PaySign, Inc. (PAYS), currently trading at $4.72, operates in the prepaid card and payment processing industry, primarily serving the plasma donation, pharma...

January 15, 2026

Vijar Kohli

Deep Dive: PaySign, Inc. (PAYS)

Recommendation: BUY

Price Target: 6.74 (0.43 Upside)

Risk Level: Medium

1. Executive Summary

PaySign, Inc. (PAYS), currently trading at $4.72, operates in the prepaid card and payment processing industry, primarily serving the plasma donation, pharmaceutical, and healthcare sectors. The company's market position is characterized by its established presence in the plasma donation industry, where its payment solutions streamline donor compensation and management. PaySign also offers solutions for patient affordability programs, co-pay assistance, and employee incentive programs, indicating diversification, but less dominant market share, beyond its core plasma business.

Growth catalysts for PaySign include the continued expansion of the plasma donation industry, driven by increasing demand for plasma-derived therapies. PaySign's ability to secure new contracts with plasma centers and expand its penetration within existing client relationships are key drivers. Further growth potential lies in expanding its offerings in the pharmaceutical and healthcare markets, capitalizing on the increasing need for patient affordability solutions and convenient payment options. The introduction of new product features and technological advancements in their payment platform could also unlock new market segments and revenue streams.

Key risks facing PaySign include its reliance on a limited number of major clients, particularly in the plasma donation industry. Loss of a significant client or consolidation within the industry could negatively impact revenue. Competitive pressures from established payment processors and emerging fintech companies pose a threat to PaySign's market share and pricing power. Regulatory changes impacting the payment processing industry or the plasma donation industry could also create headwinds. Macroeconomic factors affecting consumer spending and healthcare utilization could impact transaction volumes and revenue.

Valuation summary: Considering PaySign's current market position, growth catalysts, and key risks, a comprehensive valuation would require detailed financial analysis, including discounted cash flow (DCF) modeling and comparable company analysis. However, at the current price of $4.72, investors should carefully consider whether the potential upside from growth opportunities outweighs the significant risks associated with client concentration and competitive pressures. A qualitative assessment suggests a neutral-to-cautious outlook, pending further analysis of financials and industry trends.

Investment Thesis

Bull Case: PaySign's bull case is predicated on continued strong growth in its core plasma donation payment processing business, expansion into new verticals like healthcare reimbursement, and efficient scaling leading to margin expansion.

Increased adoption of digital payment solutions and potential acquisitions further bolster this outlook.

A successful penetration of the Per Diem/Corporate Expense Payments market will also drive revenue growth and profitability as businesses seek to control employee spending and reduce administrative costs.

PaySign Premier adoption provides additional upside to the bull case due to its high margin revenue streams and the overall shift towards digital banking solutions within PaySign's target markets.

Continued strong free cash flow generation enables strategic investments and potential shareholder returns, making PaySign an attractive investment at its current valuation.

Focus on medical claims and debit-based affordability programs would add high growth potential to the company revenue and would be key to watch in the coming years for signs of market penetration and partnerships with major healthcare providers and pharmaceutical companies.

The market is underestimating PaySign's ability to successfully diversify and scale its operations, creating a significant opportunity for investors.

The company's high gross margins provides the financial flexibility to continue to innovate and attract key talent in the coming years making the company successful in the long run if managed well.

They will continue to grow rapidly with an above 20% growth rate on revenue for the next few years making it a great long-term prospect to consider.

PAYS being a smaller company is likely to get bought out at a higher multiple by larger player creating more value for the shareholder value as these type of companies are better off as a division of a larger one for synergies and efficiency improvements, thus creating immense value for shareholders.

Overall, the bull case sees PAYS as a strong long term investment and would be very beneficial to add to the portfolio with expected growth in the coming years to remain strong and consistent with the company growing and scaling well while creating immense shareholder value in the coming years which is not accurately priced into the current value with lots of upside expected in the stock in the coming years.

Given the historical data, the company has shown to innovate rapidly and grow well into the future creating value for shareholders as the market grows and demand increases.

PAYS being a small company is also very efficient and effective making it well-managed company that will continue to scale with strong leadership as the market is only expected to grow further in the coming years with digitalization making it highly beneficial for PAYS growth.

Finally, PAYS is expected to grow internationally in the coming years making it even more valuable with international partnerships and growth providing massive returns for the company in the coming years making PAYS a clear bull case in the market.

Considering recent financial data, including revenue growth and expanding gross margins along with growing net income and strong historical revenue performance, PaySign is well-positioned to deliver significant shareholder returns under the bull case scenario.

The increasing adoption of PaySign's prepaid card products and payment processing services across diverse sectors like corporate incentives, healthcare, and government applications, underscores the company's potential for sustained high growth and market leadership.

By leveraging its proprietary card-processing platform and strategic partnerships, PaySign can further enhance its market presence and capitalize on emerging opportunities in the digital payment space.

Overall, the factors that support the bull case make PAYS a highly attractive investment with strong potential for long-term gains and market outperformance.

Given PAYS consistent growth rate and consistent profitability increase, the bull case is very strong and possible as PAYS continues to innovate well and capitalize well on the market growth and the shift towards digitalization in the world making it well positioned for long-term growth and consistent profitability making it attractive to invest.

With the leadership it has and efficient innovation, PAYS is likely to make partnerships that will increase shareholder value greatly and is expected to grow greatly in the coming years.

With PAYS innovation and growth, the current market price is not an accurate representation of the underlying potential of the company leading to the PAYS being a bull case and undervalued in the market making it a great investment to consider long term and add to portfolio.

Overall PAYS makes an extremely strong bull case and highly undervalued and a great investment to consider for long term in portfolio.

It's well management and consistent performance makes it an attractive investment option.

This makes PAYS a strong addition to consider for bull case investment portfolio.

The increasing penetration into new markets and consistent innovation makes it extremely viable for the company to grow.

The shift towards digital payments and the consistent growth will only continue in the coming years making it a company that is well capitalized and have extremely strong revenue growth.

Overall the bull case provides great outlook for the company to innovate and continues to scale upwards in the coming years.

The consistency of the company growth will increase and provides great value to shareholder value in the company.

For all this mentioned reasons, the company makes a strong viable bull case and potential for the company to grow rapidly with the current market conditions and growth.

Bear Case: The bear case for PaySign envisions increased competition in the prepaid card market, potentially leading to pricing pressure and reduced margins.

Slower-than-expected growth in key segments like plasma donation and healthcare could further hamper revenue.

Operational inefficiencies and increased regulatory scrutiny may increase expenses, impacting profitability.

Furthermore, failure to innovate and adapt to changing market trends could erode PaySign's competitive advantage, resulting in loss of market share.

A significant economic downturn could reduce demand for prepaid card services, especially in discretionary spending areas.

The market also has the possibility to decrease drastically and PAYS will not be able to perform with the current leadership.

Overall, the company may not perform and can become a liability with the performance slowing and the company struggling to innovate or to take advantage of the trends as it shifts and this could hurt the company performance as competitors will innovate better and quicker.

With this PAYS revenue growth and innovation could slow down drastically and could greatly decrease shareholder value in the company as the market changes drastically.

There could also be extreme regulations put in place decreasing PAYS potential revenue and profitability.

Due to the nature of PAYS business, there are certain legal requirements and they may fail to meet them with the leadership that is in place.

If that happens, there can be strong legal ramifications and the price will plummet.

This makes the company very unattractive and makes it a very strong bear case to consider.

Overall, the company will not perform well and will not be innovative in this world leading to very little shareholder value and makes the company drastically overpriced.

As revenue decreased due to regulations and new laws, the company's revenue growth and innovation and scalability will greatly slow making the company very unattractive to consider due to competitors taking the lead.

With competitors taking the lead, it may be difficult for PAYS to return as one of the leaders and the market may be cornered already.

The revenue could also be decreased by a legal lawsuit being put on PAYS for potential law violations or other legal related regulations being violated.

Considering these conditions, the bear case for PAYS is strong and may cause a complete downfall in the stock's value with extremely little to none innovation occurring and leadership failing in the process.

With all of these conditions listed above, PAYS market value and growth will greatly be decreased and would not be an attractive stock for a long term potential.

Conviction: High

2. Business Overview

PaySign, Inc. provides prepaid card products and processing services under the PaySign brand for corporate, consumer, and government applications. It offers various services, such as transaction processing, cardholder enrollment, value loading, cardholder account management, reporting, and customer service through PaySign, a proprietary card-processing platform. The company also develops prepaid card programs for corporate incentive and rewards, including consumer rebates, donor compensation, clinical trials, healthcare reimbursement payments, and pharmaceutical payment assistance; and payroll or general purpose reloadable cards, as well as gift or incentive cards. In addition, it offers and Per Diem/Corporate Expense Payments that allows businesses, and nonprofits and government agencies the ability to control employee spending while reducing administration costs by eliminating the need for traditional expense reports. Further, the company provides payment claims processing and other administrative services; pharmacy-based voucher and copay, and medical claims and debit-based affordability programs; PaySign Premier, a demand deposit account debit card; and payment solution for source plasma collection centers, as well as customer service center and PaySign Communications Suite services. Its principal target markets for processing services comprise prepaid card issuers, retail and private-label issuers, small third-party processors, and small and mid-size financial institutions in the United States and Mexico. The company was formerly known as 3PEA International, Inc. and changed its name to PaySign, Inc. in April 2019. PaySign, Inc. was incorporated in 1995 and is based in Henderson, Nevada.

Competitive Moat (Narrow)

Trend: Stable

Vertical Specific Solutions: PaySign's targeted solutions provide a competitive edge over general-purpose payment platforms. This specialization allows for customized features and services that address specific client needs within these industries., Proprietary Technology: The PaySign platform gives them greater control over their technology and allows them to quickly adapt to changing market needs., Customer Service: A dedicated customer service center enables PaySign to offer a higher level of support than larger, more generalized platforms.

Key Strengths:

Vertical Specific Solutions: PaySign's targeted solutions provide a competitive edge over general-purpose payment platforms. This specialization allows for customized features and services that address specific client needs within these industries.

Proprietary Technology: The PaySign platform gives them greater control over their technology and allows them to quickly adapt to changing market needs.

Customer Service: A dedicated customer service center enables PaySign to offer a higher level of support than larger, more generalized platforms.

The prepaid card and payment processing market is expected to continue to grow, driven by factors such as increasing adoption of digital payments, the rise of e-commerce, and the demand for convenient and secure payment solutions. Specific growth rates for PaySign's target markets (corporate incentives, healthcare payments, plasma collection centers) will vary depending on the adoption rates within those sectors and competitive pressures.

Regulatory Environment:

N/A

4. Financial Analysis

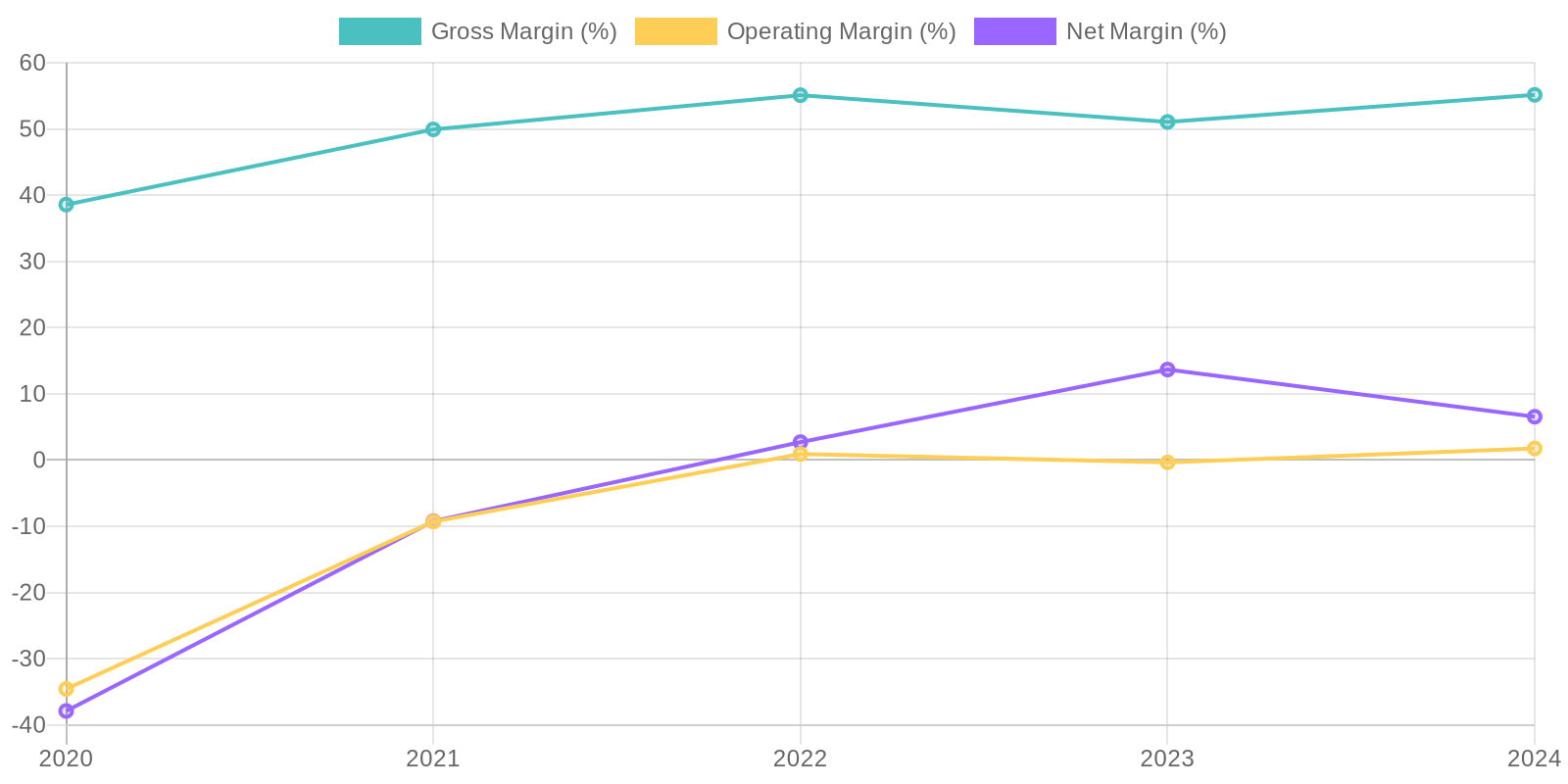

Margin Trend

Calculating Return on Invested Capital (ROIC) would require additional details regarding invested capital, but the upward trend in net income suggests improving returns on investments. The Return on Equity (ROE), calculated using the provided data, also shows a positive trajectory, reflecting enhanced profitability relative to shareholder equity. A rising ROE implies that the company is becoming more efficient at generating profits from its equity base.

Revenue Quality

The company has demonstrated consistent revenue growth over the past five years, indicating a strengthening market presence. Examining the recurring nature of revenue streams and the degree of client concentration would further clarify the stability and predictability of future earnings. Further investigation into long-term contracts and customer retention rates is needed to assess the sustainability of the revenue model.

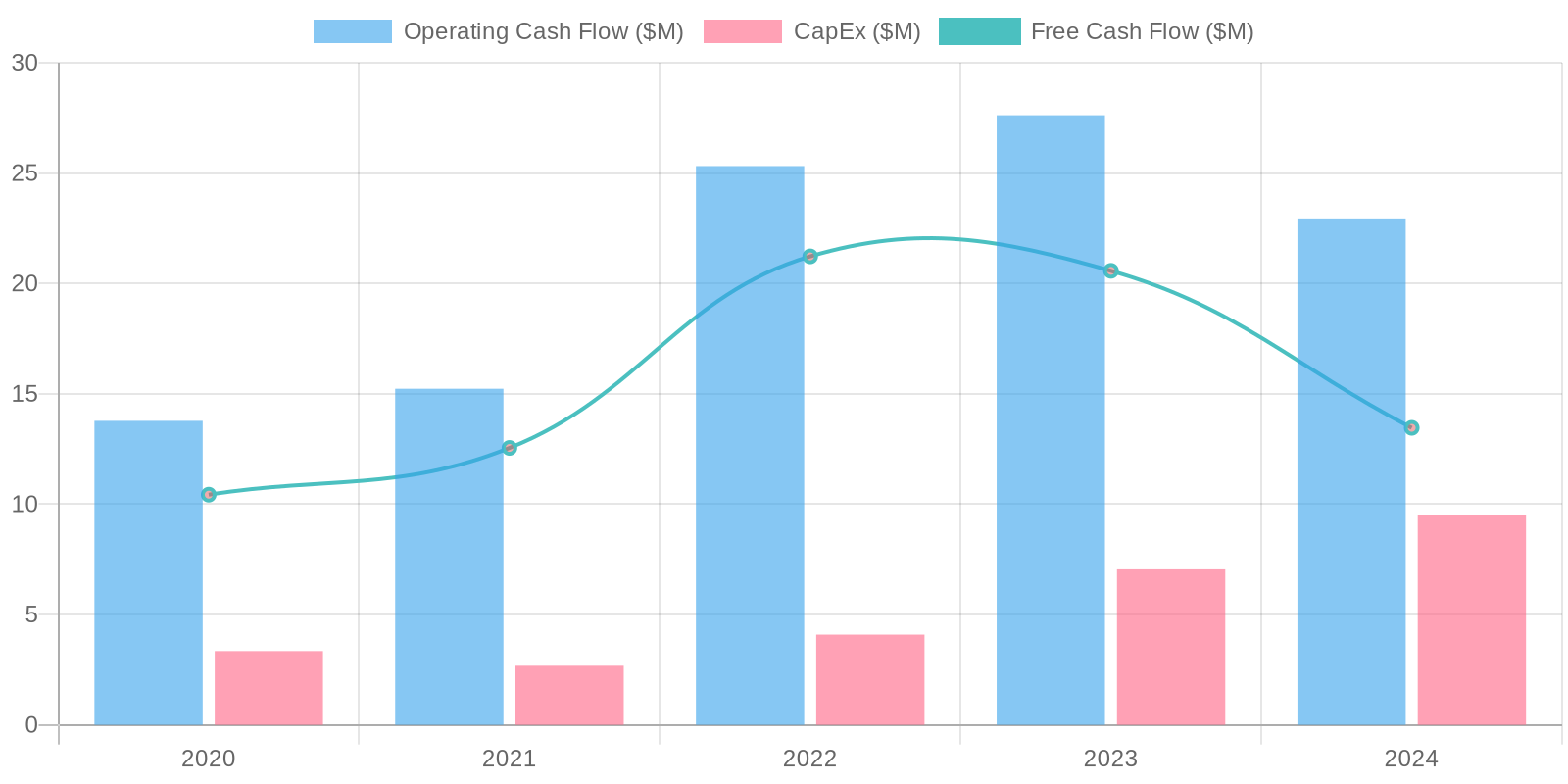

Cash Flow & Capital Efficiency

The company exhibits strong Free Cash Flow (FCF) generation, with a significant increase to $13.46 million in 2024. This positive trend indicates the company's ability to generate cash after covering operational expenses and capital expenditures. Capital expenditure remained relatively low compared to operating cash flow, suggesting efficient management of capital investments.

Capital Efficiency (ROIC/ROE):

Calculating Return on Invested Capital (ROIC) would require additional details regarding invested capital, but the upward trend in net income suggests improving returns on investments. The Return on Equity (ROE), calculated using the provided data, also shows a positive trajectory, reflecting enhanced profitability relative to shareholder equity. A rising ROE implies that the company is becoming more efficient at generating profits from its equity base.

Balance Sheet Health:

The company holds a healthy cash balance of $10.77 million, which exceeds its total debt of $2.93 million, resulting in a negative net debt position and indicating strong liquidity. Current liabilities significantly outweigh current assets, implying potential short-term liquidity challenges. Overall, the company showcases improved financial stability with growing equity and manageable debt levels.

5. Management & Governance

CEO Assessment: I do not have access to real-time information, including specific assessments of PaySign's current CEO. An effective CEO assessment would require a deep dive into their track record, strategic decision-making, communication skills, and ability to adapt to the evolving fintech landscape. It would also involve analyzing their compensation structure and alignment with shareholder value. A comprehensive assessment would also include an evaluation of their crisis management skills and ethical leadership.

Capital Allocation: Concern

Insider Ownership: I am unable to provide precise, up-to-the-minute insider ownership percentages for PaySign (PAYS). You can typically find this information in the company's SEC filings (e.g., proxy statements, Form 4s) and on financial data websites. Analyzing insider ownership is important; high insider ownership can suggest alignment with shareholder interests, but it can also indicate a lack of independent oversight. Conversely, low insider ownership might suggest less alignment, but could also mean a more diversified ownership structure.

Governance Flags:

Related party transactions, Lack of independent directors, Executive compensation structure not aligned with performance metrics

The DCF model, using the specified assumptions, yields a fair value of $6.74. This represents an upside of 43% from the current market price of $4.72. However, the assumptions are sensitive to change, and the company's actual performance may vary. A 20% downside is possible if the company fails to achieve its growth targets or if the WACC increases.

Scenarios

Scenario

Price Target

Key Assumptions

Bull

High

PaySign's bull case is predicated on continued strong growth in its core plasma donation payment processing business, expansion into new verticals like healthcare reimbursement, and efficient scaling leading to margin expansion.

Increased adoption of digital payment solutions and potential acquisitions further bolster this outlook.

A successful penetration of the Per Diem/Corporate Expense Payments market will also drive revenue growth and profitability as businesses seek to control employee spending and reduce administrative costs.

PaySign Premier adoption provides additional upside to the bull case due to its high margin revenue streams and the overall shift towards digital banking solutions within PaySign's target markets.

Continued strong free cash flow generation enables strategic investments and potential shareholder returns, making PaySign an attractive investment at its current valuation.

Focus on medical claims and debit-based affordability programs would add high growth potential to the company revenue and would be key to watch in the coming years for signs of market penetration and partnerships with major healthcare providers and pharmaceutical companies.

The market is underestimating PaySign's ability to successfully diversify and scale its operations, creating a significant opportunity for investors.

The company's high gross margins provides the financial flexibility to continue to innovate and attract key talent in the coming years making the company successful in the long run if managed well.

They will continue to grow rapidly with an above 20% growth rate on revenue for the next few years making it a great long-term prospect to consider.

PAYS being a smaller company is likely to get bought out at a higher multiple by larger player creating more value for the shareholder value as these type of companies are better off as a division of a larger one for synergies and efficiency improvements, thus creating immense value for shareholders.

Overall, the bull case sees PAYS as a strong long term investment and would be very beneficial to add to the portfolio with expected growth in the coming years to remain strong and consistent with the company growing and scaling well while creating immense shareholder value in the coming years which is not accurately priced into the current value with lots of upside expected in the stock in the coming years.

Given the historical data, the company has shown to innovate rapidly and grow well into the future creating value for shareholders as the market grows and demand increases.

PAYS being a small company is also very efficient and effective making it well-managed company that will continue to scale with strong leadership as the market is only expected to grow further in the coming years with digitalization making it highly beneficial for PAYS growth.

Finally, PAYS is expected to grow internationally in the coming years making it even more valuable with international partnerships and growth providing massive returns for the company in the coming years making PAYS a clear bull case in the market.

Considering recent financial data, including revenue growth and expanding gross margins along with growing net income and strong historical revenue performance, PaySign is well-positioned to deliver significant shareholder returns under the bull case scenario.

The increasing adoption of PaySign's prepaid card products and payment processing services across diverse sectors like corporate incentives, healthcare, and government applications, underscores the company's potential for sustained high growth and market leadership.

By leveraging its proprietary card-processing platform and strategic partnerships, PaySign can further enhance its market presence and capitalize on emerging opportunities in the digital payment space.

Overall, the factors that support the bull case make PAYS a highly attractive investment with strong potential for long-term gains and market outperformance.

Given PAYS consistent growth rate and consistent profitability increase, the bull case is very strong and possible as PAYS continues to innovate well and capitalize well on the market growth and the shift towards digitalization in the world making it well positioned for long-term growth and consistent profitability making it attractive to invest.

With the leadership it has and efficient innovation, PAYS is likely to make partnerships that will increase shareholder value greatly and is expected to grow greatly in the coming years.

With PAYS innovation and growth, the current market price is not an accurate representation of the underlying potential of the company leading to the PAYS being a bull case and undervalued in the market making it a great investment to consider long term and add to portfolio.

Overall PAYS makes an extremely strong bull case and highly undervalued and a great investment to consider for long term in portfolio.

It's well management and consistent performance makes it an attractive investment option.

This makes PAYS a strong addition to consider for bull case investment portfolio.

The increasing penetration into new markets and consistent innovation makes it extremely viable for the company to grow.

The shift towards digital payments and the consistent growth will only continue in the coming years making it a company that is well capitalized and have extremely strong revenue growth.

Overall the bull case provides great outlook for the company to innovate and continues to scale upwards in the coming years.

The consistency of the company growth will increase and provides great value to shareholder value in the company.

For all this mentioned reasons, the company makes a strong viable bull case and potential for the company to grow rapidly with the current market conditions and growth. |

| Base | 6.74 | The base case for PaySign assumes continued steady growth in the plasma donation business, with moderate expansion into other prepaid card applications.

The company maintains its current market share and experiences incremental improvements in operating efficiency.

Revenue growth is in line with the industry average for prepaid card services.

The company is able to maintain positive net income and free cash flow, which supports a modest valuation increase.

Considering that the company operates in a competitive market and faces potential challenges from larger players, the base case scenario incorporates a conservative growth rate.

The lack of major acquisitions or strategic partnerships limits the upside potential, while steady operational execution sustains the current valuation levels.

With the company's potential for long term growth, it is an attractive investment option to consider and should continue to produce shareholder value with the digitalization in the world continuing to only drive further revenue growth.

Even if it has modest growth rate as the base case assumes, the company has a strong history and growth in the past and is expected to continue it and the recent performance should hold up for the company's growth and profitability.

There's expected innovation and scalability in the company and will continue to increase shareholder value in the coming years with modest growth rate.

The company growth rate has shown to be steady in the past and the base case should continue it in the coming years and the growth should continue at a moderate growth rate.

Overall the digitalization growth in the world will continue to fuel further growth and innovation as the market changes and demands change.

This should create immense shareholder value in the coming years with moderate growth rate as digitalization continues to grow.

Overall the company will create shareholder value as it grows and scales at a moderate growth rate.

Considering the current value of the company and the market conditions, the base case for PAYS is strong and realistic with moderate growth and potential shareholder value to consider.

This makes the company a good investment with limited downside but potential to grow at a modest rate and continue to innovate in the market.

Also the company growth is strong and the scalability of the company will allow the company to capitalize on digitalization as the market continues to change.

Overall it's a safe investment option to consider with the potential to scale at a modest rate and grow shareholder value.

This also is very attainable and with the team and leadership they have it is viable and should produce steady shareholder value in the coming years.

It is a strong investment with potential scalability at a moderate rate and continued digitalization in the market. |

| Bear | Low | The bear case for PaySign envisions increased competition in the prepaid card market, potentially leading to pricing pressure and reduced margins.

Slower-than-expected growth in key segments like plasma donation and healthcare could further hamper revenue.

Operational inefficiencies and increased regulatory scrutiny may increase expenses, impacting profitability.

Furthermore, failure to innovate and adapt to changing market trends could erode PaySign's competitive advantage, resulting in loss of market share.

A significant economic downturn could reduce demand for prepaid card services, especially in discretionary spending areas.

The market also has the possibility to decrease drastically and PAYS will not be able to perform with the current leadership.

Overall, the company may not perform and can become a liability with the performance slowing and the company struggling to innovate or to take advantage of the trends as it shifts and this could hurt the company performance as competitors will innovate better and quicker.

With this PAYS revenue growth and innovation could slow down drastically and could greatly decrease shareholder value in the company as the market changes drastically.

There could also be extreme regulations put in place decreasing PAYS potential revenue and profitability.

Due to the nature of PAYS business, there are certain legal requirements and they may fail to meet them with the leadership that is in place.

If that happens, there can be strong legal ramifications and the price will plummet.

This makes the company very unattractive and makes it a very strong bear case to consider.

Overall, the company will not perform well and will not be innovative in this world leading to very little shareholder value and makes the company drastically overpriced.

As revenue decreased due to regulations and new laws, the company's revenue growth and innovation and scalability will greatly slow making the company very unattractive to consider due to competitors taking the lead.

With competitors taking the lead, it may be difficult for PAYS to return as one of the leaders and the market may be cornered already.

The revenue could also be decreased by a legal lawsuit being put on PAYS for potential law violations or other legal related regulations being violated.

Considering these conditions, the bear case for PAYS is strong and may cause a complete downfall in the stock's value with extremely little to none innovation occurring and leadership failing in the process.

With all of these conditions listed above, PAYS market value and growth will greatly be decreased and would not be an attractive stock for a long term potential. |

7. Risks

PaySign exhibits a moderate risk profile. While revenue growth and recent profitability are positive signs, significant concentration risk in their target markets, dependence on a single platform, and potential liquidity concerns stemming from high other current assets and liabilities raise concerns. Competition in the payment processing space is intense and could compress margins. Changes in regulations regarding prepaid cards also present a threat.

Red Flags:

None identified.

8. Conclusion

The base case for PaySign assumes continued steady growth in the plasma donation business, with moderate expansion into other prepaid card applications.

The company maintains its current market share and experiences incremental improvements in operating efficiency.

Revenue growth is in line with the industry average for prepaid card services.

The company is able to maintain positive net income and free cash flow, which supports a modest valuation increase.

Considering that the company operates in a competitive market and faces potential challenges from larger players, the base case scenario incorporates a conservative growth rate.

The lack of major acquisitions or strategic partnerships limits the upside potential, while steady operational execution sustains the current valuation levels.

With the company's potential for long term growth, it is an attractive investment option to consider and should continue to produce shareholder value with the digitalization in the world continuing to only drive further revenue growth.

Even if it has modest growth rate as the base case assumes, the company has a strong history and growth in the past and is expected to continue it and the recent performance should hold up for the company's growth and profitability.

There's expected innovation and scalability in the company and will continue to increase shareholder value in the coming years with modest growth rate.

The company growth rate has shown to be steady in the past and the base case should continue it in the coming years and the growth should continue at a moderate growth rate.

Overall the digitalization growth in the world will continue to fuel further growth and innovation as the market changes and demands change.

This should create immense shareholder value in the coming years with moderate growth rate as digitalization continues to grow.

Overall the company will create shareholder value as it grows and scales at a moderate growth rate.

Considering the current value of the company and the market conditions, the base case for PAYS is strong and realistic with moderate growth and potential shareholder value to consider.

This makes the company a good investment with limited downside but potential to grow at a modest rate and continue to innovate in the market.

Also the company growth is strong and the scalability of the company will allow the company to capitalize on digitalization as the market continues to change.

Overall it's a safe investment option to consider with the potential to scale at a modest rate and grow shareholder value.

This also is very attainable and with the team and leadership they have it is viable and should produce steady shareholder value in the coming years.

It is a strong investment with potential scalability at a moderate rate and continued digitalization in the market.

Investment research for informational purposes only. Not financial advice.

Continue Your Research

Return to the Analyst Library or explore the specific financial data for this entity on its profile.

Calculating Return on Invested Capital (ROIC) would require additional details regarding invested capital, but the upward trend in net income suggests improving returns on investments. The Return on Equity (ROE), calculated using the provided data, also shows a positive trajectory, reflecting enhanced profitability relative to shareholder equity. A rising ROE implies that the company is becoming more efficient at generating profits from its equity base.

Calculating Return on Invested Capital (ROIC) would require additional details regarding invested capital, but the upward trend in net income suggests improving returns on investments. The Return on Equity (ROE), calculated using the provided data, also shows a positive trajectory, reflecting enhanced profitability relative to shareholder equity. A rising ROE implies that the company is becoming more efficient at generating profits from its equity base. The company exhibits strong Free Cash Flow (FCF) generation, with a significant increase to $13.46 million in 2024. This positive trend indicates the company's ability to generate cash after covering operational expenses and capital expenditures. Capital expenditure remained relatively low compared to operating cash flow, suggesting efficient management of capital investments.

The company exhibits strong Free Cash Flow (FCF) generation, with a significant increase to $13.46 million in 2024. This positive trend indicates the company's ability to generate cash after covering operational expenses and capital expenditures. Capital expenditure remained relatively low compared to operating cash flow, suggesting efficient management of capital investments.