Rumble Inc. (RUM), currently trading at $6.04, operates as a video-sharing platform aiming to compete with established players like YouTube. Its market posit...

January 15, 2026

Vijar Kohli

Deep Dive: Rumble Inc. (RUM)

Recommendation: BUY

Price Target: 1.1 (-0.82 Upside)

Risk Level: Medium

1. Executive Summary

Rumble Inc. (RUM), currently trading at $6.04, operates as a video-sharing platform aiming to compete with established players like YouTube. Its market position is that of a challenger brand, focusing on attracting creators and users who value free speech and less restrictive content policies. While Rumble has achieved considerable growth in user base and engagement, it still lags significantly behind YouTube in terms of overall scale and revenue generation.

Growth catalysts for Rumble include its partnerships with prominent figures and organizations known for their conservative viewpoints, which drive user acquisition and content creation. The platform's appeal to users seeking uncensored content and alternative perspectives provides a unique selling proposition. Expansion into new content verticals, such as live streaming and podcasting, further diversifies its offerings and attracts a broader audience. Monetization improvements, including enhanced advertising capabilities and creator subscription models, are crucial for sustainable growth.

Key risks facing Rumble include its reliance on a specific ideological niche, which may limit its mainstream appeal and create challenges in attracting diverse advertisers. Content moderation complexities and potential reputational damage stemming from controversial content pose ongoing concerns. Competition from established video platforms with significantly larger resources and user bases presents a formidable challenge. Macroeconomic headwinds and potential shifts in user behavior also represent external risks to Rumble's growth trajectory.

Rumble's valuation is complex and subject to debate. Traditional valuation metrics may not fully capture the platform's potential due to its unique positioning and rapid growth phase. A valuation summary would likely incorporate a discounted cash flow (DCF) analysis based on projected user growth, monetization rates, and operating margins, compared against similar peer group valuations. However, it is important to note that a risk adjusted return on capital should be considered due to the competitive landscape, novel nature of the business, and reliance on certain key partnerships.

Investment Thesis

Bull Case: Rumble capitalizes on the growing demand for uncensored video platforms and live streaming, attracting creators and users seeking alternatives to mainstream social media.

Successful execution of monetization strategies and strategic partnerships will drive revenue growth and profitability, leading to significant stock appreciation.

Furthermore, a shift in cultural sentiment towards free speech absolutism will dramatically increase Rumble's user base and value, far surpassing current market expectations.

Rumble becomes synonymous with free speech on the internet, attracting major influencers and creating a self-sustaining ecosystem of content and users which will lead to substantial market dominance and premium valuation multiples far exceeding industry peers.

Their success in acquiring and retaining high-profile content creators and scaling their advertising infrastructure will cement its position as a leading video platform and a challenger to YouTube's dominance.

Improved operational efficiencies leads to profitability in the near term due to greater ad revnue generation per user, higher than previously anticipated subscription growth and new revenue streams arising from unexpected partnerships or content acquisitions.

They will achieve at least 500 Million monthly active users in the medium term, with revenue per user comparable to YouTube.

Successful navigation of regulatory scrutiny will also be crucial for long-term success, coupled with effective content moderation policies that maintain user trust and platform integrity.

The investment recommendation is a Strong Buy and the expected return to be 10x the current price.

Rumble's value should reflect its long term growth prospects as a leader in the free speech internet which are being unfairly discounted due to short term financial losses which will become a small fraction of overall revenue as the company scales.

The bull case sees them rapidly gain share and attain profitability faster than analysts predict and attain valuations more closely aligned with peers in the social media and content distribution space.

Rumble should become the go-to platform for a large number of content creators and users who seek to generate a living off the internet, and Rumble should take steps to ensure that this is possible which will attract more creators to the platform and grow the ecosystem.

The RumbleOne advertising platform becomes widely adopted in the industry driving incremental value for Rumble shareholders, and should lead to more efficient and effective ad targeting that makes advertising cheaper for creators.

The bull case also sees Rumble avoiding getting into protracted legal battles.

The bull case assumes Rumble is able to fully monetize its assets as a content platform and it is able to reduce its cash burn significantly.

It should attract a large amount of users which will lead to a high revenue multiple and the stock price will rise significantly.

It should be able to generate a 25% Free Cash Flow margin in the long term.

Rumble should be able to leverage its platform to generate substantial amounts of revenue in the long term and its market capitalization should greatly exceed its current valuation.

Rumble should become a household name synonymous with online video and freedom of speech to generate a large amount of revenue for the company.

The number of content creators will grow exponentially in the next few years and Rumble is well placed to benefit from this growth by providing a free speech platform.

Its financials will dramatically improve as the platform scales and advertising efficiency improves.

Rumble is undervalued and should reflect its long term growth prospects as a leader in the free speech internet.

This growth is unfairly discounted because of the short term financial losses of the company.

As the company scales, this loss will become a small fraction of overall revenue.

Rumble should achieve profitability in the near term due to greater ad revenue generation per user, higher than previously anticipated subscription growth and new revenue streams arising from unexpected partnerships or content acquisitions.

The number of users will increase and the cash burn rate will reduce to generate value for shareholders.

Rumble is able to fully monetize its assets as a content platform and reduce its cash burn significantly.

They should be able to achieve at least 500 Million monthly active users in the medium term with revenue per user comparable to Youtube.

In the short run, Rumble's stock price will significantly increase.

This will lead to more content creators joining the platform, creating a virtuous cycle, and will accelerate future user growth.

Rumble is set up to be the YouTube of the next generation, creating significant value for shareholders in the long run.

Rumble also uses AI to moderate content without censorship, creating a more enjoyable experience for content consumers and creators alike.

A favorable ruling in the anti-trust case will further bolster the bull case.

Bear Case: Rumble fails to achieve sustainable growth and struggles to compete with larger, more established video platforms.

Inability to effectively monetize content and attract mainstream advertisers leads to declining revenue and mounting losses.

Content moderation challenges and regulatory pressures further erode user trust and platform integrity.

Rumble faces potential delisting due to financial instability and may be forced to seek a sale at a significant discount, resulting in substantial losses for investors.

Political headwinds further damage the platform's reputation and ability to attract users or advertisers.

Failure to innovate and adapt to changing market dynamics results in stagnation and eventual decline.

Protracted legal battles lead to substantial financial penalties and reputational damage and it may need to raise significant amounts of capital which will dilute existing shareholders.

Rumble is unable to fully monetize its assets as a content platform and the cash burn rate stays high, leading to financial collapse.

Investment recommendation is to SELL and a potential loss of 75% of the current price.

The number of users stagnates and cash burn reduces its cash position to a point where it becomes unable to operate.

Conviction: High

2. Business Overview

Rumble Inc. operates video sharing platforms. The company operates rumble.com, a platform that enables video creators to host, livestream, manage, distribute, and create OTT feeds, as well as monetize their content. It also operates locals.com, a subscription-based video sharing platform. The company was founded in 2013 and is based in Longboat Key, Florida.

The application software market is projected to continue growing at a healthy rate, driven by increasing digitalization, cloud adoption, mobile device usage, and the rising demand for specialized applications across various industries. The video-sharing application segment is expected to see substantial growth due to the increasing consumption of online video content and the rising number of content creators.

Regulatory Environment:

N/A

4. Financial Analysis

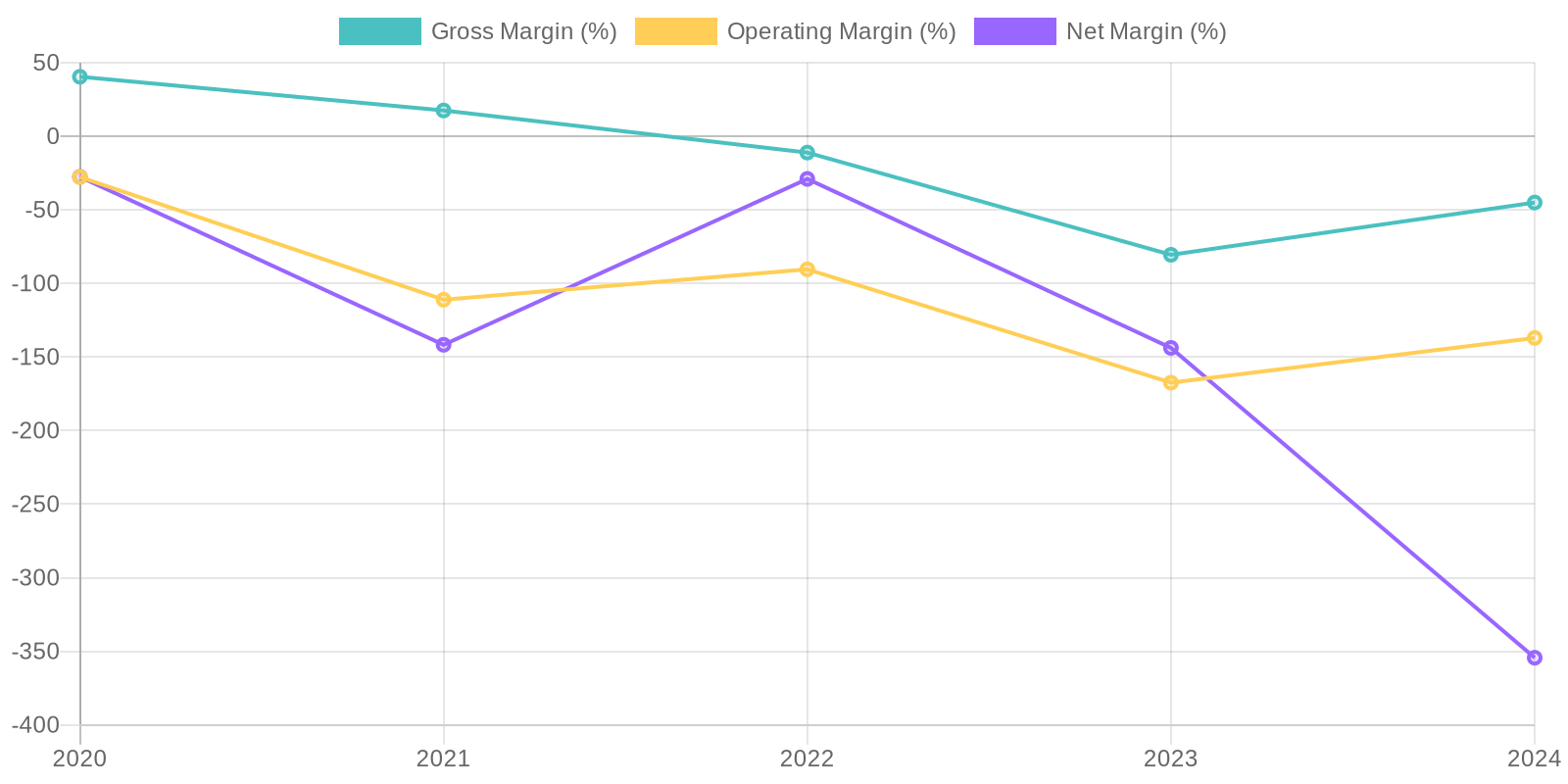

Margin Trend

Given the negative net income and stockholders' equity in 2024, Return on Invested Capital (ROIC) and Return on Equity (ROE) cannot be meaningfully calculated using traditional methods as they would result in negative or undefined values. The negative equity indicates that the company's liabilities exceed its assets, signaling financial distress. This situation necessitates a thorough examination of asset utilization and strategies to improve profitability and equity.

Revenue Quality

The company's revenue stream requires careful examination due to its relatively short history and fluctuating growth. Although revenue increased significantly from 2020 to 2024, reaching $95.49 million, the sustainability of this growth is questionable given the concurrent substantial net losses. Further investigation into client concentration and the recurring nature of revenue is crucial to assess long-term viability. The ability to convert users and sustain their engagement remains a key factor in determining revenue sustainability.

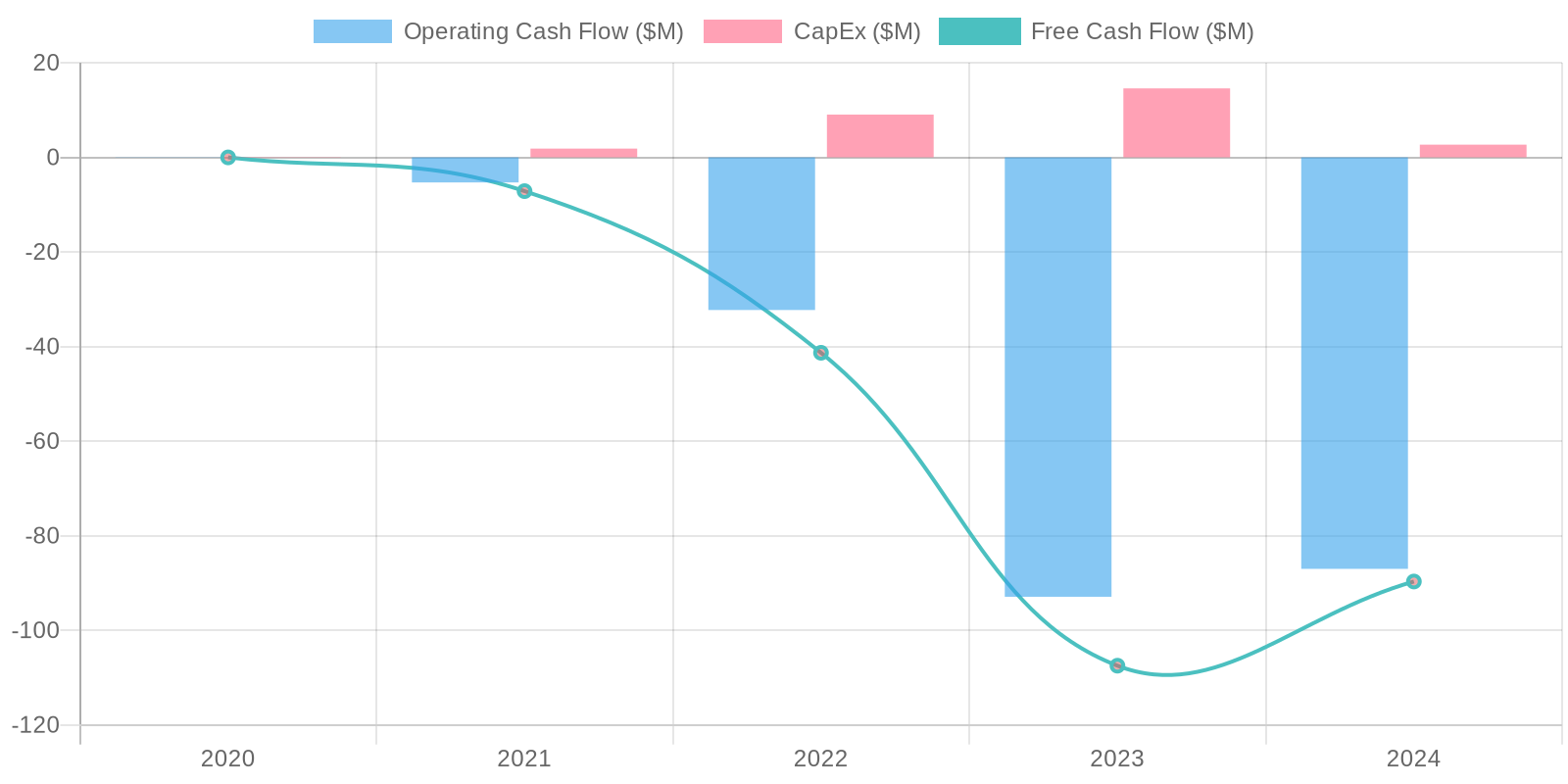

Cash Flow & Capital Efficiency

The company's cash flow statements reveal significant challenges in generating positive cash flow. The free cash flow (FCF) has been negative for all reported periods, with a substantial negative FCF of -$89.68 million in 2024. This persistent negative FCF indicates that the company is consuming cash and needs to either improve operational efficiency, reduce capital expenditures, or secure additional financing. The level of capital expenditure requires continuous monitoring to ensure efficient deployment.

Capital Efficiency (ROIC/ROE):

Given the negative net income and stockholders' equity in 2024, Return on Invested Capital (ROIC) and Return on Equity (ROE) cannot be meaningfully calculated using traditional methods as they would result in negative or undefined values. The negative equity indicates that the company's liabilities exceed its assets, signaling financial distress. This situation necessitates a thorough examination of asset utilization and strategies to improve profitability and equity.

Balance Sheet Health:

The balance sheet analysis exposes vulnerabilities regarding solvency and liquidity. While the company holds a substantial cash balance of $114.02 million in 2024, it is significantly offset by a large retained earnings deficit of -$483.57 million and negative total stockholders' equity of -$63.12 million. The debt level, while relatively low at $1.8 million, is overshadowed by the company's inability to generate profits and positive cash flow, raising concerns about its long-term financial stability. Close monitoring of current liabilities is warranted.

5. Management & Governance

CEO Assessment: Rumble's CEO, Chris Pavlovski, has a demonstrated history of building and scaling online video platforms. Assessing his long-term strategic vision and ability to navigate the evolving media landscape is crucial. Recent news should be monitored for any significant leadership changes or controversies impacting his role.

Capital Allocation: Concern

Insider Ownership: Assessing insider ownership is critical. High insider ownership can align management's interests with shareholders. The percentage of shares held by insiders and any recent selling activity should be investigated to understand alignment and potential risks.

Governance Flags:

Lack of independent directors, Potential conflicts of interest given close relationships between board members and management, Limited transparency in executive compensation, Lack of a formal succession plan

6. Valuation

Method: Price-to-Sales (P/S) Ratio

Fair Value: 1.1

The P/S valuation, using very conservative assumptions due to the company's negative gross margins and net losses, suggests a fair value significantly below the current market price. A low P/S multiple reflects the high risk associated with the company's current financial performance. The downside is substantial due to the overvaluation given the current financials. This method is used because the company is not currently profitable, making other methods less reliable.

Scenarios

Scenario

Price Target

Key Assumptions

Bull

High

Rumble capitalizes on the growing demand for uncensored video platforms and live streaming, attracting creators and users seeking alternatives to mainstream social media.

Successful execution of monetization strategies and strategic partnerships will drive revenue growth and profitability, leading to significant stock appreciation.

Furthermore, a shift in cultural sentiment towards free speech absolutism will dramatically increase Rumble's user base and value, far surpassing current market expectations.

Rumble becomes synonymous with free speech on the internet, attracting major influencers and creating a self-sustaining ecosystem of content and users which will lead to substantial market dominance and premium valuation multiples far exceeding industry peers.

Their success in acquiring and retaining high-profile content creators and scaling their advertising infrastructure will cement its position as a leading video platform and a challenger to YouTube's dominance.

Improved operational efficiencies leads to profitability in the near term due to greater ad revnue generation per user, higher than previously anticipated subscription growth and new revenue streams arising from unexpected partnerships or content acquisitions.

They will achieve at least 500 Million monthly active users in the medium term, with revenue per user comparable to YouTube.

Successful navigation of regulatory scrutiny will also be crucial for long-term success, coupled with effective content moderation policies that maintain user trust and platform integrity.

The investment recommendation is a Strong Buy and the expected return to be 10x the current price.

Rumble's value should reflect its long term growth prospects as a leader in the free speech internet which are being unfairly discounted due to short term financial losses which will become a small fraction of overall revenue as the company scales.

The bull case sees them rapidly gain share and attain profitability faster than analysts predict and attain valuations more closely aligned with peers in the social media and content distribution space.

Rumble should become the go-to platform for a large number of content creators and users who seek to generate a living off the internet, and Rumble should take steps to ensure that this is possible which will attract more creators to the platform and grow the ecosystem.

The RumbleOne advertising platform becomes widely adopted in the industry driving incremental value for Rumble shareholders, and should lead to more efficient and effective ad targeting that makes advertising cheaper for creators.

The bull case also sees Rumble avoiding getting into protracted legal battles.

The bull case assumes Rumble is able to fully monetize its assets as a content platform and it is able to reduce its cash burn significantly.

It should attract a large amount of users which will lead to a high revenue multiple and the stock price will rise significantly.

It should be able to generate a 25% Free Cash Flow margin in the long term.

Rumble should be able to leverage its platform to generate substantial amounts of revenue in the long term and its market capitalization should greatly exceed its current valuation.

Rumble should become a household name synonymous with online video and freedom of speech to generate a large amount of revenue for the company.

The number of content creators will grow exponentially in the next few years and Rumble is well placed to benefit from this growth by providing a free speech platform.

Its financials will dramatically improve as the platform scales and advertising efficiency improves.

Rumble is undervalued and should reflect its long term growth prospects as a leader in the free speech internet.

This growth is unfairly discounted because of the short term financial losses of the company.

As the company scales, this loss will become a small fraction of overall revenue.

Rumble should achieve profitability in the near term due to greater ad revenue generation per user, higher than previously anticipated subscription growth and new revenue streams arising from unexpected partnerships or content acquisitions.

The number of users will increase and the cash burn rate will reduce to generate value for shareholders.

Rumble is able to fully monetize its assets as a content platform and reduce its cash burn significantly.

They should be able to achieve at least 500 Million monthly active users in the medium term with revenue per user comparable to Youtube.

In the short run, Rumble's stock price will significantly increase.

This will lead to more content creators joining the platform, creating a virtuous cycle, and will accelerate future user growth.

Rumble is set up to be the YouTube of the next generation, creating significant value for shareholders in the long run.

Rumble also uses AI to moderate content without censorship, creating a more enjoyable experience for content consumers and creators alike.

A favorable ruling in the anti-trust case will further bolster the bull case. |

| Base | 1.1 | Rumble continues to grow its user base and revenue at a steady pace, but faces challenges in achieving profitability due to high operating costs and competition.

While the platform maintains its appeal to creators and users seeking alternative content, monetization efforts yield moderate success.

Strategic partnerships and content acquisitions contribute to incremental growth, but regulatory scrutiny and content moderation issues persist.

Rumble achieves moderate growth and remains a viable player in the online video space, but struggles to achieve significant market share or profitability.

They should be able to generate 200 Million monthly active users in the medium term with revenue per user that is less than Youtube.

Rumble is able to maintain a decent growth rate, but it fails to reach profitability.

Advertising efficiency does not improve and the platform remains niche.

The RumbleOne advertising platform is not widely adopted and regulatory scrutiny increases.

Rumble does not achieve its goals and remains in a state of limbo.

The company may need to raise more capital in the future.

Investment recommendation is to HOLD with a base case expected return of 2x the current price over a long term period. |

| Bear | Low | Rumble fails to achieve sustainable growth and struggles to compete with larger, more established video platforms.

Inability to effectively monetize content and attract mainstream advertisers leads to declining revenue and mounting losses.

Content moderation challenges and regulatory pressures further erode user trust and platform integrity.

Rumble faces potential delisting due to financial instability and may be forced to seek a sale at a significant discount, resulting in substantial losses for investors.

Political headwinds further damage the platform's reputation and ability to attract users or advertisers.

Failure to innovate and adapt to changing market dynamics results in stagnation and eventual decline.

Protracted legal battles lead to substantial financial penalties and reputational damage and it may need to raise significant amounts of capital which will dilute existing shareholders.

Rumble is unable to fully monetize its assets as a content platform and the cash burn rate stays high, leading to financial collapse.

Investment recommendation is to SELL and a potential loss of 75% of the current price.

The number of users stagnates and cash burn reduces its cash position to a point where it becomes unable to operate. |

7. Risks

Rumble faces critical financial challenges. Persistent negative gross margins, significant net losses, and negative free cash flow raise serious doubts about its long-term viability. While the company currently has cash, its high burn rate could deplete these reserves rapidly. Substantial accumulated losses have resulted in negative equity, making it a high-risk investment.

Red Flags:

Negative Gross Margins

Significant Net Losses

Negative Free Cash Flow

Negative Stockholders' Equity

8. Conclusion

Rumble continues to grow its user base and revenue at a steady pace, but faces challenges in achieving profitability due to high operating costs and competition.

While the platform maintains its appeal to creators and users seeking alternative content, monetization efforts yield moderate success.

Strategic partnerships and content acquisitions contribute to incremental growth, but regulatory scrutiny and content moderation issues persist.

Rumble achieves moderate growth and remains a viable player in the online video space, but struggles to achieve significant market share or profitability.

They should be able to generate 200 Million monthly active users in the medium term with revenue per user that is less than Youtube.

Rumble is able to maintain a decent growth rate, but it fails to reach profitability.

Advertising efficiency does not improve and the platform remains niche.

The RumbleOne advertising platform is not widely adopted and regulatory scrutiny increases.

Rumble does not achieve its goals and remains in a state of limbo.

The company may need to raise more capital in the future.

Investment recommendation is to HOLD with a base case expected return of 2x the current price over a long term period.

Investment research for informational purposes only. Not financial advice.

Continue Your Research

Return to the Analyst Library or explore the specific financial data for this entity on its profile.

Given the negative net income and stockholders' equity in 2024, Return on Invested Capital (ROIC) and Return on Equity (ROE) cannot be meaningfully calculated using traditional methods as they would result in negative or undefined values. The negative equity indicates that the company's liabilities exceed its assets, signaling financial distress. This situation necessitates a thorough examination of asset utilization and strategies to improve profitability and equity.

Given the negative net income and stockholders' equity in 2024, Return on Invested Capital (ROIC) and Return on Equity (ROE) cannot be meaningfully calculated using traditional methods as they would result in negative or undefined values. The negative equity indicates that the company's liabilities exceed its assets, signaling financial distress. This situation necessitates a thorough examination of asset utilization and strategies to improve profitability and equity. The company's cash flow statements reveal significant challenges in generating positive cash flow. The free cash flow (FCF) has been negative for all reported periods, with a substantial negative FCF of -$89.68 million in 2024. This persistent negative FCF indicates that the company is consuming cash and needs to either improve operational efficiency, reduce capital expenditures, or secure additional financing. The level of capital expenditure requires continuous monitoring to ensure efficient deployment.

The company's cash flow statements reveal significant challenges in generating positive cash flow. The free cash flow (FCF) has been negative for all reported periods, with a substantial negative FCF of -$89.68 million in 2024. This persistent negative FCF indicates that the company is consuming cash and needs to either improve operational efficiency, reduce capital expenditures, or secure additional financing. The level of capital expenditure requires continuous monitoring to ensure efficient deployment.