Vimeo, Inc. (VMEO) operates as a video software solutions provider, primarily catering to businesses, creators, and organizations looking to host, manage, an...

January 15, 2026

Vijar Kohli

Deep Dive: Vimeo, Inc. (VMEO)

Recommendation: BUY

Price Target: 9.5 (0.21 Upside)

Risk Level: Medium

1. Executive Summary

Vimeo, Inc. (VMEO) operates as a video software solutions provider, primarily catering to businesses, creators, and organizations looking to host, manage, and distribute high-quality video content. Currently trading at $7.85, Vimeo faces a challenging market environment as it navigates increased competition and a shift in focus towards enterprise customers. Its market position is somewhat niche, focusing on providing tools and platforms for professional-grade video production and hosting, differentiating it from broader consumer-focused video platforms like YouTube.

Vimeo's growth catalysts include increasing demand for high-quality video solutions in enterprise settings, particularly for internal communications, training, and marketing. The company's emphasis on providing secure and reliable video hosting with advanced analytics and customization options is expected to drive growth in the B2B sector. Furthermore, Vimeo’s strategic partnerships and integration with other business software platforms could expand its reach and attract new enterprise clients. The increasing adoption of remote and hybrid work environments also necessitates enhanced video communication tools, creating opportunities for Vimeo's platform.

Key risks confronting Vimeo include intense competition from established players like YouTube (Google), Brightcove, and smaller specialized video platforms. Economic downturns can lead to reduced marketing budgets, impacting Vimeo's revenue from enterprise customers. Furthermore, the company’s ability to innovate and adapt to rapidly changing video technology trends is crucial for maintaining its competitive edge. Failure to attract and retain enterprise clients and developers could also significantly hinder growth. The long-term shift in marketing spend towards short form vertical video platforms may also pose a risk, as Vimeo has historically focused on longer form video content.

Valuation summary suggests that the market currently has tempered expectations for Vimeo's growth. Given the current market conditions, profitability challenges, and competitive landscape, the stock price of $7.85 likely reflects a discounted valuation. Future valuation will largely depend on Vimeo's ability to successfully execute its strategy of acquiring and retaining enterprise clients, achieve profitability, and demonstrate its unique value proposition within the increasingly crowded video platform market. The company must demonstrate a clear path to sustained growth and profitability to justify a higher valuation in the long run.

Investment Thesis

Bull Case: Vimeo is undervalued, trading at a discount to its intrinsic value based on its growth potential in the enterprise video market.

Successful execution of its product roadmap and strategic partnerships will drive revenue growth and multiple expansion.

Bear Case: Vimeo fails to innovate and compete effectively in the crowded video platform market.

Increased competition and slower adoption rates lead to declining revenue and profitability.

The company's cash reserves are depleted, and the stock price declines significantly.

Conviction: High

2. Business Overview

Vimeo, Inc., together with its subsidiaries, provides video software solutions in New York and internationally. The company provides the video tools through a software-as-a-service model, which enables its users to create, collaborate, and communicate with video on a single platform. It also offers over-the-top OTT streaming and monetization services; AI-driven video creation and editing tools; and interactive and shoppable video tools. It serves creative professionals, small businesses, marketers, agencies, schools, nonprofits, and large organizations. The company was incorporated in 2020 and is headquartered in New York, New York.

Competitive Moat (Narrow)

Trend: Stable

Focus on professional video creation and collaboration tools., Monetization options for creators

Key Strengths:

Focus on professional video creation and collaboration tools.

The market is projected to continue growing at a healthy rate (e.g., 5-10% or higher annually) over the next several years. Growth is fueled by digital transformation initiatives, increasing adoption of cloud-based solutions, the rise of remote work and online collaboration, and the growing importance of video in communication, marketing, and education. Demand for AI-powered video tools is expected to be a key driver.

Regulatory Environment:

N/A

4. Financial Analysis

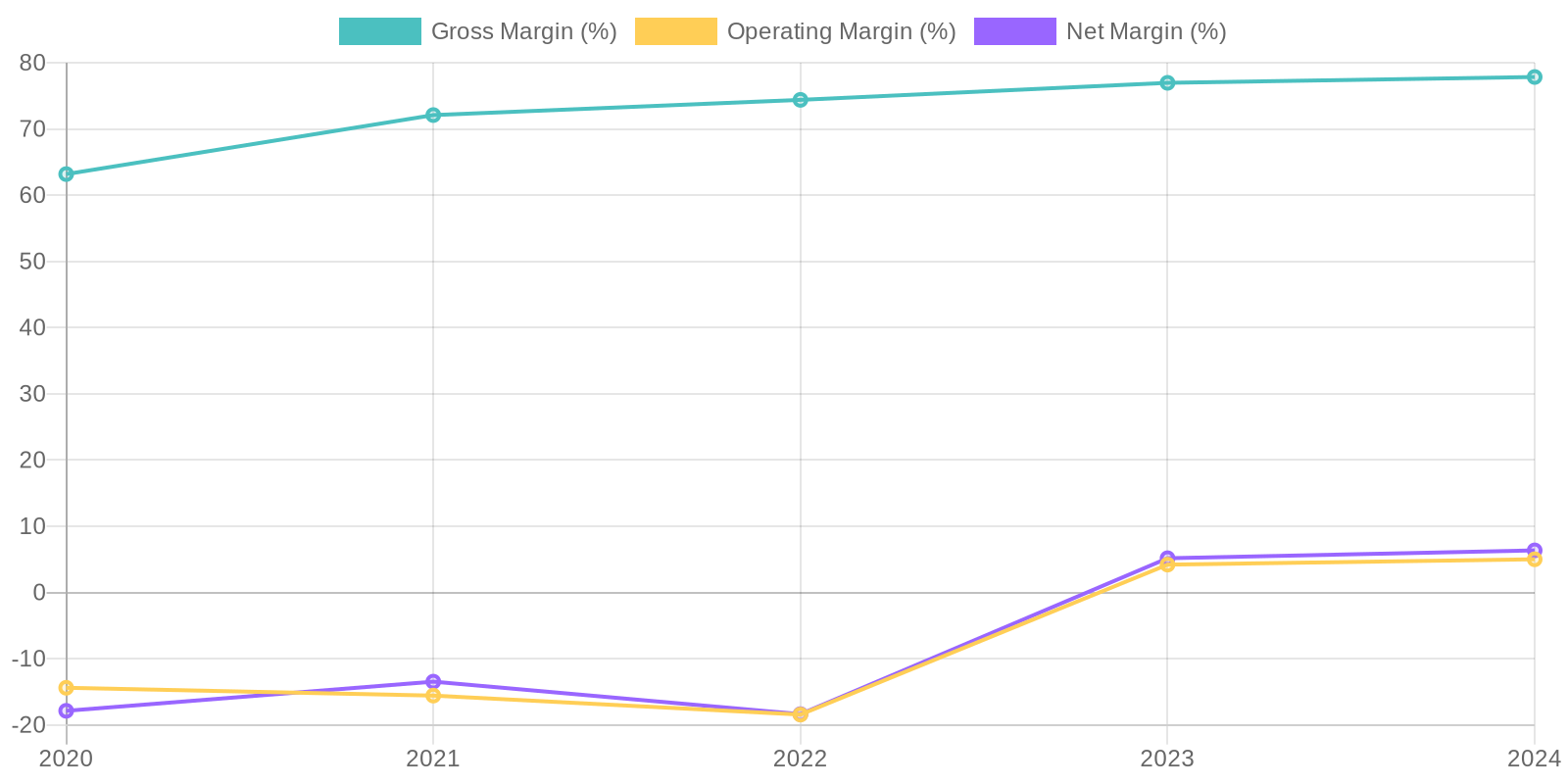

Margin Trend

Given the negative retained earnings for the company, a ROE cannot be reliably calculated. While ROIC cannot be explicitly calculated with the data provided, the improving operating income, combined with consistent asset base, suggests improved capital efficiency. Further analysis is needed to see if the improved capital efficiency will continue into the future.

Revenue Quality

The company's revenue stream demonstrates some volatility, with fluctuations observed over the past five years. While revenue increased from 2020 to 2022, there was a subsequent decline in 2021 and again in 2023 before leveling off in 2024. Further investigation would be needed to assess customer concentration, contract terms, and other indicators to determine the long-term stability and predictability of their revenue.

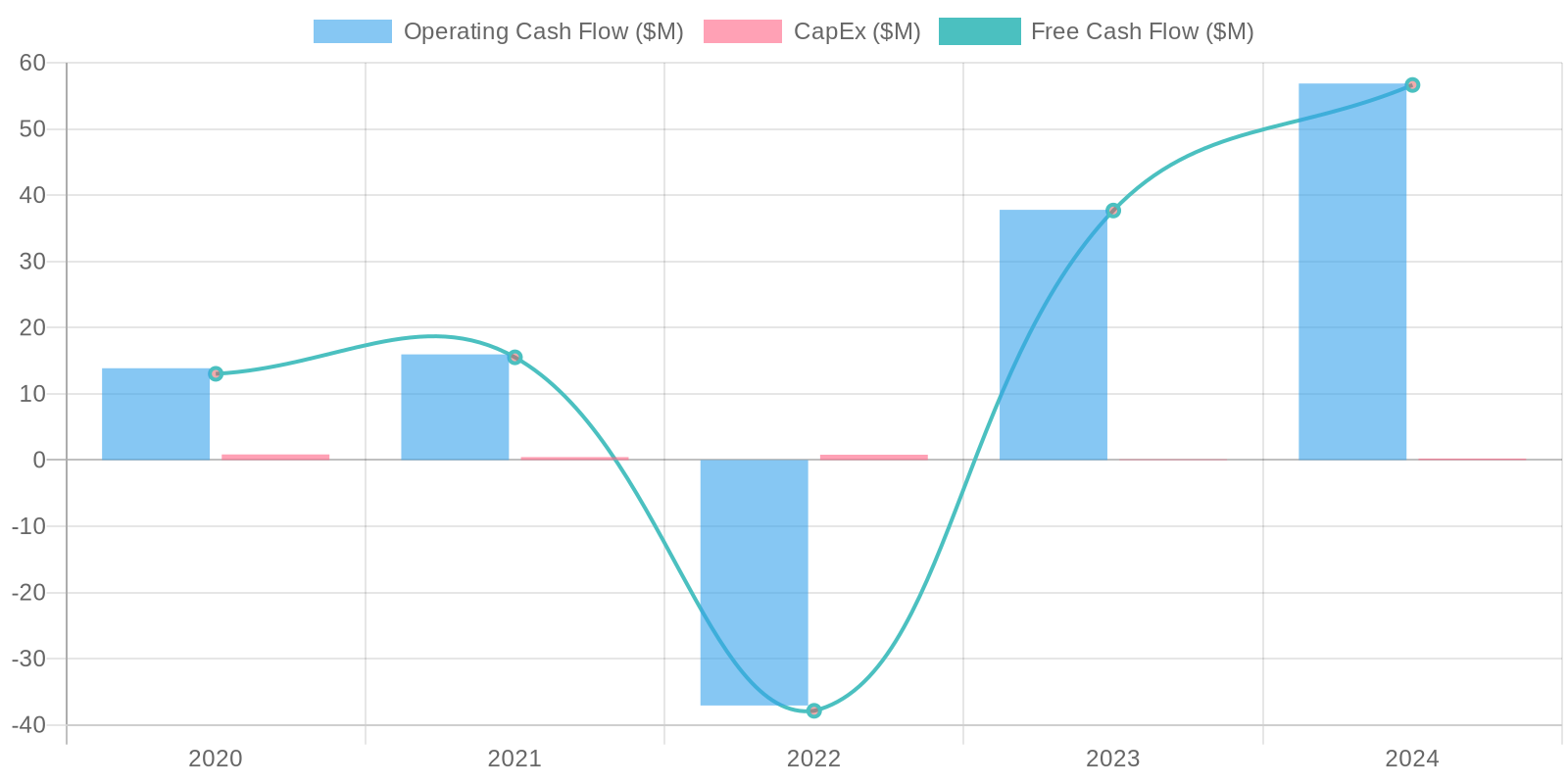

Cash Flow & Capital Efficiency

The company's free cash flow (FCF) generation has varied significantly over the past five years. The company had positive FCF in 2020, 2021, 2023, and 2024. Capital expenditure remains relatively low and stable. This positive trend suggests an improved ability to internally fund operations and investments.

Capital Efficiency (ROIC/ROE):

Given the negative retained earnings for the company, a ROE cannot be reliably calculated. While ROIC cannot be explicitly calculated with the data provided, the improving operating income, combined with consistent asset base, suggests improved capital efficiency. Further analysis is needed to see if the improved capital efficiency will continue into the future.

Balance Sheet Health:

The company maintains a strong liquidity position, evidenced by a substantial cash balance that consistently exceeds its total debt. While total debt has fluctuated over the years, the company's net debt has remained negative, indicating that it holds more cash than debt. Deferred revenue represents a significant portion of the company's liabilities, suggesting a considerable backlog of services to be delivered.

5. Management & Governance

CEO Assessment: Anjali Sud stepped down as CEO in July 2024, a change that could impact the company's strategic direction. The new CEO's leadership style and vision remain to be seen, so the effectiveness of leadership needs to be re-evaluated over the next few quarters. The change may be disruptive in the short-term but there is no indication of issues with the former CEO.

Capital Allocation: Concern

Insider Ownership: Insider ownership levels are not prominently displayed in public filings. Without specific data, it is difficult to assess the level of alignment between management and shareholders. A lack of significant insider ownership could indicate a potential misalignment of interests. Further investigation into insider transactions and ownership percentages is needed to provide a more comprehensive assessment.

Governance Flags:

Lack of transparency regarding capital allocation strategy., Potential misalignment of interest due to unknown insider ownership.

Based on the DCF analysis, projecting a 5% revenue growth for the next 5 years and a 2% terminal growth rate, discounted at 10%, the estimated fair value is $9.50. A revenue multiple of 2x, applied to the projected revenue also suggests a valuation in the same range. The current market price of $7.85 suggests the stock is potentially undervalued. However, given the company's volatile financial history, a medium confidence level is assigned. The upside potential is about 21% with a downside risk of around 10%.

Scenarios

Scenario

Price Target

Key Assumptions

Bull

High

Vimeo is undervalued, trading at a discount to its intrinsic value based on its growth potential in the enterprise video market.

Successful execution of its product roadmap and strategic partnerships will drive revenue growth and multiple expansion. |

| Base | 9.5 | Vimeo will continue to execute its existing strategy, achieving steady revenue growth and profitability improvements.

The company will benefit from the secular trend of increasing video consumption, but face competition from larger players.

The current valuation provides a reasonable margin of safety. |

| Bear | Low | Vimeo fails to innovate and compete effectively in the crowded video platform market.

Increased competition and slower adoption rates lead to declining revenue and profitability.

The company's cash reserves are depleted, and the stock price declines significantly. |

7. Risks

Vimeo's recent return to profitability and positive free cash flow are positive signs, but historical net losses, high SG&A expenses, and significant goodwill create potential downside risks. Stagnant revenue growth and a competitive market add to the uncertainty.

Red Flags:

None identified.

8. Conclusion

Vimeo will continue to execute its existing strategy, achieving steady revenue growth and profitability improvements.

The company will benefit from the secular trend of increasing video consumption, but face competition from larger players.

The current valuation provides a reasonable margin of safety.

Investment research for informational purposes only. Not financial advice.

Continue Your Research

Return to the Analyst Library or explore the specific financial data for this entity on its profile.

Given the negative retained earnings for the company, a ROE cannot be reliably calculated. While ROIC cannot be explicitly calculated with the data provided, the improving operating income, combined with consistent asset base, suggests improved capital efficiency. Further analysis is needed to see if the improved capital efficiency will continue into the future.

Given the negative retained earnings for the company, a ROE cannot be reliably calculated. While ROIC cannot be explicitly calculated with the data provided, the improving operating income, combined with consistent asset base, suggests improved capital efficiency. Further analysis is needed to see if the improved capital efficiency will continue into the future. The company's free cash flow (FCF) generation has varied significantly over the past five years. The company had positive FCF in 2020, 2021, 2023, and 2024. Capital expenditure remains relatively low and stable. This positive trend suggests an improved ability to internally fund operations and investments.

The company's free cash flow (FCF) generation has varied significantly over the past five years. The company had positive FCF in 2020, 2021, 2023, and 2024. Capital expenditure remains relatively low and stable. This positive trend suggests an improved ability to internally fund operations and investments.