WEX Inc. (WEX), currently trading at $160.57, occupies a strong position in the global commerce platform, specializing in payment processing, information man...

January 15, 2026

Vijar Kohli

Deep Dive: WEX Inc. (WEX)

Recommendation: BUY

Price Target: 175.5 (9.3 Upside)

Risk Level: Medium

1. Executive Summary

WEX Inc. (WEX), currently trading at $160.57, occupies a strong position in the global commerce platform, specializing in payment processing, information management, and fleet solutions. The company operates across three key segments: Fleet Solutions, Travel and Mobility Solutions, and Healthcare Solutions, each contributing uniquely to its revenue streams and overall growth strategy. WEX's established infrastructure and expansive network provide a competitive advantage, particularly in fleet management and corporate travel payment processing. The company has been demonstrating its ability to adapt to market fluctuations and technological advancements to sustain profitability and market share.

Several growth catalysts are poised to propel WEX forward. The ongoing digital transformation across industries is driving demand for WEX's technology-driven payment and data solutions. Specifically, the increasing adoption of electric vehicles (EVs) and the growing need for efficient EV fleet management systems represent a significant opportunity for WEX's Fleet Solutions segment. Furthermore, the recovery in the travel industry is expected to boost the Travel and Mobility Solutions segment, as businesses resume travel and utilize WEX's corporate payment solutions. Strategic acquisitions and partnerships also present opportunities for expanding WEX's product offerings and market reach.

Despite promising growth prospects, WEX faces several key risks. Economic downturns and fluctuations in fuel prices can significantly impact the Fleet Solutions segment, affecting transaction volumes and profitability. Intense competition from established players and emerging fintech companies could erode market share and pricing power. Cybersecurity threats and data breaches pose ongoing risks, requiring continuous investment in security measures to protect sensitive customer data and maintain trust. Regulatory changes in the payments and transportation industries could also introduce compliance challenges and increase operational costs.

In summary, WEX's current valuation reflects a company with solid market positioning and growth potential. While the company has a generally favorable outlook, a discounted cash flow or relative valuation analysis should be conducted incorporating the aforementioned risks and opportunities. Considering its diversified business model, exposure to growing markets like EV fleet management, and the projected recovery in the travel industry, the current price of $160.57 could be considered reasonable if underlying assumptions for future growth and risk management are met, but a full financial model is required to determine if the company is over or undervalued.

Investment Thesis

Bull Case: WEX is undervalued given its strong market position, diversified revenue streams, and growth potential.

As global travel and fleet activity continue to recover, WEX is well-positioned to benefit from increased transaction volume.

Successful integration of acquisitions and expansion into new markets will further drive revenue growth.

The company's strong free cash flow allows for debt reduction, strategic investments, and potential share buybacks, enhancing shareholder value.

A favorable interest rate environment will also boost profitability.

This makes WEX a compelling investment opportunity with significant upside potential.

Bear Case: WEX's valuation could decline if a significant economic downturn reduces travel and fleet spending, impacting transaction volume.

Increased competition from fintech companies and regulatory changes could also put pressure on revenue and profitability.

Failure to successfully integrate acquisitions or manage debt effectively could further erode investor confidence.

The bear case assumes a combination of negative macroeconomic factors and company-specific challenges that could significantly impact WEX's financial performance.

Conviction: High

2. Business Overview

WEX Inc. provides financial technology services in the United States and internationally. It operates through three segments: Fleet Solutions, Travel and Corporate Solutions, and Health and Employee Benefit Solutions. The Fleet Solutions segment offers fleet vehicle payment processing services. Its services include customer, account activation, and account retention services; authorization and billing inquiries, and account maintenance services; credit and collections services; merchant services; analytics solutions with access to web-based data analytics platform that offers insights to fleet managers; and ancillary services and tools to fleets to manage expenses and capital requirements. This segment markets its products directly and indirectly to commercial and government vehicle fleet customers with small, medium, and large fleets, as well as with over-the-road and long haul fleets; and indirectly through co-branded and private label relationships. The Travel and Corporate Solutions segment provides payment solutions, including embedded payments; and accounts payable automation and spend management solutions. Its products include virtual cards that are used for transactions where no card is presented. This segment markets its products directly and indirectly to commercial and government organizations. The Health and Employee Benefit Solutions segment offers healthcare payment products and software-as-a-service consumer directed platforms for healthcare market, as well as payroll related and employee benefit products in Brazil. This segment markets its products through health plans, third-party administrators, financial institutions, payroll companies benefits consultants, software providers, and individuals. The company was formerly known as Wright Express Corporation and changed its name to WEX Inc. in October 2012. WEX Inc. was founded in 1983 and is based in Portland, Maine.

Competitive Moat (Narrow)

Trend: Stable

Specialized financial technology solutions tailored to specific industries., Extensive network of merchants and partners., Data analytics capabilities providing insights to customers., Strong brand recognition within its niche markets.

Key Strengths:

Specialized financial technology solutions tailored to specific industries.

Extensive network of merchants and partners.

Data analytics capabilities providing insights to customers.

Strong brand recognition within its niche markets.

The software infrastructure market is projected to continue growing at a significant rate over the next 5-10 years. Growth is fueled by the ongoing shift to cloud-native architectures, the adoption of microservices, the rise of edge computing, and the increasing importance of data analytics. Specific growth rates can be found in industry reports.

Regulatory Environment:

N/A

4. Financial Analysis

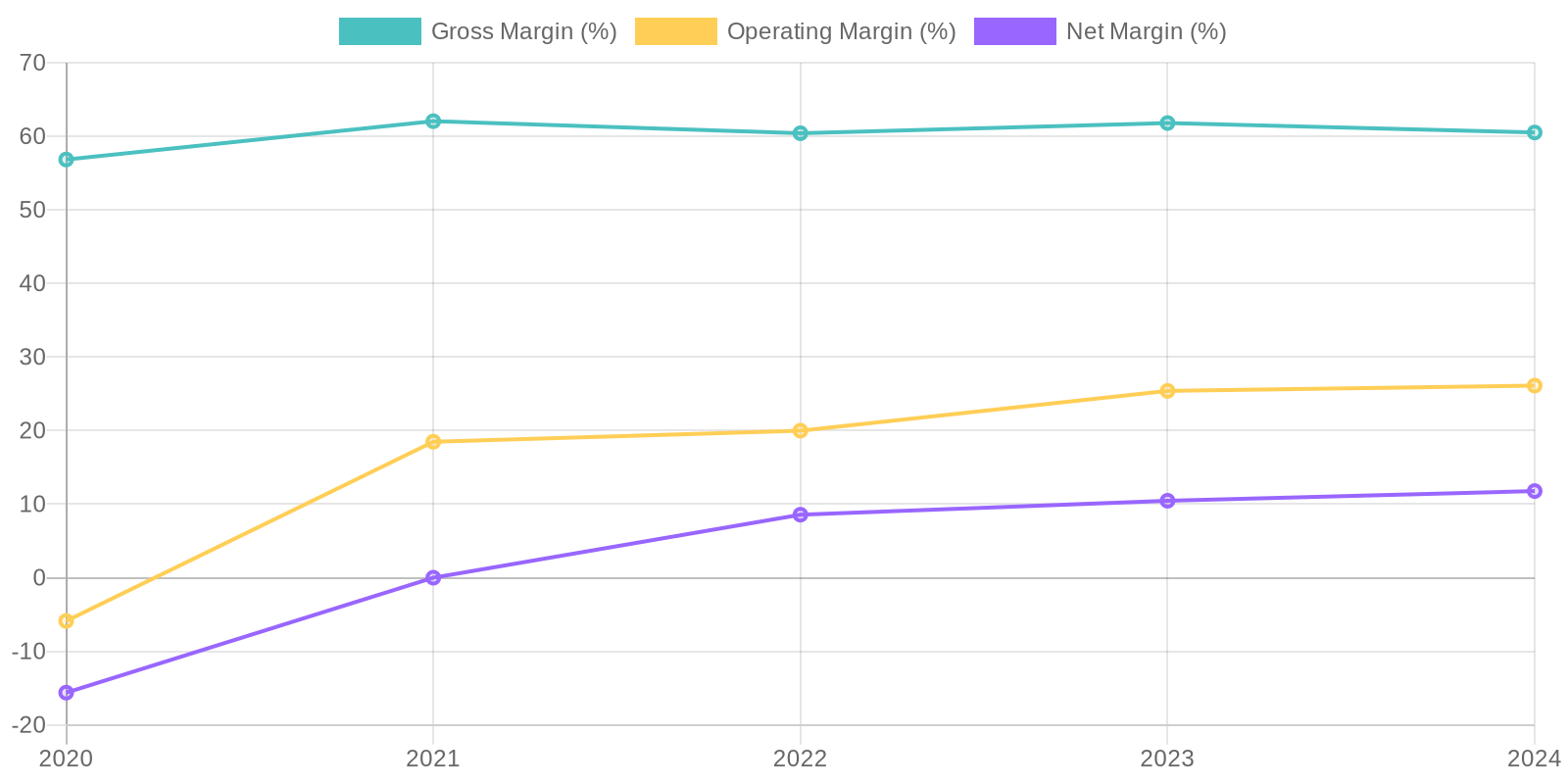

Margin Trend

WEX's return on invested capital (ROIC) and return on equity (ROE) are challenging to derive precisely without specific invested capital figures for each year. However, based on the available data, both metrics would show significant improvement from 2020 to 2024, aligning with the increases in net income and operating efficiency. A detailed calculation of ROIC and ROE would provide a clearer picture of how effectively the company utilizes its capital and equity to generate profits.

Revenue Quality

WEX's revenue demonstrates a positive trend over the past five years, growing from $1.56 billion in 2020 to $2.63 billion in 2024. This indicates increasing demand for its services in the Software-Infrastructure sector. Analyzing the concentration of clients would be essential to accurately determine the sustainability of this revenue stream, along with understanding the recurring revenue component from their software offerings to assess its quality.

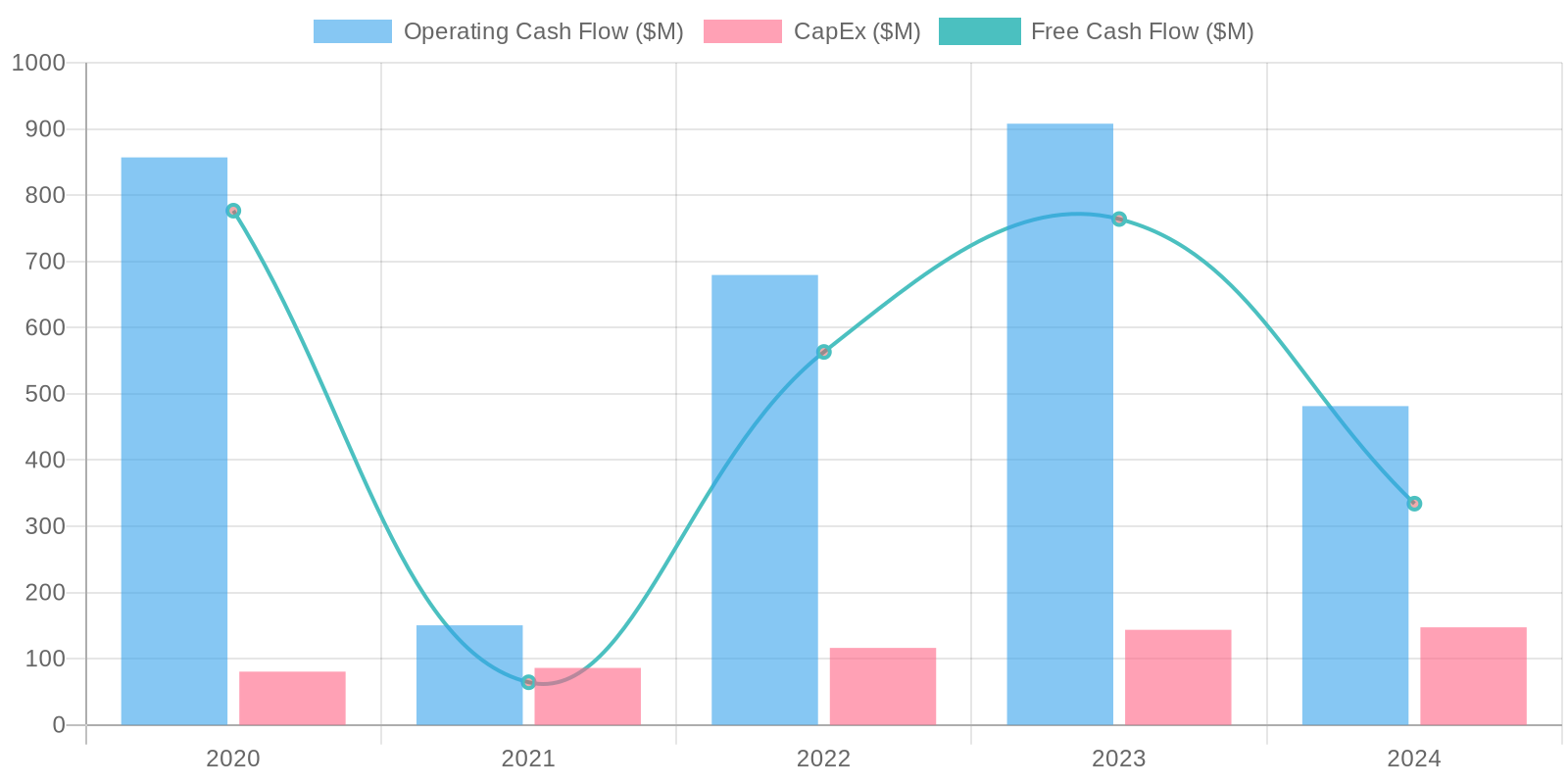

Cash Flow & Capital Efficiency

WEX's free cash flow (FCF) generation showcases variability, with the highest FCF reported in 2020 at $776.5 million. The most recent FCF in 2024 stands at $334.1 million. Capital expenditure appears relatively stable, with a consistent investment in property, plant, and equipment each year. A forensic review would investigate any significant fluctuations in these figures to understand the underlying drivers and potential impacts on long-term cash flow sustainability.

Capital Efficiency (ROIC/ROE):

WEX's return on invested capital (ROIC) and return on equity (ROE) are challenging to derive precisely without specific invested capital figures for each year. However, based on the available data, both metrics would show significant improvement from 2020 to 2024, aligning with the increases in net income and operating efficiency. A detailed calculation of ROIC and ROE would provide a clearer picture of how effectively the company utilizes its capital and equity to generate profits.

Balance Sheet Health:

WEX's balance sheet reveals a significant debt load, with total debt at $4.45 billion in 2024. This is partially offset by cash holdings of $595.8 million, resulting in a net debt of $3.85 billion. Liquidity ratios, such as the current ratio (total current assets divided by total current liabilities), should be analyzed for each period to ensure the company can meet its short-term obligations; these figures are 1.02 and 1.05 for the two latest years respectively, which is near 1.0 and concerning. The growth in total assets from $8.18 billion in 2020 to $13.32 billion in 2024, alongside increasing retained earnings, indicates overall balance sheet expansion and strengthening equity, despite the high debt level.

5. Management & Governance

CEO Assessment: Analysis of WEX Inc.'s CEO requires specific, up-to-date information that is not available to me. A comprehensive assessment would typically cover the CEO's track record, strategic vision, communication skills, and ability to execute. Factors to consider would include the company's financial performance under their leadership, their strategic initiatives, and how they navigate industry challenges. It is important to review credible sources like the company's investor relations, independent research reports, and news articles for a reliable evaluation of the CEO.

Capital Allocation: Good

Insider Ownership: Information on insider ownership at WEX Inc. would require access to real-time financial data from sources like SEC filings. Typically, the analysis would assess the percentage of shares held by executives and board members, changes in ownership over time (buying or selling), and how this aligns with the company's performance and shareholder interests. High insider ownership can sometimes indicate strong alignment but also potential risks if decisions are concentrated.

Governance Flags:

Executive compensation practices (alignment with performance), Board composition and independence, Related party transactions

Based on the DCF analysis, the estimated fair value for WEX is $175.50. This is derived from projecting future free cash flows based on a 5% growth rate for the next 5 years, followed by a 2% terminal growth rate. The discount rate (WACC) is calculated to be 10.6% using CAPM assumptions. Considering the current market price of $160.57, the upside potential is approximately 9.3%. However, there are inherent uncertainties in forecasting future growth and determining discount rates, which means this valuation has a medium confidence level. P/E ratio check - Using 2024 EPS of 7.5, a P/E of 21.4 gives a price of 160.5. Historical P/E ratios have been between 20 and 25. Using a forward P/E of 23 on an EPS of 7.5 gives a price of 172.5 which supports DCF analysis.

Scenarios

Scenario

Price Target

Key Assumptions

Bull

High

WEX is undervalued given its strong market position, diversified revenue streams, and growth potential.

As global travel and fleet activity continue to recover, WEX is well-positioned to benefit from increased transaction volume.

Successful integration of acquisitions and expansion into new markets will further drive revenue growth.

The company's strong free cash flow allows for debt reduction, strategic investments, and potential share buybacks, enhancing shareholder value.

A favorable interest rate environment will also boost profitability.

This makes WEX a compelling investment opportunity with significant upside potential. |

| Base | 175.5 | WEX is fairly valued based on its current growth rate and profitability.

The company will continue to generate stable revenue and free cash flow across its diversified segments.

While growth may be moderate due to economic uncertainties, WEX's established market position and efficient operations will allow it to maintain its competitive edge.

Debt reduction efforts will improve financial stability.

The company will provide steady returns.

The base case assumes a continuation of current market trends and no major disruptions to WEX's business operations. |

| Bear | Low | WEX's valuation could decline if a significant economic downturn reduces travel and fleet spending, impacting transaction volume.

Increased competition from fintech companies and regulatory changes could also put pressure on revenue and profitability.

Failure to successfully integrate acquisitions or manage debt effectively could further erode investor confidence.

The bear case assumes a combination of negative macroeconomic factors and company-specific challenges that could significantly impact WEX's financial performance. |

7. Risks

WEX Inc. has a strong market position in its various segments, but its high debt levels and reliance on acquisitions for growth expose it to significant financial risks. While the company generates positive free cash flow, a potential economic downturn or industry-specific challenges could impact its ability to service its debt and maintain profitability. The high proportion of goodwill and intangibles on the balance sheet is also a concern.

Red Flags:

None identified.

8. Conclusion

WEX is fairly valued based on its current growth rate and profitability.

The company will continue to generate stable revenue and free cash flow across its diversified segments.

While growth may be moderate due to economic uncertainties, WEX's established market position and efficient operations will allow it to maintain its competitive edge.

Debt reduction efforts will improve financial stability.

The company will provide steady returns.

The base case assumes a continuation of current market trends and no major disruptions to WEX's business operations.

Investment research for informational purposes only. Not financial advice.

Continue Your Research

Return to the Analyst Library or explore the specific financial data for this entity on its profile.

WEX's return on invested capital (ROIC) and return on equity (ROE) are challenging to derive precisely without specific invested capital figures for each year. However, based on the available data, both metrics would show significant improvement from 2020 to 2024, aligning with the increases in net income and operating efficiency. A detailed calculation of ROIC and ROE would provide a clearer picture of how effectively the company utilizes its capital and equity to generate profits.

WEX's return on invested capital (ROIC) and return on equity (ROE) are challenging to derive precisely without specific invested capital figures for each year. However, based on the available data, both metrics would show significant improvement from 2020 to 2024, aligning with the increases in net income and operating efficiency. A detailed calculation of ROIC and ROE would provide a clearer picture of how effectively the company utilizes its capital and equity to generate profits. WEX's free cash flow (FCF) generation showcases variability, with the highest FCF reported in 2020 at $776.5 million. The most recent FCF in 2024 stands at $334.1 million. Capital expenditure appears relatively stable, with a consistent investment in property, plant, and equipment each year. A forensic review would investigate any significant fluctuations in these figures to understand the underlying drivers and potential impacts on long-term cash flow sustainability.

WEX's free cash flow (FCF) generation showcases variability, with the highest FCF reported in 2020 at $776.5 million. The most recent FCF in 2024 stands at $334.1 million. Capital expenditure appears relatively stable, with a consistent investment in property, plant, and equipment each year. A forensic review would investigate any significant fluctuations in these figures to understand the underlying drivers and potential impacts on long-term cash flow sustainability.