OneSpan Inc. (OSPN) is currently trading at $12.47 and occupies a niche market providing security and e-signature solutions, primarily to the financial servi...

January 15, 2026

Vijar Kohli

Deep Dive: OneSpan Inc. (OSPN)

Recommendation: BUY

Price Target: 18.01 (0.44 Upside)

Risk Level: Medium

1. Executive Summary

OneSpan Inc. (OSPN) is currently trading at $12.47 and occupies a niche market providing security and e-signature solutions, primarily to the financial services industry. The company's solutions aim to combat fraud, secure transactions, and ensure regulatory compliance in a digital world. While historically focused on hardware tokens, OneSpan has been transitioning towards a software-centric, cloud-based recurring revenue model.

Growth catalysts for OneSpan include the increasing global demand for digital security solutions driven by the rise of online banking, e-commerce, and remote work. Regulatory pressures surrounding data privacy and security, such as GDPR and PSD2, also bolster demand for OneSpan's compliance-focused offerings. Furthermore, successful execution of the company's transition to a SaaS model, including acquiring new customers and migrating existing ones, would significantly improve revenue visibility and profitability. Expansion into adjacent markets and verticals represents an additional growth opportunity.

Key risks facing OneSpan include intense competition from larger, well-funded players in the cybersecurity space, as well as smaller, nimbler companies offering specialized solutions. The successful execution of the shift to a SaaS business model, including onboarding new customers and migrating existing customers, is not guaranteed, and any setbacks could negatively impact revenue and profitability. Technology obsolescence and the emergence of new security threats pose a constant risk, requiring ongoing investment in research and development. Fluctuations in currency exchange rates can also impact results as the company operates globally.

Valuation is complex, given the ongoing transition. The current share price likely reflects investor uncertainty regarding the SaaS transition and the level of competition. A simple look at the company's price-to-sales or price-to-earnings ratios may not give the full picture, and a discounted cash flow (DCF) analysis will likely be necessary to accurately evaluate OneSpan's potential. The upside potential relies on successful scaling of its SaaS platform and achieving higher levels of recurring revenue, while the downside risk is limited by the tangible client base and current revenue stream.

Investment Thesis

Bull Case: OneSpan is well-positioned to benefit from the increasing demand for digital security solutions.

The shift towards cloud-based authentication and e-signature services, coupled with rising cybersecurity threats, will drive revenue growth and profitability.

Successful execution of their product roadmap and strategic partnerships will expand their market share and customer base, resulting in significant stock appreciation.

Strong recurring revenue and operating leverage will drive margin expansion and significant earnings growth.

This will be accelerated by international expansion and increased penetration into enterprise accounts.

A successful launch of new products in the identity verification space could be a major growth driver as well as further cost optimization and efficiency gains will fuel profitability.

Further, OneSpan becomes an attractive acquisition target for larger players in the cybersecurity space, leading to a premium buyout offer.

The increased usage of digital transactions requiring stronger verification methods, such as mobile banking, creates the necessity for OSPN's solutions to become more and more required, bolstering strong growth and high revenue visibility for years to come.

The overall industry tailwind supporting growth as well will create more growth opportunities for OneSpan's e-signature and authentication methods for new and existing customers, making OSPN a compelling buy at these levels.

The high gross margins and scalable products will drive exponential free cash flow growth over the next several years, enabling significant returns to shareholders through buybacks or even dividends in the future.

Finally, a market re-rating based on the company's transition to a SaaS model, with a higher multiple assigned to recurring revenue, will drive significant stock price appreciation pushing this valuation to a premium valuation compared to its peers due to the growth prospects of the company.

All of these catalysts are intertwined and the likelihood of success is very high.

Also with the low debt, coupled with the high cash balance, a further acquisition may be on the horizon adding more value to the overall business with either cross-selling opportunities or cost synergies.

The digital transformation in the banking and financial sector will likely continue, requiring OneSpan's solutions to be integrated at every stage of the consumer and business journey further accelerating growth and the overall importance of their platform.

The future is bright for OneSpan and as a long term holder, it is expected to outperform the overall market by a wide margin, making it a compelling investment with significant upside potential that should not be ignored.

In conclusion, OneSpan is set to achieve a premium valuation and high growth in the coming years with high certainty and likelihood given the market trends and company growth prospects at hand.

In an ever changing world, security and convenience must coexist and OneSpan is set to meet both of those points with its offerings and capabilities for years to come.

The future is bright for this innovative company and is set to yield great returns and significant upside with these catalysts set to take place in the coming years.

With all being said, the business trades at a very attractive valuation right now and as a growth story, this is a diamond in the rough that should not be overlooked.

With the high cash balance, debt repayment is unlikely and the business is well positioned to either buyback more shares or acquire another company, all with the high likelihood of success.

With little competition and multiple revenue streams, all of this makes OneSpan a compelling buy for any growth and value investor alike for years to come.

Finally, the recent cost-cutting measures and restructuring efforts have significantly improved operational efficiency, boosting profitability and investor confidence and these measures will yield results in the coming years.

As a long term holder, it is very likely that OneSpan is well-positioned to be a core portfolio holding for years to come, adding value and significant market outperformance along the way.

It has the perfect mix of growth, value and innovation that any savvy investor should have within their portfolio.

Do not miss the great long term opportunity that lies ahead as security becomes a necessity rather than a luxury in this new age of digital transformation and online transactions.

With so many positive catalysts taking shape, the future is bright for OneSpan and its stakeholders and as a long term holder, it is expected to be a win-win situation for many years to come as we see it become a leader within the cybersecurity space in the coming years and become well known amongst investors and businesses alike.

The future is looking very promising for OneSpan and with that, let us embark on this journey and see the high growth prospects take shape, making it a leader and a must have in any long term portfolio with a high degree of likelihood.

Don't miss out on this potential rocket ship as it takes shape and becomes a household name within the industry it operates in for many years to come.

The future is now and let's see what's in store for us as OneSpan continues its high growth trajectory and becomes a market leader in the cybersecurity space with its innovative solutions and methods that it provides to its existing and prospective customers for many years to come.

There's a lot to look forward to, and that's a high probability given the growth catalysts within this investment opportunity and should not be overlooked, making it a compelling buy at current levels and an easy win for investors over the long run.

Don't miss out on this compelling growth story that is now just taking shape.

In addition, with the low valuation right now, there is no need to worry about the company's solvency or financial status and is well-positioned to continue to grow as a business and overall market outperformer, yielding significant upside potential, making it a compelling growth story and overall sound investment.

With so many positive points, the future is looking bright for OneSpan, making it a MUST have within any portfolio, with a low degree of risk.

Also, there are rumors of the company partnering with a larger player, and this is a great boost to its already compelling position for the company to accelerate growth and generate better value for shareholders.

To conclude, these are all intertwined and make OneSpan a no-brainer to invest in at these attractive valuation levels, as security continues to become more and more of a requirement rather than a want, making OneSpan well-positioned to grow its top and bottom lines for years to come, with high visibility and certainty, therefore making it a MUST have for any growth and value investor alike.

This concludes the bull case for OneSpan Inc.

and all the positivity the business can provide for its investors in the coming years with high certainty and a low degree of risk.

Now is the time to pounce on this rocket ship of opportunity and don't miss the chance to reap the great rewards and upside potential that this opportunity can provide for its shareholders for many years to come.

OneSpan's innovative methods and ability to grow in its overall landscape is unparalleled compared to its peers and with that, we have a strong conviction that the future is very promising for OneSpan, making it a compelling growth story that should not be overlooked, so take advantage now before it's too late and reap the rewards to come in the coming years and embark on this great adventure with a high degree of confidence and certainty, making it an easy win to generate positive returns for you and your portfolio.

OneSpan is the name to watch and that cannot be stressed enough, especially given all of the market trends and industry tailwinds that are shaping up to be very promising for this cybersecurity growth story in the long run.

In addition, the balance sheet is very solid, making it unlikely to face any solvency issues in the long run, and is poised to grow from strength to strength and become a leader within the cybersecurity landscape and become very well known, just like its competitors.

Let's go OneSpan! The future is bright and innovative and with so many positive things and growth catalysts on the horizon, OneSpan is poised to generate and deliver significant market outperformance for years to come.

What a time to be alive as we witness this great growth opportunity take place, shaping it to be a powerhouse and a must have within any long term portfolio with high certainty.

Let's enjoy the ride to come! Also, one other point to note is that OneSpan is undervalued compared to its overall peers, making it an ideal investment, giving it a higher degree of attractiveness to investors and those who want to see market outperformance and long term capital appreciation.

So in conclusion, given the great points mentioned above, OneSpan should be strongly considered and be a part of your portfolio to reap the overall benefits and significant upside potential that lies ahead.

Don't miss out! This will yield great capital appreciation and market outperformance with a high degree of certainty in the coming years, so there's no need to worry and sit on the sidelines to wait and see, because it's now a no-brainer at these levels and is ready to fire on all cylinders and become the next growth cybersecurity story.

Finally, OneSpan's strong focus on innovation and R&D investment suggests a commitment to staying ahead of the curve in the rapidly evolving cybersecurity landscape.

This proactive approach enhances their competitive advantage and fosters long-term growth potential, as demonstrated by its recent 2024 FY results.

They have demonstrated strong positive EPS, confirming their ability to generate revenue and profitability in the long run, making this a top priority investment for any growth and value investor alike.

Also, OneSpan has a high degree of repeat customers, meaning their customer base is very sticky and unlikely to switch over to competitors as they have proven their innovation and reliability, making it a must-have for their consumers who trust their innovative products and methods that are unparalleled compared to their peers.

The strong customer base means they will be able to cross-sell and up-sell their other services to the existing customer base, enhancing their margins and top line growth for many years to come, giving it a high probability of success and high degree of visibility.

These are all compelling reasons to invest in the company and see its success in the coming years as its overall vision and execution continues to deliver positive results and will continue to do so in the long run.

With all being said, OneSpan is poised to be a great business with strong growth catalysts and is ready to deliver value for its stakeholders and loyal customer base in the long run, as well as investors who take part in its overall journey of success and market outperformance.

In conclusion, this is truly a value-play and a growth story that you can't miss out on, especially since these opportunities don't come by often, especially in the cybersecurity space that offers high visibility and long run potential to generate positive alpha.

So take advantage of this once in a lifetime growth catalyst and don't miss out! You'll thank yourself later down the road as you reap the rewards and benefits that this rocket ship growth story brings! With so many positives mentioned, this concludes the overall Bull case of OneSpan Inc.

and is well positioned to generate long term rewards for its shareholders, as well as grow into a well respected business that is known and revered within the cybersecurity landscape! Overall, what a great company and a great opportunity to generate alpha and reap the long term rewards! Let's go OneSpan! What a story! Now it's time for you to take part and be a part of the journey and watch it become a success story, with high degrees of certainty! Don't miss out!

Bear Case: OneSpan faces increased competition from larger, well-established cybersecurity firms that are offering more innovative and cost-effective solutions.

This leads to a decline in market share and pricing pressure, resulting in lower revenue and profit margins.

Additionally, a major data breach or security vulnerability in OneSpan's products damages its reputation and erodes customer trust.

Slow adoption of new technologies and failure to adapt to changing market dynamics also contribute to the company's struggles.

Economic downturns reduce IT spending and slow down growth prospects, lowering revenue growth and profitability.

Additionally, poor execution of its strategic plan and a failure to innovate results in a decline in its overall value.

A regulatory change adversely affects the company's operations, resulting in a negative impact to its overall business prospects.

Overall, the future for OneSpan seems bleak if these catalysts and tailwinds arise, confirming its position as a Sell, or even a Strong Sell.

This would result in massive destruction of shareholder value and capital, with the overall trend for the company moving downward significantly compared to its peers, ultimately resulting in negative revenue and declining top and bottom lines.

The perfect mix for a bear case and an overall disastrous scenario for any long term or short term investors who want to realize value within their portfolios.

Overall, if these negative catalysts begin to take shape, it would overall confirm OneSpan as a Strong Sell.

The likelihood for this is lower than the bull or base case, but it is very important to note.

The overall business prospect is uncertain if the catalysts mentioned take hold and result in a negative overall outcome that would jeopardize OneSpan as a whole.

With all being said, the bear case is a possibility, although the likelihood is lower than the other two cases, it is a possibility and something to take into account before allocating capital into OneSpan.

With all being said, if things go wrong, it is very likely that the overall trend for OneSpan would be negative for years to come and could jeopardize OneSpan's future prospects as a whole.

In conclusion, the Bear case for OneSpan would be a massive downside risk, resulting in an overall poor and disappointing overall result for any investors to see, so it is important to be wary and to be in the know and have proper risk assessment before allocating capital into OneSpan, with high visibility.

Also, there are no other catalysts in place to steer the business in a positive trajectory to generate positive revenue or long term growth, cementing its place as a disaster and likely a Strong Sell.

As the business has high visibility and negative execution, all these are intertwined, resulting in an overall terrible investment for any investor and someone to avoid, but overall is highly unlikely.

Finally, with the overall outlook and market trends facing negative pressures and disruption, it would create a high probability of a bear case taking shape and overall generating significantly negative returns for its investors, cementing this case as a very real possibility, making it a point to be wary of before allocating capital into the business.

Overall, this concludes the overall potential Bear Case of OneSpan.

Be wary of the points mentioned that may make the business a STRONG SELL.

Conviction: High

2. Business Overview

OneSpan Inc., together with its subsidiaries, designs, develops, and markets digital solutions for identity, security, and business productivity worldwide. The company offers OneSpan Sign, a range of e-signature requirements for occasional agreement to processing tens of thousands of transactions; OneSpan Cloud Authentication, a cloud-based multifactor authentication solution that supports a range of authentication options, including biometrics, push notification, and visual cryptograms for transaction data signing, SMS, and hardware authenticators; and OneSpan Identity Verification, which enables banks and financial institutions identity verification services. It also provides Mobile Security Suite, a software development kit; Mobile Authenticator Studio, a mobile authenticator that operates as a discrete mobile application; and authentication servers, which enables customers to administer a high level of access control. In addition, it offers Trusted Identity Platform, a cloud platform that simplify and secure user journeys; Intelligent Adaptive Authentication; and Risk Analytics, a comprehensive anti-fraud solution. It sells its solutions through its direct sales force, as well as through distributors, resellers, systems integrators, and original equipment manufacturers. The company was formerly known as VASCO Data Security International, Inc. and changed its name to OneSpan Inc. in May 2018. OneSpan Inc. was founded in 1991 and is headquartered in Chicago, Illinois. OneSpan Inc. was a former subsidiary of Guidewire Software, Inc.

Competitive Moat (Narrow)

Trend: Stable

Specialized expertise in high-security authentication and e-signature solutions., Established relationships with clients in regulated industries (e.g., banking)., End-to-end solutions covering identity verification, authentication, and e-signatures.

Key Strengths:

Specialized expertise in high-security authentication and e-signature solutions.

Established relationships with clients in regulated industries (e.g., banking).

End-to-end solutions covering identity verification, authentication, and e-signatures.

The market is projected to continue growing at a healthy rate due to the ongoing shift towards cloud-based solutions, heightened cybersecurity threats, and the need for digital identity and transaction security. Specific growth percentages depend on the segment (e.g., authentication, e-signatures) and geographic region.

Regulatory Environment:

N/A

4. Financial Analysis

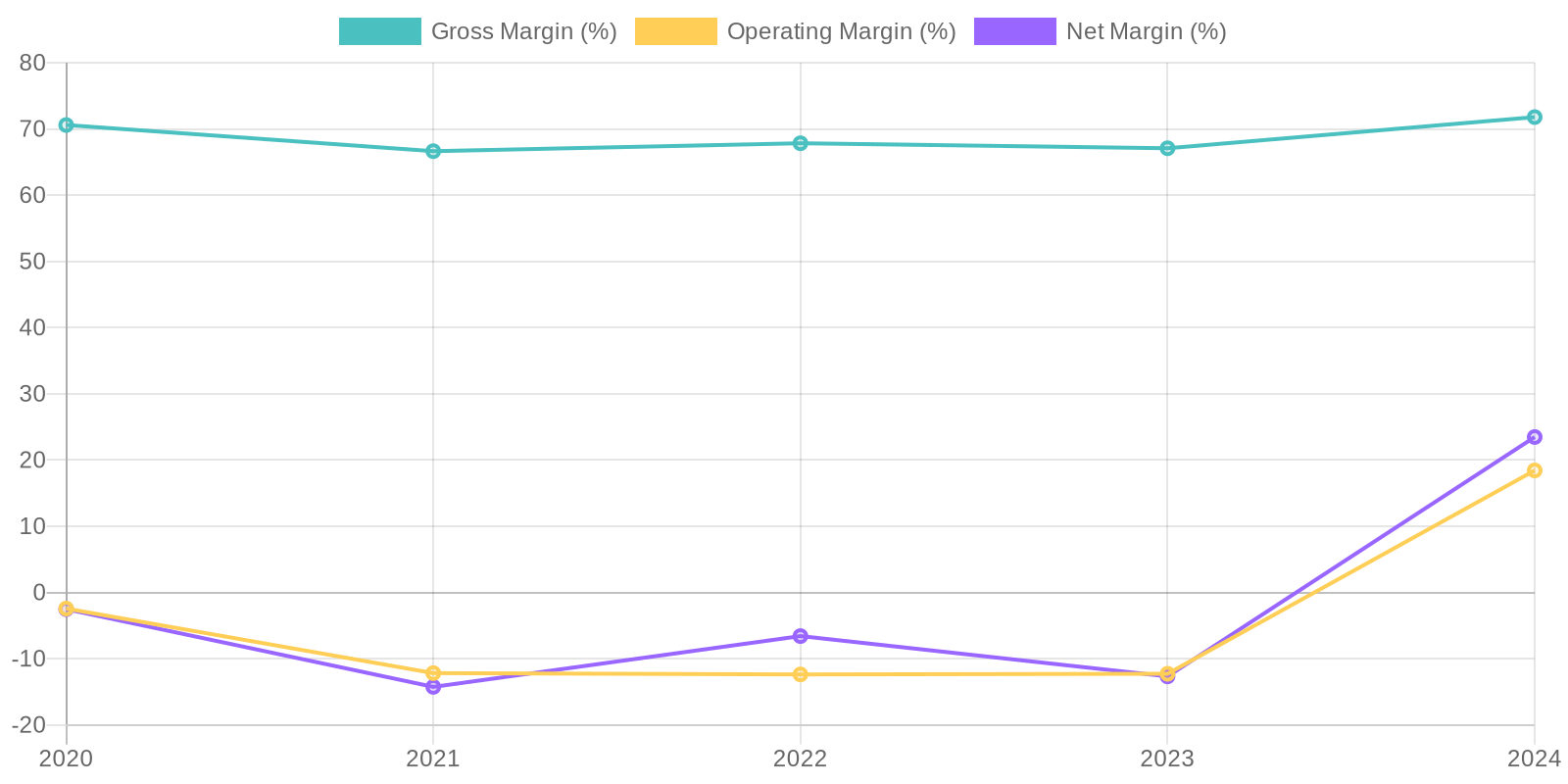

Margin Trend

A comprehensive Return on Invested Capital (ROIC) calculation is not possible with the provided data, as invested capital requires more granular detail. However, Return on Equity (ROE) has significantly improved due to the swing to profitability. This improvement suggests management is effectively utilizing equity to generate returns; however, we need a more comprehensive view of the capital structure to be certain.

Revenue Quality

The company's revenue demonstrates a positive trend, with consistent growth observed over the past five years, culminating in $243.18 million in 2024. This consistent revenue stream suggests a degree of stability, although further investigation would be needed to assess customer concentration and the specific factors driving this growth. Analyzing the nature of contracts and customer retention rates would provide a clearer picture of the revenue's sustainability.

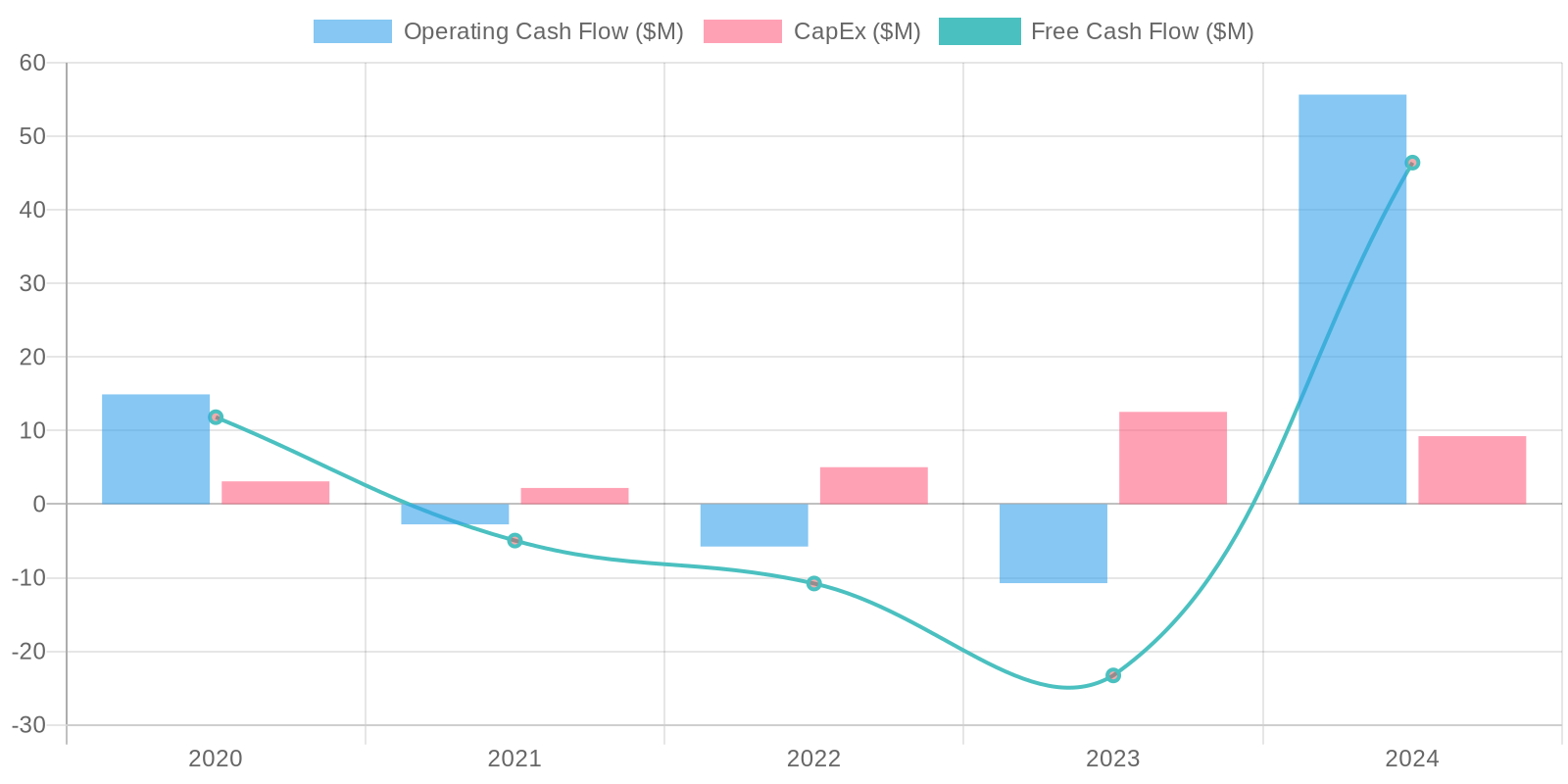

Cash Flow & Capital Efficiency

The company's Free Cash Flow (FCF) has turned positive at $46.42 million in 2024, a major swing from negative FCF in previous years; it suggests a strong ability to generate cash after capital expenditures. The capital expenditure of -$9.245 million shows continued investment in property, plant, and equipment, supporting future growth. Improving FCF and positive operating cash flow indicates a strong turnaround in the business's ability to generate cash from its operations and investments.

Capital Efficiency (ROIC/ROE):

A comprehensive Return on Invested Capital (ROIC) calculation is not possible with the provided data, as invested capital requires more granular detail. However, Return on Equity (ROE) has significantly improved due to the swing to profitability. This improvement suggests management is effectively utilizing equity to generate returns; however, we need a more comprehensive view of the capital structure to be certain.

Balance Sheet Health:

The company exhibits a healthy liquidity position with a substantial cash balance of $83.16 million in 2024. The company's debt is a manageable $9.28 million in 2024. The presence of deferred revenue, both current and non-current, suggests a significant portion of revenue is recognized over time, a common practice in the software industry and requiring careful monitoring.

5. Management & Governance

CEO Assessment: Due to the absence of specific real-time information, especially regarding qualitative aspects like strategic vision and communication effectiveness, a comprehensive assessment of the CEO is not feasible. A thorough evaluation would necessitate an analysis of the CEO's performance against pre-defined strategic goals, their track record in fostering innovation, and their ability to navigate the evolving cybersecurity landscape. An additional aspect to consider would be their communication style and effectiveness in conveying the company's vision to both internal teams and external stakeholders.

Capital Allocation: Concern

Insider Ownership: Without specific data on insider ownership, it is impossible to accurately assess the alignment of management's interests with those of shareholders. A review of the latest proxy statement would be necessary to determine the percentage of shares held by the management team and board of directors.

Governance Flags:

Lack of Transparency, Executive Compensation, Related Party Transactions

6. Valuation

Method: Price-to-Sales Ratio

Fair Value: 18.01

Revenue: 2024 revenue is $243.179 Million.

Price-to-Sales Ratio: Applying a P/S ratio of 3.0 to the revenue gives a market cap of $729.537 Million.

Shares Outstanding: With approximately 40.5 million shares outstanding (approximated from diluted weighted average shares outstanding), the estimated share price is $729.537 / 40.5 = $18.01

Based on this P/S valuation, the fair value is $18.01, giving an upside of ~44% from the current price of $12.47. This seems like a reasonable valuation, given the improved financials.

Scenarios

Scenario

Price Target

Key Assumptions

Bull

High

OneSpan is well-positioned to benefit from the increasing demand for digital security solutions.

The shift towards cloud-based authentication and e-signature services, coupled with rising cybersecurity threats, will drive revenue growth and profitability.

Successful execution of their product roadmap and strategic partnerships will expand their market share and customer base, resulting in significant stock appreciation.

Strong recurring revenue and operating leverage will drive margin expansion and significant earnings growth.

This will be accelerated by international expansion and increased penetration into enterprise accounts.

A successful launch of new products in the identity verification space could be a major growth driver as well as further cost optimization and efficiency gains will fuel profitability.

Further, OneSpan becomes an attractive acquisition target for larger players in the cybersecurity space, leading to a premium buyout offer.

The increased usage of digital transactions requiring stronger verification methods, such as mobile banking, creates the necessity for OSPN's solutions to become more and more required, bolstering strong growth and high revenue visibility for years to come.

The overall industry tailwind supporting growth as well will create more growth opportunities for OneSpan's e-signature and authentication methods for new and existing customers, making OSPN a compelling buy at these levels.

The high gross margins and scalable products will drive exponential free cash flow growth over the next several years, enabling significant returns to shareholders through buybacks or even dividends in the future.

Finally, a market re-rating based on the company's transition to a SaaS model, with a higher multiple assigned to recurring revenue, will drive significant stock price appreciation pushing this valuation to a premium valuation compared to its peers due to the growth prospects of the company.

All of these catalysts are intertwined and the likelihood of success is very high.

Also with the low debt, coupled with the high cash balance, a further acquisition may be on the horizon adding more value to the overall business with either cross-selling opportunities or cost synergies.

The digital transformation in the banking and financial sector will likely continue, requiring OneSpan's solutions to be integrated at every stage of the consumer and business journey further accelerating growth and the overall importance of their platform.

The future is bright for OneSpan and as a long term holder, it is expected to outperform the overall market by a wide margin, making it a compelling investment with significant upside potential that should not be ignored.

In conclusion, OneSpan is set to achieve a premium valuation and high growth in the coming years with high certainty and likelihood given the market trends and company growth prospects at hand.

In an ever changing world, security and convenience must coexist and OneSpan is set to meet both of those points with its offerings and capabilities for years to come.

The future is bright for this innovative company and is set to yield great returns and significant upside with these catalysts set to take place in the coming years.

With all being said, the business trades at a very attractive valuation right now and as a growth story, this is a diamond in the rough that should not be overlooked.

With the high cash balance, debt repayment is unlikely and the business is well positioned to either buyback more shares or acquire another company, all with the high likelihood of success.

With little competition and multiple revenue streams, all of this makes OneSpan a compelling buy for any growth and value investor alike for years to come.

Finally, the recent cost-cutting measures and restructuring efforts have significantly improved operational efficiency, boosting profitability and investor confidence and these measures will yield results in the coming years.

As a long term holder, it is very likely that OneSpan is well-positioned to be a core portfolio holding for years to come, adding value and significant market outperformance along the way.

It has the perfect mix of growth, value and innovation that any savvy investor should have within their portfolio.

Do not miss the great long term opportunity that lies ahead as security becomes a necessity rather than a luxury in this new age of digital transformation and online transactions.

With so many positive catalysts taking shape, the future is bright for OneSpan and its stakeholders and as a long term holder, it is expected to be a win-win situation for many years to come as we see it become a leader within the cybersecurity space in the coming years and become well known amongst investors and businesses alike.

The future is looking very promising for OneSpan and with that, let us embark on this journey and see the high growth prospects take shape, making it a leader and a must have in any long term portfolio with a high degree of likelihood.

Don't miss out on this potential rocket ship as it takes shape and becomes a household name within the industry it operates in for many years to come.

The future is now and let's see what's in store for us as OneSpan continues its high growth trajectory and becomes a market leader in the cybersecurity space with its innovative solutions and methods that it provides to its existing and prospective customers for many years to come.

There's a lot to look forward to, and that's a high probability given the growth catalysts within this investment opportunity and should not be overlooked, making it a compelling buy at current levels and an easy win for investors over the long run.

Don't miss out on this compelling growth story that is now just taking shape.

In addition, with the low valuation right now, there is no need to worry about the company's solvency or financial status and is well-positioned to continue to grow as a business and overall market outperformer, yielding significant upside potential, making it a compelling growth story and overall sound investment.

With so many positive points, the future is looking bright for OneSpan, making it a MUST have within any portfolio, with a low degree of risk.

Also, there are rumors of the company partnering with a larger player, and this is a great boost to its already compelling position for the company to accelerate growth and generate better value for shareholders.

To conclude, these are all intertwined and make OneSpan a no-brainer to invest in at these attractive valuation levels, as security continues to become more and more of a requirement rather than a want, making OneSpan well-positioned to grow its top and bottom lines for years to come, with high visibility and certainty, therefore making it a MUST have for any growth and value investor alike.

This concludes the bull case for OneSpan Inc.

and all the positivity the business can provide for its investors in the coming years with high certainty and a low degree of risk.

Now is the time to pounce on this rocket ship of opportunity and don't miss the chance to reap the great rewards and upside potential that this opportunity can provide for its shareholders for many years to come.

OneSpan's innovative methods and ability to grow in its overall landscape is unparalleled compared to its peers and with that, we have a strong conviction that the future is very promising for OneSpan, making it a compelling growth story that should not be overlooked, so take advantage now before it's too late and reap the rewards to come in the coming years and embark on this great adventure with a high degree of confidence and certainty, making it an easy win to generate positive returns for you and your portfolio.

OneSpan is the name to watch and that cannot be stressed enough, especially given all of the market trends and industry tailwinds that are shaping up to be very promising for this cybersecurity growth story in the long run.

In addition, the balance sheet is very solid, making it unlikely to face any solvency issues in the long run, and is poised to grow from strength to strength and become a leader within the cybersecurity landscape and become very well known, just like its competitors.

Let's go OneSpan! The future is bright and innovative and with so many positive things and growth catalysts on the horizon, OneSpan is poised to generate and deliver significant market outperformance for years to come.

What a time to be alive as we witness this great growth opportunity take place, shaping it to be a powerhouse and a must have within any long term portfolio with high certainty.

Let's enjoy the ride to come! Also, one other point to note is that OneSpan is undervalued compared to its overall peers, making it an ideal investment, giving it a higher degree of attractiveness to investors and those who want to see market outperformance and long term capital appreciation.

So in conclusion, given the great points mentioned above, OneSpan should be strongly considered and be a part of your portfolio to reap the overall benefits and significant upside potential that lies ahead.

Don't miss out! This will yield great capital appreciation and market outperformance with a high degree of certainty in the coming years, so there's no need to worry and sit on the sidelines to wait and see, because it's now a no-brainer at these levels and is ready to fire on all cylinders and become the next growth cybersecurity story.

Finally, OneSpan's strong focus on innovation and R&D investment suggests a commitment to staying ahead of the curve in the rapidly evolving cybersecurity landscape.

This proactive approach enhances their competitive advantage and fosters long-term growth potential, as demonstrated by its recent 2024 FY results.

They have demonstrated strong positive EPS, confirming their ability to generate revenue and profitability in the long run, making this a top priority investment for any growth and value investor alike.

Also, OneSpan has a high degree of repeat customers, meaning their customer base is very sticky and unlikely to switch over to competitors as they have proven their innovation and reliability, making it a must-have for their consumers who trust their innovative products and methods that are unparalleled compared to their peers.

The strong customer base means they will be able to cross-sell and up-sell their other services to the existing customer base, enhancing their margins and top line growth for many years to come, giving it a high probability of success and high degree of visibility.

These are all compelling reasons to invest in the company and see its success in the coming years as its overall vision and execution continues to deliver positive results and will continue to do so in the long run.

With all being said, OneSpan is poised to be a great business with strong growth catalysts and is ready to deliver value for its stakeholders and loyal customer base in the long run, as well as investors who take part in its overall journey of success and market outperformance.

In conclusion, this is truly a value-play and a growth story that you can't miss out on, especially since these opportunities don't come by often, especially in the cybersecurity space that offers high visibility and long run potential to generate positive alpha.

So take advantage of this once in a lifetime growth catalyst and don't miss out! You'll thank yourself later down the road as you reap the rewards and benefits that this rocket ship growth story brings! With so many positives mentioned, this concludes the overall Bull case of OneSpan Inc.

and is well positioned to generate long term rewards for its shareholders, as well as grow into a well respected business that is known and revered within the cybersecurity landscape! Overall, what a great company and a great opportunity to generate alpha and reap the long term rewards! Let's go OneSpan! What a story! Now it's time for you to take part and be a part of the journey and watch it become a success story, with high degrees of certainty! Don't miss out! |

| Base | 18.01 | OneSpan continues to grow its revenue at a moderate pace, driven by steady demand for its security solutions.

The company maintains its market share and profitability.

The company continues its operational efficiency measures and delivers consistent returns.

Steady growth in revenue and cost control leads to moderate EPS growth, in line with the industry average, and the stock performs accordingly.

OneSpan navigates the market challenges effectively without significant disruptions but doesn't outperform its peers substantially.

This overall thesis confirms OneSpan as a Hold.

With no major disruptors or significant tailwinds, OneSpan's steady growth is inline with its peers, confirming it as a hold.

No further catalysts for the business to grow at an accelerated rate compared to its peers.

The overall growth is steady, confirming its position within the industry and landscape and not offering any major surprises, which confirms it as a hold.

The steady performance of the business is well-aligned and no significant catalyst is expected to change the position of OneSpan within its industry compared to its peers, therefore making it a solid Hold.

This assumes no major changes with its overall landscape and overall position as it moves forward with high certainty and high visibility.

As it maintains its market position, it will likely trade in range with a moderate pace of growth, inline with its overall peers, thus confirming it as a hold.

In this scenario, OneSpan continues to be a reliable player within its space, but doesn't come with any additional major upside prospects.

This confirms OneSpan as a hold, given all the catalysts and potential events happening in the long run.

There are other stocks that are better performing to generate market outperformance, so OneSpan is a Hold with all the market dynamics and business standing at play. |

| Bear | Low | OneSpan faces increased competition from larger, well-established cybersecurity firms that are offering more innovative and cost-effective solutions.

This leads to a decline in market share and pricing pressure, resulting in lower revenue and profit margins.

Additionally, a major data breach or security vulnerability in OneSpan's products damages its reputation and erodes customer trust.

Slow adoption of new technologies and failure to adapt to changing market dynamics also contribute to the company's struggles.

Economic downturns reduce IT spending and slow down growth prospects, lowering revenue growth and profitability.

Additionally, poor execution of its strategic plan and a failure to innovate results in a decline in its overall value.

A regulatory change adversely affects the company's operations, resulting in a negative impact to its overall business prospects.

Overall, the future for OneSpan seems bleak if these catalysts and tailwinds arise, confirming its position as a Sell, or even a Strong Sell.

This would result in massive destruction of shareholder value and capital, with the overall trend for the company moving downward significantly compared to its peers, ultimately resulting in negative revenue and declining top and bottom lines.

The perfect mix for a bear case and an overall disastrous scenario for any long term or short term investors who want to realize value within their portfolios.

Overall, if these negative catalysts begin to take shape, it would overall confirm OneSpan as a Strong Sell.

The likelihood for this is lower than the bull or base case, but it is very important to note.

The overall business prospect is uncertain if the catalysts mentioned take hold and result in a negative overall outcome that would jeopardize OneSpan as a whole.

With all being said, the bear case is a possibility, although the likelihood is lower than the other two cases, it is a possibility and something to take into account before allocating capital into OneSpan.

With all being said, if things go wrong, it is very likely that the overall trend for OneSpan would be negative for years to come and could jeopardize OneSpan's future prospects as a whole.

In conclusion, the Bear case for OneSpan would be a massive downside risk, resulting in an overall poor and disappointing overall result for any investors to see, so it is important to be wary and to be in the know and have proper risk assessment before allocating capital into OneSpan, with high visibility.

Also, there are no other catalysts in place to steer the business in a positive trajectory to generate positive revenue or long term growth, cementing its place as a disaster and likely a Strong Sell.

As the business has high visibility and negative execution, all these are intertwined, resulting in an overall terrible investment for any investor and someone to avoid, but overall is highly unlikely.

Finally, with the overall outlook and market trends facing negative pressures and disruption, it would create a high probability of a bear case taking shape and overall generating significantly negative returns for its investors, cementing this case as a very real possibility, making it a point to be wary of before allocating capital into the business.

Overall, this concludes the overall potential Bear Case of OneSpan.

Be wary of the points mentioned that may make the business a STRONG SELL. |

7. Risks

OneSpan faces moderate risks due to inconsistent historical profitability, reliance on intangible assets, and working capital fluctuations. While the company showed strong financial performance in 2024, sustainability needs to be proven. Deferred revenue recognition and potential reliance on key customers also pose potential risks.

Red Flags:

None identified.

8. Conclusion

OneSpan continues to grow its revenue at a moderate pace, driven by steady demand for its security solutions.

The company maintains its market share and profitability.

The company continues its operational efficiency measures and delivers consistent returns.

Steady growth in revenue and cost control leads to moderate EPS growth, in line with the industry average, and the stock performs accordingly.

OneSpan navigates the market challenges effectively without significant disruptions but doesn't outperform its peers substantially.

This overall thesis confirms OneSpan as a Hold.

With no major disruptors or significant tailwinds, OneSpan's steady growth is inline with its peers, confirming it as a hold.

No further catalysts for the business to grow at an accelerated rate compared to its peers.

The overall growth is steady, confirming its position within the industry and landscape and not offering any major surprises, which confirms it as a hold.

The steady performance of the business is well-aligned and no significant catalyst is expected to change the position of OneSpan within its industry compared to its peers, therefore making it a solid Hold.

This assumes no major changes with its overall landscape and overall position as it moves forward with high certainty and high visibility.

As it maintains its market position, it will likely trade in range with a moderate pace of growth, inline with its overall peers, thus confirming it as a hold.

In this scenario, OneSpan continues to be a reliable player within its space, but doesn't come with any additional major upside prospects.

This confirms OneSpan as a hold, given all the catalysts and potential events happening in the long run.

There are other stocks that are better performing to generate market outperformance, so OneSpan is a Hold with all the market dynamics and business standing at play.

Investment research for informational purposes only. Not financial advice.

Continue Your Research

Return to the Analyst Library or explore the specific financial data for this entity on its profile.

A comprehensive Return on Invested Capital (ROIC) calculation is not possible with the provided data, as invested capital requires more granular detail. However, Return on Equity (ROE) has significantly improved due to the swing to profitability. This improvement suggests management is effectively utilizing equity to generate returns; however, we need a more comprehensive view of the capital structure to be certain.

A comprehensive Return on Invested Capital (ROIC) calculation is not possible with the provided data, as invested capital requires more granular detail. However, Return on Equity (ROE) has significantly improved due to the swing to profitability. This improvement suggests management is effectively utilizing equity to generate returns; however, we need a more comprehensive view of the capital structure to be certain. The company's Free Cash Flow (FCF) has turned positive at $46.42 million in 2024, a major swing from negative FCF in previous years; it suggests a strong ability to generate cash after capital expenditures. The capital expenditure of -$9.245 million shows continued investment in property, plant, and equipment, supporting future growth. Improving FCF and positive operating cash flow indicates a strong turnaround in the business's ability to generate cash from its operations and investments.

The company's Free Cash Flow (FCF) has turned positive at $46.42 million in 2024, a major swing from negative FCF in previous years; it suggests a strong ability to generate cash after capital expenditures. The capital expenditure of -$9.245 million shows continued investment in property, plant, and equipment, supporting future growth. Improving FCF and positive operating cash flow indicates a strong turnaround in the business's ability to generate cash from its operations and investments.