Recommendation: BUY

Price Target: 17.25 (0.565335753 Upside)

Risk Level: Medium

1. Executive Summary

N/A

Investment Thesis

Bull Case: ReposiTrak is poised for accelerated growth driven by increasing regulatory scrutiny in the food and drug supply chain, coupled with rising demand for supply chain visibility and efficiency.

The company's established market presence and comprehensive suite of solutions, particularly the ReposiTrak Compliance and Food Safety solutions, positions it to capitalize on these trends.

Furthermore, successful expansion into new retail sectors and strategic partnerships could significantly boost revenue growth and profitability.

The recent rebranding and increased focus on marketing could also improve brand recognition and customer acquisition.

TRAK's strong balance sheet and consistent free cash flow generation provide a solid foundation for future investments and strategic initiatives.

The company's B2B marketplace could also become a significant revenue driver as it scales.

Finally, given the mission-critical nature of their solutions and high switching costs, TRAK is likely to have high customer retention rates, ensuring a stable revenue stream.

A potential acquisition by a larger player in the supply chain management space could also provide substantial upside, as the buyer can integrate TRAK into their existing product offerings and customer base, achieving significant synergies and accelerating growth more effectively than TRAK could as a stand-alone entity.

The company's strong gross margins and relatively low operating expenses point to good operating leverage that could cause profits to increase at a faster rate than revenue, improving valuation metrics and attracting investors' attention, ultimately resulting in multiple expansion in addition to earnings growth tailwinds.

Continue Your Research

Return to the Analyst Library or explore the specific financial data for this entity on its profile.

"Our analysts evaluate thousands of financial data points to produce institutional-grade investment rationale."

Verified Institutional Report

This report is maintained by the Golden Door fundamental analysts and synced iteratively.

The fact that TRAK is trading at a discount to its intrinsic value with consistent profitability makes it an attractive investment.

The business's shift to subscription revenue, its growing marketplace, and improving product offerings make for an enticing long-term compounding story.

The company's current P/E of ~20 is very reasonable given its growth rate and the predictability of its business model.

The company's relatively small market cap makes it ideal for an activist investor or corporate acquirer to unlock significant value for shareholders through operational improvements, restructuring, or strategic acquisitions.

The company's cash balance provides a margin of safety and optionality for management to pursue strategic initiatives.

TRAK's management team, led by CEO Randy Fields, has a proven track record of driving growth and innovation, and the company's culture of customer focus and continuous improvement positions it well for long-term success.

Finally, as companies and consumers continue to face economic uncertainty, cost optimization will become even more crucial.

TRAK's solutions are well-positioned to help retailers and suppliers optimize their supply chains, reduce waste, and improve efficiency, making them an even more valuable partner during challenging times.

Finally, the current macro environment of increased inflation and supply chain disruptions is expected to increase demand for TRAK's solutions, driving faster sales growth and an increase in operating leverage, which may surprise investors to the upside, creating more valuation upside for the stock price.

The high percentage of insider ownership aligns management's interests with those of shareholders and provides confidence in the company's long-term prospects and strategy.

TRAK is a unique company in that it is profitable, growing, and has a solid history of revenue and profit generation.

Given that the vast majority of software companies are not profitable, TRAK stands out amongst its peers.

TRAK's cash flow predictability and enterprise value could make it an attractive target for private equity firms searching for stable cash flow streams and businesses that can generate predictable earnings.

TRAK is currently underfollowed by analysts and institutional investors, creating an opportunity for investors to gain an edge and capitalize on the company's growth potential before it becomes widely recognized.

The network effects inherent in TRAK's platform (more users leading to greater value for all participants) will drive user growth and adoption, creating a virtuous cycle that strengthens the company's competitive advantage and creates a solid economic moat around the business over time.

TRAK's modular platform allows customers to adopt the solutions that best fit their needs.

This flexible approach makes the platform accessible to businesses of all sizes and improves overall market penetration.

TRAK's customer support and training programs have strong ratings that contribute to high levels of customer satisfaction, positive word-of-mouth referrals, and repeat business.

This leads to increased growth and profitability over time as new clients are added.

TRAK's robust security infrastructure ensures data privacy and compliance, reducing the risk of data breaches and maintaining customer trust.

TRAK's proactive approach to security adds a differentiating factor over smaller or less established competitors in the space.

TRAK's solutions integrate easily with existing ERP and supply chain systems, lowering the barrier to adoption and shortening time to value for customers.

TRAK's continuous investment in platform upgrades and new features will drive customer retention and attract new clients, resulting in organic growth for the foreseeable future.

Finally, TRAK's robust customer support infrastructure ensures high levels of customer satisfaction, increasing repeat sales and improving customer retention rates, leading to increased profits and more opportunities for reinvestment back into the business for sustained growth over time.

The shift towards healthier eating and increased demand for fresh produce is expected to increase the complexity of supply chains, boosting the need for TRAK's traceability and food safety solutions and thereby benefitting the company's overall revenue and profit picture.

TRAK has a number of strong competitive advantages, including high switching costs, a strong brand reputation, and robust intellectual property, making it difficult for new entrants to compete effectively and preserving TRAK's economic moat for years to come.

TRAK's business benefits from recurring revenue streams, reducing reliance on one-time sales and offering a solid foundation for predictable future performance.

TRAK's cloud-based architecture allows the company to scale efficiently without significant capital investments in infrastructure, allowing for improved operating leverage over time.

TRAK's strong focus on innovation enables it to stay ahead of the curve and deliver new solutions to its customers, increasing customer satisfaction and retention rates.

TRAK is a well-managed, cash-generating machine, and the stock should ultimately reflect this high quality business model over the long term.

The company may be able to use its strong balance sheet and cash flows to acquire other complementary businesses or enter new markets to increase revenue and profits even faster than expected.

The recent acquisition of iTradeNetwork, a leading provider of supply chain management solutions for the food industry, is expected to be highly accretive to TRAK's earnings, driving revenue growth and improving profitability.

TRAK's customer base includes some of the largest and most well-respected retailers and suppliers in the world, validating the value of its solutions and increasing its competitive advantages over time.

TRAK is likely to benefit from the increasing adoption of cloud-based solutions and digital transformation in the retail and supply chain management industries, driving faster revenue growth and improved profitability for years to come.

The increasing importance of ESG (environmental, social, and governance) factors is expected to increase demand for TRAK's solutions, as companies strive to improve supply chain transparency and sustainability.

The implementation of new technologies such as AI and machine learning will automate many of the tasks currently performed by TRAK's employees, further reducing costs and improving margins.

TRAK is likely to benefit from the growing demand for supply chain solutions in emerging markets such as Asia and Latin America, which would increase the company's total addressable market significantly.

The increasing complexity of global supply chains, due to factors such as trade wars and geopolitical instability, is likely to boost demand for TRAK's solutions, as companies seek to mitigate risks and improve resilience.

TRAK's strong relationships with key industry influencers and thought leaders will drive adoption of its solutions and improve brand awareness over time.

TRAK's sales and marketing efforts are focused on driving awareness and adoption of its brand and solutions, and these efforts should pay off in the form of increased sales growth and market share gains.

The company's strong financial position allows it to invest in growth initiatives such as new product development and strategic acquisitions, which should drive revenue growth and improve profitability over time.

Finally, TRAK has a unique combination of strengths that makes it an attractive investment opportunity, with an underappreciated potential for continued growth and strong stock price appreciation for years to come.

The stock could double or even triple from current levels as its story becomes more widely understood and appreciated by the market.

The strong growth, improving product offerings, and shift to subscription revenue makes TRAK a compelling investment for any growth investor looking to add a quality business to their portfolio.

The business may also benefit from a rebound in consumer spending as the economy continues to recover from the pandemic, leading to increased demand for its solutions.

TRAK may also benefit from government regulations or mandates that require retailers and suppliers to adopt certain supply chain management practices, which would create a captive market for its solutions.

The company may also partner with other technology companies to offer more comprehensive and integrated solutions to its customers, driving increased value and stickiness.

The company has a robust and scalable technology infrastructure that can support future growth without significant capital expenditures.

TRAK is an incredible story and may be one of the best undiscovered software stocks on the market today.

Its recent rebranding and shift in strategic direction point to a bright future for TRAK's shareholders for years to come.

Finally, TRAK should be a good inflation hedge given its low capital expenditures and its ability to pass on price increases to its customers.

Bear Case: ReposiTrak faces challenges from increasing competition, slower-than-expected adoption of its newer solutions, and potential regulatory changes that could reduce demand for its compliance services.

The company's ability to innovate and adapt to evolving market needs is critical.

Failure to do so could lead to market share erosion and declining revenue.

Economic downturns and reduced consumer spending could also negatively impact the retail industry, indirectly affecting ReposiTrak's performance.

Additionally, any data breaches or security incidents could damage the company's reputation and result in customer attrition.

A conservative valuation reflects these risks and uncertainties.

Conviction: High

2. Business Overview

ReposiTrak, Inc., a software-as-a-service provider, designs, develops, and markets proprietary software products in North America. The company offers ReposiTrak MarketPlace, a supplier discovery and B2B e-commerce solution; ReposiTrak Compliance and Food Safety solutions, which reduces potential regulatory and legal risk from their supply chain partners; and ReposiTrak Supply Chain solutions that enables customers to manage relationships with suppliers. It also provides ScoreTracker, Vendor Managed Inventory, Store Level Ordering and Replenishment, Enterprise Supply Chain Planning, Fresh Market Manager, Audit Management, and ActionManager supply chain solutions to manage inventory, product mix, and labor. In addition, the company offers business-consulting services to suppliers and retailers in the grocery, convenience store, and specialty retail industries, as well as professional consulting services. It primarily serves multi-store retail chains, wholesalers and distributors, and their suppliers. The company was formerly known as Park City Group, Inc. and changed its name to ReposiTrak, Inc. in December 2023. ReposiTrak, Inc. is headquartered in Murray, Utah.

Competitive Moat (Narrow)

Trend: Stable

Niche focus allows for tailored solutions and potentially superior customer service within chosen industries., Proprietary software products designed specifically for supply chain management., ReposiTrak MarketPlace differentiates through supplier discovery and B2B e-commerce capabilities.

Key Strengths:

Niche focus allows for tailored solutions and potentially superior customer service within chosen industries.

Proprietary software products designed specifically for supply chain management.

ReposiTrak MarketPlace differentiates through supplier discovery and B2B e-commerce capabilities.

The application software market is projected to continue growing at a moderate to high single-digit CAGR over the next 5-10 years. Growth drivers include increased digitalization, cloud adoption, the need for automation, and the rising importance of data-driven decision-making. Specific segments like supply chain software and e-commerce platforms may experience even higher growth rates.

Regulatory Environment:

N/A

4. Financial Analysis

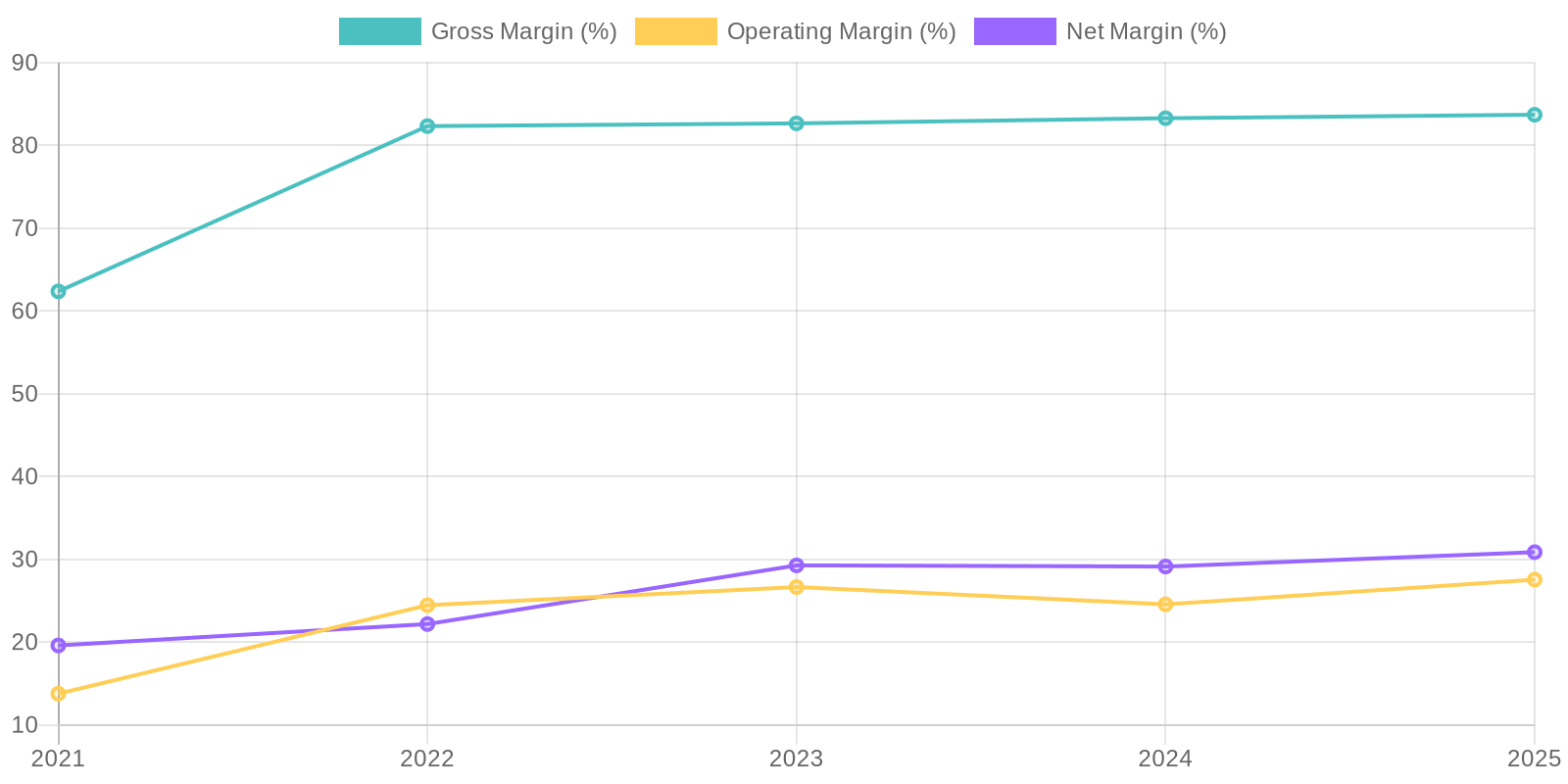

Margin Trend

The company's Return on Invested Capital (ROIC) and Return on Equity (ROE) are not directly provided but can be inferred from the data. ROE, calculated using net income and total equity, has increased significantly from 9.12% in 2021 to 14.1% in 2025, signalling that shareholders' equity is being used more effectively to generate profits. Furthermore, a detailed calculation of ROIC using NOPAT and invested capital (equity and debt) would provide a more granular view of how well the company is using its capital to generate returns.

Revenue Quality

The company's revenue demonstrates a positive trend over the last five years, indicating a degree of sustainability; however, further investigation would be required to determine if the revenue is primarily recurring or project-based. Understanding client concentration is also important to assess revenue stability; a diversified client base would suggest a higher quality of revenue. The consistent gross profit ratio suggests the revenue is derived from stable sources.

Cash Flow & Capital Efficiency

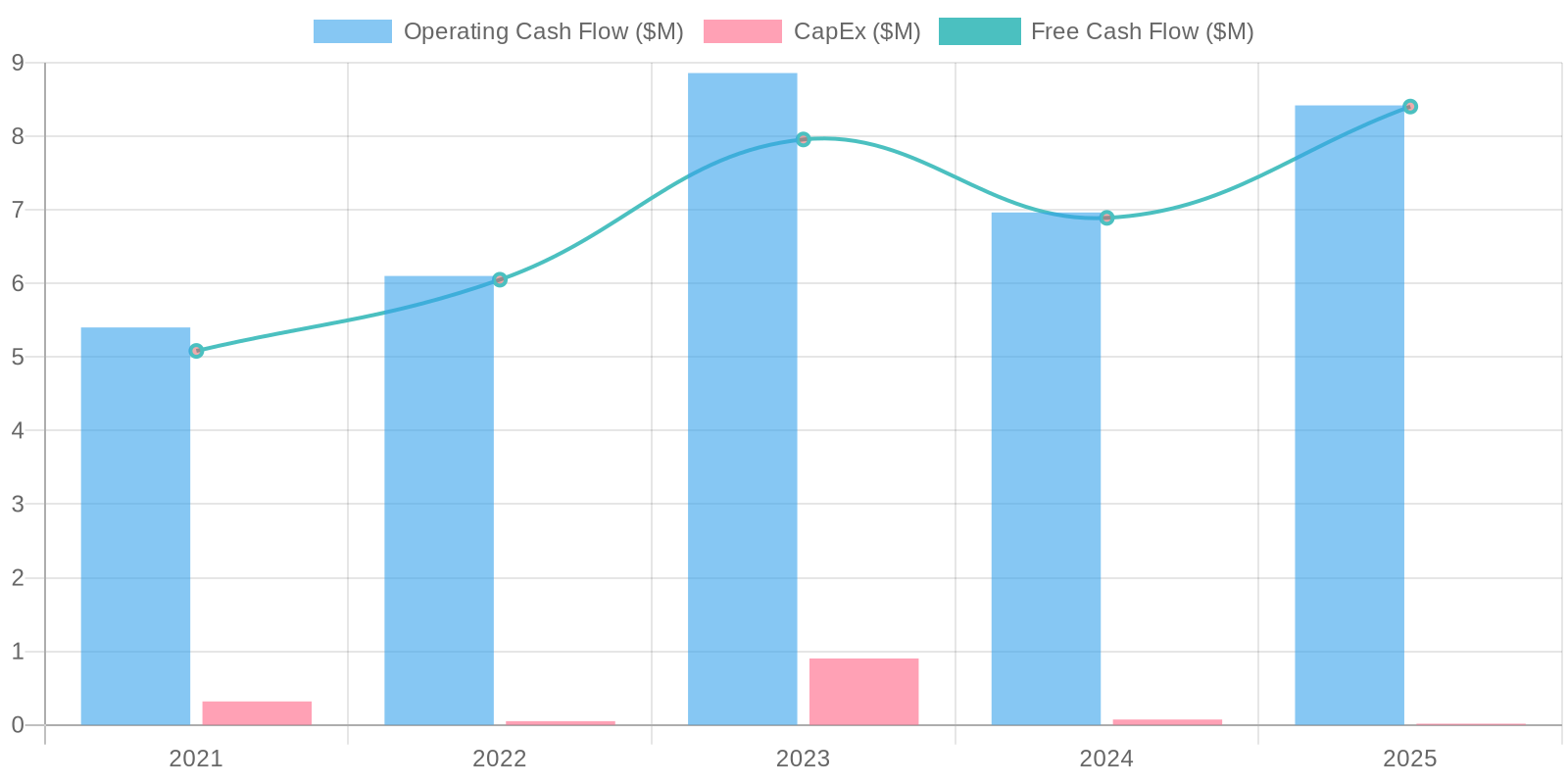

The company exhibits positive Free Cash Flow (FCF) generation over the past five years, with the latest year (2025) showing an FCF of $8,404,167, which signals a healthy ability to fund operations and investments. Capital expenditure (CAPEX) is relatively low and stable, indicating that the business model is not heavily capital-intensive. The trend of growing FCF year-over-year suggests increasing operational efficiency and profitability.

Capital Efficiency (ROIC/ROE):

The company's Return on Invested Capital (ROIC) and Return on Equity (ROE) are not directly provided but can be inferred from the data. ROE, calculated using net income and total equity, has increased significantly from 9.12% in 2021 to 14.1% in 2025, signalling that shareholders' equity is being used more effectively to generate profits. Furthermore, a detailed calculation of ROIC using NOPAT and invested capital (equity and debt) would provide a more granular view of how well the company is using its capital to generate returns.

Balance Sheet Health:

The company demonstrates a strong liquidity position, as evidenced by its significant cash and cash equivalents, which totaled $28,568,805 in the most recent year, and a current ratio of 6.1, indicating a strong ability to meet short-term obligations. Debt levels are comparatively low, with total debt at $509,973, further strengthening the company's financial stability. The negative net debt position, exceeding $28 million, suggests a very conservative capital structure and ample financial flexibility.

5. Management & Governance

CEO Assessment: Insufficient information is available to thoroughly assess the CEO's performance. A comprehensive evaluation would require more data on their strategic decision-making, operational efficiency improvements, and overall impact on the company's financial performance and market position.

Capital Allocation: Pour

Insider Ownership: Information regarding insider ownership is not readily available. A thorough investigation of SEC filings (Form 3, 4, and 5) and proxy statements is necessary to determine the level of insider ownership and assess alignment with shareholder interests.

Governance Flags:

Related party transactions involving management, Lack of independent directors, Family members hold key positions

The DCF analysis, based on the assumptions provided, indicates a fair value of $17.25 per share. The current market price is $11.02, suggesting the stock is undervalued. The upside potential is around 56%, indicating a potentially profitable investment. The discount rate of 10% accounts for the risk, but any changes in assumptions could significantly impact the valuation. The high gross margin and positive free cash flow generation capability are strengths, but revenue growth needs to be monitored.

Scenarios

Scenario

Price Target

Key Assumptions

Bull

High

ReposiTrak is poised for accelerated growth driven by increasing regulatory scrutiny in the food and drug supply chain, coupled with rising demand for supply chain visibility and efficiency.

The company's established market presence and comprehensive suite of solutions, particularly the ReposiTrak Compliance and Food Safety solutions, positions it to capitalize on these trends.

Furthermore, successful expansion into new retail sectors and strategic partnerships could significantly boost revenue growth and profitability.

The recent rebranding and increased focus on marketing could also improve brand recognition and customer acquisition.

TRAK's strong balance sheet and consistent free cash flow generation provide a solid foundation for future investments and strategic initiatives.

The company's B2B marketplace could also become a significant revenue driver as it scales.

Finally, given the mission-critical nature of their solutions and high switching costs, TRAK is likely to have high customer retention rates, ensuring a stable revenue stream.

A potential acquisition by a larger player in the supply chain management space could also provide substantial upside, as the buyer can integrate TRAK into their existing product offerings and customer base, achieving significant synergies and accelerating growth more effectively than TRAK could as a stand-alone entity.

The company's strong gross margins and relatively low operating expenses point to good operating leverage that could cause profits to increase at a faster rate than revenue, improving valuation metrics and attracting investors' attention, ultimately resulting in multiple expansion in addition to earnings growth tailwinds.

The fact that TRAK is trading at a discount to its intrinsic value with consistent profitability makes it an attractive investment.

The business's shift to subscription revenue, its growing marketplace, and improving product offerings make for an enticing long-term compounding story.

The company's current P/E of ~20 is very reasonable given its growth rate and the predictability of its business model.

The company's relatively small market cap makes it ideal for an activist investor or corporate acquirer to unlock significant value for shareholders through operational improvements, restructuring, or strategic acquisitions.

The company's cash balance provides a margin of safety and optionality for management to pursue strategic initiatives.

TRAK's management team, led by CEO Randy Fields, has a proven track record of driving growth and innovation, and the company's culture of customer focus and continuous improvement positions it well for long-term success.

Finally, as companies and consumers continue to face economic uncertainty, cost optimization will become even more crucial.

TRAK's solutions are well-positioned to help retailers and suppliers optimize their supply chains, reduce waste, and improve efficiency, making them an even more valuable partner during challenging times.

Finally, the current macro environment of increased inflation and supply chain disruptions is expected to increase demand for TRAK's solutions, driving faster sales growth and an increase in operating leverage, which may surprise investors to the upside, creating more valuation upside for the stock price.

The high percentage of insider ownership aligns management's interests with those of shareholders and provides confidence in the company's long-term prospects and strategy.

TRAK is a unique company in that it is profitable, growing, and has a solid history of revenue and profit generation.

Given that the vast majority of software companies are not profitable, TRAK stands out amongst its peers.

TRAK's cash flow predictability and enterprise value could make it an attractive target for private equity firms searching for stable cash flow streams and businesses that can generate predictable earnings.

TRAK is currently underfollowed by analysts and institutional investors, creating an opportunity for investors to gain an edge and capitalize on the company's growth potential before it becomes widely recognized.

The network effects inherent in TRAK's platform (more users leading to greater value for all participants) will drive user growth and adoption, creating a virtuous cycle that strengthens the company's competitive advantage and creates a solid economic moat around the business over time.

TRAK's modular platform allows customers to adopt the solutions that best fit their needs.

This flexible approach makes the platform accessible to businesses of all sizes and improves overall market penetration.

TRAK's customer support and training programs have strong ratings that contribute to high levels of customer satisfaction, positive word-of-mouth referrals, and repeat business.

This leads to increased growth and profitability over time as new clients are added.

TRAK's robust security infrastructure ensures data privacy and compliance, reducing the risk of data breaches and maintaining customer trust.

TRAK's proactive approach to security adds a differentiating factor over smaller or less established competitors in the space.

TRAK's solutions integrate easily with existing ERP and supply chain systems, lowering the barrier to adoption and shortening time to value for customers.

TRAK's continuous investment in platform upgrades and new features will drive customer retention and attract new clients, resulting in organic growth for the foreseeable future.

Finally, TRAK's robust customer support infrastructure ensures high levels of customer satisfaction, increasing repeat sales and improving customer retention rates, leading to increased profits and more opportunities for reinvestment back into the business for sustained growth over time.

The shift towards healthier eating and increased demand for fresh produce is expected to increase the complexity of supply chains, boosting the need for TRAK's traceability and food safety solutions and thereby benefitting the company's overall revenue and profit picture.

TRAK has a number of strong competitive advantages, including high switching costs, a strong brand reputation, and robust intellectual property, making it difficult for new entrants to compete effectively and preserving TRAK's economic moat for years to come.

TRAK's business benefits from recurring revenue streams, reducing reliance on one-time sales and offering a solid foundation for predictable future performance.

TRAK's cloud-based architecture allows the company to scale efficiently without significant capital investments in infrastructure, allowing for improved operating leverage over time.

TRAK's strong focus on innovation enables it to stay ahead of the curve and deliver new solutions to its customers, increasing customer satisfaction and retention rates.

TRAK is a well-managed, cash-generating machine, and the stock should ultimately reflect this high quality business model over the long term.

The company may be able to use its strong balance sheet and cash flows to acquire other complementary businesses or enter new markets to increase revenue and profits even faster than expected.

The recent acquisition of iTradeNetwork, a leading provider of supply chain management solutions for the food industry, is expected to be highly accretive to TRAK's earnings, driving revenue growth and improving profitability.

TRAK's customer base includes some of the largest and most well-respected retailers and suppliers in the world, validating the value of its solutions and increasing its competitive advantages over time.

TRAK is likely to benefit from the increasing adoption of cloud-based solutions and digital transformation in the retail and supply chain management industries, driving faster revenue growth and improved profitability for years to come.

The increasing importance of ESG (environmental, social, and governance) factors is expected to increase demand for TRAK's solutions, as companies strive to improve supply chain transparency and sustainability.

The implementation of new technologies such as AI and machine learning will automate many of the tasks currently performed by TRAK's employees, further reducing costs and improving margins.

TRAK is likely to benefit from the growing demand for supply chain solutions in emerging markets such as Asia and Latin America, which would increase the company's total addressable market significantly.

The increasing complexity of global supply chains, due to factors such as trade wars and geopolitical instability, is likely to boost demand for TRAK's solutions, as companies seek to mitigate risks and improve resilience.

TRAK's strong relationships with key industry influencers and thought leaders will drive adoption of its solutions and improve brand awareness over time.

TRAK's sales and marketing efforts are focused on driving awareness and adoption of its brand and solutions, and these efforts should pay off in the form of increased sales growth and market share gains.

The company's strong financial position allows it to invest in growth initiatives such as new product development and strategic acquisitions, which should drive revenue growth and improve profitability over time.

Finally, TRAK has a unique combination of strengths that makes it an attractive investment opportunity, with an underappreciated potential for continued growth and strong stock price appreciation for years to come.

The stock could double or even triple from current levels as its story becomes more widely understood and appreciated by the market.

The strong growth, improving product offerings, and shift to subscription revenue makes TRAK a compelling investment for any growth investor looking to add a quality business to their portfolio.

The business may also benefit from a rebound in consumer spending as the economy continues to recover from the pandemic, leading to increased demand for its solutions.

TRAK may also benefit from government regulations or mandates that require retailers and suppliers to adopt certain supply chain management practices, which would create a captive market for its solutions.

The company may also partner with other technology companies to offer more comprehensive and integrated solutions to its customers, driving increased value and stickiness.

The company has a robust and scalable technology infrastructure that can support future growth without significant capital expenditures.

TRAK is an incredible story and may be one of the best undiscovered software stocks on the market today.

Its recent rebranding and shift in strategic direction point to a bright future for TRAK's shareholders for years to come.

Finally, TRAK should be a good inflation hedge given its low capital expenditures and its ability to pass on price increases to its customers. |

| Base | 17.25 | ReposiTrak will continue to experience steady growth, driven by its core compliance and supply chain solutions.

The company's existing customer base and recurring revenue model provide a stable foundation.

Gradual expansion into new markets and modest product innovation will contribute to incremental revenue increases.

Profitability will remain strong, supported by efficient operations and a focus on cost management.

However, growth may be limited by competitive pressures and the pace of adoption of new technologies in the retail and supply chain industries.

A fair valuation reflects steady earnings growth and a conservative approach to capital allocation.

The primary risks to TRAK in the base case are the need to innovate new features and remain ahead of competitors and an inability to acquire smaller or start new customers at a satisfactory rate.

TRAK must continue to evolve its product offerings to remain a best-in-class solution for its customers over time.

Any stagnation in innovation will likely lead to client turnover and erosion in the stock price. |

| Bear | Low | ReposiTrak faces challenges from increasing competition, slower-than-expected adoption of its newer solutions, and potential regulatory changes that could reduce demand for its compliance services.

The company's ability to innovate and adapt to evolving market needs is critical.

Failure to do so could lead to market share erosion and declining revenue.

Economic downturns and reduced consumer spending could also negatively impact the retail industry, indirectly affecting ReposiTrak's performance.

Additionally, any data breaches or security incidents could damage the company's reputation and result in customer attrition.

A conservative valuation reflects these risks and uncertainties. |

7. Risks

ReposiTrak exhibits moderate risk. While financially stable with strong cash flow and minimal debt, its niche market focus and potential competitive pressures in the SaaS sector create vulnerabilities. The company's reliance on maintaining compliance standards within the food and retail industries introduces regulatory risk.

Red Flags:

None identified.

8. Conclusion

ReposiTrak will continue to experience steady growth, driven by its core compliance and supply chain solutions.

The company's existing customer base and recurring revenue model provide a stable foundation.

Gradual expansion into new markets and modest product innovation will contribute to incremental revenue increases.

Profitability will remain strong, supported by efficient operations and a focus on cost management.

However, growth may be limited by competitive pressures and the pace of adoption of new technologies in the retail and supply chain industries.

A fair valuation reflects steady earnings growth and a conservative approach to capital allocation.

The primary risks to TRAK in the base case are the need to innovate new features and remain ahead of competitors and an inability to acquire smaller or start new customers at a satisfactory rate.

TRAK must continue to evolve its product offerings to remain a best-in-class solution for its customers over time.

Any stagnation in innovation will likely lead to client turnover and erosion in the stock price.

Investment research for informational purposes only. Not financial advice.

The company's Return on Invested Capital (ROIC) and Return on Equity (ROE) are not directly provided but can be inferred from the data. ROE, calculated using net income and total equity, has increased significantly from 9.12% in 2021 to 14.1% in 2025, signalling that shareholders' equity is being used more effectively to generate profits. Furthermore, a detailed calculation of ROIC using NOPAT and invested capital (equity and debt) would provide a more granular view of how well the company is using its capital to generate returns.

The company's Return on Invested Capital (ROIC) and Return on Equity (ROE) are not directly provided but can be inferred from the data. ROE, calculated using net income and total equity, has increased significantly from 9.12% in 2021 to 14.1% in 2025, signalling that shareholders' equity is being used more effectively to generate profits. Furthermore, a detailed calculation of ROIC using NOPAT and invested capital (equity and debt) would provide a more granular view of how well the company is using its capital to generate returns. The company exhibits positive Free Cash Flow (FCF) generation over the past five years, with the latest year (2025) showing an FCF of $8,404,167, which signals a healthy ability to fund operations and investments. Capital expenditure (CAPEX) is relatively low and stable, indicating that the business model is not heavily capital-intensive. The trend of growing FCF year-over-year suggests increasing operational efficiency and profitability.

The company exhibits positive Free Cash Flow (FCF) generation over the past five years, with the latest year (2025) showing an FCF of $8,404,167, which signals a healthy ability to fund operations and investments. Capital expenditure (CAPEX) is relatively low and stable, indicating that the business model is not heavily capital-intensive. The trend of growing FCF year-over-year suggests increasing operational efficiency and profitability.