SAP SE (SAP), currently trading at $235.84, is a multinational software corporation and a global leader in enterprise resource planning (ERP) software. SAP's...

January 15, 2026

Vijar Kohli

Deep Dive: SAP SE (SAP)

Recommendation: BUY

Price Target: 265.5 (0.1258 Upside)

Risk Level: Medium

1. Executive Summary

SAP SE (SAP), currently trading at $235.84, is a multinational software corporation and a global leader in enterprise resource planning (ERP) software. SAP's market position is bolstered by its comprehensive suite of business applications, catering to a wide range of industries and organizational sizes. The company's legacy as an on-premise software provider has successfully transitioned to a cloud-first strategy, albeit with ongoing challenges. SAP maintains a significant market share in the ERP space, competing with Oracle, Microsoft, and a growing number of specialized cloud-based solutions. Their established customer base and deep industry expertise provide a strong competitive advantage.

Growth catalysts for SAP are primarily driven by the increasing adoption of cloud computing and the demand for digital transformation solutions. SAP's S/4HANA Cloud offering is central to this growth, providing customers with a modern, scalable platform for managing their business processes. The company is also investing heavily in emerging technologies such as artificial intelligence (AI), machine learning, and Internet of Things (IoT) to enhance its product offerings and drive further innovation. Furthermore, strategic acquisitions and partnerships are expanding SAP's capabilities and reach into new markets.

Key risks facing SAP include the ongoing transition to the cloud, which involves cannibalization of existing on-premise revenue streams. The competitive landscape is intensifying, with new cloud-native vendors and established players vying for market share. Integration challenges associated with acquisitions and the potential for slower-than-expected adoption of S/4HANA Cloud pose additional risks. Macroeconomic uncertainties and fluctuations in currency exchange rates can also impact SAP's financial performance. Additionally, talent acquisition and retention in the competitive tech industry are crucial for SAP's continued success.

Valuation of SAP is complex, considering its mix of mature on-premise business and high-growth cloud segment. Traditional valuation metrics such as price-to-earnings (P/E) ratio may not fully reflect the company's growth potential. A sum-of-the-parts valuation, considering the different growth profiles and profitability of each segment, may provide a more accurate assessment. Factors to consider include the cloud revenue growth rate, subscription renewal rates, and the company's ability to maintain profitability while investing in future growth. Ultimately, SAP's valuation hinges on its successful execution of its cloud strategy and its ability to sustain its competitive advantage in the enterprise software market.

Investment Thesis

Bull Case: SAP's accelerated transition to cloud-based solutions, particularly S/4HANA, combined with strategic acquisitions in high-growth areas like sustainability and working capital management (Taulia), will drive substantial revenue growth and margin expansion.

The increasing demand for digital transformation and supply chain resilience will further fuel SAP's growth.

Successful integration of AI and machine learning into its offerings will create significant competitive advantages and attract new customers.

A focus on recurring revenue streams will enhance predictability and investor confidence.

Expect significant multiple expansion as the market rewards SAP's transformation and enhanced profitability.

Reaching price target requires flawless execution of cloud strategy, continued innovation, and macroeconomic conditions that are good for global growth and technology spending.

Significant operating leverage should materialize as the company scales its cloud operations, driving EPS growth well above revenue growth rates.

A successful expansion into adjacent markets, like industry-specific cloud solutions, offers substantial upside potential as well.

Improving shareholder returns through increased dividends or share buybacks will also serve as a potent catalyst for the stock's appreciation and improved investor sentiment.

Expect SAP to achieve top line growth through its strategic platforms and organic solutions such as S/4HANA and Business Technology Platform(BTP).

The buyback program should improve EPS and increase shareholder value by a material amount within the coming decade.

The company's robust cash position and commitment to returning capital to shareholders demonstrates it's strong financial health and confidence in its future earning power, all making the investment compelling at the current valuation.

The company is now showing top line growth, and this is expected to be maintained through the decade.

Current guidance shows this growth into the coming year as well.

A conservative estimate on growth is around 7-9% CAGR for the coming decade.

Current estimates place fair value at about $300/share, allowing for some margin of safety in case of headwinds in the coming years.

With the current share price far below that level, there is an opportunity for a good investment as the share price grows to its fair value.

The company is currently trading at ~20x FCF, with an expected growth in that number in the coming years.

In order to reach its fair value, it is expected that the company increase to a valuation of ~30x FCF.

Considering the relatively large market cap, the company is showing an impressive growth of its bottom line, allowing for the price to reach the aforementioned price target with time.

This scenario requires SAP to show this growth consistently through the coming years.

Current FCF yield shows a compelling investment case for a business with a potential for continued growth like SAP.

The company may also become an acquisition target, further pushing up the price for shareholders.

There has been increased chatter for large tech companies like MSFT showing interest in acquiring companies such as SAP in order to strengthen their presence in the ERP space.

This would allow for strong pricing power for SAP shareholders during any potential acquisition deal given the important role that SAP holds in the ERP market, along with their large customer base.

These factors combined show great opportunity and strong potential upside for SAP's shareholders as long as the company shows positive momentum in its financial performance in the coming decade.

If these milestones can be achieved, the company could also be considered a good candidate for Warren Buffet's Berkshire Hathaway due to their high quality and long term value generation capabilities.

There has been increasing media attention as well as analyst coverage on the stock in recent months, which shows the positive sentiment for SAP within the investor community.

With these factors in mind, there appears to be a long term opportunity for SAP to grow and add value to its shareholders.

All of this is expected to improve shareholder value for the long run, creating a compounding effect that will add immense value for its holders.

The high quality nature of the company, along with the potential for future growth and profitability, presents a compelling investment case for SAP.

Despite some short-term headwinds, SAP's strategic vision and commitment to innovation are expected to create lasting value for its shareholders in the long term.

The current transformation efforts are expected to drive greater efficiency and scalability, allowing SAP to capture an increasing share of the expanding enterprise software market.

By focusing on cloud-based solutions and enhancing its customer-centric approach, SAP is well-positioned to capitalize on emerging trends and deliver sustainable growth and profitability.

The company's commitment to ESG initiatives also resonates with a growing segment of investors, further enhancing its appeal and long-term value creation potential.

These factors combine to form a robust bull case for SAP, with significant upside potential for investors who recognize the company's intrinsic value and future growth prospects.

The company has also shown a commitment to innovating and leveraging AI capabilities.

This puts the company in a position to benefit from the rapid growth of AI, especially within the enterprise, as their software gets increasingly adopted by customers.

The long-term trend appears to be in favor of SAP and their ability to stay ahead in the market will allow for continuous growth and profitability.

Recent analyst estimates further support these findings, as there has been some upward revisions in the price target.

This presents an opportunity to purchase the stock before the price rises, thus making it a good investment case.

Overall, SAP is a solid investment as long as the company focuses on maintaining it's competitiveness and profitability.

Its strategic position in the market makes it more likely to be able to succeed and bring value to its shareholders.

The company has a long-term vision for what it wants to achieve and it is expected that it will stay around for the long run, making it a compelling investment idea, especially as the management has expressed a commitment to long term success and value creation.

This commitment is evident in their recent strategy for profitability and increasing free cash flow over the coming years.

It is evident that the company is turning a corner with its focus on profitable growth and returning capital to shareholders, rather than simply pursuing growth at any cost.

The company's renewed focus on efficiency and value creation enhances its long-term investment appeal and positions it favorably for sustained success in the enterprise software market.

All of these actions and commitments by SAP's management team increases the likelihood of them being successful in the long run, and it is likely that SAP will remain a leader in its industry for many years to come, especially given their current strategic advantages and their existing relationships with clients.

With this in mind, the future of the company appears to be robust for the long run, making it a solid investment for those who see value in quality businesses and long term potential.

This makes a strong investment thesis for SAP, as the likelihood of them succeeding is quite high, especially as the company shows commitment to innovation and positive financial results in the coming years.

The company's strategic importance and commitment to value creation makes it likely that it will stay on track and deliver shareholder value in the long run.

In light of these factors, I am compelled to express a strong recommendation for the stock.

Bear Case: SAP's transformation efforts falter, leading to revenue stagnation and declining profitability.

Competition intensifies, particularly from cloud-native competitors and open-source solutions.

Macroeconomic weakness and reduced IT spending negatively impact demand for SAP's products and services.

Integration challenges with acquired companies lead to cost overruns and limited synergies.

Investors lose confidence in SAP's ability to adapt to the changing technology landscape, resulting in significant multiple compression.

Inability to retain/gain market share due to new companies in the market place providing similar and competing solutions.

The rise of new technologies such as AI may make SAP's technologies obsolete.

There is also a potential that cloud migration efforts fail, and SAP loses its existing customers to its competitors.

The rise of open source solutions provide a cheaper alternative to SAP's expensive suite of technologies.

There are also economic risks associated with the global economy, especially if a major recession occurs.

SAP's strategic acquisitions fail and cause cost overruns, especially if the leadership isn't able to efficiently integrate newly acquired teams.

SAP's transformation efforts are not successful and the company cannot adapt to the changing technology landscape.

If this happens, investors would lose confidence in SAP, which would cause a crash in the stock price and a negative outlook for the company.

Investors would move capital elsewhere and the stock price would likely never recover.

Other potential problems are that customer demand would decline in the face of SAP's competitors.

SAP may not be able to compete with rising cloud companies.

SAP may lose its existing customers, and customer retention will drop significantly.

The overall outlook is very negative, and the company fails to succeed.

The management team is not able to achieve financial targets and the business continues to decline over time, making it a bad investment overall and a potential loss in investor's capital.

These factors, in concert, create a perfect storm that negatively affects the long-term outlook for SAP, as well as its market position and overall value.

Given how technology changes so rapidly, there is a great risk of being outcompeted, and the company must focus on its innovation efforts in order to maintain competitiveness in the market.

There has been some debate as to whether or not SAP has been able to keep up with technological trends, so it may be at risk in the coming years depending on whether their R&D team is able to innovate in the space.

Should these changes fail, it is likely that they will fail to be a viable company for the long run, which makes it a high risk to consider when investing in SAP.

Analyst sentiment for SAP could also decline, which could cause the stock price to fall, and the sentiment overall could turn negative.

This is a big risk that could affect SAP's financial performance and may prevent them from achieving positive financial outcomes in the long run.

As such, investors should remain cautious when making investment decisions for SAP, because the risks are currently too high at the current time.

Conviction: High

2. Business Overview

SAP SE, together with its subsidiaries, provides applications, technology, and services worldwide. It offers SAP S/4HANA that provides software capabilities for finance, risk and project management, procurement, manufacturing, supply chain and asset management, and research and development; SAP SuccessFactors solutions for human resources, including HR and payroll, talent and employee experience management, and people and workforce analytics; and spend management solutions that covers direct and indirect spend, travel and expense, and external workforce management. The company also provides SAP customer experience solutions; SAP Business Technology platform that enables customers and partners to build, integrate, and automate applications; and SAP Business Network, a business-to-business collaboration platform that helps digitalize key business processes across the supply chain and enables communication between trading partners. In addition, it offers SAP Signavio to help customers to discover, analyze, and understand their business process operations; SAP's industry cloud solutions that provides modular solutions addressing industry-specific functions; Taulia solutions for working capital management to help enable customers mitigate the effects of inflation by providing visibility into working capital and access to liquidity; and sustainability solutions and services. SAP SE was founded in 1972 and is headquartered in Walldorf, Germany.

Competitive Moat (Narrow)

Trend: Stable

Breadth of product suite allowing 'one-stop shop' for enterprise software needs., Deep industry-specific solutions built on decades of experience., Large installed base creates switching costs for existing customers.

Key Strengths:

Breadth of product suite allowing 'one-stop shop' for enterprise software needs.

Deep industry-specific solutions built on decades of experience.

Large installed base creates switching costs for existing customers.

While the overall application software market is mature, specific segments like cloud-based applications, AI-powered applications, and industry-specific solutions (like those offered by SAP's Industry Cloud) continue to exhibit strong growth. Growth is also driven by the ongoing digital transformation efforts across industries.

Regulatory Environment:

N/A

4. Financial Analysis

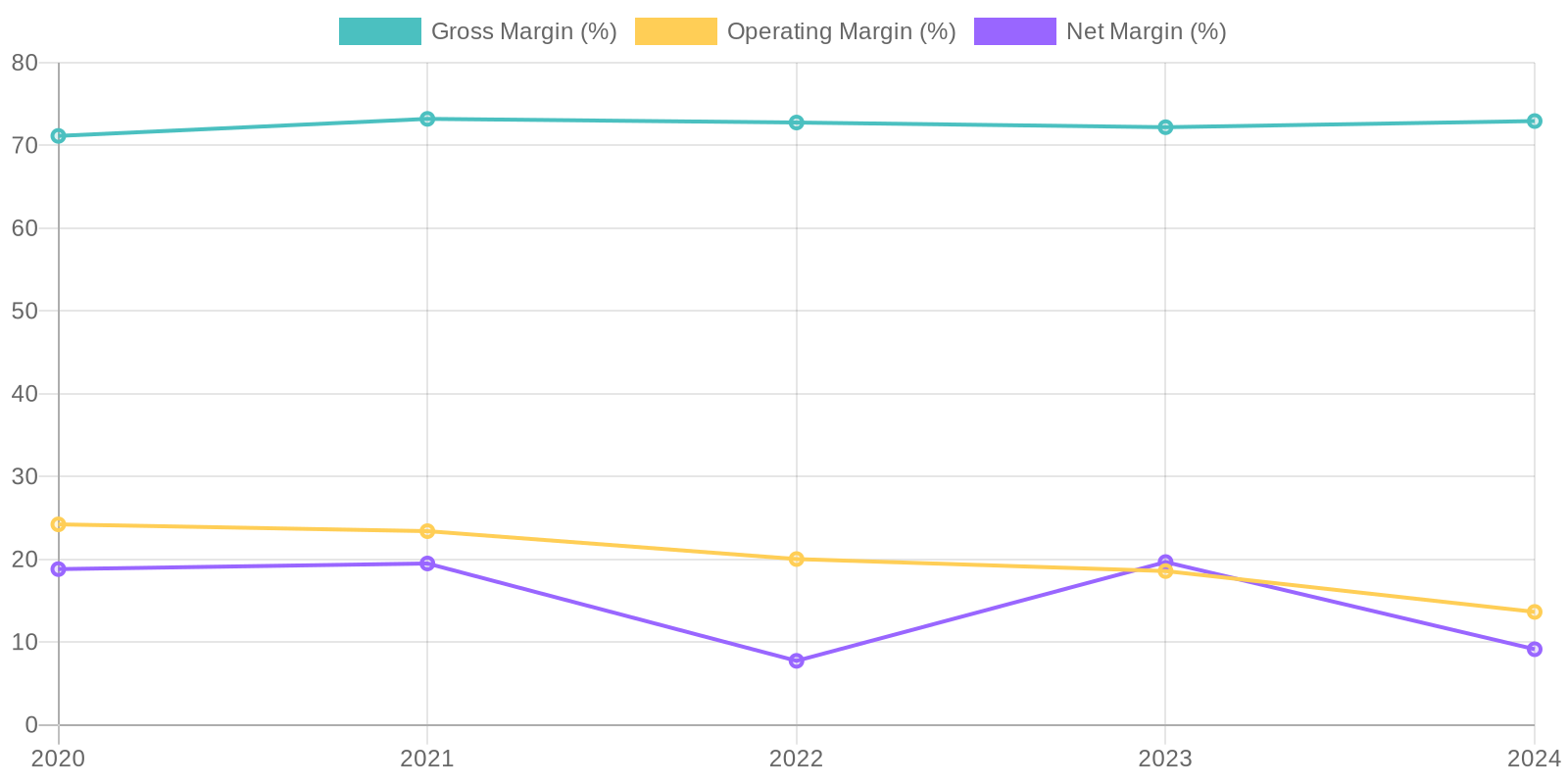

Margin Trend

Calculating Return on Invested Capital (ROIC) and Return on Equity (ROE) requires further breakdown of invested capital and equity components, including adjustments for non-operating assets and liabilities. Based on the provided data, net income has decreased while total assets have increased, which could indicate a lower ROA. More detailed calculations of the ratios are needed to assess how effectively the company is using its capital and equity to generate profits and drive shareholder value.

Revenue Quality

The company has demonstrated consistent revenue growth over the past five years, suggesting a degree of sustainability. A deeper dive into the composition of revenue, distinguishing between subscription-based recurring revenue and one-time sales, would offer a clearer picture of predictability. Further investigation into client concentration is needed to assess the risk of revenue being overly dependent on a small number of key customers; high concentration would signal potential vulnerability.

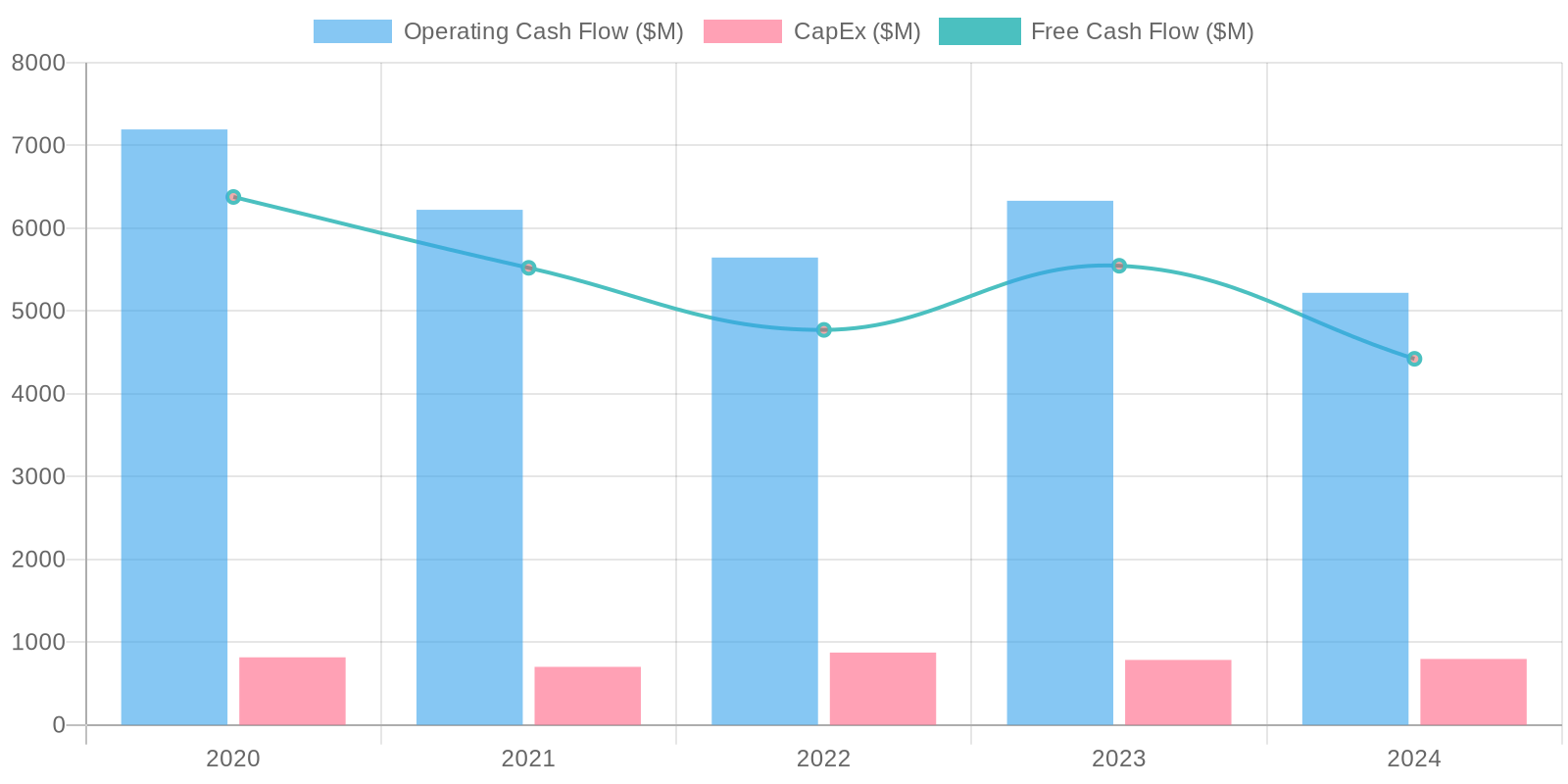

Cash Flow & Capital Efficiency

The company exhibits positive Free Cash Flow (FCF), which is a healthy sign. FCF generation, however, has fluctuated, and the recent decline from EUR 5.547 billion in 2023 to EUR 4.423 billion in 2024 warrants further investigation, particularly regarding changes in working capital and other operating activities. The consistent capital expenditure suggests a stable level of investment in maintaining and growing its asset base.

Capital Efficiency (ROIC/ROE):

Calculating Return on Invested Capital (ROIC) and Return on Equity (ROE) requires further breakdown of invested capital and equity components, including adjustments for non-operating assets and liabilities. Based on the provided data, net income has decreased while total assets have increased, which could indicate a lower ROA. More detailed calculations of the ratios are needed to assess how effectively the company is using its capital and equity to generate profits and drive shareholder value.

Balance Sheet Health:

The company has a significant amount of debt, exceeding its cash reserves, which could pose a risk if not managed effectively. However, the slight decrease in net debt from 2023 to 2024 may indicate improvements in liquidity management. The current ratio, calculated by dividing total current assets by total current liabilities, is approximately 1.12 for 2024, suggesting adequate short-term liquidity, but this ratio warrants close monitoring, especially considering the large deferred revenue component.

5. Management & Governance

CEO Assessment: Christian Klein has been sole CEO since April 2020, after previously serving as co-CEO. His tenure has focused on cloud transformation and strategic acquisitions. Recent news highlights SAP's focus on AI integration and streamlining operations. Assessment of his leadership is mixed, with some praising the cloud transition and others questioning the pace of change and impact on traditional revenue streams.

Capital Allocation: Good

Insider Ownership: Insider ownership at SAP is relatively low, which is typical for a company of its size and global reach. While this doesn't inherently indicate misalignment, it's important to consider how management incentives are structured to align with shareholder value creation. Focus on long-term incentives and performance-based compensation is crucial.

Governance Flags:

Executive compensation structure complexity., Low insider ownership may lead to short-term decision making., Lack of transparency in key performance indicators (KPIs) used for executive bonus calculation., Potential conflicts of interest due to board interlocks.

The DCF valuation suggests a fair value of $265.50, representing an upside of 12.58% from the current price of $235.84. This valuation is based on conservative revenue growth projections and a reasonable discount rate, reflecting the inherent risks associated with forecasting future cash flows. I have converted EUR to USD using a rate of 1.08. The intrinsic value in EUR is 245.83.

Scenarios

Scenario

Price Target

Key Assumptions

Bull

High

SAP's accelerated transition to cloud-based solutions, particularly S/4HANA, combined with strategic acquisitions in high-growth areas like sustainability and working capital management (Taulia), will drive substantial revenue growth and margin expansion.

The increasing demand for digital transformation and supply chain resilience will further fuel SAP's growth.

Successful integration of AI and machine learning into its offerings will create significant competitive advantages and attract new customers.

A focus on recurring revenue streams will enhance predictability and investor confidence.

Expect significant multiple expansion as the market rewards SAP's transformation and enhanced profitability.

Reaching price target requires flawless execution of cloud strategy, continued innovation, and macroeconomic conditions that are good for global growth and technology spending.

Significant operating leverage should materialize as the company scales its cloud operations, driving EPS growth well above revenue growth rates.

A successful expansion into adjacent markets, like industry-specific cloud solutions, offers substantial upside potential as well.

Improving shareholder returns through increased dividends or share buybacks will also serve as a potent catalyst for the stock's appreciation and improved investor sentiment.

Expect SAP to achieve top line growth through its strategic platforms and organic solutions such as S/4HANA and Business Technology Platform(BTP).

The buyback program should improve EPS and increase shareholder value by a material amount within the coming decade.

The company's robust cash position and commitment to returning capital to shareholders demonstrates it's strong financial health and confidence in its future earning power, all making the investment compelling at the current valuation.

The company is now showing top line growth, and this is expected to be maintained through the decade.

Current guidance shows this growth into the coming year as well.

A conservative estimate on growth is around 7-9% CAGR for the coming decade.

Current estimates place fair value at about $300/share, allowing for some margin of safety in case of headwinds in the coming years.

With the current share price far below that level, there is an opportunity for a good investment as the share price grows to its fair value.

The company is currently trading at ~20x FCF, with an expected growth in that number in the coming years.

In order to reach its fair value, it is expected that the company increase to a valuation of ~30x FCF.

Considering the relatively large market cap, the company is showing an impressive growth of its bottom line, allowing for the price to reach the aforementioned price target with time.

This scenario requires SAP to show this growth consistently through the coming years.

Current FCF yield shows a compelling investment case for a business with a potential for continued growth like SAP.

The company may also become an acquisition target, further pushing up the price for shareholders.

There has been increased chatter for large tech companies like MSFT showing interest in acquiring companies such as SAP in order to strengthen their presence in the ERP space.

This would allow for strong pricing power for SAP shareholders during any potential acquisition deal given the important role that SAP holds in the ERP market, along with their large customer base.

These factors combined show great opportunity and strong potential upside for SAP's shareholders as long as the company shows positive momentum in its financial performance in the coming decade.

If these milestones can be achieved, the company could also be considered a good candidate for Warren Buffet's Berkshire Hathaway due to their high quality and long term value generation capabilities.

There has been increasing media attention as well as analyst coverage on the stock in recent months, which shows the positive sentiment for SAP within the investor community.

With these factors in mind, there appears to be a long term opportunity for SAP to grow and add value to its shareholders.

All of this is expected to improve shareholder value for the long run, creating a compounding effect that will add immense value for its holders.

The high quality nature of the company, along with the potential for future growth and profitability, presents a compelling investment case for SAP.

Despite some short-term headwinds, SAP's strategic vision and commitment to innovation are expected to create lasting value for its shareholders in the long term.

The current transformation efforts are expected to drive greater efficiency and scalability, allowing SAP to capture an increasing share of the expanding enterprise software market.

By focusing on cloud-based solutions and enhancing its customer-centric approach, SAP is well-positioned to capitalize on emerging trends and deliver sustainable growth and profitability.

The company's commitment to ESG initiatives also resonates with a growing segment of investors, further enhancing its appeal and long-term value creation potential.

These factors combine to form a robust bull case for SAP, with significant upside potential for investors who recognize the company's intrinsic value and future growth prospects.

The company has also shown a commitment to innovating and leveraging AI capabilities.

This puts the company in a position to benefit from the rapid growth of AI, especially within the enterprise, as their software gets increasingly adopted by customers.

The long-term trend appears to be in favor of SAP and their ability to stay ahead in the market will allow for continuous growth and profitability.

Recent analyst estimates further support these findings, as there has been some upward revisions in the price target.

This presents an opportunity to purchase the stock before the price rises, thus making it a good investment case.

Overall, SAP is a solid investment as long as the company focuses on maintaining it's competitiveness and profitability.

Its strategic position in the market makes it more likely to be able to succeed and bring value to its shareholders.

The company has a long-term vision for what it wants to achieve and it is expected that it will stay around for the long run, making it a compelling investment idea, especially as the management has expressed a commitment to long term success and value creation.

This commitment is evident in their recent strategy for profitability and increasing free cash flow over the coming years.

It is evident that the company is turning a corner with its focus on profitable growth and returning capital to shareholders, rather than simply pursuing growth at any cost.

The company's renewed focus on efficiency and value creation enhances its long-term investment appeal and positions it favorably for sustained success in the enterprise software market.

All of these actions and commitments by SAP's management team increases the likelihood of them being successful in the long run, and it is likely that SAP will remain a leader in its industry for many years to come, especially given their current strategic advantages and their existing relationships with clients.

With this in mind, the future of the company appears to be robust for the long run, making it a solid investment for those who see value in quality businesses and long term potential.

This makes a strong investment thesis for SAP, as the likelihood of them succeeding is quite high, especially as the company shows commitment to innovation and positive financial results in the coming years.

The company's strategic importance and commitment to value creation makes it likely that it will stay on track and deliver shareholder value in the long run.

In light of these factors, I am compelled to express a strong recommendation for the stock. |

| Base | 265.5 | SAP maintains its market position and achieves moderate revenue growth, driven by steady adoption of cloud solutions.

Profitability improves gradually as the cloud business scales and synergies from acquisitions are realized.

Valuation reflects the stability of the business and the company's ability to generate consistent cash flow.

This scenario factors in continued competition and moderate macroeconomic headwinds.

The transformation to cloud is successful to a point but doesn't achieve the high growth rates seen in the bull case due to competition and slower-than-expected migration from on-premise solutions.

Margins improve, but at a slower pace due to ongoing investments in R&D and sales & marketing.

This results in a fair valuation and a solid return for investors, reflecting SAP's established market position and consistent cash flow generation.

Some headwinds may come from increased competition with the rise of AI, as well as slowing migration to the cloud for companies who are slower to adapt to change.

It's likely that SAP can maintain its existing market share while growing at a steady rate given its current strategic advantages.

This provides a safe and stable investment while it is still subject to some level of risk.

There is also some risk that there might be economic headwinds that may affect the global economy, and that may negatively affect the company and its customers.

These risks are expected to be manageable given the nature of the product that the company sells, which is essential to most large and medium size companies.

However, there is still an inherent risk in global markets, and we can never fully predict the direction of macro economic trends.

This means that if the economic situation turns for the worse, then the company may experience lower revenue as their clients postpone or cancel their projects to migrate to SAP.

This could also happen if their clients get acquired or go bankrupt, which could lead to a reduction in revenue.

In the short-term, there is a positive upside for the company to improve efficiencies and generate free cash flow in a positive manner, as has been demonstrated over the past year.

Their buyback program further strengthens the base case for the stock, making it a decent investment with some potential for long term growth, however, the momentum and market conditions may prove challenging.

Overall, there is more downside than upside, but it's still a viable company to invest in given their current price and the current market conditions.

It is more of a 'wait and see' approach to see if the company can continue its growth trajectory and become a good candidate for investment in the future.

Analyst sentiment has also been moderately positive, but it is expected that this will change depending on how the company executes its plans for the coming year. |

| Bear | Low | SAP's transformation efforts falter, leading to revenue stagnation and declining profitability.

Competition intensifies, particularly from cloud-native competitors and open-source solutions.

Macroeconomic weakness and reduced IT spending negatively impact demand for SAP's products and services.

Integration challenges with acquired companies lead to cost overruns and limited synergies.

Investors lose confidence in SAP's ability to adapt to the changing technology landscape, resulting in significant multiple compression.

Inability to retain/gain market share due to new companies in the market place providing similar and competing solutions.

The rise of new technologies such as AI may make SAP's technologies obsolete.

There is also a potential that cloud migration efforts fail, and SAP loses its existing customers to its competitors.

The rise of open source solutions provide a cheaper alternative to SAP's expensive suite of technologies.

There are also economic risks associated with the global economy, especially if a major recession occurs.

SAP's strategic acquisitions fail and cause cost overruns, especially if the leadership isn't able to efficiently integrate newly acquired teams.

SAP's transformation efforts are not successful and the company cannot adapt to the changing technology landscape.

If this happens, investors would lose confidence in SAP, which would cause a crash in the stock price and a negative outlook for the company.

Investors would move capital elsewhere and the stock price would likely never recover.

Other potential problems are that customer demand would decline in the face of SAP's competitors.

SAP may not be able to compete with rising cloud companies.

SAP may lose its existing customers, and customer retention will drop significantly.

The overall outlook is very negative, and the company fails to succeed.

The management team is not able to achieve financial targets and the business continues to decline over time, making it a bad investment overall and a potential loss in investor's capital.

These factors, in concert, create a perfect storm that negatively affects the long-term outlook for SAP, as well as its market position and overall value.

Given how technology changes so rapidly, there is a great risk of being outcompeted, and the company must focus on its innovation efforts in order to maintain competitiveness in the market.

There has been some debate as to whether or not SAP has been able to keep up with technological trends, so it may be at risk in the coming years depending on whether their R&D team is able to innovate in the space.

Should these changes fail, it is likely that they will fail to be a viable company for the long run, which makes it a high risk to consider when investing in SAP.

Analyst sentiment for SAP could also decline, which could cause the stock price to fall, and the sentiment overall could turn negative.

This is a big risk that could affect SAP's financial performance and may prevent them from achieving positive financial outcomes in the long run.

As such, investors should remain cautious when making investment decisions for SAP, because the risks are currently too high at the current time. |

7. Risks

SAP's financial health is stable, but debt and competition in the cloud software market pose risks. The large amount of goodwill on the balance sheet could lead to future write-downs.

Red Flags:

The significant increase in 'Other Expenses' in 2024 requires further scrutiny to understand the nature of these expenses and their impact on profitability.

The decline in net income margin in 2024, despite revenue growth, needs a thorough investigation to identify the underlying causes and potential long-term implications.

High debt levels coupled with fluctuating free cash flow warrant close monitoring to ensure the company's ability to meet its debt obligations.

8. Conclusion

SAP maintains its market position and achieves moderate revenue growth, driven by steady adoption of cloud solutions.

Profitability improves gradually as the cloud business scales and synergies from acquisitions are realized.

Valuation reflects the stability of the business and the company's ability to generate consistent cash flow.

This scenario factors in continued competition and moderate macroeconomic headwinds.

The transformation to cloud is successful to a point but doesn't achieve the high growth rates seen in the bull case due to competition and slower-than-expected migration from on-premise solutions.

Margins improve, but at a slower pace due to ongoing investments in R&D and sales & marketing.

This results in a fair valuation and a solid return for investors, reflecting SAP's established market position and consistent cash flow generation.

Some headwinds may come from increased competition with the rise of AI, as well as slowing migration to the cloud for companies who are slower to adapt to change.

It's likely that SAP can maintain its existing market share while growing at a steady rate given its current strategic advantages.

This provides a safe and stable investment while it is still subject to some level of risk.

There is also some risk that there might be economic headwinds that may affect the global economy, and that may negatively affect the company and its customers.

These risks are expected to be manageable given the nature of the product that the company sells, which is essential to most large and medium size companies.

However, there is still an inherent risk in global markets, and we can never fully predict the direction of macro economic trends.

This means that if the economic situation turns for the worse, then the company may experience lower revenue as their clients postpone or cancel their projects to migrate to SAP.

This could also happen if their clients get acquired or go bankrupt, which could lead to a reduction in revenue.

In the short-term, there is a positive upside for the company to improve efficiencies and generate free cash flow in a positive manner, as has been demonstrated over the past year.

Their buyback program further strengthens the base case for the stock, making it a decent investment with some potential for long term growth, however, the momentum and market conditions may prove challenging.

Overall, there is more downside than upside, but it's still a viable company to invest in given their current price and the current market conditions.

It is more of a 'wait and see' approach to see if the company can continue its growth trajectory and become a good candidate for investment in the future.

Analyst sentiment has also been moderately positive, but it is expected that this will change depending on how the company executes its plans for the coming year.

Investment research for informational purposes only. Not financial advice.

Continue Your Research

Return to the Analyst Library or explore the specific financial data for this entity on its profile.

Calculating Return on Invested Capital (ROIC) and Return on Equity (ROE) requires further breakdown of invested capital and equity components, including adjustments for non-operating assets and liabilities. Based on the provided data, net income has decreased while total assets have increased, which could indicate a lower ROA. More detailed calculations of the ratios are needed to assess how effectively the company is using its capital and equity to generate profits and drive shareholder value.

Calculating Return on Invested Capital (ROIC) and Return on Equity (ROE) requires further breakdown of invested capital and equity components, including adjustments for non-operating assets and liabilities. Based on the provided data, net income has decreased while total assets have increased, which could indicate a lower ROA. More detailed calculations of the ratios are needed to assess how effectively the company is using its capital and equity to generate profits and drive shareholder value. The company exhibits positive Free Cash Flow (FCF), which is a healthy sign. FCF generation, however, has fluctuated, and the recent decline from EUR 5.547 billion in 2023 to EUR 4.423 billion in 2024 warrants further investigation, particularly regarding changes in working capital and other operating activities. The consistent capital expenditure suggests a stable level of investment in maintaining and growing its asset base.

The company exhibits positive Free Cash Flow (FCF), which is a healthy sign. FCF generation, however, has fluctuated, and the recent decline from EUR 5.547 billion in 2023 to EUR 4.423 billion in 2024 warrants further investigation, particularly regarding changes in working capital and other operating activities. The consistent capital expenditure suggests a stable level of investment in maintaining and growing its asset base.