Deep Dive: VeriSign, Inc. (VRSN)

Recommendation: HOLD Price Target: 255.78 (0.0263 Upside) Risk Level: Medium

1. Executive Summary

VeriSign (VRSN) currently holds a dominant market position as the exclusive registry for .com and .net domain names, a critical component of the internet infrastructure. This quasi-monopoly provides substantial recurring revenue and high barriers to entry, supporting significant profitability and cash flow generation. Its business model benefits from the increasing importance of online presence for businesses and individuals, making domain names a relatively inelastic service. At a current price of $249.22, VeriSign presents a compelling case for investors seeking stable, albeit potentially moderate, growth.

Several growth catalysts underpin VeriSign's long-term prospects. The primary driver is the annual price increases for .com domain names, allowed by its agreement with ICANN (Internet Corporation for Assigned Names and Numbers). While these increases are capped, they still contribute significantly to revenue growth. Further growth potential lies in the increasing number of internet users and businesses establishing an online presence, driving new domain name registrations. Additionally, VeriSign could potentially expand its services beyond domain name registration into related areas like cybersecurity or DNS services, leveraging its existing infrastructure and customer base.

Despite its strong position, VeriSign faces several key risks. The renewal of its agreement with ICANN is a recurring concern, as unfavorable terms could limit future price increases or even introduce competition. Technological disruptions, such as the emergence of alternative domain name systems or decentralized web technologies, could erode its market share, although this is a longer-term threat. Economic downturns could impact domain name registrations and renewals, although the essential nature of domain names provides some resilience. Regulatory scrutiny regarding its pricing and market dominance remains a persistent risk.

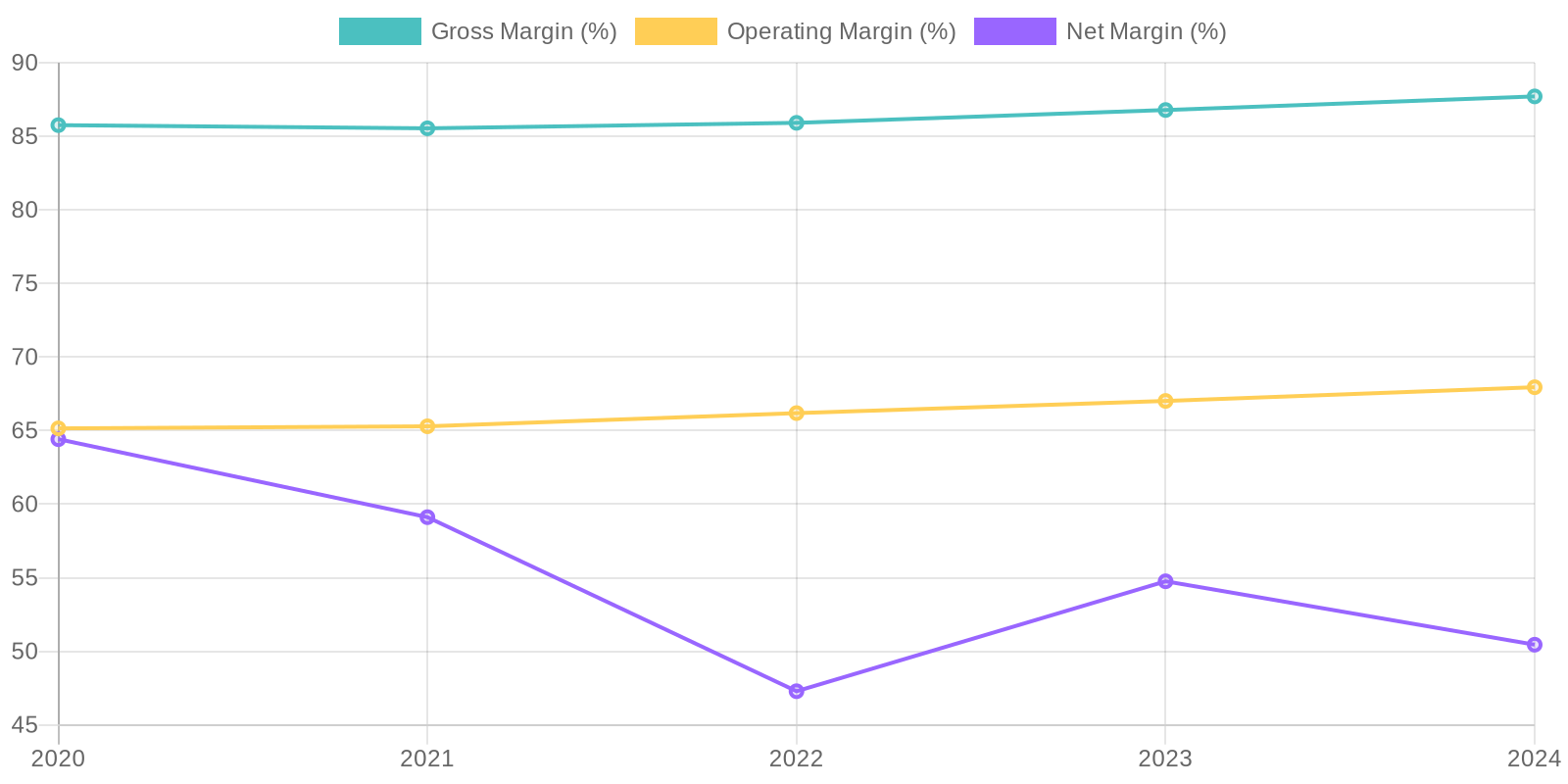

From a valuation perspective, VeriSign's stock price reflects its stable revenue stream and high profitability. Traditional valuation metrics like Price-to-Earnings (P/E) and Price-to-Free Cash Flow (P/FCF) might appear elevated compared to broader market averages. However, this premium is justified by its consistent revenue growth, high margins, and strong cash generation. A discounted cash flow (DCF) analysis, considering conservative growth rates and a reasonable discount rate, can provide a more comprehensive valuation. The current price suggests the market anticipates continued, albeit moderate, growth and limited significant disruptions to its business model. Investors should carefully consider the risks and growth catalysts outlined above when evaluating VeriSign's long-term investment potential.

Calculating ROIC requires additional data on invested capital, but the provided information allows for an assessment of trends based on available data. The company's ROE is negative due to the negative equity reported on the balance sheet, which requires further investigation into the causes of this equity deficit. The consistently high net income figures relative to revenue suggest potentially efficient asset utilization, although a more comprehensive ROIC calculation would provide a clearer picture of capital efficiency.

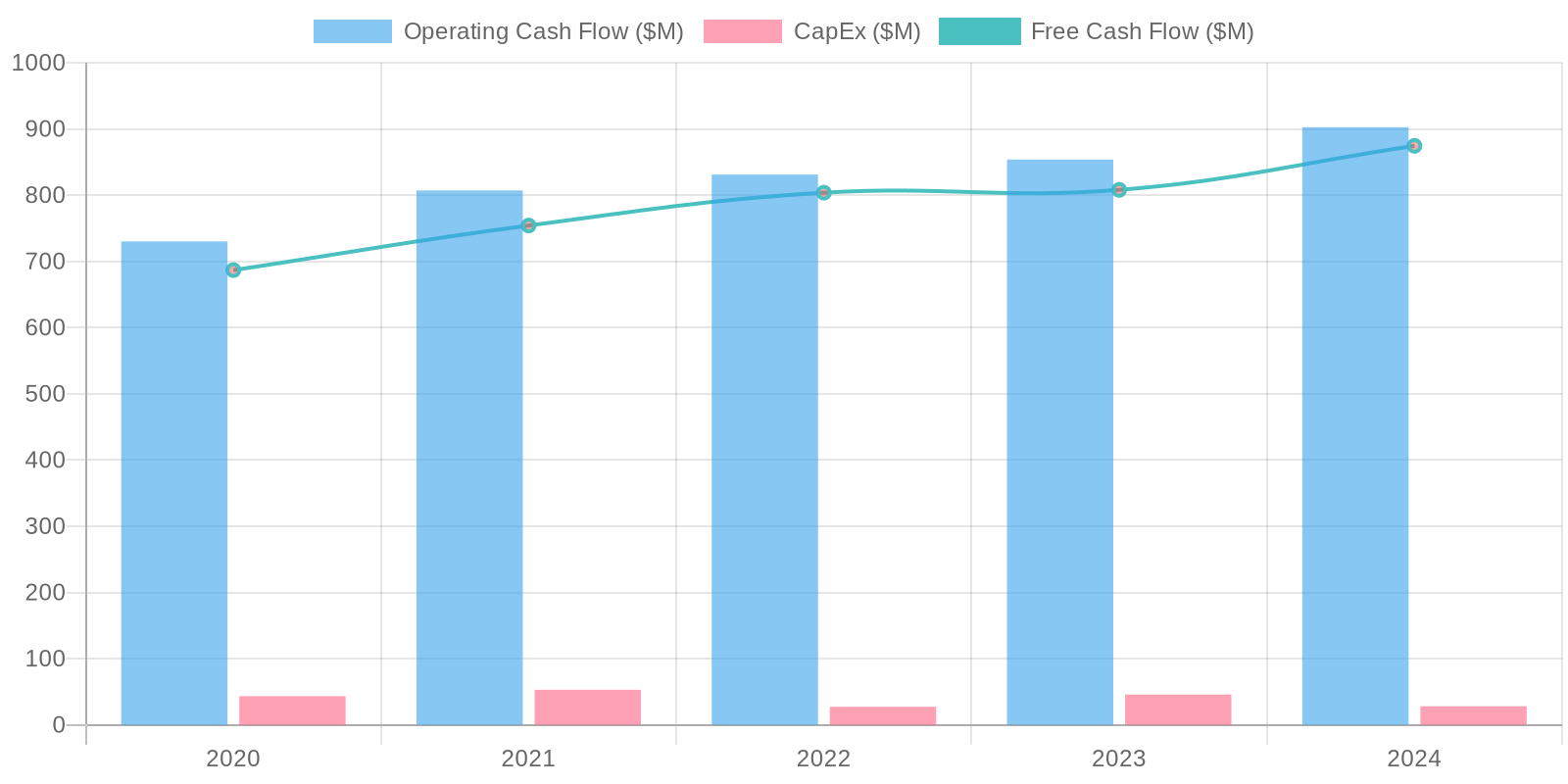

Calculating ROIC requires additional data on invested capital, but the provided information allows for an assessment of trends based on available data. The company's ROE is negative due to the negative equity reported on the balance sheet, which requires further investigation into the causes of this equity deficit. The consistently high net income figures relative to revenue suggest potentially efficient asset utilization, although a more comprehensive ROIC calculation would provide a clearer picture of capital efficiency. The company exhibits strong free cash flow generation, with FCF consistently positive and closely aligned with net income, indicating a healthy conversion rate. Capital expenditures are relatively low, suggesting limited need for reinvestment to maintain operations. The consistent positive free cash flow allows the company flexibility in managing its debt and pursuing growth opportunities, although significant cash is being used for stock repurchases.

The company exhibits strong free cash flow generation, with FCF consistently positive and closely aligned with net income, indicating a healthy conversion rate. Capital expenditures are relatively low, suggesting limited need for reinvestment to maintain operations. The consistent positive free cash flow allows the company flexibility in managing its debt and pursuing growth opportunities, although significant cash is being used for stock repurchases.