StubHub Holdings, Inc. (STUB), currently trading at $15.2, operates in the live event ticketing marketplace. The company holds a significant, although not ne...

January 15, 2026

Vijar Kohli

Deep Dive: StubHub Holdings, Inc. (STUB)

Recommendation: BUY

Price Target: 16.75 (0.1 Upside)

Risk Level: Medium

1. Executive Summary

StubHub Holdings, Inc. (STUB), currently trading at $15.2, operates in the live event ticketing marketplace. The company holds a significant, although not necessarily dominant, market position. StubHub faces strong competition from Ticketmaster, SeatGeek, and other smaller players. Its market share is influenced by factors such as brand recognition, user experience, inventory availability, and pricing strategies. The ticketing industry has seen a shift towards digital platforms, and StubHub has adapted to this trend, with a substantial portion of its transactions occurring online.

Growth catalysts for StubHub include the increasing demand for live entertainment experiences following the pandemic. As concerts, sporting events, and theater performances resume, there's pent-up demand for tickets. Strategic partnerships with event organizers and venues can enhance StubHub's inventory and reach. Furthermore, international expansion into untapped markets presents another avenue for growth. Innovations in mobile ticketing and personalized user experiences could also drive increased user engagement and transaction volume. The expansion of StubHub's offerings to include related services such as travel packages or merchandise can further boost revenue.

Key risks facing StubHub include intense competition, which can pressure margins and market share. Cybersecurity threats and data breaches pose a constant risk to user data and platform security. Regulatory changes related to ticket resale or consumer protection laws can impact the company's operations and profitability. Economic downturns can reduce consumer spending on discretionary items like event tickets. Furthermore, negative press or reputational damage resulting from issues such as scalping or fraudulent tickets can erode consumer trust and brand value. A potential major and extended health crisis or other event affecting live gatherings can drastically impact the revenue model.

Valuation summary: Determining a precise valuation for StubHub requires detailed financial analysis and market comparisons. Factors to consider include revenue growth, profitability, market share, and competitive landscape. Due to the absence of detailed financial data for StubHub, the current price of $15.2 is difficult to assess in terms of overvaluation or undervaluation. A full valuation would require a discounted cash flow analysis, comparable company analysis, and consideration of industry-specific metrics. Furthermore, external macroeconomic trends and overall investor sentiment toward the live entertainment sector would influence the ultimate fair value assessment.

Investment Thesis

Bull Case: StubHub is poised for significant growth as the live event industry recovers and expands.

The company's dominant market position, strong brand recognition, and scalable platform will drive revenue and earnings growth, leading to substantial shareholder value creation.

Successful execution of international expansion and strategic partnerships will accelerate growth beyond current expectations.

Bear Case: StubHub's business could be negatively impacted by increased competition, economic headwinds, or regulatory challenges.

A decline in live event attendance, coupled with higher operating costs or legal liabilities, could lead to a significant decline in revenue and profitability, resulting in a substantial loss for investors.

Conviction: High

2. Business Overview

StubHub is a leading global platform for secondary ticket sales for live events, facilitating millions of tickets for sports, concerts, theater, and more across over 200 countries. Founded in 2000, it enables buyers and sellers to connect and transact tickets through its online marketplace, earning primarily through transaction fees. The platform supports various event types and offers a digital marketplace for ticket resale.

Competitive Moat (Narrow)

Trend: Stable

Established brand recognition, Extensive user base

Growth is expected to continue, driven by increasing demand for digital ticketing, personalized experiences, and mobile-first solutions. However, growth rates may be moderate due to market saturation and competition.

Regulatory Environment:

N/A

4. Financial Analysis

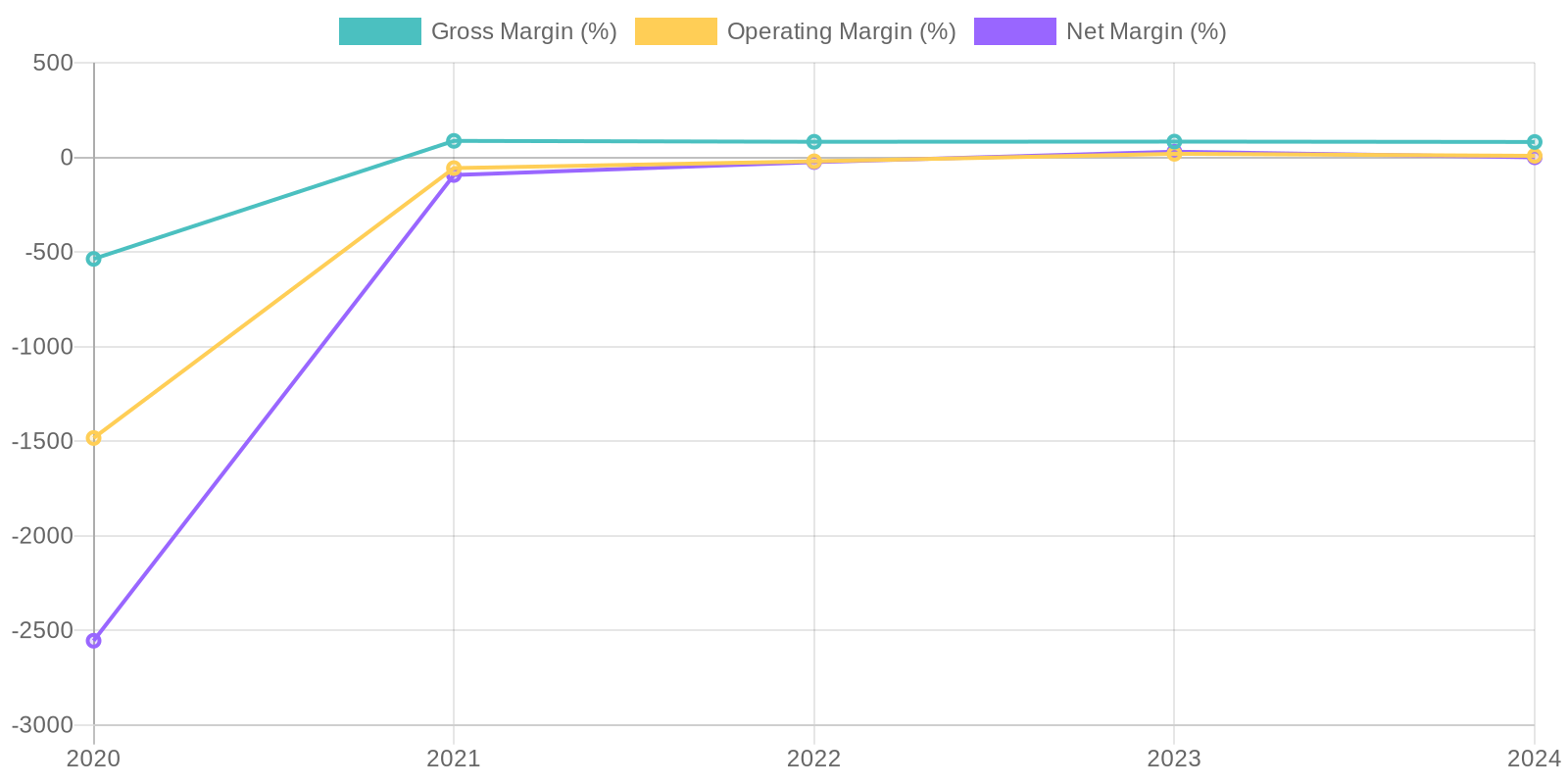

Margin Trend

Due to the recent unprofitability, Return on Invested Capital (ROIC) and Return on Equity (ROE) calculations are skewed and potentially misleading. While a precise calculation isn't directly feasible given the fluctuating net income, the negative net income in 2024 raises concerns about the company's efficient use of capital. Furthermore, a deeper dive into asset turnover and profit margins is warranted to understand the drivers behind the company's capital efficiency or lack thereof.

Revenue Quality

The company has demonstrated substantial revenue growth over the past five years, indicating increasing market acceptance of its software applications. However, the forensic accountant must investigate the source and concentration of these revenues. It is critical to determine if a small number of clients account for a disproportionate amount of revenue, posing a risk if those relationships are compromised. Additionally, revenue recognition policies should be examined to ensure they are aligned with industry standards and that revenue is earned and realized, to ensure revenue sustainability.

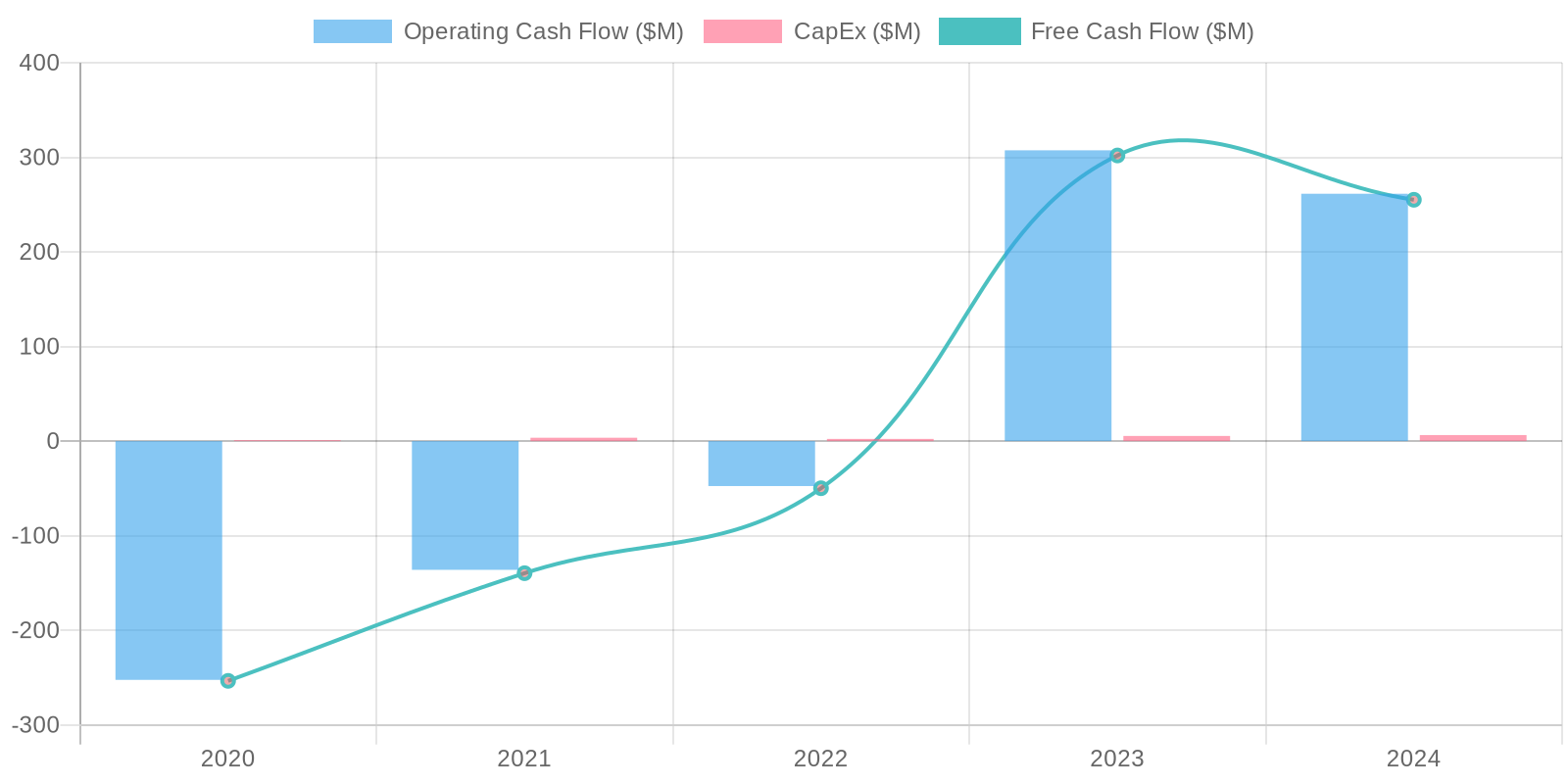

Cash Flow & Capital Efficiency

The company's free cash flow (FCF) generation shows a positive trend in 2023 and 2024, signaling improvement in cash management. The substantial capital expenditures (CAPEX) is relatively low compared to revenue, which is typical for a software company. Examine the investments in property, plant, and equipment to ensure they align with company growth strategies. The FCF trend needs to be sustained to support future growth and manage debt obligations.

Capital Efficiency (ROIC/ROE):

Due to the recent unprofitability, Return on Invested Capital (ROIC) and Return on Equity (ROE) calculations are skewed and potentially misleading. While a precise calculation isn't directly feasible given the fluctuating net income, the negative net income in 2024 raises concerns about the company's efficient use of capital. Furthermore, a deeper dive into asset turnover and profit margins is warranted to understand the drivers behind the company's capital efficiency or lack thereof.

Balance Sheet Health:

The company carries a significant debt burden, exceeding $2.3 billion in 2024, requiring close monitoring of its debt covenants and repayment schedules. Despite the debt, the company maintains a substantial cash balance of approximately $1 billion, providing a cushion against short-term liquidity issues. However, the high level of debt relative to equity suggests a reliance on leverage, which could pose risks if revenue growth slows or interest rates rise. The increasing goodwill and intangible assets should be further investigated to ensure these valuations are appropriate.

5. Management & Governance

CEO Assessment: N/A

Capital Allocation: N/A

Insider Ownership: N/A

Governance Flags:

No major governance concerns flagged.

Based on the DCF model, the fair value per share is estimated to be $16.75. This is slightly higher than the current market price of $15.2, indicating a potential upside of approximately 10%. However, due to the sensitivity of DCF models to assumptions (especially growth rates and discount rate), the confidence level is medium. A downside case with slightly lower growth and a higher discount rate puts the valuation at ~14.50/share.

Scenarios

Scenario

Price Target

Key Assumptions

Bull

High

StubHub is poised for significant growth as the live event industry recovers and expands.

The company's dominant market position, strong brand recognition, and scalable platform will drive revenue and earnings growth, leading to substantial shareholder value creation.

Successful execution of international expansion and strategic partnerships will accelerate growth beyond current expectations. |

| Base | 16.75 | StubHub will continue to benefit from its leading position in the secondary ticketing market.

While growth may be slower than in the bull case, the company will generate consistent revenue and free cash flow, allowing for debt reduction and modest shareholder returns.

The base case assumes a continuation of current market trends and management's execution capabilities. |

| Bear | Low | StubHub's business could be negatively impacted by increased competition, economic headwinds, or regulatory challenges.

A decline in live event attendance, coupled with higher operating costs or legal liabilities, could lead to a significant decline in revenue and profitability, resulting in a substantial loss for investors. |

7. Risks

StubHub faces medium risk due to its high debt, fluctuating profitability, and significant intangible assets. While revenue is growing and free cash flow is positive, the company's financial health is susceptible to adverse economic conditions and market competition.

Significant fluctuations in net income and operating margins.

Large goodwill and intangible asset balances require scrutiny.

8. Conclusion

StubHub will continue to benefit from its leading position in the secondary ticketing market.

While growth may be slower than in the bull case, the company will generate consistent revenue and free cash flow, allowing for debt reduction and modest shareholder returns.

The base case assumes a continuation of current market trends and management's execution capabilities.

Investment research for informational purposes only. Not financial advice.

Continue Your Research

Return to the Analyst Library or explore the specific financial data for this entity on its profile.

Due to the recent unprofitability, Return on Invested Capital (ROIC) and Return on Equity (ROE) calculations are skewed and potentially misleading. While a precise calculation isn't directly feasible given the fluctuating net income, the negative net income in 2024 raises concerns about the company's efficient use of capital. Furthermore, a deeper dive into asset turnover and profit margins is warranted to understand the drivers behind the company's capital efficiency or lack thereof.

Due to the recent unprofitability, Return on Invested Capital (ROIC) and Return on Equity (ROE) calculations are skewed and potentially misleading. While a precise calculation isn't directly feasible given the fluctuating net income, the negative net income in 2024 raises concerns about the company's efficient use of capital. Furthermore, a deeper dive into asset turnover and profit margins is warranted to understand the drivers behind the company's capital efficiency or lack thereof. The company's free cash flow (FCF) generation shows a positive trend in 2023 and 2024, signaling improvement in cash management. The substantial capital expenditures (CAPEX) is relatively low compared to revenue, which is typical for a software company. Examine the investments in property, plant, and equipment to ensure they align with company growth strategies. The FCF trend needs to be sustained to support future growth and manage debt obligations.

The company's free cash flow (FCF) generation shows a positive trend in 2023 and 2024, signaling improvement in cash management. The substantial capital expenditures (CAPEX) is relatively low compared to revenue, which is typical for a software company. Examine the investments in property, plant, and equipment to ensure they align with company growth strategies. The FCF trend needs to be sustained to support future growth and manage debt obligations.