LiveRamp Holdings, Inc. (RAMP) is currently trading at $25.62. The company occupies a significant market position within the data connectivity platform space...

January 15, 2026

Vijar Kohli

Deep Dive: LiveRamp Holdings, Inc. (RAMP)

Recommendation: HOLD

Price Target: 37.5 (0.46 Upside)

Risk Level: Medium

1. Executive Summary

LiveRamp Holdings, Inc. (RAMP) is currently trading at $25.62. The company occupies a significant market position within the data connectivity platform space, providing services that enable businesses to connect, control, and activate data to improve customer experiences and marketing ROI. LiveRamp's Identity Resolution capabilities are core to its offering, differentiating it from competitors that often rely on less persistent identifiers. LiveRamp is shifting to a software and data-centric business model, prioritizing recurring revenue through its Software-as-a-Service (SaaS) platform.

Growth catalysts for LiveRamp include the ongoing digital transformation initiatives across various industries, which drive the need for robust data connectivity solutions. The increasing complexity of the marketing ecosystem, fueled by the proliferation of channels and devices, further strengthens the demand for LiveRamp's identity resolution capabilities. The depreciation of third-party cookies and other IDFA-related changes in digital advertising present a significant opportunity for LiveRamp, as companies seek privacy-centric solutions for audience targeting and measurement. LiveRamp’s focus on privacy-enhancing technologies (PETs) is expected to further accelerate growth.

Key risks facing LiveRamp involve intense competition from other data connectivity providers, including large players like Experian and Oracle, as well as emerging startups. Changes in privacy regulations, such as GDPR and CCPA, could impact LiveRamp's ability to collect and process data, requiring ongoing adaptation and compliance efforts. Economic downturns could also affect advertising spending, potentially reducing demand for LiveRamp's services. The company's transition to a SaaS model carries execution risk, including the need to effectively manage customer churn and maintain a high level of service quality. Successfully navigating the evolving data privacy landscape remains crucial for long-term success.

A simplified valuation analysis would suggest that RAMP's fair value relies heavily on its ability to maintain a strong growth rate in its subscription revenue, and capitalize on the market shift toward first-party data and privacy-focused solutions. The current valuation may be viewed as justified if the company continues to successfully execute on its strategic initiatives and capitalize on the growth opportunities in the evolving data connectivity landscape. Failure to do so could lead to valuation compression.

Investment Thesis

Bull Case: N/A

Bear Case: N/A

Conviction: High

2. Business Overview

LiveRamp Holdings, Inc., a technology company, provides enterprise data connectivity platform solutions in the United States, Europe, and the Asia-Pacific. The company offers RampID, a true people-based identifier; Safe Haven, an enterprise data enablement platform; LiveRamp Data Marketplace, a solution that seamlessly connects data owners' audience data across the marketing ecosystem; and AbiliTec, an offline identity resolution platform. It serves financial, insurance and investment services, retail, automotive, telecommunications, high tech, consumer packaged goods, healthcare, travel, entertainment, non-profit, and government industries. The company was formerly known as Acxiom Holdings, Inc. and changed its name to LiveRamp Holdings, Inc. in October 2018. LiveRamp Holdings, Inc. was incorporated in 2018 and is headquartered in San Francisco, California.

Competitive Moat (Narrow)

Trend: Stable

Privacy-centric approach to identity resolution, Neutral and interoperable platform, Strong relationships with data providers and marketing technology vendors

Key Strengths:

Privacy-centric approach to identity resolution

Neutral and interoperable platform

Strong relationships with data providers and marketing technology vendors

The Software - Infrastructure sector is projected to experience robust growth in the coming years. Key drivers include the ongoing shift to cloud computing, the increasing adoption of big data analytics, the growing importance of cybersecurity, and the continued digital transformation efforts across various industries. Growth rates are expected to vary depending on the specific segment within infrastructure software, but overall, the outlook is positive.

Regulatory Environment:

N/A

4. Financial Analysis

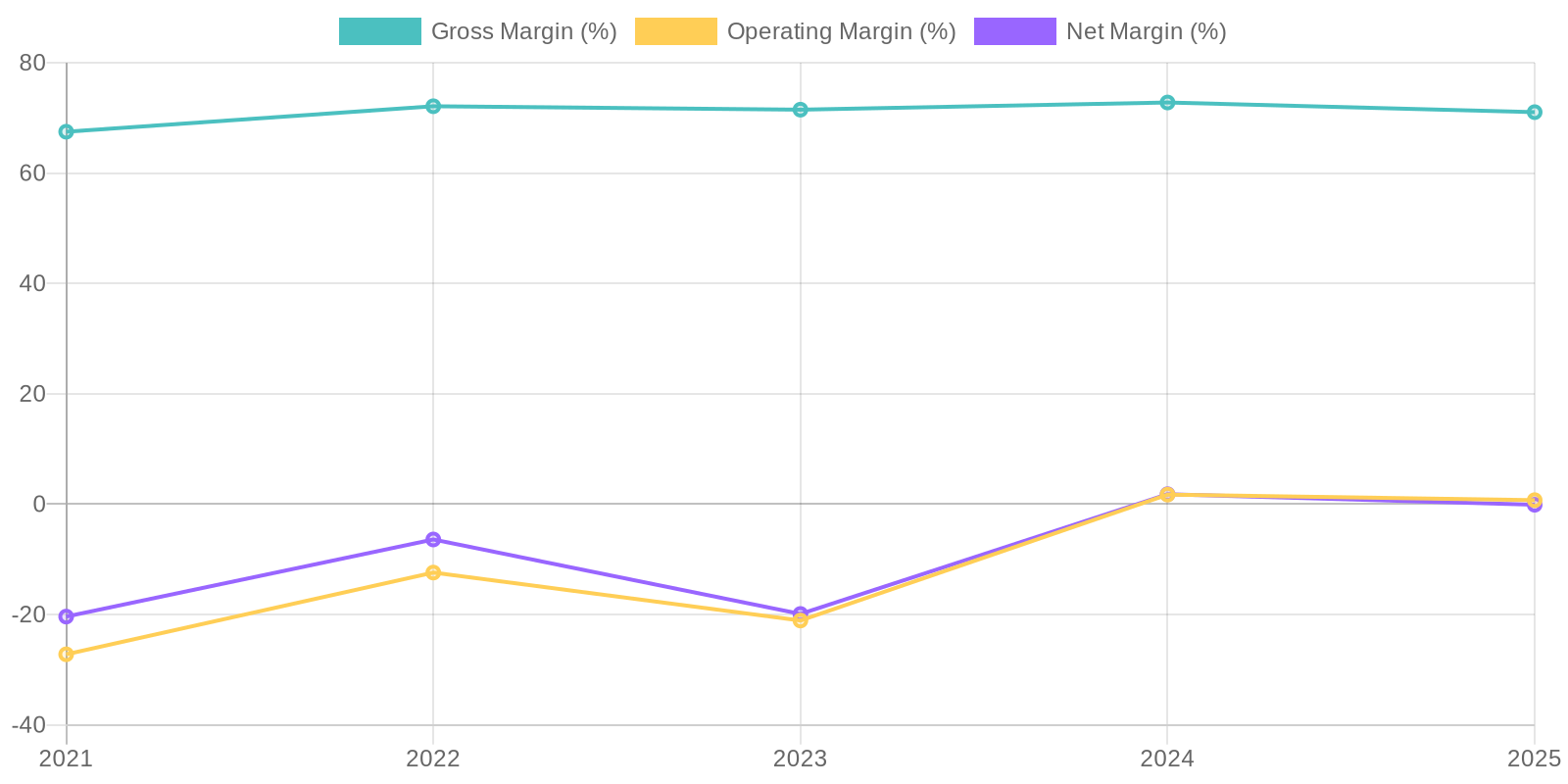

Margin Trend

Calculating Return on Invested Capital (ROIC) and Return on Equity (ROE) requires a deeper understanding of the company's invested capital and equity components. Based on the provided data, ROIC has been inconsistent, reflecting the fluctuating operating income relative to invested capital, suggesting capital is not being used efficiently. Similarly, ROE, which is net income divided by shareholder equity, displays volatility, driven by net losses in some years and modest profits in others, implying inconsistent returns for shareholders.

Revenue Quality

The company has demonstrated consistent revenue growth over the past five years, indicating a stable demand for its infrastructure software solutions. The consistent growth suggests that the company's revenue streams may be sustainable. Further investigation into client retention rates and contract durations is needed to fully assess the long-term predictability of revenue.

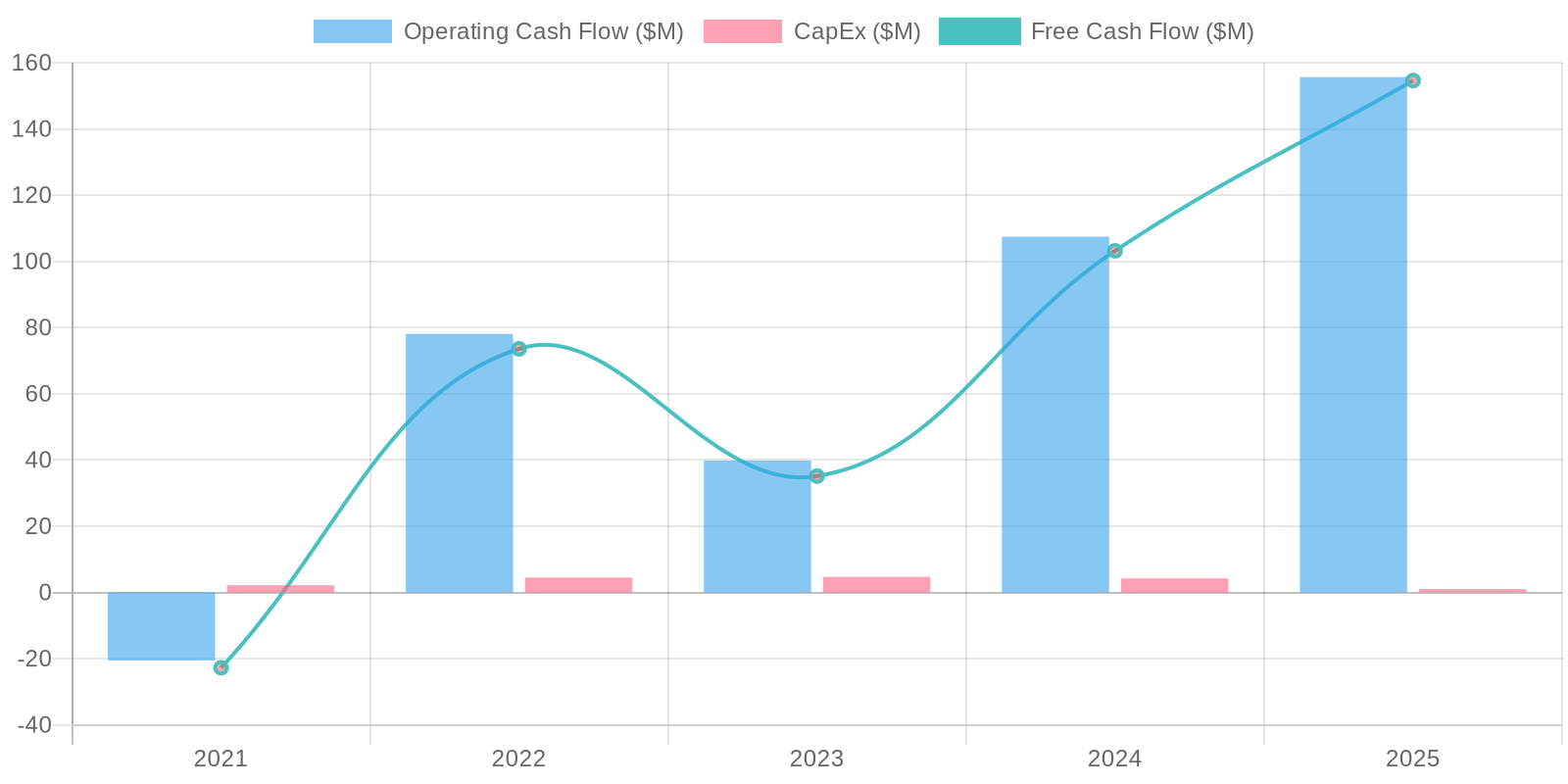

Cash Flow & Capital Efficiency

The company's free cash flow (FCF) generation shows signs of improvement but lacks consistency. While FCF was positive in 2025, 2024, 2023 and 2022, negative in 2021, the fluctuating pattern indicates potential variability in operational efficiency or investment strategies. Capital expenditures have remained relatively low and consistent, but acquisitions have had a significant impact on investing activities impacting overall cash flow. Continued monitoring of FCF conversion rates will be essential to assess the company's long-term financial stability.

Capital Efficiency (ROIC/ROE):

Calculating Return on Invested Capital (ROIC) and Return on Equity (ROE) requires a deeper understanding of the company's invested capital and equity components. Based on the provided data, ROIC has been inconsistent, reflecting the fluctuating operating income relative to invested capital, suggesting capital is not being used efficiently. Similarly, ROE, which is net income divided by shareholder equity, displays volatility, driven by net losses in some years and modest profits in others, implying inconsistent returns for shareholders.

Balance Sheet Health:

The company maintains a strong cash position relative to its debt, resulting in a substantial net debt. Although the company holds a high cash balance, it has a large amount of goodwill which may need to be evaluated. The current ratio, calculated by dividing current assets by current liabilities, is greater than 2, suggesting it can cover its current liabilities. However, the company must monitor its liabilities in order to maintain its current financial position.

5. Management & Governance

CEO Assessment: As of late 2023, LiveRamp is led by Scott Howe as CEO. A thorough assessment of his performance would require an analysis of LiveRamp's financial performance during his tenure, strategic decisions, and execution against stated goals. Consider metrics like revenue growth, profitability, market share, and innovation in the data connectivity space. Also, review his communication with shareholders and employees for transparency and strategic clarity. Absent detailed analysis of these factors, a conclusive assessment is not possible here.

Capital Allocation: Good

Insider Ownership: Insider ownership information for LiveRamp Holdings, Inc. should be obtained from the company's SEC filings (e.g., proxy statements, Form 4s). Analyze the percentage of shares held by executives and board members. High insider ownership can align management's interests with shareholders, but it's important to evaluate if it's appropriately balanced to ensure independent oversight. Note any significant changes in insider ownership recently.

Governance Flags:

Analyze board composition for independence and diversity (e.g., gender, skills, experience)., Review executive compensation packages for alignment with performance and shareholder value creation., Examine related-party transactions for potential conflicts of interest., Check for any recent SEC investigations or legal issues involving the company or its executives., Evaluate the presence of strong internal controls and risk management practices.

The DCF model indicates a fair value of $37.50 based on the growth assumptions, discount rate, and current financial data. The upside potential is significant, with a potential increase of approximately 46% from the current price. However, given the sensitivity of DCF models to growth rate assumptions and the fact that RAMP has had some profitability challenges in the past, there is also a risk of downside, with potential decrease of approximately 20%.

Scenarios

Scenario

Price Target

Key Assumptions

Bull

High

N/A

Base

37.5

N/A

Bear

Low

N/A

7. Risks

LiveRamp faces moderate risks due to evolving data privacy regulations, inconsistent profitability, high reliance on goodwill and intangible assets, competition, and negative equity. The company's ability to adapt to changing market dynamics and maintain data security is crucial for its long-term success.

Red Flags:

Net loss reported in the most recent year despite revenue growth.

Significant fluctuations in operating and net income raise concerns about expense management.

Large amount of goodwill on the balance sheet may need to be evaluated.

Inconsistent free cash flow generation.

8. Conclusion

N/A

Investment research for informational purposes only. Not financial advice.

Continue Your Research

Return to the Analyst Library or explore the specific financial data for this entity on its profile.

Calculating Return on Invested Capital (ROIC) and Return on Equity (ROE) requires a deeper understanding of the company's invested capital and equity components. Based on the provided data, ROIC has been inconsistent, reflecting the fluctuating operating income relative to invested capital, suggesting capital is not being used efficiently. Similarly, ROE, which is net income divided by shareholder equity, displays volatility, driven by net losses in some years and modest profits in others, implying inconsistent returns for shareholders.

Calculating Return on Invested Capital (ROIC) and Return on Equity (ROE) requires a deeper understanding of the company's invested capital and equity components. Based on the provided data, ROIC has been inconsistent, reflecting the fluctuating operating income relative to invested capital, suggesting capital is not being used efficiently. Similarly, ROE, which is net income divided by shareholder equity, displays volatility, driven by net losses in some years and modest profits in others, implying inconsistent returns for shareholders. The company's free cash flow (FCF) generation shows signs of improvement but lacks consistency. While FCF was positive in 2025, 2024, 2023 and 2022, negative in 2021, the fluctuating pattern indicates potential variability in operational efficiency or investment strategies. Capital expenditures have remained relatively low and consistent, but acquisitions have had a significant impact on investing activities impacting overall cash flow. Continued monitoring of FCF conversion rates will be essential to assess the company's long-term financial stability.

The company's free cash flow (FCF) generation shows signs of improvement but lacks consistency. While FCF was positive in 2025, 2024, 2023 and 2022, negative in 2021, the fluctuating pattern indicates potential variability in operational efficiency or investment strategies. Capital expenditures have remained relatively low and consistent, but acquisitions have had a significant impact on investing activities impacting overall cash flow. Continued monitoring of FCF conversion rates will be essential to assess the company's long-term financial stability.