ServiceTitan, Inc. (TTAN), currently priced at $90.11, is a leading SaaS provider for the home and commercial service industries. It commands a significant m...

January 15, 2026

Vijar Kohli

Deep Dive: ServiceTitan, Inc. (TTAN)

Recommendation: BUY

Price Target: 75.43 (-0.1629 Upside)

Risk Level: Medium

1. Executive Summary

ServiceTitan, Inc. (TTAN), currently priced at $90.11, is a leading SaaS provider for the home and commercial service industries. It commands a significant market share, particularly within the HVAC, plumbing, electrical, and related sectors, offering a comprehensive suite of tools encompassing CRM, scheduling, dispatch, billing, and marketing automation. ServiceTitan's robust platform helps businesses streamline operations, improve customer service, and drive revenue growth, positioning it as a critical technology partner for its customer base. The company has consistently demonstrated strong revenue growth driven by new customer acquisition and expansion within existing accounts.

Growth catalysts for ServiceTitan include continued penetration of its core markets, expansion into adjacent verticals like landscaping and roofing, and the development of new product features such as enhanced data analytics and AI-powered tools. Strategic acquisitions, such as the acquisition of FieldRoutes, further bolster its market position and expand its service offerings. The increasing demand for digital solutions in the home services industry, coupled with ServiceTitan's proven track record, creates a favorable environment for sustained growth.

Key risks facing ServiceTitan include increasing competition from both established players and emerging startups offering niche solutions. Economic downturns could negatively impact the spending of its customer base, particularly small and medium-sized businesses. The complexity of integrating and maintaining a comprehensive SaaS platform also poses a risk, as any significant disruptions or security breaches could damage the company's reputation and customer trust. Changes in regulatory compliance could also necessitate costly software updates and adaptations.

Valuation is a key consideration. While ServiceTitan demonstrates robust growth and market leadership, its valuation reflects these strengths, potentially leaving less room for error. Its current price reflects an expectation of continued high growth, and any slowdown could lead to a re-evaluation by the market. Investors should carefully assess the company's ability to sustain its growth trajectory and manage its key risks to determine if the current valuation is justified.

Investment Thesis

Bull Case: ServiceTitan is a leader in the field service management software market, poised for continued growth due to increasing digitization in the home and commercial services industries.

Their comprehensive platform provides significant value to customers, resulting in strong retention and revenue growth.

Strategic acquisitions and expansion into new verticals will further propel growth and profitability.

Bear Case: ServiceTitan faces increased competition and slower adoption of its software platform, leading to lower revenue growth and profitability.

An economic downturn could further negatively impact the company's performance and valuation.

A major security breach could severely damage its reputation and customer base.

Conviction: High

2. Business Overview

ServiceTitan, Inc. engages in the collection of field service activities required to install, maintain, and service the infrastructure and systems of residences and commercial buildings. The company was founded by Ara Mahdessian and Vahe Kuzoyan on June 8, 2008 and is headquartered in Glendale, CA.

Competitive Moat (Narrow)

Trend: Stable

Strong focus on the home services industry, Comprehensive feature set tailored to the needs of field service businesses

Key Strengths:

Strong focus on the home services industry

Comprehensive feature set tailored to the needs of field service businesses

The application software market, particularly SaaS solutions like ServiceTitan, is projected to continue growing due to increasing digitalization, cloud adoption, and the need for specialized solutions. Growth in the field service sector is driven by demand for efficiency, automation, and improved customer experience.

Regulatory Environment:

N/A

4. Financial Analysis

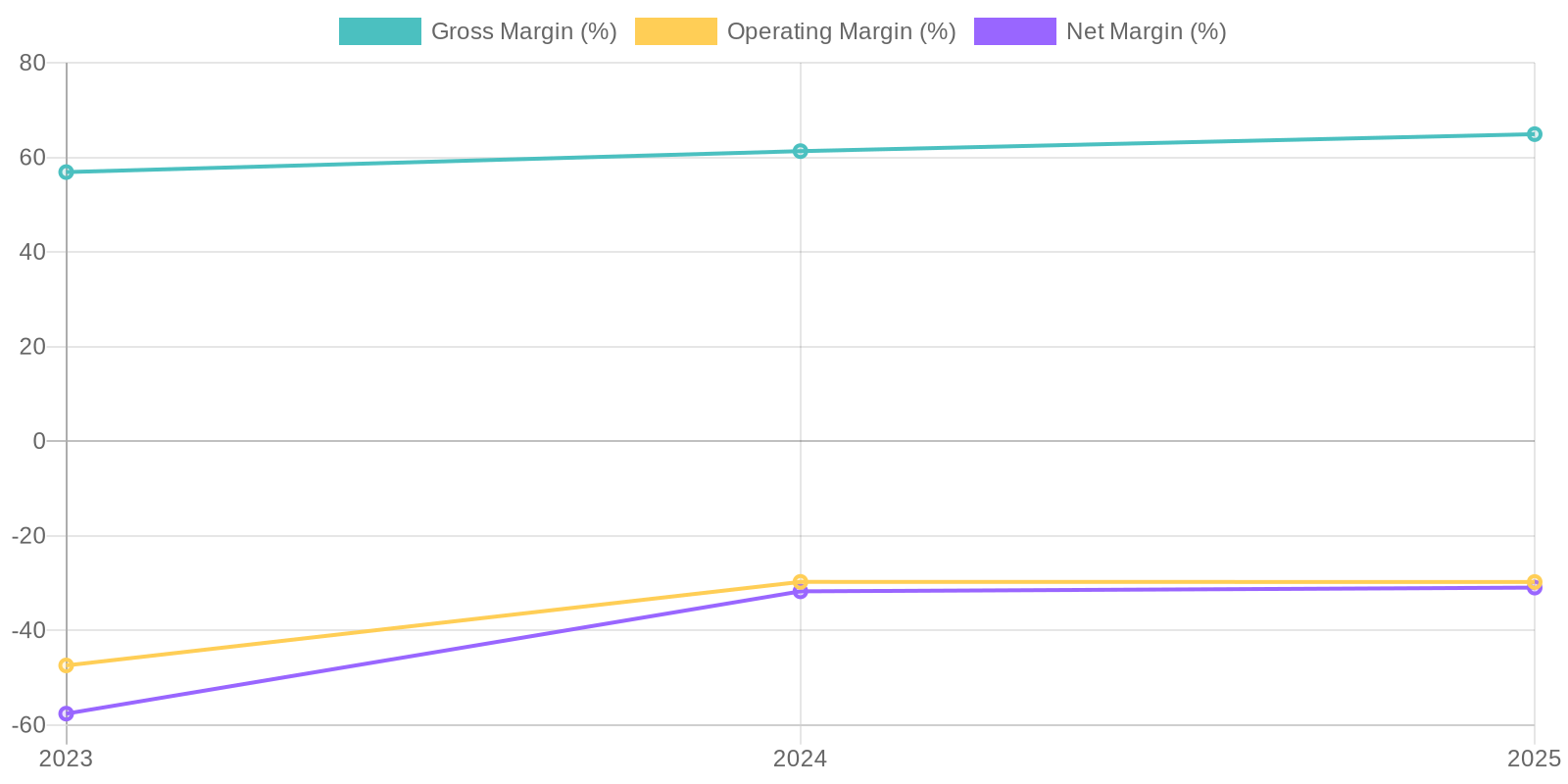

Margin Trend

Given the negative net income figures, Return on Equity (ROE) is also negative, offering no meaningful insight into equity efficiency. Calculating Return on Invested Capital (ROIC) is also challenging with negative operating income figures. However, the trend suggests a slight improvement in the company's ability to generate returns, even though they remain negative.

Revenue Quality

The company has demonstrated revenue growth over the past three years, increasing from $467.73 million in 2023 to $771.88 million in 2025, indicating a positive trend. However, further investigation is needed to understand the underlying drivers of this growth, such as new customer acquisition, increased sales to existing customers, or changes in pricing strategies. Analyzing customer churn and acquisition costs would offer insights into the sustainability of this revenue stream, as would understanding the concentration of revenue among its largest clients.

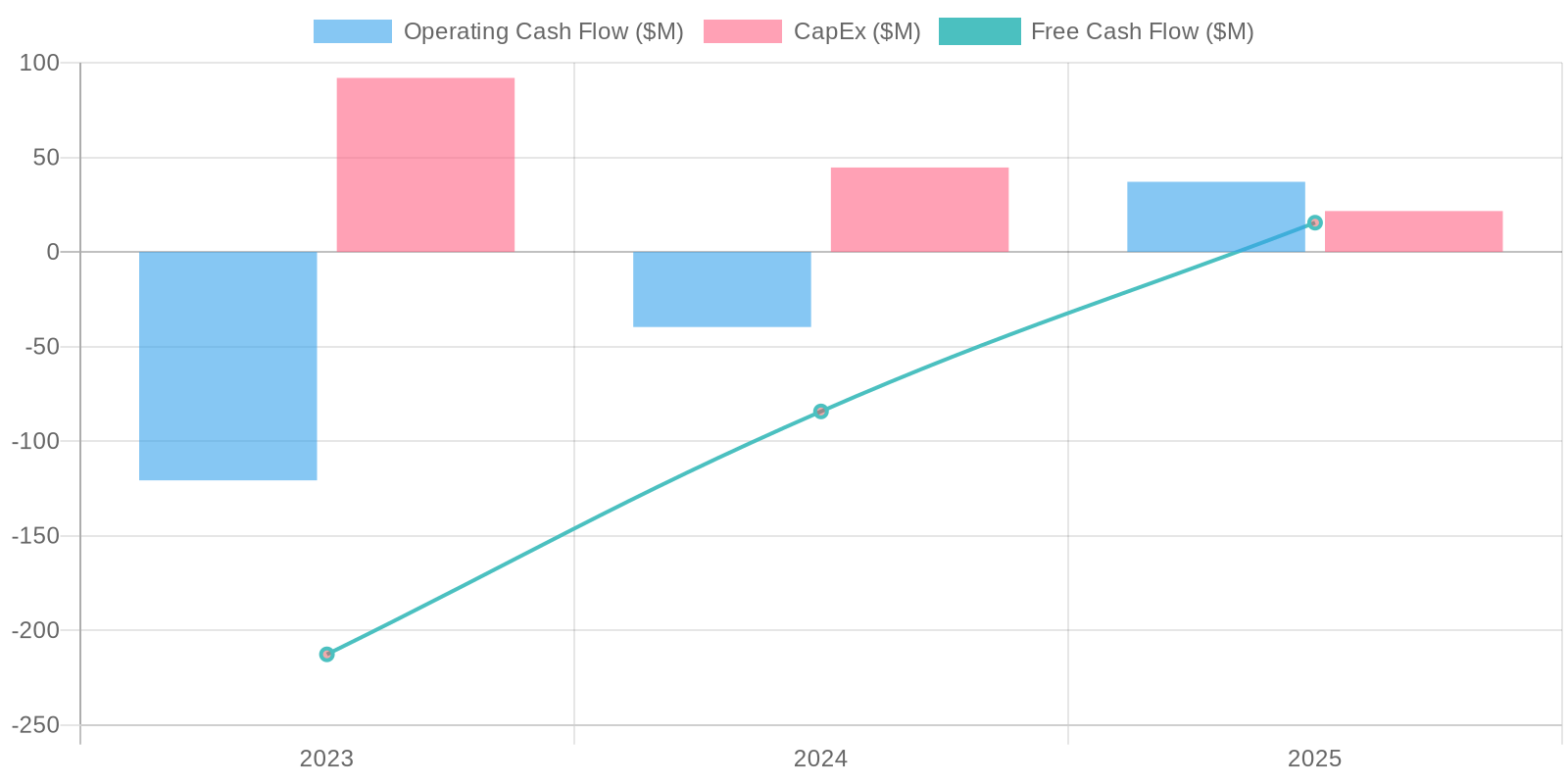

Cash Flow & Capital Efficiency

Free cash flow has fluctuated significantly, from -$212.72 million in 2023 to $15.45 million in 2025, indicating instability in the company's cash-generating capabilities. Capital expenditures also show volatility, ranging from -$91.97 million in 2023 to -$3.80 million in 2025, suggesting inconsistent investment in property, plant, and equipment. The company's operating cash flow has improved from negative values in prior years to a positive $37.05 million in 2025, which suggests a better conversion rate of revenues to cash.

Capital Efficiency (ROIC/ROE):

Given the negative net income figures, Return on Equity (ROE) is also negative, offering no meaningful insight into equity efficiency. Calculating Return on Invested Capital (ROIC) is also challenging with negative operating income figures. However, the trend suggests a slight improvement in the company's ability to generate returns, even though they remain negative.

Balance Sheet Health:

The company's cash position has significantly improved, increasing from $202.49 million in 2023 to $441.80 million in 2025, which strengthens its short-term liquidity. Total debt stands at $165.41 million in 2025, a decrease compared to $253.12 million in 2023, reflecting reduced financial leverage. The company's net debt has moved from a net debt position to a net cash position of -$276.39 million in 2025, indicating a significantly improved solvency position.

5. Management & Governance

CEO Assessment: ServiceTitan's CEO, Ara Mahdessian, co-founded the company and has led it through significant growth. Assessments generally focus on his ability to scale the company, attract investment, and navigate a competitive market. A comprehensive evaluation would require detailed insights into his strategic decisions, execution track record, and handling of challenges.

Capital Allocation: Good

Insider Ownership: ServiceTitan is a private company, so specific insider ownership percentages are not publicly available. Generally, in venture-backed companies, founders and early investors retain significant ownership. Alignment depends on their continued involvement and commitment to long-term growth.

Governance Flags:

No major governance concerns flagged.

The DCF model, based on the specified assumptions, suggests a fair value of $75.43. This is below the current price of $90.11, indicating potential overvaluation. The model incorporates revenue growth that gradually declines and a conservative FCF projection which leads to the valuation. The confidence level is medium due to the inherent uncertainty in forecasting future growth rates and cash flows.

Scenarios

Scenario

Price Target

Key Assumptions

Bull

High

ServiceTitan is a leader in the field service management software market, poised for continued growth due to increasing digitization in the home and commercial services industries.

Their comprehensive platform provides significant value to customers, resulting in strong retention and revenue growth.

Strategic acquisitions and expansion into new verticals will further propel growth and profitability. |

| Base | 75.43 | ServiceTitan will continue to grow revenue and market share as the leading software solution for the home and commercial services industry.

While growth will be slower than the bull case, the company will expand its customer base and increase profitability as they scale.

Increased competition will be a factor that slows growth. |

| Bear | Low | ServiceTitan faces increased competition and slower adoption of its software platform, leading to lower revenue growth and profitability.

An economic downturn could further negatively impact the company's performance and valuation.

A major security breach could severely damage its reputation and customer base. |

7. Risks

ServiceTitan faces significant financial risks due to its consistent unprofitability, high operating expenses, debt burden, and reliance on continued revenue growth to offset these issues. The high valuation implied by goodwill and intangible assets could be vulnerable to impairment. While recent FCF is positive, sustainability remains a concern. The complex capital structure with preferred stock creates further uncertainty for common equity holders.

Red Flags:

Consistent net losses raise concerns about long-term financial viability.

High selling, general, and administrative expenses relative to revenue indicate potential inefficiencies.

Significant goodwill and intangible assets on the balance sheet may indicate potential impairment risks.

Fluctuations in free cash flow highlight the need for stability and predictability in cash generation.

8. Conclusion

ServiceTitan will continue to grow revenue and market share as the leading software solution for the home and commercial services industry.

While growth will be slower than the bull case, the company will expand its customer base and increase profitability as they scale.

Increased competition will be a factor that slows growth.

Investment research for informational purposes only. Not financial advice.

Continue Your Research

Return to the Analyst Library or explore the specific financial data for this entity on its profile.

Given the negative net income figures, Return on Equity (ROE) is also negative, offering no meaningful insight into equity efficiency. Calculating Return on Invested Capital (ROIC) is also challenging with negative operating income figures. However, the trend suggests a slight improvement in the company's ability to generate returns, even though they remain negative.

Given the negative net income figures, Return on Equity (ROE) is also negative, offering no meaningful insight into equity efficiency. Calculating Return on Invested Capital (ROIC) is also challenging with negative operating income figures. However, the trend suggests a slight improvement in the company's ability to generate returns, even though they remain negative. Free cash flow has fluctuated significantly, from -$212.72 million in 2023 to $15.45 million in 2025, indicating instability in the company's cash-generating capabilities. Capital expenditures also show volatility, ranging from -$91.97 million in 2023 to -$3.80 million in 2025, suggesting inconsistent investment in property, plant, and equipment. The company's operating cash flow has improved from negative values in prior years to a positive $37.05 million in 2025, which suggests a better conversion rate of revenues to cash.

Free cash flow has fluctuated significantly, from -$212.72 million in 2023 to $15.45 million in 2025, indicating instability in the company's cash-generating capabilities. Capital expenditures also show volatility, ranging from -$91.97 million in 2023 to -$3.80 million in 2025, suggesting inconsistent investment in property, plant, and equipment. The company's operating cash flow has improved from negative values in prior years to a positive $37.05 million in 2025, which suggests a better conversion rate of revenues to cash.