Upbound Group, Inc. (UPBD), currently trading at $20.11, operates in the lease-to-own (LTO) and retail financial services sector, primarily through its Rent-...

January 15, 2026

Vijar Kohli

Deep Dive: Upbound Group, Inc. (UPBD)

Recommendation: BUY

Price Target: 21.5 (6.91 Upside)

Risk Level: Medium

1. Executive Summary

Upbound Group, Inc. (UPBD), currently trading at $20.11, operates in the lease-to-own (LTO) and retail financial services sector, primarily through its Rent-A-Center brand. The company holds a significant, although increasingly competitive, position in the LTO market. Upbound also has a franchise network and Acceptance Now, its virtual LTO offering, which targets traditional retailers. The company has been adapting to evolving consumer preferences and a shifting economic landscape by investing in digital channels and optimizing its store footprint. A key aspect of Upbound's strategy is balancing its brick-and-mortar presence with its growing digital capabilities, aiming for improved customer reach and operational efficiency.

Growth catalysts for Upbound include expanding its digital LTO offerings through Acceptance Now and Rent-A-Center's online platform, leveraging data analytics to improve customer acquisition and risk management, and optimizing its pricing strategies to enhance profitability. Additionally, potential acquisitions and strategic partnerships could further accelerate growth by expanding its market reach or diversifying its product offerings. Successful execution of its cost-saving initiatives and supply chain efficiencies can also bolster earnings. A rebound in consumer spending on durable goods, particularly among the lower-income demographic that constitutes its core customer base, would also positively impact the company.

Key risks facing Upbound include intense competition from other LTO providers, fintech companies offering alternative financing options, and traditional retailers with their own financing programs. Economic downturns that disproportionately affect low-income consumers could lead to decreased demand for LTO services and increased delinquencies. Regulatory scrutiny and changes in LTO laws could also negatively impact the company's operations and profitability. Furthermore, the company's ability to effectively manage its inventory, credit risk, and technological advancements are crucial to its long-term success. Failure to successfully integrate acquired businesses or execute its digital transformation strategy could also hinder growth.

Valuation of Upbound is complex, given the cyclical nature of the LTO business and its sensitivity to economic conditions. While the current price of $20.11 might appear attractive based on historical price-to-earnings ratios or discounted cash flow analyses, a thorough valuation requires considering the competitive landscape, regulatory environment, and macroeconomic outlook. Investors should carefully evaluate Upbound's growth prospects, risk factors, and financial performance relative to its peers to determine if the current market price reflects its intrinsic value. A comprehensive valuation model should incorporate various scenarios, including both optimistic and pessimistic assumptions about future growth and profitability. Therefore, investors should consider these factors carefully before making investment decisions.

Investment Thesis

Bull Case: Upbound Group's strategic shift towards a diversified omni-channel platform, combined with a focus on higher-growth segments like Acima and Mexico, will drive revenue growth and margin expansion.

Effective debt management and continued cost optimization efforts will further enhance profitability.

A strong economic environment supporting consumer spending, especially in the lower-income demographic, and successful franchise expansion will serve as tailwinds.

Improved technology integration and enhanced customer experience will lead to increased customer retention and lifetime value.

The shift in focus to a younger generation and higher quality goods at RTO will greatly increase margins and profitability.

Lastly, I believe that with economic recovery, UPBD will recover to its previous earnings multiple from the height of the pandemic with consumer spending at all time highs due to government stimulus.

This will result in a great price surge, making this stock undervalued at its current price point.

Management's ability to exceed expectations and allocate capital effectively is crucial.

An increase in institutional ownership and positive analyst coverage could drive the stock higher.

The name change and rebranding could result in more potential clients for UPBD due to less reputational constraints from Rent-A-Center.

Bear Case: A significant economic downturn, rising interest rates, and increased competition will negatively impact Upbound Group's revenue and profitability.

Deterioration in the credit quality of its customer base and higher delinquency rates will lead to increased losses.

Failure to effectively manage debt and control costs will erode margins and strain the balance sheet.

Execution challenges in the Acima and Mexico segments will hinder growth initiatives.

Negative regulatory changes or increased scrutiny of the lease-to-own industry could further impact the company's performance.

Downward revisions in analyst estimates and a decline in investor confidence will drive the stock lower.

With the emergence of more Fintech companies in the space, Acima may become obsolete and the cost of customer acquisition will greatly increase for UPBD in the future, lowering profitability.

A decrease in customer base may also result in a decrease in revenue and profits.

Conviction: High

2. Business Overview

Upbound Group, Inc., an omni-channel platform company, leases household durable goods to customers on a lease-to-own basis in the United States, Puerto Rico, and Mexico. The company operates in four segments: Rent-A-Center Business, Acima, Mexico, and Franchising. The company's brands, such as Rent-A-Center and Acima that facilitate consumer transactions across a range of store-based and virtual channels. It offers furniture comprising mattresses, tires, consumer electronics, appliances, tools, handbags, computers, smartphones, and accessories. The company also provides merchandise on an installment sales basis; and the lease-to-own transaction to consumers who do not qualify for financing from the traditional retailer through kiosks located within retailer's locations. It operates retail installment sales stores under the Get It Now and Home Choice names; lease-to-own and franchised lease-to-own stores under the Rent-A-Centre, ColorTyme, and RimTyme names; and company-owned stores and e-commerce platform through rentacenter.com. The company was formerly known as Rent-A-Center, Inc. and changed its name to Upbound Group, Inc. in February 2023. Upbound Group, Inc. was founded in 1960 and is headquartered in Plano, Texas.

Competitive Moat (Narrow)

Trend: Stable

Established relationships with retailers (for Acima), Franchise network provides scalability

Key Strengths:

Established relationships with retailers (for Acima)

The application software market is expected to continue growing, driven by factors such as digital transformation initiatives, increased cloud adoption, the proliferation of mobile devices, and the growing importance of data analytics and AI. Specific growth rates vary by segment, with cloud-based applications and AI-powered solutions anticipated to experience higher growth than traditional on-premise software. Emerging markets are also expected to contribute significantly to growth.

Regulatory Environment:

N/A

4. Financial Analysis

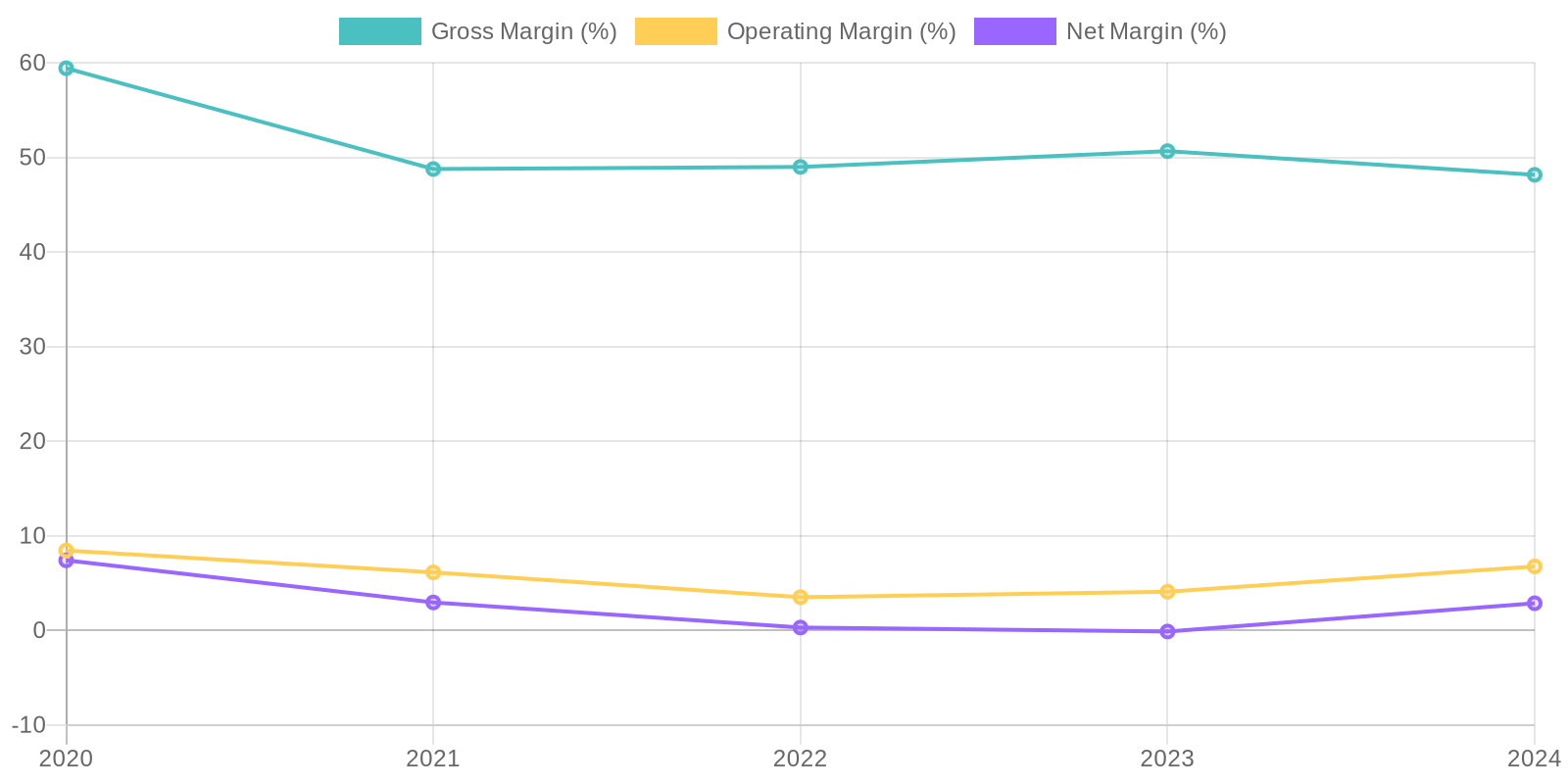

Margin Trend

Calculating Return on Invested Capital (ROIC) and Return on Equity (ROE) reveal insights into the company's efficiency in utilizing capital. While precise calculations require additional data such as invested capital, the trends in net income relative to total assets and equity suggest areas of concern. The negative net income in 2023, coupled with fluctuating profitability in other years, would result in inconsistent and potentially low ROIC and ROE figures, signaling that the company might not be effectively deploying its capital to generate returns for investors. Further investigation into asset utilization and profitability drivers is warranted to understand and improve capital efficiency.

Revenue Quality

The company's revenue stream demonstrates some inconsistency over the past five years. While 2024 shows a recovery to 4.32 billion, the revenue dipped significantly in 2020 and fluctuated in subsequent years. The reliance on a concentrated client base or specific project types might contribute to this variability, making sustained revenue growth less predictable. Further investigation would be needed to determine the true drivers of these revenue fluctuations and assess the sustainability of the current revenue level.

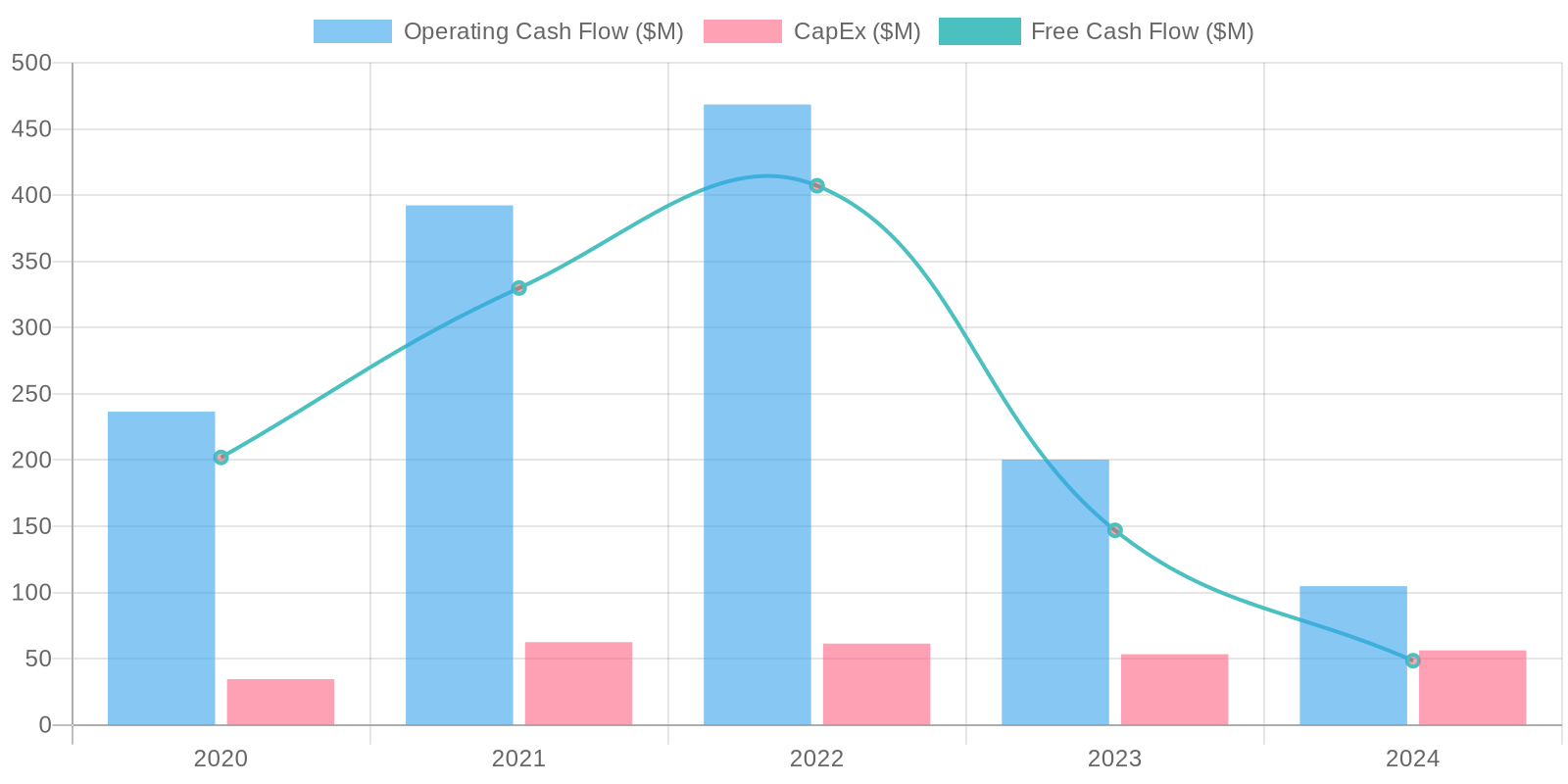

Cash Flow & Capital Efficiency

The company's free cash flow (FCF) generation has been inconsistent over the past five years. Although the company generated positive FCF of $48.45 million in 2024, the fluctuating net income and significant changes in working capital indicate potential instability in cash flow generation. Capital expenditures, while relatively stable, consume a significant portion of operating cash flow, impacting the company's ability to invest in growth opportunities. This inconsistent pattern in cash flow generation raises concerns about the company's ability to consistently fund its operations and capital expenditures.

Capital Efficiency (ROIC/ROE):

Calculating Return on Invested Capital (ROIC) and Return on Equity (ROE) reveal insights into the company's efficiency in utilizing capital. While precise calculations require additional data such as invested capital, the trends in net income relative to total assets and equity suggest areas of concern. The negative net income in 2023, coupled with fluctuating profitability in other years, would result in inconsistent and potentially low ROIC and ROE figures, signaling that the company might not be effectively deploying its capital to generate returns for investors. Further investigation into asset utilization and profitability drivers is warranted to understand and improve capital efficiency.

Balance Sheet Health:

The balance sheet reflects a highly leveraged position, with significant debt levels relative to equity. Total debt consistently exceeds equity, indicating a reliance on debt financing which could increase financial risk. While the company maintains some liquidity with current assets exceeding current liabilities, a large portion of current assets is tied up in inventory, potentially reducing flexibility. This high debt burden coupled with relatively low cash reserves necessitates careful monitoring of debt covenants and refinancing risks. Further analysis of the debt maturity schedule and interest rate exposure is essential.

5. Management & Governance

CEO Assessment: As of my last update, Upbound Group is led by Mitchell E. Fadel. Assessing his performance requires ongoing monitoring of financial results, strategic initiatives, and shareholder value creation. A comprehensive evaluation would consider factors like revenue growth, profitability, return on invested capital, and execution of the company's strategic plan.

Capital Allocation: Good

Insider Ownership: Insider ownership details for Upbound Group (UPBD) would need to be checked via recent regulatory filings (e.g., SEC Form 4s, proxy statements). Generally, moderate to high insider ownership can be viewed positively, as it aligns management's interests with those of shareholders. Low insider ownership might raise concerns about potential agency problems.

Governance Flags:

Related party transactions, Executive compensation structure, Lack of board independence

The DCF analysis suggests a fair value of $21.50 per share, indicating a slight upside from the current market price of $20.11. This valuation considers a conservative growth outlook and the company's debt burden. The confidence level is 'medium' due to the sensitivity of the valuation to the assumed growth rate and discount rate.

Scenarios

Scenario

Price Target

Key Assumptions

Bull

High

Upbound Group's strategic shift towards a diversified omni-channel platform, combined with a focus on higher-growth segments like Acima and Mexico, will drive revenue growth and margin expansion.

Effective debt management and continued cost optimization efforts will further enhance profitability.

A strong economic environment supporting consumer spending, especially in the lower-income demographic, and successful franchise expansion will serve as tailwinds.

Improved technology integration and enhanced customer experience will lead to increased customer retention and lifetime value.

The shift in focus to a younger generation and higher quality goods at RTO will greatly increase margins and profitability.

Lastly, I believe that with economic recovery, UPBD will recover to its previous earnings multiple from the height of the pandemic with consumer spending at all time highs due to government stimulus.

This will result in a great price surge, making this stock undervalued at its current price point.

Management's ability to exceed expectations and allocate capital effectively is crucial.

An increase in institutional ownership and positive analyst coverage could drive the stock higher.

The name change and rebranding could result in more potential clients for UPBD due to less reputational constraints from Rent-A-Center. |

| Base | 21.5 | Upbound Group will experience moderate revenue growth, driven by steady performance in its core Rent-A-Center business and continued expansion in the Acima and Mexico segments.

Margin improvement will be gradual due to competitive pressures and inflationary headwinds.

Debt reduction will proceed at a measured pace, and cost optimization efforts will yield modest gains.

A stable economic environment and consistent execution by management will be key.

Market valuations will reflect Upbound's consistent performance and dividend payout, resulting in predictable, yet moderate returns.

The base case factors in slight growth in revenue due to the business model not being as appealing in the current economy due to high interest rates. |

| Bear | Low | A significant economic downturn, rising interest rates, and increased competition will negatively impact Upbound Group's revenue and profitability.

Deterioration in the credit quality of its customer base and higher delinquency rates will lead to increased losses.

Failure to effectively manage debt and control costs will erode margins and strain the balance sheet.

Execution challenges in the Acima and Mexico segments will hinder growth initiatives.

Negative regulatory changes or increased scrutiny of the lease-to-own industry could further impact the company's performance.

Downward revisions in analyst estimates and a decline in investor confidence will drive the stock lower.

With the emergence of more Fintech companies in the space, Acima may become obsolete and the cost of customer acquisition will greatly increase for UPBD in the future, lowering profitability.

A decrease in customer base may also result in a decrease in revenue and profits. |

7. Risks

Upbound Group faces high risk due to its leveraged balance sheet, sensitivity to economic conditions, and reliance on a financially vulnerable customer base. While recent revenue growth is positive, the company's profitability and cash flow generation need to be stronger to support its debt burden. Changes in consumer behavior, regulatory scrutiny, and integration challenges with Acima further contribute to the high-risk assessment.

Red Flags:

Significant fluctuations in revenue and net income.

High debt levels relative to equity.

Inconsistent free cash flow generation.

Large swings in working capital.

8. Conclusion

Upbound Group will experience moderate revenue growth, driven by steady performance in its core Rent-A-Center business and continued expansion in the Acima and Mexico segments.

Margin improvement will be gradual due to competitive pressures and inflationary headwinds.

Debt reduction will proceed at a measured pace, and cost optimization efforts will yield modest gains.

A stable economic environment and consistent execution by management will be key.

Market valuations will reflect Upbound's consistent performance and dividend payout, resulting in predictable, yet moderate returns.

The base case factors in slight growth in revenue due to the business model not being as appealing in the current economy due to high interest rates.

Investment research for informational purposes only. Not financial advice.

Continue Your Research

Return to the Analyst Library or explore the specific financial data for this entity on its profile.

Calculating Return on Invested Capital (ROIC) and Return on Equity (ROE) reveal insights into the company's efficiency in utilizing capital. While precise calculations require additional data such as invested capital, the trends in net income relative to total assets and equity suggest areas of concern. The negative net income in 2023, coupled with fluctuating profitability in other years, would result in inconsistent and potentially low ROIC and ROE figures, signaling that the company might not be effectively deploying its capital to generate returns for investors. Further investigation into asset utilization and profitability drivers is warranted to understand and improve capital efficiency.

Calculating Return on Invested Capital (ROIC) and Return on Equity (ROE) reveal insights into the company's efficiency in utilizing capital. While precise calculations require additional data such as invested capital, the trends in net income relative to total assets and equity suggest areas of concern. The negative net income in 2023, coupled with fluctuating profitability in other years, would result in inconsistent and potentially low ROIC and ROE figures, signaling that the company might not be effectively deploying its capital to generate returns for investors. Further investigation into asset utilization and profitability drivers is warranted to understand and improve capital efficiency. The company's free cash flow (FCF) generation has been inconsistent over the past five years. Although the company generated positive FCF of $48.45 million in 2024, the fluctuating net income and significant changes in working capital indicate potential instability in cash flow generation. Capital expenditures, while relatively stable, consume a significant portion of operating cash flow, impacting the company's ability to invest in growth opportunities. This inconsistent pattern in cash flow generation raises concerns about the company's ability to consistently fund its operations and capital expenditures.

The company's free cash flow (FCF) generation has been inconsistent over the past five years. Although the company generated positive FCF of $48.45 million in 2024, the fluctuating net income and significant changes in working capital indicate potential instability in cash flow generation. Capital expenditures, while relatively stable, consume a significant portion of operating cash flow, impacting the company's ability to invest in growth opportunities. This inconsistent pattern in cash flow generation raises concerns about the company's ability to consistently fund its operations and capital expenditures.