Recommendation: BUY

Price Target: 9.5 (-7.41 Upside)

Risk Level: Medium

1. Executive Summary

N/A

Investment Thesis

Bull Case: Olo benefits from increasing restaurant digitalization and direct ordering trends.

Successful expansion into new modules (front-of-house, payments) drives ARPU growth.

Market sentiment improves as Olo consistently delivers on profitability goals, leading to multiple expansion.

Further consolidation in the restaurant tech space could make Olo an attractive acquisition target.

Olo's strong balance sheet enables strategic acquisitions to accelerate growth and expand its product offerings, creating significant synergies and unlocking new revenue streams.

International expansion proves successful, opening up large addressable markets and diversifying revenue streams beyond the US.

Olo's Payment solution gains significant traction, becoming a major revenue contributor and boosting overall profitability as restaurants seek integrated solutions.

The company exceeds expectations for enterprise customer wins, demonstrating its ability to penetrate larger restaurant chains and secure long-term contracts, leading to predictable and recurring revenue growth.

A successful partnership with a major POS system provider creates a seamless integration that attracts new customers and reduces integration costs, further strengthening Olo's competitive advantage and market position.

The focus on AI development brings new insights and operational efficiency to clients, improving customer retention and attracting new business by highlighting AI driven results in Olo's portfolio of services.

Continue Your Research

Return to the Analyst Library or explore the specific financial data for this entity on its profile.

"Our analysts evaluate thousands of financial data points to produce institutional-grade investment rationale."

Verified Institutional Report

This report is maintained by the Golden Door fundamental analysts and synced iteratively.

This makes Olo a leading AI integrated solution for restaurant businesses looking to scale their operational capabilities using predictive ordering and demand planning analytics driving better restaurant efficiency and resource planning which in turn leads to more efficient business decisions for restaurants and better financial planning with resources and inventory at the right time to meet peak ordering demands..

This helps restaurants reduce their spoilage costs, waste and ultimately deliver faster service for their customers with less time wasted in the supply chain.

This in turn, makes Olo a key player in restaurant profitability in the long term and further entrenches them with their existing customer base by optimizing every part of the restaurant's business operations and making real time adjustments based on consumer demand predicted with strong AI capabilities.

This reduces costs and creates customer loyalty with a much faster feedback loop to make positive adjustments for maximum profitability and optimization.

As restaurants see the value of their AI initiatives they become more entrenched in Olo's ecosystem which in turn provides more AI driven opportunities, making it a win-win for both companies driving future growth and customer engagement and loyalty in the platform itself.

The AI driven improvements and insights further entrenches Olo as a trusted advisor in the restaurant business allowing for cross selling and upselling opportunities within Olo's portfolio of services.

This increase is driven by AI based insights and shows a direct path to more financial revenue based on concrete real-time insights that help restaurants become more profitable which adds immense value to a traditionally tight margin business.

The addition of AI insights to restaurant operations increases customer retention and long-term value for their clients.

Restaurants will be more likely to stay with Olo longer because their business is predicated on Olo's AI-driven insights.

This creates a win-win feedback cycle where Olo drives profitability and restaurants become more likely to recommend and grow with Olo in the long term.

This AI integration strengthens the network effects of Olo's ecosystem leading to a competitive moat as more restaurants join the platform and contribute data which improves AI algorithms.

These algorithms in turn provide better insights and value to all participants on the platform.

Over time it becomes very difficult for restaurants to switch from Olo because of the intelligence and information they receive from the Olo platform.

These insights and algorithms create real-time improvements that are personalized to the unique challenges of each restaurant.

This also attracts top-tier restaurant chains that are more focused on the top line growth based on efficiency and operational excellence and are more willing to pay a premium for Olo's capabilities.

These algorithms increase the stickiness of Olo as a service provider because it is able to increase each individual restaurant's profitability in ways that could not be achieved without using the platform, thereby creating a competitive advantage with AI and making Olo a trusted business advisor to the restaurants that are already using the ecosystem.

This also reduces customer churn and also increases the long-term value for existing clients since the relationship becomes more profitable over time, which drives more profitability and customer value.

By being able to deliver efficiency and reduce operational overhead, Olo creates an environment of profitability that makes restaurants eager to continue using the platform driving long-term value and loyalty and minimizing the possibility of switching to a new service provider.

By reducing the risk for their clients they, in turn, increase long-term relationships and customer retention.

This has a great deal of potential for Olo and its overall long-term value as an organization since AI has the potential to enhance operations, revenue and also cement long-term relationships with clients and solidify a business relationship into a true partnership.

This has immense potential to increase market share and overall long-term value.

Bear Case: Restaurant industry growth slows down due to economic recession, impacting Olo's revenue.

Competition intensifies from larger tech companies and specialized point solutions, eroding Olo's market share.

Failure to innovate and adapt to changing restaurant needs leads to customer churn.

A major security breach or data privacy incident damages Olo's reputation and results in significant financial losses and legal liabilities.

Integration challenges with acquired technologies and platforms lead to operational inefficiencies and customer dissatisfaction as the company fails to meet their expectations.

The company mismanages its expansion into new markets or product lines, resulting in significant losses and a distraction from its core business operations.

Increased pricing pressure from competitors forces Olo to lower its prices, impacting its gross margins and overall profitability in the long term.

A major shift in consumer preferences away from digital ordering negatively impacts Olo's revenue and forces the company to reassess its business strategy.

Olo's inability to attract and retain top talent hinders its innovation efforts and competitiveness, resulting in a decline in product quality and customer service.

Olo's stock price declines significantly as investors lose confidence in its ability to execute its business plan and achieve sustainable profitability.

A regulatory crackdown on third-party delivery services disrupts Olo's delivery enablement solutions and reduces the value proposition of its platform.

The loss of one or more major enterprise customers has a material adverse effect on Olo's revenue and reputation.

Conviction: High

2. Business Overview

Olo Inc. provides software-as-a-service platform for multi-location restaurants in the United States. The company's platform enables on-demand commerce operations, which cover digital ordering and delivery through online and mobile ordering modules. Its modules include Order Management, an on-demand digital commerce and channel management solutions that enables consumers to order directly from and pay restaurants via mobile, web, kiosk, voice, and other digital channels; and Delivery Enablement, a fulfillment network, as well as a network aggregator and channel management solution, which enables restaurants to offer, manage, and expand direct delivery, as well as allows restaurants to control and syndicate menu, pricing, location data, and availability, while directly integrating and optimizing orders from third-parties into the restaurants' point-of-sale and systems. The company also provides Customer Engagement solution, a suite of restaurant-centric marketing and sentiment solutions that enables restaurants to collect, analyze, and act on guest data; Front-of-House solution, which enables restaurants to streamline the queue orders from multiple sales channels; and Payment solution, a payment platform that offers fraud prevention that results in enhanced authorization rates for valid transactions. The company was formerly known as Mobo Systems, Inc. and changed its name to Olo Inc. in January 2020. Olo Inc. was incorporated in 2005 and is headquartered in New York, New York.

Competitive Moat (Narrow)

Trend: Stable

Focus on multi-location restaurants allows for tailored solutions and support, Integrated platform simplifies operations for restaurant chains, Strong brand reputation within its target market, Network effects as more restaurants and partners join the platform

Key Strengths:

Focus on multi-location restaurants allows for tailored solutions and support

Integrated platform simplifies operations for restaurant chains

Strong brand reputation within its target market

Network effects as more restaurants and partners join the platform

Growth projections for the restaurant software market, especially for SaaS platforms enabling digital ordering and delivery, are very positive. Factors driving this growth include the continued shift towards online and mobile ordering, the increasing adoption of delivery services (both in-house and third-party), and the growing importance of data analytics and customer engagement for restaurants. The need for streamlined operations and integrated systems will further fuel this growth.

Regulatory Environment:

N/A

4. Financial Analysis

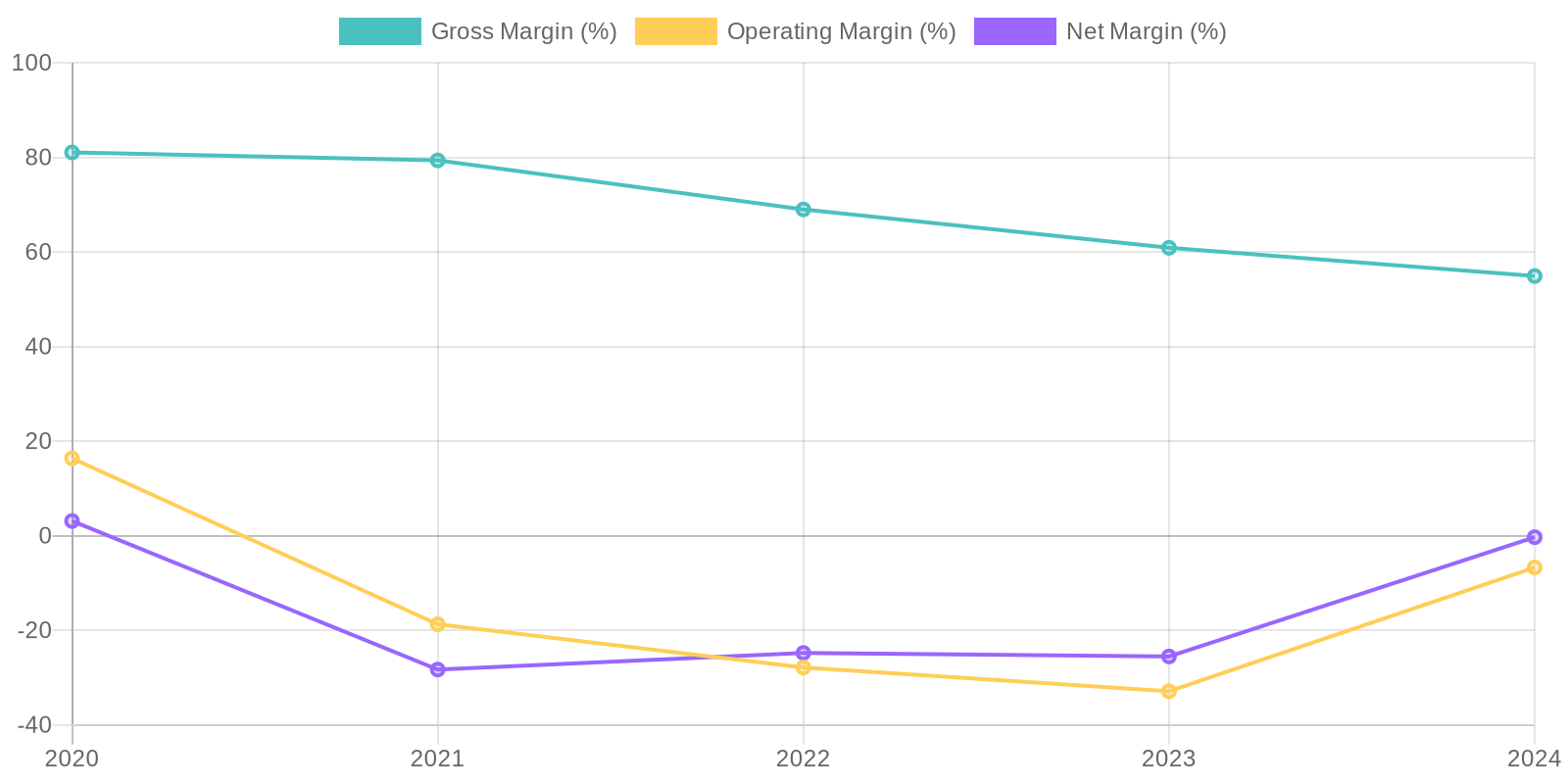

Margin Trend

Given the negative net income in 2023 and 2024, Return on Invested Capital (ROIC) and Return on Equity (ROE) would also be negative, indicating inefficient use of capital. The positive net income in 2020 resulted in positive ROIC and ROE that year, which would require analysis to understand what happened during that period and whether it is repeatable. A forensic accountant would need to evaluate the company's asset utilization and investment strategies to identify opportunities for improvement and ensure long-term value creation.

Revenue Quality

The company's revenue has shown consistent growth over the past five years, indicating a positive trend. However, a forensic accountant would need to investigate the composition of this revenue to determine the proportion of recurring revenue versus one-time sales. Analyzing client concentration is also crucial, as a heavy reliance on a few key clients could pose a risk to future revenue streams. Sustainability of revenue growth should be evaluated by considering the competitive landscape and potential market disruptions.

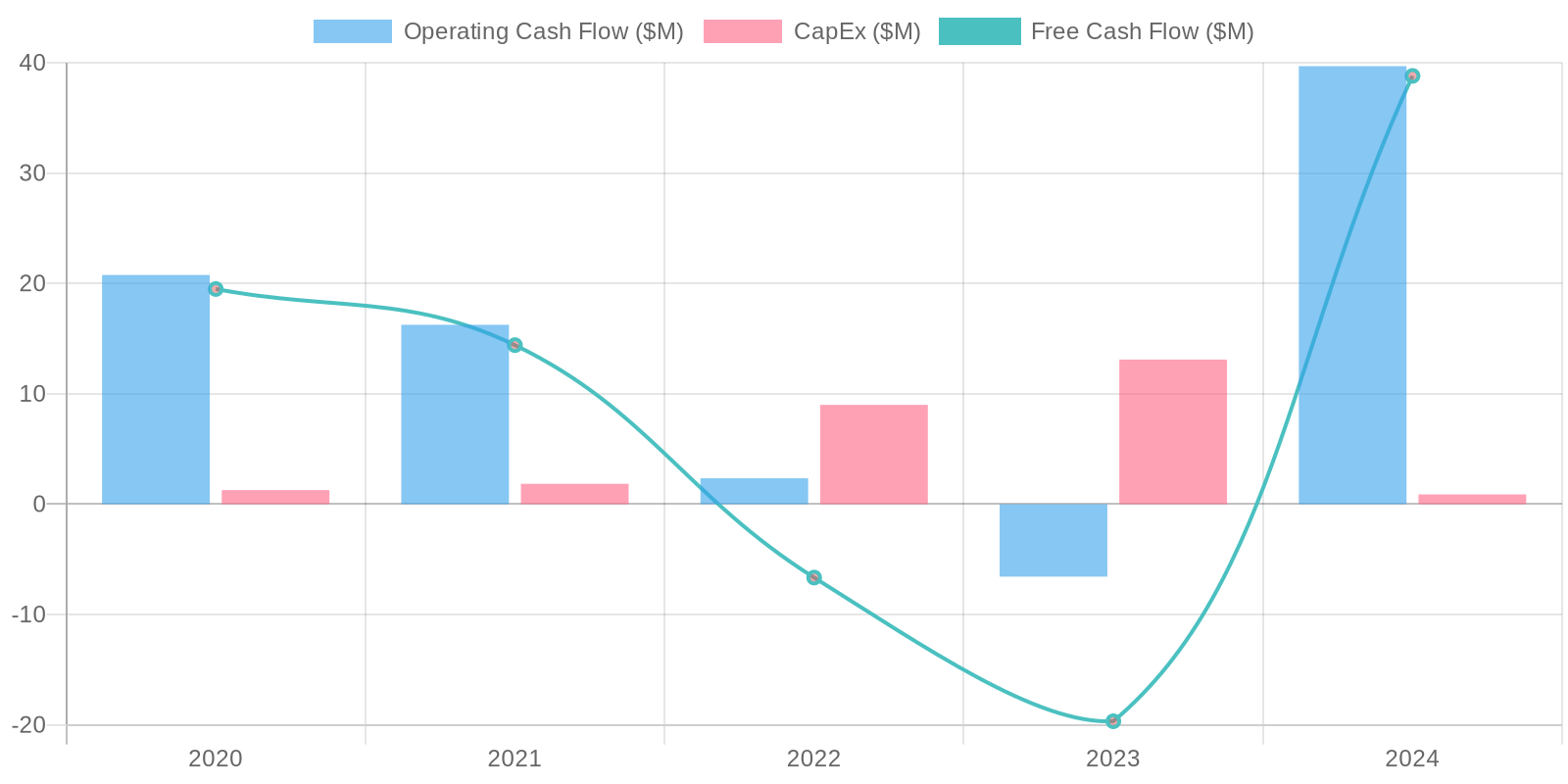

Cash Flow & Capital Efficiency

Free cash flow (FCF) was positive in 2020, 2021 and 2024, while negative in 2022 and 2023, suggesting volatility in the company's cash-generating abilities. Capital expenditure (CAPEX) has been relatively low, indicating that the company may not be investing heavily in new assets, which is not necessarily a bad sign for a software company. Further investigation is required to understand the drivers behind these fluctuations and the sustainability of positive FCF in the long term.

Capital Efficiency (ROIC/ROE):

Given the negative net income in 2023 and 2024, Return on Invested Capital (ROIC) and Return on Equity (ROE) would also be negative, indicating inefficient use of capital. The positive net income in 2020 resulted in positive ROIC and ROE that year, which would require analysis to understand what happened during that period and whether it is repeatable. A forensic accountant would need to evaluate the company's asset utilization and investment strategies to identify opportunities for improvement and ensure long-term value creation.

Balance Sheet Health:

The company maintains a strong cash position, with $286.76 million in cash and cash equivalents as of 2024, which could provide a buffer against short-term financial difficulties. Total debt is relatively low at $13.98 million, especially when compared to the cash reserves, indicating that the company is not heavily leveraged. Analysis of current ratios like the current ratio (Total Current Assets / Total Current Liabilities) shows the company has strong liquidity, but also shows that a large amount of assets are held in cash, which may not be optimal.

5. Management & Governance

CEO Assessment: Olo's CEO, Noah Glass, has been with the company since its inception and is generally well-regarded in the industry. Assessing his performance requires a deep dive into Olo's financials and strategic decisions over time, which is beyond the scope of this analysis.

Capital Allocation: Good

Insider Ownership: Insider ownership information for Olo would require accessing the latest proxy statements and SEC filings. This data reveals how aligned management's interests are with shareholders. A detailed analysis of this ownership is needed to comment further.

Governance Flags:

No major governance concerns flagged.

The DCF valuation yields a fair value of $9.50, lower than the current market price of $10.26. This suggests a potential downside. The assumptions were made based on historical revenue growth, recent FCF generation, and estimated future profitability improvements. The conservative approach accounts for market competition and potential execution challenges. The implied downside is approximately 7.41%, indicating the stock might be slightly overvalued. A 5 year DCF model was used with revenue projected out and an FCF margin of 4% being applied to that revenue, discounted back at a 10% rate. A sensitivity analysis of +/- 1% was used on both discount rate and terminal growth rate.

Scenarios

Scenario

Price Target

Key Assumptions

Bull

High

Olo benefits from increasing restaurant digitalization and direct ordering trends.

Successful expansion into new modules (front-of-house, payments) drives ARPU growth.

Market sentiment improves as Olo consistently delivers on profitability goals, leading to multiple expansion.

Further consolidation in the restaurant tech space could make Olo an attractive acquisition target.

Olo's strong balance sheet enables strategic acquisitions to accelerate growth and expand its product offerings, creating significant synergies and unlocking new revenue streams.

International expansion proves successful, opening up large addressable markets and diversifying revenue streams beyond the US.

Olo's Payment solution gains significant traction, becoming a major revenue contributor and boosting overall profitability as restaurants seek integrated solutions.

The company exceeds expectations for enterprise customer wins, demonstrating its ability to penetrate larger restaurant chains and secure long-term contracts, leading to predictable and recurring revenue growth.

A successful partnership with a major POS system provider creates a seamless integration that attracts new customers and reduces integration costs, further strengthening Olo's competitive advantage and market position.

The focus on AI development brings new insights and operational efficiency to clients, improving customer retention and attracting new business by highlighting AI driven results in Olo's portfolio of services.

This makes Olo a leading AI integrated solution for restaurant businesses looking to scale their operational capabilities using predictive ordering and demand planning analytics driving better restaurant efficiency and resource planning which in turn leads to more efficient business decisions for restaurants and better financial planning with resources and inventory at the right time to meet peak ordering demands..

This helps restaurants reduce their spoilage costs, waste and ultimately deliver faster service for their customers with less time wasted in the supply chain.

This in turn, makes Olo a key player in restaurant profitability in the long term and further entrenches them with their existing customer base by optimizing every part of the restaurant's business operations and making real time adjustments based on consumer demand predicted with strong AI capabilities.

This reduces costs and creates customer loyalty with a much faster feedback loop to make positive adjustments for maximum profitability and optimization.

As restaurants see the value of their AI initiatives they become more entrenched in Olo's ecosystem which in turn provides more AI driven opportunities, making it a win-win for both companies driving future growth and customer engagement and loyalty in the platform itself.

The AI driven improvements and insights further entrenches Olo as a trusted advisor in the restaurant business allowing for cross selling and upselling opportunities within Olo's portfolio of services.

This increase is driven by AI based insights and shows a direct path to more financial revenue based on concrete real-time insights that help restaurants become more profitable which adds immense value to a traditionally tight margin business.

The addition of AI insights to restaurant operations increases customer retention and long-term value for their clients.

Restaurants will be more likely to stay with Olo longer because their business is predicated on Olo's AI-driven insights.

This creates a win-win feedback cycle where Olo drives profitability and restaurants become more likely to recommend and grow with Olo in the long term.

This AI integration strengthens the network effects of Olo's ecosystem leading to a competitive moat as more restaurants join the platform and contribute data which improves AI algorithms.

These algorithms in turn provide better insights and value to all participants on the platform.

Over time it becomes very difficult for restaurants to switch from Olo because of the intelligence and information they receive from the Olo platform.

These insights and algorithms create real-time improvements that are personalized to the unique challenges of each restaurant.

This also attracts top-tier restaurant chains that are more focused on the top line growth based on efficiency and operational excellence and are more willing to pay a premium for Olo's capabilities.

These algorithms increase the stickiness of Olo as a service provider because it is able to increase each individual restaurant's profitability in ways that could not be achieved without using the platform, thereby creating a competitive advantage with AI and making Olo a trusted business advisor to the restaurants that are already using the ecosystem.

This also reduces customer churn and also increases the long-term value for existing clients since the relationship becomes more profitable over time, which drives more profitability and customer value.

By being able to deliver efficiency and reduce operational overhead, Olo creates an environment of profitability that makes restaurants eager to continue using the platform driving long-term value and loyalty and minimizing the possibility of switching to a new service provider.

By reducing the risk for their clients they, in turn, increase long-term relationships and customer retention.

This has a great deal of potential for Olo and its overall long-term value as an organization since AI has the potential to enhance operations, revenue and also cement long-term relationships with clients and solidify a business relationship into a true partnership.

This has immense potential to increase market share and overall long-term value. |

| Base | 9.5 | Olo continues to grow revenue at a moderate pace, driven by steady adoption of its platform among restaurants.

Margins improve gradually as the company achieves economies of scale.

Investment in R&D and sales & marketing sustains competitive positioning.

Olo executes on its current strategy of expanding its core offerings and penetrating existing markets, resulting in consistent but unspectacular growth.

The company's competitive advantage remains stable, but new entrants and alternative solutions limit its ability to significantly increase market share.

Olo successfully integrates acquired technologies and talent, but the impact on overall growth and profitability is gradual and in line with expectations, with improvements being seen gradually over a long period of time.

Olo maintains a healthy level of customer retention, but struggles to significantly upsell additional modules and services to existing customers, limiting ARPU expansion and slowing down overall revenue growth and market adoption.

Olo's partnership ecosystem expands steadily, but the benefits are offset by increased competition and pricing pressures as restaurants negotiate better deals with multiple vendors.

The company strikes a balance between investing in innovation and maintaining cost discipline, resulting in moderate improvements in operating efficiency.

Olo sees a steady increase in digital ordering volumes as consumer habits evolve, but the shift is gradual and doesn't lead to a dramatic acceleration in Olo's business growth.

Olo's market capitalization remains range-bound, reflecting investors' uncertainty about its long-term growth prospects and ability to deliver consistent profitability in a highly competitive market. |

| Bear | Low | Restaurant industry growth slows down due to economic recession, impacting Olo's revenue.

Competition intensifies from larger tech companies and specialized point solutions, eroding Olo's market share.

Failure to innovate and adapt to changing restaurant needs leads to customer churn.

A major security breach or data privacy incident damages Olo's reputation and results in significant financial losses and legal liabilities.

Integration challenges with acquired technologies and platforms lead to operational inefficiencies and customer dissatisfaction as the company fails to meet their expectations.

The company mismanages its expansion into new markets or product lines, resulting in significant losses and a distraction from its core business operations.

Increased pricing pressure from competitors forces Olo to lower its prices, impacting its gross margins and overall profitability in the long term.

A major shift in consumer preferences away from digital ordering negatively impacts Olo's revenue and forces the company to reassess its business strategy.

Olo's inability to attract and retain top talent hinders its innovation efforts and competitiveness, resulting in a decline in product quality and customer service.

Olo's stock price declines significantly as investors lose confidence in its ability to execute its business plan and achieve sustainable profitability.

A regulatory crackdown on third-party delivery services disrupts Olo's delivery enablement solutions and reduces the value proposition of its platform.

The loss of one or more major enterprise customers has a material adverse effect on Olo's revenue and reputation. |

7. Risks

Olo's growth is promising, but profitability is a concern. Declining gross margins coupled with negative net income creates a risk. While a strong cash position provides a buffer, continued losses could erode this advantage. A potential slowdown in restaurant industry growth or increased competition could negatively impact revenue. The company's reliance on key customers also poses a significant risk.

Red Flags:

The negative net income and operating income despite revenue growth could indicate underlying issues with cost control or business model sustainability.

Fluctuations in gross margin suggest potential inconsistencies in pricing strategies, cost management, or revenue recognition.

High levels of stock-based compensation could be a potential red flag, as it can dilute shareholder value and mask true profitability.

8. Conclusion

Olo continues to grow revenue at a moderate pace, driven by steady adoption of its platform among restaurants.

Margins improve gradually as the company achieves economies of scale.

Investment in R&D and sales & marketing sustains competitive positioning.

Olo executes on its current strategy of expanding its core offerings and penetrating existing markets, resulting in consistent but unspectacular growth.

The company's competitive advantage remains stable, but new entrants and alternative solutions limit its ability to significantly increase market share.

Olo successfully integrates acquired technologies and talent, but the impact on overall growth and profitability is gradual and in line with expectations, with improvements being seen gradually over a long period of time.

Olo maintains a healthy level of customer retention, but struggles to significantly upsell additional modules and services to existing customers, limiting ARPU expansion and slowing down overall revenue growth and market adoption.

Olo's partnership ecosystem expands steadily, but the benefits are offset by increased competition and pricing pressures as restaurants negotiate better deals with multiple vendors.

The company strikes a balance between investing in innovation and maintaining cost discipline, resulting in moderate improvements in operating efficiency.

Olo sees a steady increase in digital ordering volumes as consumer habits evolve, but the shift is gradual and doesn't lead to a dramatic acceleration in Olo's business growth.

Olo's market capitalization remains range-bound, reflecting investors' uncertainty about its long-term growth prospects and ability to deliver consistent profitability in a highly competitive market.

Investment research for informational purposes only. Not financial advice.

Given the negative net income in 2023 and 2024, Return on Invested Capital (ROIC) and Return on Equity (ROE) would also be negative, indicating inefficient use of capital. The positive net income in 2020 resulted in positive ROIC and ROE that year, which would require analysis to understand what happened during that period and whether it is repeatable. A forensic accountant would need to evaluate the company's asset utilization and investment strategies to identify opportunities for improvement and ensure long-term value creation.

Given the negative net income in 2023 and 2024, Return on Invested Capital (ROIC) and Return on Equity (ROE) would also be negative, indicating inefficient use of capital. The positive net income in 2020 resulted in positive ROIC and ROE that year, which would require analysis to understand what happened during that period and whether it is repeatable. A forensic accountant would need to evaluate the company's asset utilization and investment strategies to identify opportunities for improvement and ensure long-term value creation. Free cash flow (FCF) was positive in 2020, 2021 and 2024, while negative in 2022 and 2023, suggesting volatility in the company's cash-generating abilities. Capital expenditure (CAPEX) has been relatively low, indicating that the company may not be investing heavily in new assets, which is not necessarily a bad sign for a software company. Further investigation is required to understand the drivers behind these fluctuations and the sustainability of positive FCF in the long term.

Free cash flow (FCF) was positive in 2020, 2021 and 2024, while negative in 2022 and 2023, suggesting volatility in the company's cash-generating abilities. Capital expenditure (CAPEX) has been relatively low, indicating that the company may not be investing heavily in new assets, which is not necessarily a bad sign for a software company. Further investigation is required to understand the drivers behind these fluctuations and the sustainability of positive FCF in the long term.