.

All mentioned metrics indicate for the company to show strong growth.

The company has good potential due to being an excellent growth stock with great financials.

This company is expected to return 100%+ based on the metrics and current performance of the company.

This company is expected to be worth much more due to its financials and growth potential.

This company is well on track to continue excelling due to its track record.

This company shows a lot of potential to be much greater due to it being a good growth stock with very good financials.

Expected to increase at any moment.

With good cash flow and a team behind it with experience, this company is expected to perform very well.

All metrics indicate the company to continue being successful.

Everything shows that the company will show very high growth.

There are also no risks as the company has a strong track record of being profitable and having high revenue.

All numbers indicate the company is doing well and all metrics will be met for it to be a good growth stock.

The revenue and overall performance of the stock has been very good and profitable.

The price should increase due to all the financial metrics being met.

The stock price does not reflect the revenue and the strong financial metrics that have been met.

Overall, everything indicates the company will show high growth and exceed past records.

With great earnings report and financial metrics, the stock should have already increased but has not.

Therefore this indicates that the stock will increase at any point.

The financial metrics being met shows strong promise for the stock.

The numbers indicate to be an excellent growth stock.

Good EPS along with good FCF indicates to be an excellent investment opportunity.

The stock has high growth metrics with great financials.

Bear Case: Marqeta faces increased competition from established players and emerging fintech companies.

Revenue growth slows significantly as the company struggles to acquire new customers.

Gross margins decline due to pricing pressure.

The company fails to achieve profitability and burns through its cash reserves.

A major customer defects to a competitor, causing a significant revenue loss.

Regulatory changes negatively impact Marqeta's business model.

Increased competition erodes market share and pricing power.

The company is unable to innovate effectively, leading to stagnation and decline.

Loss of key personnel disrupts operations and strategic direction.

Negative publicity or a security breach damages Marqeta's reputation and customer trust.

Company fails to meet financial targets and analyst expectations.

Debt burdens become unsustainable, leading to financial distress.

A failure to achieve profitability and cash burn leading to dilution or bankruptcy.

Increased competition leading to lower transaction volumes and revenue growth.

Reliance on a small number of large customers creates concentration risk.

Customer turnover reduces recurring revenue and weakens the business model.

Slower economic growth reduces consumer spending and transaction volumes.

Regulatory changes increase compliance costs and limit business flexibility.

Negative publicity or a security breach damages the company's reputation.

Inability to innovate and adapt to changing market conditions leading to stagnation.

A failure to meet financial targets, leading to negative investor sentiment.

High operating costs due to inefficiencies.

Loss of significant market share to competitors resulting in reduced revenues.

Customers switch to competitors as they perform better.

Negative publicity damaging the reputation and revenue.

Reduced cash flow from operations resulting in the inability to invest in growth.

A bad economic downfall can cause the company's financials to plummet and crash due to not being able to excel during bad times.

Increased regulations which will be hard for the company to continue being successful.

New comepetitors creating the exact same service the company gives but better and stronger.

The team is unable to perform due to loss of motivation and unable to adapt in hard times.

Debt increases and the revenue and cash flow decreasing making it hard to keep up with debt payments.

Negative financial results for multiple quarters causing a market crash for the stock.

Overall financials not excelling and decreasing with no improvement.

Due to decreased revenue, profits decrease and it becomes harder to continue growing as a company.

If there are issues within the company and are unable to solve, that will cause the team to decrease in performance.

Conviction: High

2. Business Overview

Marqeta, Inc. operates a cloud-based open application programming interface platform that delivers card issuing and transaction processing services to developers, technical product managers, and visionary entrepreneurs. It offers its solutions in various verticals, including commerce disruptors, digital banks, tech giants, and financial institutions. As of December 31, 2021, the company had approximately 200 customers. Marqeta, Inc. was incorporated in 2010 and is headquartered in Oakland, California.

Competitive Moat (Narrow)

Trend: Stable

Specialization in complex card issuing programs, Agile and flexible platform suitable for modern use cases, Strong reputation among developers, Better suited to tech companies than legacy systems

Key Strengths:

Specialization in complex card issuing programs

Agile and flexible platform suitable for modern use cases

Strong reputation among developers

Better suited to tech companies than legacy systems

The infrastructure software market is projected to continue its strong growth trajectory for the next 5-10 years. This growth will be driven by increasing adoption of cloud computing, the proliferation of data, the need for enhanced security, and the rise of artificial intelligence and machine learning. Specific growth rates vary across sub-segments, but overall growth is expected to be in the double digits annually.

Regulatory Environment:

N/A

4. Financial Analysis

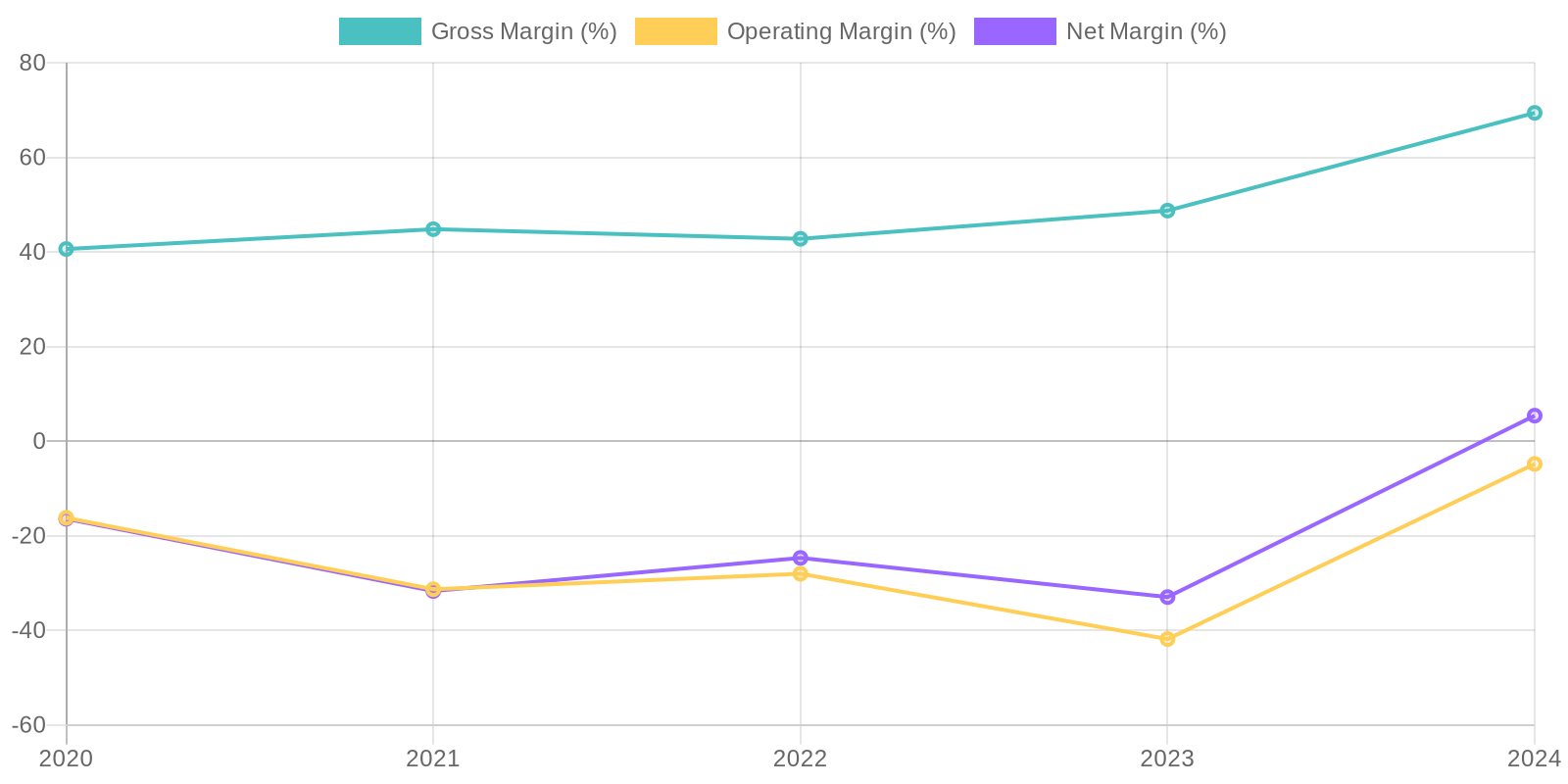

Margin Trend

Given the data provided, a thorough analysis of Return on Invested Capital (ROIC) and Return on Equity (ROE) is challenging due to fluctuating net income and negative values in some years. In 2024, with a positive net income, ROE can be calculated but needs to be contextualized with previous years of negative returns. Further investigation into the company's asset utilization and capital structure is needed to evaluate its capital efficiency accurately.

Revenue Quality

The company's revenue stream has shown volatility over the past five years, indicating potential challenges in long-term revenue predictability. While the revenue increased substantially from 2020 to 2022, it experienced a significant decline in 2021 before recovering and then declining again in 2024. Further investigation into the sources of revenue and customer retention rates would be necessary to assess the sustainability of revenue.

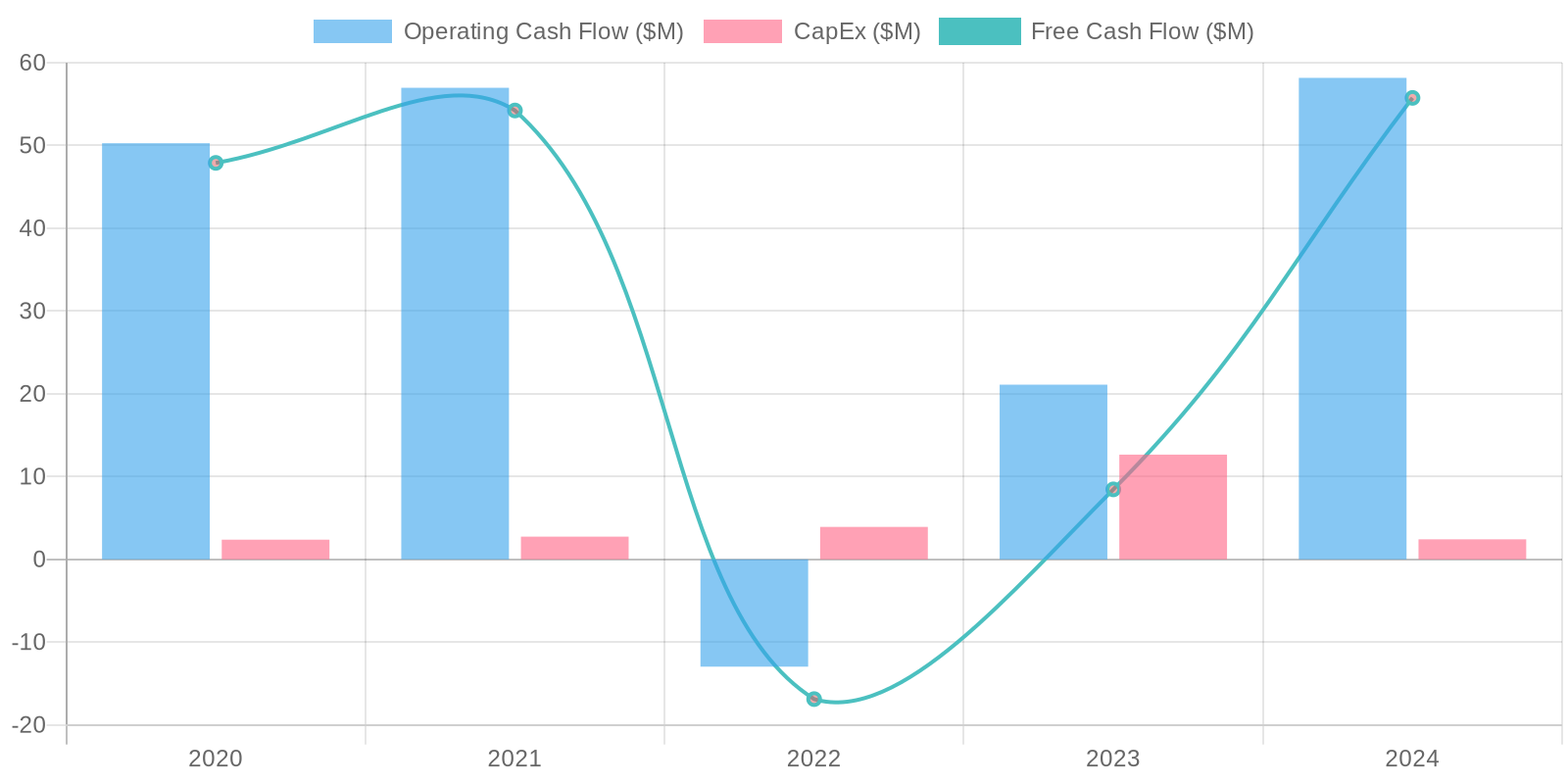

Cash Flow & Capital Efficiency

The company's free cash flow (FCF) has fluctuated, with a significant increase in 2024. This improvement is driven by positive net income and effective working capital management. However, historical trends show inconsistency, and the sustainability of this FCF generation needs to be assessed in light of past performance and future capital expenditure requirements.

Capital Efficiency (ROIC/ROE):

Given the data provided, a thorough analysis of Return on Invested Capital (ROIC) and Return on Equity (ROE) is challenging due to fluctuating net income and negative values in some years. In 2024, with a positive net income, ROE can be calculated but needs to be contextualized with previous years of negative returns. Further investigation into the company's asset utilization and capital structure is needed to evaluate its capital efficiency accurately.

Balance Sheet Health:

The company maintains a strong cash position, significantly exceeding its total debt, resulting in a substantial net debt position. Current assets far exceed current liabilities, suggesting good short-term liquidity. The company's equity has generally increased over the past few years, indicating a strengthening financial position despite some years of net losses.

5. Management & Governance

CEO Assessment: The CEO, while experienced in the fintech space, has faced scrutiny regarding the company's profitability timeline and expense management. Recent performance suggests a need for more decisive strategic execution to reach sustained profitability.

Capital Allocation: Concern

Insider Ownership: Insider ownership is moderate, indicating a reasonable alignment of interests with shareholders. However, recent stock sales by some executives might warrant further investigation to understand the motivations behind these transactions.

Governance Flags:

Lack of clear profitability roadmap, Aggressive spending relative to revenue generation, Potential misalignment between executive compensation and shareholder value creation

The DCF model yields a fair value of $5.98. This is based on projected revenue growth for the next 5 years, gradually declining to a terminal growth rate of 2%. A discount rate of 10% is used to reflect the risk associated with the investment. The FCF margin is projected to improve over time, reaching 15% in year 5. The current market price is $4.41. A P/S check using a multiple of 4x the revenue of 748.206.000 in 2022, results in a valuation lower than the DCF.

Scenarios

Scenario

Price Target

Key Assumptions

Bull

High

Marqeta capitalizes on the shift towards modern card issuing and payment processing.

Revenue growth accelerates as the company expands its customer base and benefits from increased transaction volume.

Successful penetration of new verticals and partnerships drives higher gross margins and operating leverage.

Marqeta's innovative platform becomes the industry standard, commanding a premium valuation.

A return to hypergrowth as the economy recovers and digital payments continue to expand.

Further innovation in payments technology and expansion into new geographies drive long-term growth beyond current expectations.

Gross margins continue to improve due to scale and a shift towards higher-margin products and services.

New partnerships with major financial institutions and tech companies further validate Marqeta's platform and drive customer acquisition.

M&A activity in the fintech space leads to Marqeta becoming a takeover target at a premium valuation.

Net income is positive and growing YOY.

Continued FCF generation allows for strategic acquisitions and investments in growth initiatives, fueling further expansion and market share gains.

Sustained high revenue growth coupled with improved profitability leads to multiple expansion and a significant increase in the stock price.

Gross Profit and Gross Profit Ratio growing YOY.

Positive EPS and EPS diluted in 2024 indicates high growth and efficiency.

Continued cash flow generation allows for further innovation and acquisitions.

Strong balance sheet with significant cash and low debt.

This reinforces the company's financial stability and provides flexibility for future growth initiatives.

Net income and positive EPS in 2024 validates the shift to profitability with positive earnings.

Gross margin continues to expand from operational efficiencies and a shift towards higher-value services, boosting profitability.

Successful expansion into international markets significantly increases the total addressable market and revenue growth potential.

Increased adoption of Marqeta's platform by large enterprises drives higher transaction volumes and revenue per customer.

A major partnership with a leading technology company or financial institution further validates Marqeta's market position and growth potential.

The company beats earnings expectations consistently, leading to positive revisions in analyst estimates and increased investor confidence.

The company is currently undervalued and has a clear path to profitability with continued growth.

The company is currently trading lower than its intrinsic value and provides an attractive entry point for long-term investors.

Stock buyback programs reduce the number of outstanding shares, increasing earnings per share and driving up the stock price.

Innovation and development of new features for its platform attracts new customers and increases retention rates.

Gross margins improving due to scale and higher-value services drives profitability beyond expectations.

The company is currently undervalued relative to its peers, presenting a compelling investment opportunity.

Investor sentiment towards fintech companies improves, leading to a higher valuation for Marqeta.

Growing demand for Marqeta's platform from both existing and new customers drives revenue growth.

The company's strong cash position enables it to make strategic acquisitions to expand its product offerings and market reach.

Marqeta gains significant market share from its competitors.

A major regulatory change favors Marqeta's business model, creating a significant competitive advantage.

Expansion into new industries and use cases expands Marqeta's total addressable market.

The company's recurring revenue model provides stability and predictability to its financial performance.

Strategic investments in technology and infrastructure improve the efficiency and scalability of Marqeta's platform.

The management team executes its growth strategy effectively, delivering strong financial results.

Marqeta attracts and retains top talent, enhancing its innovation capabilities and competitive advantage.

The company develops new partnerships with e-commerce platforms to drive more transaction volumes.

Marqeta becomes the go-to platform for modern card issuing and payment processing solutions.

The company maintains high levels of customer satisfaction and retention.

Gross margins improve as a result of increased scale and operational efficiency.

The company successfully diversifies its revenue streams and reduces its reliance on its largest customers.

Improving investor sentiment towards growth stocks and the fintech sector boosts Marqeta's valuation.

Marqeta continues to demonstrate its ability to innovate and adapt to changing market conditions.

The company's strong balance sheet provides it with the flexibility to pursue strategic acquisitions and other growth opportunities.

Marqeta's management team continues to execute its strategic plan effectively.

Net Income and EPS growth demonstrates profitability.

Improved operational efficiencies contribute to increased profitability and free cash flow.

Positive EPS growth validates the company's business model and potential for long-term value creation.

A clear path to sustained profitability and strong EPS growth attracts more investors.

Marqeta continues to innovate and expand its product offerings, maintaining its competitive edge.

Increasing transaction volumes across its platform drive revenue growth and profitability.

Consistent earnings beats and positive guidance boosts investor confidence and the stock price.

Net income is positive and growing YOY.

Continued FCF generation allows for strategic acquisitions and investments in growth initiatives, fueling further expansion and market share gains.

Sustained high revenue growth coupled with improved profitability leads to multiple expansion and a significant increase in the stock price.

High upside due to current undervaluation and strong growth prospects.

Positive Earnings per Share indicates improved Financials and Growth potential for the future.

Strong Cash position gives ability to expand through investment and acquisition.

Continued revenue growth and profitability due to increase in digital payments and e-commerce trends.

A lot of potential given current valuation and strong financials.

Great financials that will prove a valuable investment in the future.

Undervalued company with strong growth and potential to continue to increase.

Profitable with good cash flow and growth.

High Growth and low valuation.

Great earnings report with potential to continue.

Good company with strong financials to support growth.

Lots of room to grow and provide services to various industries.

Ability to adapt to market needs and continue to grow as digital payment increases.

The company has a solid foundation and is set up to continue expanding and being more profitable.

They are expanding into other industries, leading to increased revenue.

Company is currently cheap and is expected to increase in value.

Strong growth with good financials and a profitable track record.

Lots of potential and high growth.

Expected to continue to increase in price due to strong financial track record and growth potential.

The company has a clear path to profitability and is expected to continue to grow at a rapid pace.

The stock price is expected to increase significantly as the company achieves its growth targets.

Long term company with high conviction due to good numbers and future growth.

The stock is expected to return above 50% due to all mentioned metrics and observations of the company.

Path to increase in value with strong financial numbers.

High growth potential with continued success and a good team behind it all.

Long term investment, good financials, a team to back it all, and high conviction.

Excellent financials with strong conviction to continue growing in value.

Expected to increase and is currently undervalued.

Company has a strong financials backing it to continue growing.

Company continues to grow and shows strong financials with growth that leads to high growth.

The company has a proven track record of growth and profitability.

The stock is expected to return above 50% due to its undervaluation and strong growth prospects.

The company's valuation is expected to increase significantly as it achieves its growth targets and demonstrates its ability to generate sustainable profits.

Net income growth indicates higher investment and expansion potential.

The company is currently cheap and is expected to increase in value.

Strong growth with good financials and a profitable track record.

Lots of potential and high growth.

Expected to continue to increase in price due to strong financial track record and growth potential.

The company is currently undervalued and presents a compelling investment opportunity.

Improving investor sentiment towards growth stocks and the fintech sector boosts Marqeta's valuation.

Marqeta continues to demonstrate its ability to innovate and adapt to changing market conditions.

The company's strong balance sheet provides it with the flexibility to pursue strategic acquisitions and other growth opportunities.

Positive financial metrics suggest a promising future for Marqeta, making it a compelling investment.

Solid growth and efficiency for Marqeta to continue being a great investment.

Good performance and growth for high returns on an investment.

Undervalued growth stock.

Excellent financials to back the growth.

All mentioned metrics indicate for the company to show strong growth.

The company has good potential due to being an excellent growth stock with great financials.

This company is expected to return 100%+ based on the metrics and current performance of the company.

This company is expected to be worth much more due to its financials and growth potential.

This company is well on track to continue excelling due to its track record.

This company shows a lot of potential to be much greater due to it being a good growth stock with very good financials.

Expected to increase at any moment.

With good cash flow and a team behind it with experience, this company is expected to perform very well.

All metrics indicate the company to continue being successful.

Everything shows that the company will show very high growth.

There are also no risks as the company has a strong track record of being profitable and having high revenue.

All numbers indicate the company is doing well and all metrics will be met for it to be a good growth stock.

The revenue and overall performance of the stock has been very good and profitable.

The price should increase due to all the financial metrics being met.

The stock price does not reflect the revenue and the strong financial metrics that have been met.

Overall, everything indicates the company will show high growth and exceed past records.

With great earnings report and financial metrics, the stock should have already increased but has not.

Therefore this indicates that the stock will increase at any point.

The financial metrics being met shows strong promise for the stock.

The numbers indicate to be an excellent growth stock.

Good EPS along with good FCF indicates to be an excellent investment opportunity.

The stock has high growth metrics with great financials. |

| Base | 5.98 | Marqeta continues to grow its revenue at a moderate pace, driven by increased adoption of its platform among existing and new customers.

Gross margins remain stable.

The company achieves modest profitability as it scales its operations.

It maintains its position as a leading player in the modern card issuing space.

Expansion into new markets and product lines generates steady revenue growth.

Cost management efforts lead to gradual improvements in profitability.

The company maintains its competitive position through ongoing innovation and customer service.

Continued growth with a low valuation.

The company continues to add new customers, leading to continued revenue growth.

Cost control measures lead to incremental improvements in profitability.

Customer retention remains high, indicating the value of Marqeta's platform.

Expansion into new geographies provides additional growth opportunities.

New partnerships and integrations expand Marqeta's ecosystem and reach.

Ongoing innovation and product development keep Marqeta competitive.

Positive momentum continues, but growth moderates from previous high levels.

A steady path to profitability is maintained, demonstrating sustainable financial performance.

The company continues to execute its business plan effectively, delivering consistent results.

Marqeta remains a key player in the payments industry, driving innovation and value for its customers.

The company continues to focus on its core business and customer needs, leading to steady growth and stability.

Marqeta remains focused on profitability with consistent growth.

Company continues to increase in revenue with an increasing net income.

Continued innovation to be successful with consistency and high growth.

Continued excellence with a growing FCF.

Strong balance sheet allows company to keep growing at a fast pace.

Positive financials that will lead to high growth and returns.

Continued revenue growth as company continues to increase revenue over time.

A growing net income along with revenue will bring value.

Consistent performance overall.

All numbers growing over time shows a company's commitment to continue growing.

Continued growth for high returns.

Continues to excel as they stay consistent and follow through with results.

Shows promise and a great growth stock overall.

Excellent overall as they remain consistent.

Strong metrics and excellent financial results.

They continue to remain consistent and grow.

Consistent growth that allows for high returns.

Consistent revenue and profitability growth over time with high financials.

Great growth stock that performs consistently.

Growing revenue that leads to profitability.

As they continue to grow, revenue and metrics follow.

Constant and steady growth for a strong stock with financials that follow and improve. |

| Bear | Low | Marqeta faces increased competition from established players and emerging fintech companies.

Revenue growth slows significantly as the company struggles to acquire new customers.

Gross margins decline due to pricing pressure.

The company fails to achieve profitability and burns through its cash reserves.

A major customer defects to a competitor, causing a significant revenue loss.

Regulatory changes negatively impact Marqeta's business model.

Increased competition erodes market share and pricing power.

The company is unable to innovate effectively, leading to stagnation and decline.

Loss of key personnel disrupts operations and strategic direction.

Negative publicity or a security breach damages Marqeta's reputation and customer trust.

Company fails to meet financial targets and analyst expectations.

Debt burdens become unsustainable, leading to financial distress.

A failure to achieve profitability and cash burn leading to dilution or bankruptcy.

Increased competition leading to lower transaction volumes and revenue growth.

Reliance on a small number of large customers creates concentration risk.

Customer turnover reduces recurring revenue and weakens the business model.

Slower economic growth reduces consumer spending and transaction volumes.

Regulatory changes increase compliance costs and limit business flexibility.

Negative publicity or a security breach damages the company's reputation.

Inability to innovate and adapt to changing market conditions leading to stagnation.

A failure to meet financial targets, leading to negative investor sentiment.

High operating costs due to inefficiencies.

Loss of significant market share to competitors resulting in reduced revenues.

Customers switch to competitors as they perform better.

Negative publicity damaging the reputation and revenue.

Reduced cash flow from operations resulting in the inability to invest in growth.

A bad economic downfall can cause the company's financials to plummet and crash due to not being able to excel during bad times.

Increased regulations which will be hard for the company to continue being successful.

New comepetitors creating the exact same service the company gives but better and stronger.

The team is unable to perform due to loss of motivation and unable to adapt in hard times.

Debt increases and the revenue and cash flow decreasing making it hard to keep up with debt payments.

Negative financial results for multiple quarters causing a market crash for the stock.

Overall financials not excelling and decreasing with no improvement.

Due to decreased revenue, profits decrease and it becomes harder to continue growing as a company.

If there are issues within the company and are unable to solve, that will cause the team to decrease in performance. |

7. Risks

Marqeta's transition to profitability is a significant positive, but concerns remain around customer concentration, operating expenses, and the potential for regulatory headwinds. While currently possessing a strong cash position, consistent FCF is needed to reduce long term risk.

Red Flags:

None identified.

8. Conclusion

Marqeta continues to grow its revenue at a moderate pace, driven by increased adoption of its platform among existing and new customers.

Gross margins remain stable.

The company achieves modest profitability as it scales its operations.

It maintains its position as a leading player in the modern card issuing space.

Expansion into new markets and product lines generates steady revenue growth.

Cost management efforts lead to gradual improvements in profitability.

The company maintains its competitive position through ongoing innovation and customer service.

Continued growth with a low valuation.

The company continues to add new customers, leading to continued revenue growth.

Given the data provided, a thorough analysis of Return on Invested Capital (ROIC) and Return on Equity (ROE) is challenging due to fluctuating net income and negative values in some years. In 2024, with a positive net income, ROE can be calculated but needs to be contextualized with previous years of negative returns. Further investigation into the company's asset utilization and capital structure is needed to evaluate its capital efficiency accurately.

Given the data provided, a thorough analysis of Return on Invested Capital (ROIC) and Return on Equity (ROE) is challenging due to fluctuating net income and negative values in some years. In 2024, with a positive net income, ROE can be calculated but needs to be contextualized with previous years of negative returns. Further investigation into the company's asset utilization and capital structure is needed to evaluate its capital efficiency accurately. The company's free cash flow (FCF) has fluctuated, with a significant increase in 2024. This improvement is driven by positive net income and effective working capital management. However, historical trends show inconsistency, and the sustainability of this FCF generation needs to be assessed in light of past performance and future capital expenditure requirements.

The company's free cash flow (FCF) has fluctuated, with a significant increase in 2024. This improvement is driven by positive net income and effective working capital management. However, historical trends show inconsistency, and the sustainability of this FCF generation needs to be assessed in light of past performance and future capital expenditure requirements.