Xerox Holdings Corporation (XRX), currently trading at $2.69, faces a challenging market position marked by declining revenue in its legacy print and paper b...

January 15, 2026

Vijar Kohli

Deep Dive: Xerox Holdings Corporation (XRX)

Recommendation: BUY

Price Target: 1.45 (-46.09 Upside)

Risk Level: Medium

1. Executive Summary

Xerox Holdings Corporation (XRX), currently trading at $2.69, faces a challenging market position marked by declining revenue in its legacy print and paper business. The company is undergoing a significant transformation, attempting to diversify into higher-growth areas like digital services, IT solutions, and software. Xerox's historical reliance on hardware sales and managed print services necessitates a strategic shift to adapt to evolving customer demands and digital transformation trends.

Growth catalysts for Xerox hinge on the successful execution of its diversification strategy. Key areas include expanding its IT services offerings, leveraging its existing customer base to cross-sell new solutions, and developing innovative software solutions. The company also aims to improve operational efficiency through cost reduction initiatives and strategic partnerships. Successful navigation of these growth areas will be crucial for Xerox to regain market relevance and drive sustainable revenue growth. Specific areas of focus include digital workflow solutions and expanding into adjacent markets through strategic acquisitions.

Key risks confronting Xerox include the continued decline in demand for traditional printing products and services, intense competition from established players in the IT services market, and potential challenges in integrating acquired businesses. Furthermore, the company faces execution risk associated with its transformation efforts, including potential disruptions to its existing business and difficulties in attracting and retaining talent with expertise in new technology areas. Economic downturns can also significantly impact hardware sales and managed services, creating additional headwinds. The debt burden also requires careful management as the company seeks to invest in new growth opportunities.

Valuation summary suggests Xerox is currently undervalued, reflecting market skepticism regarding its transformation efforts and concerns about its declining legacy business. The current price likely incorporates expectations of continued revenue decline and limited growth prospects. A successful pivot towards higher-growth areas and improved operational efficiency could unlock significant value. However, failure to execute on its transformation strategy could result in further value erosion. A comprehensive analysis of Xerox's financial performance, including revenue trends, profitability metrics, and cash flow generation, is essential to determine its intrinsic value. Furthermore, comparing Xerox's valuation multiples to its peers in the IT services and digital solutions sectors can provide insights into its relative attractiveness as an investment.

Investment Thesis

Bull Case: Xerox is poised for a turnaround driven by cost reductions, growth in higher-margin digital services, and strategic acquisitions.

Successful execution of these initiatives will lead to significant earnings growth and a re-rating of the stock.

Bear Case: Xerox will face continued revenue decline and margin pressure due to the secular decline in printing and its inability to adapt to changing market conditions.

High debt levels will further constrain the company's performance, leading to a significant decline in shareholder value.

Conviction: High

2. Business Overview

Xerox Holdings Corporation, a workplace technology company, designs, develops, and sells document management systems and solutions in the United States, Europe, Canada, and internationally. It offers workplace solutions, including desktop monochrome, and color and multifunction printers; digital printing presses and light production devices, and solutions; and digital services that leverage workflow automation, personalization and communication software, content management solutions, and digitization services. The company also provides graphic communications and production solutions; and IT services, end user computing devices, network infrastructure, communications technology, and a range of managed IT solutions, such as technology product support, professional engineering, and commercial robotic process automation. In addition, it provides FreeFlow a portfolio of software solutions for the automation and integration to the processing of print job comprises file preparation, final production, and electronic publishing; XMPie, a personalization and communication software that support the needs of omni-channel communications customers; DocuShare, a content management platform to capture, store, and share paper and digital content; and CareAR, an enterprise augmented reality business. Further, the company sells paper products and wide-format systems. The company sells its products and services directly to its customers through its direct sales force, as well as through independent agents, dealers, value-added resellers, systems integrators, and e-commerce marketplaces. Xerox Holdings Corporation was founded in 1906 and is headquartered in Norwalk, Connecticut.

Competitive Moat (Narrow)

Trend: Stable

Legacy customer base., Integrated hardware and software solutions for document management.

Key Strengths:

Legacy customer base.

Integrated hardware and software solutions for document management.

Growth in the IT services market is generally projected to continue, driven by digital transformation initiatives, cloud adoption, cybersecurity concerns, and the increasing complexity of IT environments. However, the growth rate may vary across different segments. For example, cloud-based services and cybersecurity solutions are likely to experience higher growth than traditional on-premise IT support.

Regulatory Environment:

N/A

4. Financial Analysis

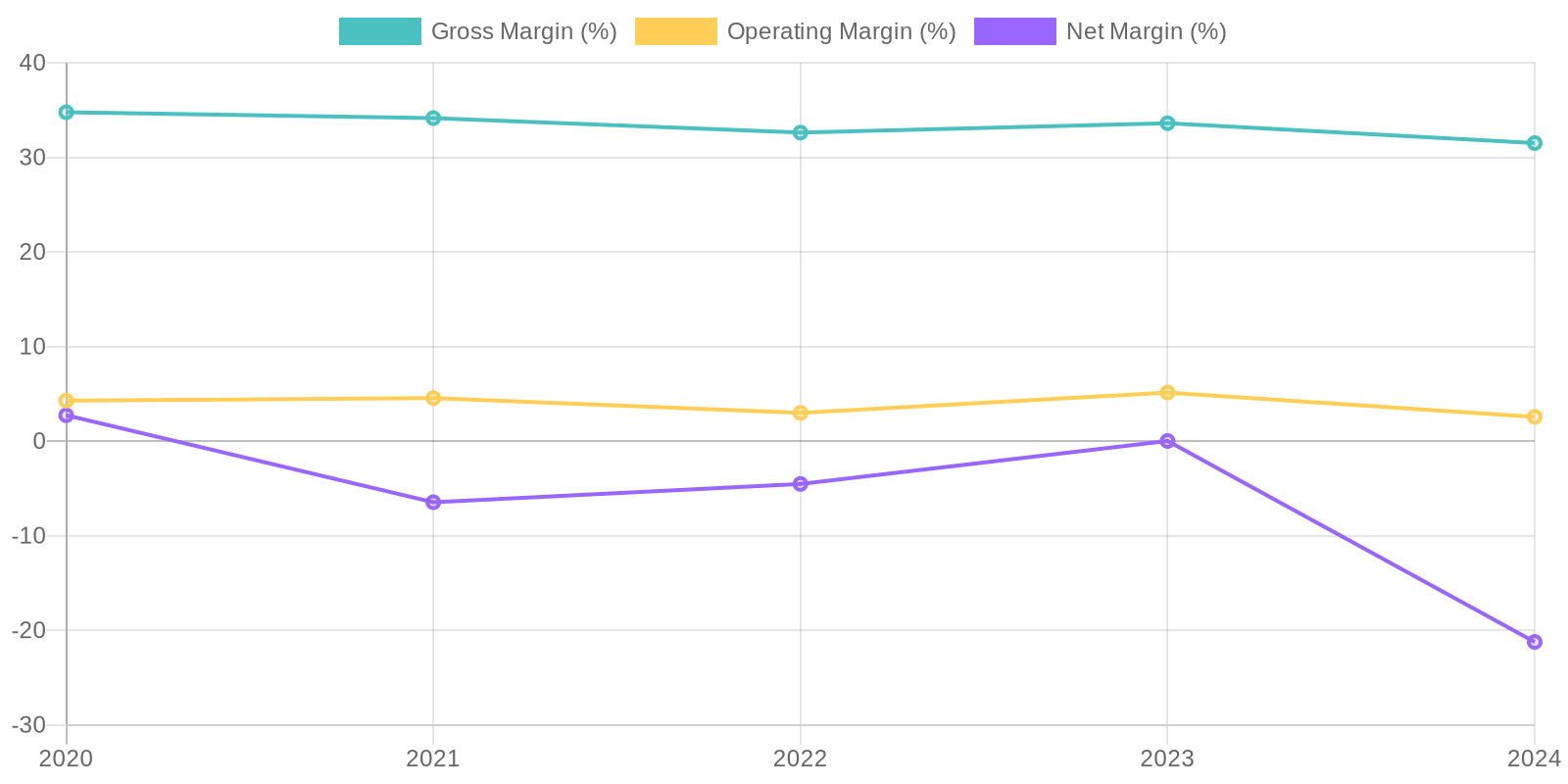

Margin Trend

Calculating ROIC is difficult given the inconsistent profitability. For 2020, ROIC would have been positive, but it has trended downwards since. Return on Equity (ROE) mirrors this trend, with 2024 showing a negative ROE given the net loss and equity base. These metrics indicate declining efficiency in utilizing capital to generate profits.

Revenue Quality

The company's revenue has shown a declining trend over the past five years, indicating potential challenges in maintaining its market position. Although the data does not explicitly detail the recurring nature of revenue, the IT services industry typically benefits from long-term contracts and recurring service agreements, yet the revenue decline suggests potential client attrition or reduced service demand. Further investigation is warranted to understand client concentration and the specific drivers behind the revenue contraction to ensure future sustainability.

Cash Flow & Capital Efficiency

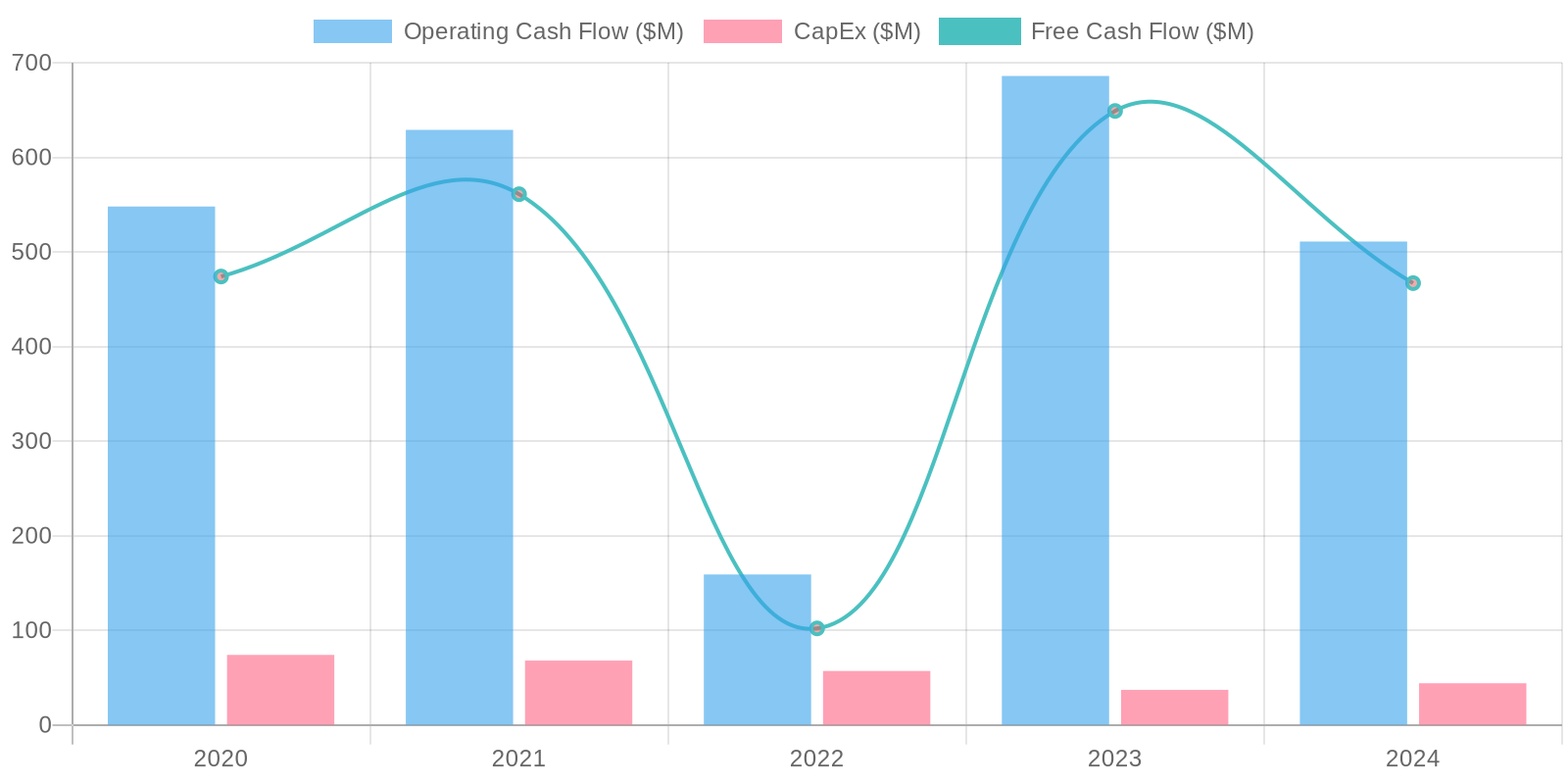

The company's free cash flow (FCF) generation presents a mixed picture. While the company generated $467 million in FCF in 2024, it represents a volatile trend compared to prior years. Capital expenditure appears well-managed, consistently requiring a relatively small portion of operating cash flow. Monitoring the consistency and growth of FCF will be crucial to assess the company's long-term financial health.

Capital Efficiency (ROIC/ROE):

Calculating ROIC is difficult given the inconsistent profitability. For 2020, ROIC would have been positive, but it has trended downwards since. Return on Equity (ROE) mirrors this trend, with 2024 showing a negative ROE given the net loss and equity base. These metrics indicate declining efficiency in utilizing capital to generate profits.

Balance Sheet Health:

The balance sheet reveals increasing reliance on debt, with total debt rising from $4.786 billion in 2020 to $3.588 billion in 2024, heightening financial risk. While current assets exceed current liabilities, the substantial debt burden and negative net income raise concerns about the company's solvency. A substantial portion of assets are tied up in goodwill and intangibles, which may be overvalued and could lead to future write-downs.

5. Management & Governance

CEO Assessment: As of late 2023, Xerox is led by Steven Bandrowczak, who took over as CEO in early 2023. A thorough assessment of his long-term performance would require more time. His immediate focus has been on navigating Xerox through a challenging macroeconomic environment and executing on the company's strategic initiatives.

Capital Allocation: Concern

Insider Ownership: Insider ownership in Xerox is relatively low, suggesting limited direct alignment between the management team's financial interests and those of external shareholders. More details about the exact percentage of insider ownership should be obtained from the latest proxy statements or SEC filings.

Based on the DCF valuation with the above assumptions, the fair value per share is $1.45. This is significantly lower than some previous valuations, reflecting the company's recent negative net income, declining revenue trend and debt burden. The key drivers of this valuation are the conservative revenue growth assumptions and the discount rate, reflecting the risks associated with XRX's turnaround and debt levels.

Scenarios

Scenario

Price Target

Key Assumptions

Bull

High

Xerox is poised for a turnaround driven by cost reductions, growth in higher-margin digital services, and strategic acquisitions.

Successful execution of these initiatives will lead to significant earnings growth and a re-rating of the stock. |

| Base | 1.45 | Xerox will maintain its market position and generate steady free cash flow. While revenue growth will be limited, cost controls and debt reduction will support a modest increase in shareholder value. |

| Bear | Low | Xerox will face continued revenue decline and margin pressure due to the secular decline in printing and its inability to adapt to changing market conditions.

High debt levels will further constrain the company's performance, leading to a significant decline in shareholder value. |

7. Risks

Xerox faces substantial risks due to declining revenue, a significant net loss, high debt, and negative equity. The business model is vulnerable to ongoing digitization trends, and the company's financial health is a major concern. The reliance on legacy printing solutions and potentially overvalued goodwill further exacerbate these risks.

Red Flags:

Significant net loss in the most recent year.

Declining revenue trend over the past five years.

Increasing debt levels raising solvency concerns.

8. Conclusion

Xerox will maintain its market position and generate steady free cash flow. While revenue growth will be limited, cost controls and debt reduction will support a modest increase in shareholder value.

Investment research for informational purposes only. Not financial advice.

Continue Your Research

Return to the Analyst Library or explore the specific financial data for this entity on its profile.

Calculating ROIC is difficult given the inconsistent profitability. For 2020, ROIC would have been positive, but it has trended downwards since. Return on Equity (ROE) mirrors this trend, with 2024 showing a negative ROE given the net loss and equity base. These metrics indicate declining efficiency in utilizing capital to generate profits.

Calculating ROIC is difficult given the inconsistent profitability. For 2020, ROIC would have been positive, but it has trended downwards since. Return on Equity (ROE) mirrors this trend, with 2024 showing a negative ROE given the net loss and equity base. These metrics indicate declining efficiency in utilizing capital to generate profits. The company's free cash flow (FCF) generation presents a mixed picture. While the company generated $467 million in FCF in 2024, it represents a volatile trend compared to prior years. Capital expenditure appears well-managed, consistently requiring a relatively small portion of operating cash flow. Monitoring the consistency and growth of FCF will be crucial to assess the company's long-term financial health.

The company's free cash flow (FCF) generation presents a mixed picture. While the company generated $467 million in FCF in 2024, it represents a volatile trend compared to prior years. Capital expenditure appears well-managed, consistently requiring a relatively small portion of operating cash flow. Monitoring the consistency and growth of FCF will be crucial to assess the company's long-term financial health.