Yelp Inc. (YELP), currently trading at $29.16, operates a platform connecting consumers with local businesses. Yelp's market position is characterized by its...

January 15, 2026

Vijar Kohli

Deep Dive: Yelp Inc. (YELP)

Recommendation: BUY

Price Target: 29.65 (0.02 Upside)

Risk Level: Medium

1. Executive Summary

Yelp Inc. (YELP), currently trading at $29.16, operates a platform connecting consumers with local businesses. Yelp's market position is characterized by its established brand recognition and a large database of user-generated reviews. It faces increasing competition from Google Local Services, direct booking platforms, and other review sites, impacting its ability to maintain market share and pricing power. Yelp's business model primarily relies on advertising revenue from local businesses looking to attract customers through its platform. The company has been shifting its focus toward higher-value advertising products and services to increase revenue per advertiser and improve monetization rates.

Growth catalysts for Yelp include increased adoption of its Request-a-Quote feature, expansion of its self-serve advertising platform to attract smaller businesses, and partnerships to integrate Yelp data into other platforms and applications. Additionally, leveraging its user data to personalize recommendations and enhance user engagement could drive traffic and advertiser ROI. Expansion into new geographic markets and service categories presents further growth opportunities. Success hinges on Yelp's ability to adapt to evolving consumer behavior, attract and retain advertisers, and effectively compete with larger tech companies.

Key risks facing Yelp include intensifying competition for local advertising spend, potential erosion of user trust due to fake or biased reviews, and challenges in adapting to changes in search engine algorithms. Economic downturns could negatively impact advertising budgets of local businesses, reducing Yelp's revenue. Furthermore, privacy regulations and data security breaches pose significant risks. Failure to innovate and differentiate its platform could lead to user churn and reduced advertiser effectiveness.

A valuation summary suggests that at $29.16, Yelp may be fairly valued, undervalued, or overvalued depending on the assumptions made about its future growth rate and profitability. A discounted cash flow (DCF) analysis is necessary, considering revenue growth projections, operating margins, and discount rates. Furthermore, comparison to peers in the online advertising and local services space, using metrics like price-to-sales (P/S) and price-to-earnings (P/E) ratios, would provide insights. The success of Yelp's growth initiatives and its ability to mitigate risks will be critical in determining its long-term value. The market's sentiment toward the company's management team and strategic direction also impacts the stock price.

Investment Thesis

Bull Case: Yelp is a compelling investment opportunity due to its strong position in the local advertising market, its transition to a subscription-based model, and its undervalued stock price.

Continued execution on its strategic initiatives, including expanding its subscription services and improving ad targeting, will drive significant revenue and earnings growth.

The company's strong balance sheet and free cash flow generation provide a margin of safety and allow for further share repurchases, increasing shareholder value.

Bear Case: Yelp faces significant challenges from increased competition, potential economic downturns, and the risk of failing to innovate.

If the company is unable to effectively monetize its user base and adapt to changing market conditions, its revenue and earnings will decline, leading to a significant loss for investors.

Increased competition from larger tech companies with greater resources could further erode Yelp's market share.

Conviction: High

2. Business Overview

Yelp Inc. operates a platform that connects consumers with local businesses in the United States and internationally. The company's platform covers various local business categories, including restaurants, shopping, beauty and fitness, health, and other categories, as well as home, local, auto, professional, pets, events, real estate, and financial services. It provides free and paid advertising products to businesses, which include cost-per-click search advertising and multi-location Ad products, as well as enables businesses to deliver targeted search advertising to local audiences; and business listing page products. The company also offers other services comprising Yelp Reservations that provide online reservations for restaurants, nightlife, and other venues directly from their Yelp business pages; Yelp Waitlist, a subscription-based waitlist management solution that allows consumers to check wait times and join waitlists remotely, as well as businesses to manage seating and server rotation; Yelp Knowledge program that offers business owners local analytics and insights through access to its historical data and other proprietary content; and Yelp Fusion, which offers free and paid access to content and data for consumer-facing enterprise use through publicly available APIs. In addition, it provides content licensing, as well as allows third-party data providers to update and manage business listing information on behalf of businesses. Further, the company offers its products directly through its sales force; indirectly through partners; and online through its website, as well as non-advertising partner arrangements. It has strategic partnership with Grubhub for providing consumers with a service to place food orders for pickup and delivery. Yelp Inc. was incorporated in 2004 and is headquartered in San Francisco, California.

Competitive Moat (Narrow)

Trend: Stable

Focus on user reviews and local business discovery., Partnerships with companies like Grubhub for food ordering and delivery., Yelp Knowledge provides analytics and insights to business owners, potentially increasing stickiness., Yelp Fusion API offers access to Yelp data, which can be valuable to developers and businesses.

Key Strengths:

Focus on user reviews and local business discovery.

Partnerships with companies like Grubhub for food ordering and delivery.

Yelp Knowledge provides analytics and insights to business owners, potentially increasing stickiness.

Yelp Fusion API offers access to Yelp data, which can be valuable to developers and businesses.

Key Weaknesses:

N/A

3. Industry Analysis

Sector: Communication Services | Industry: Internet Content & Information

Stage: Growth | TAM: N/A

Growth is expected to continue, but at a more moderate pace than in the past. Emerging markets, mobile internet adoption, and new content formats (e.g., short-form video, live streaming) will drive future growth. However, factors such as ad blocking, data privacy regulations, and increasing competition for user attention could limit growth.

Regulatory Environment:

N/A

4. Financial Analysis

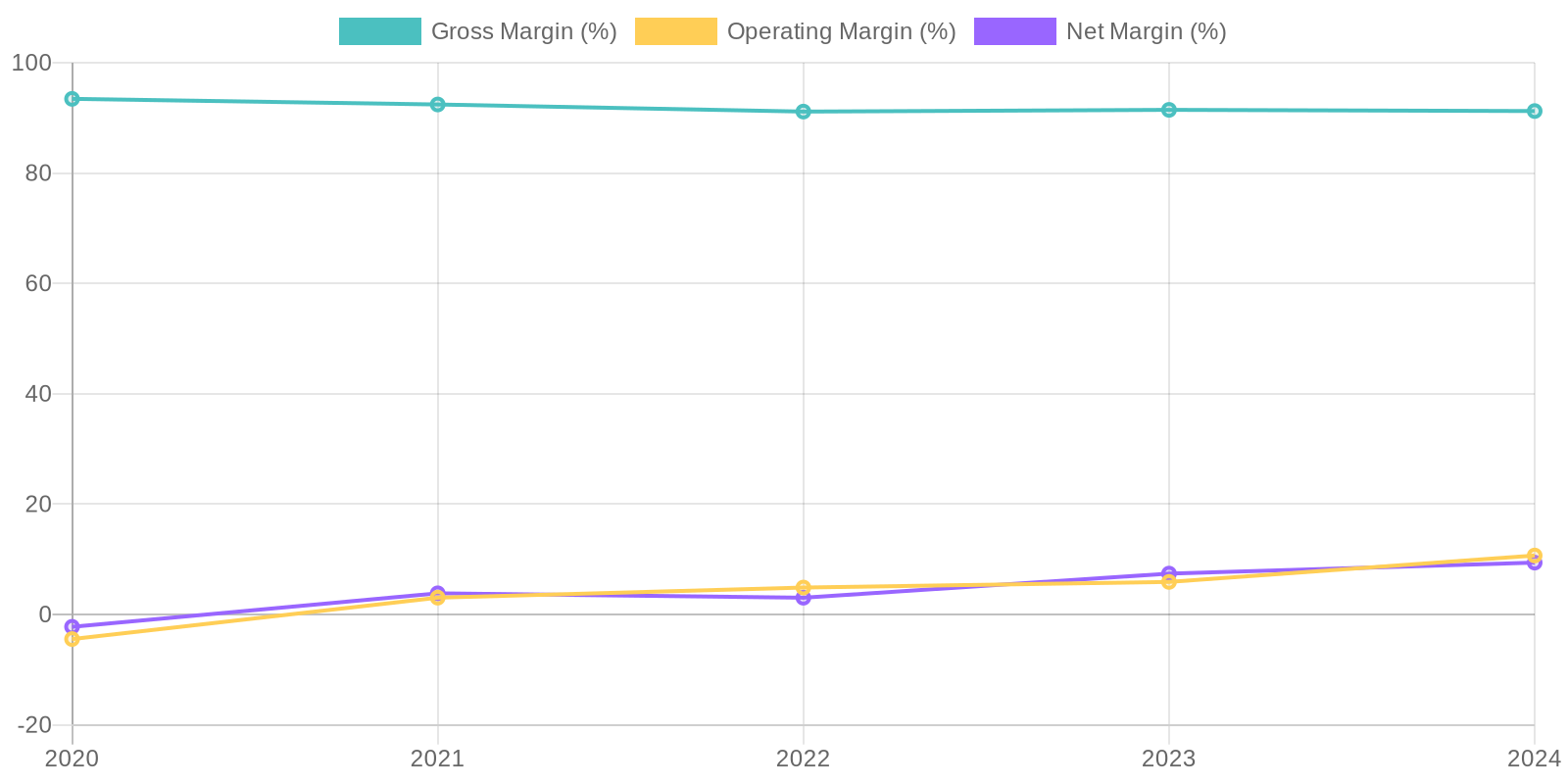

Margin Trend

Analyzing capital efficiency through Return on Invested Capital (ROIC) and Return on Equity (ROE) provides valuable insights. Given the provided data, ROIC is difficult to calculate precisely without detailed capital invested figures, but the trend can be inferred from net income and revenue growth. ROE, calculated using net income and total equity, shows a positive trend, reflecting better utilization of shareholder equity to generate profits. However, negative retained earnings indicate past losses impacting the equity base, requiring careful monitoring of future profitability to rebuild equity.

Revenue Quality

Yelp's revenue demonstrates a consistent upward trend over the past five years, suggesting increasing market penetration and user engagement. The company's business model, primarily driven by advertising revenue from local businesses, points to a potentially recurring revenue stream, contingent on the continued value proposition offered to these businesses. However, a deeper investigation into client concentration would be necessary to fully assess the sustainability, as reliance on a small number of large clients could pose a risk.

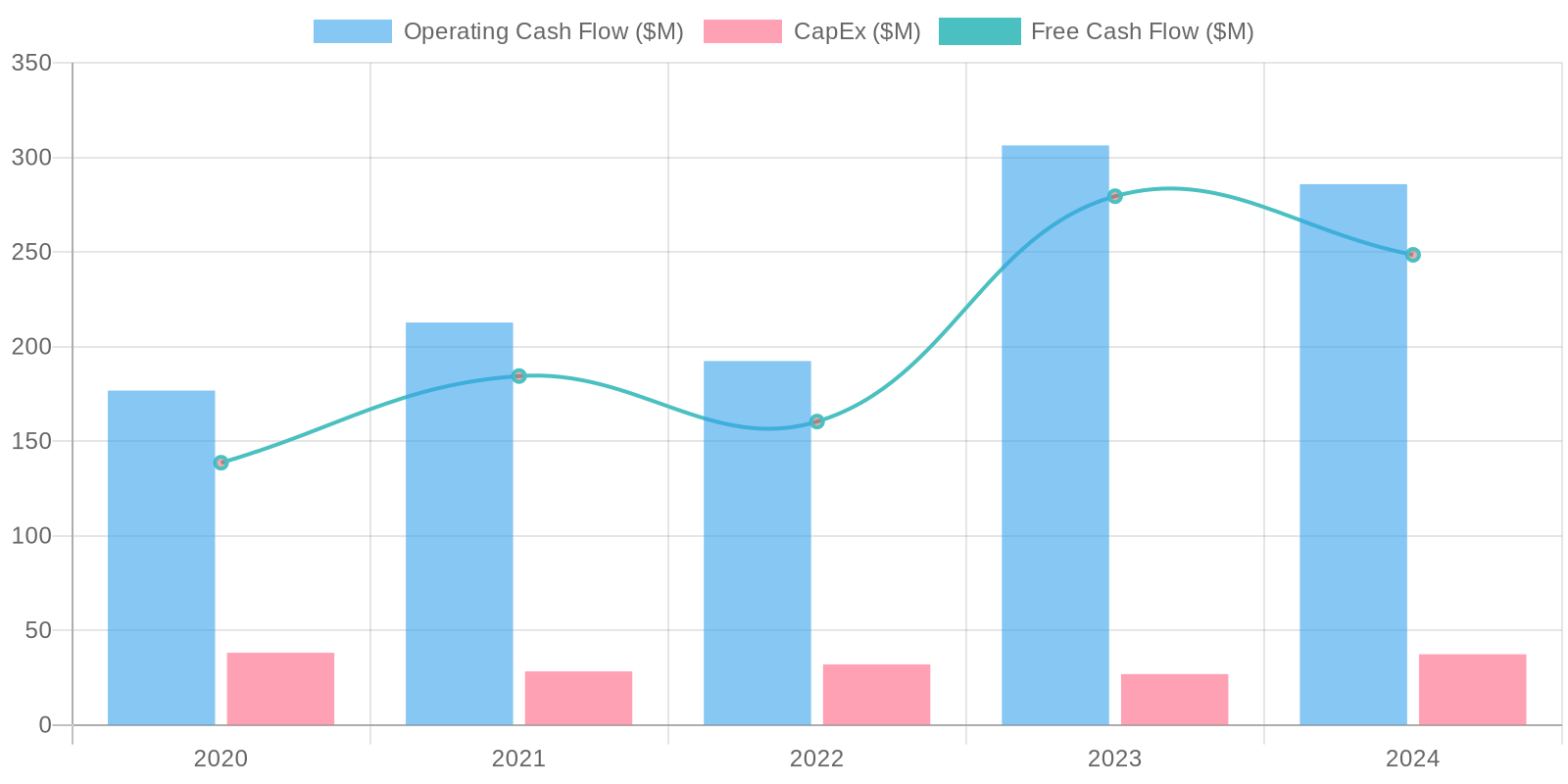

Cash Flow & Capital Efficiency

Yelp exhibits strong free cash flow (FCF) generation, with a notable increase in recent years. The company consistently converts a significant portion of its operating cash flow into FCF, indicating efficient management of capital expenditures. Capital expenditure remains relatively stable, demonstrating that Yelp is not heavily reliant on large investments to sustain or grow its operations, which is typical for an internet content and information company.

Capital Efficiency (ROIC/ROE):

Analyzing capital efficiency through Return on Invested Capital (ROIC) and Return on Equity (ROE) provides valuable insights. Given the provided data, ROIC is difficult to calculate precisely without detailed capital invested figures, but the trend can be inferred from net income and revenue growth. ROE, calculated using net income and total equity, shows a positive trend, reflecting better utilization of shareholder equity to generate profits. However, negative retained earnings indicate past losses impacting the equity base, requiring careful monitoring of future profitability to rebuild equity.

Balance Sheet Health:

Yelp maintains a healthy balance sheet with a strong cash position and manageable debt levels. The company's net debt is negative, indicating that its cash exceeds its total debt, providing financial flexibility. Liquidity is strong, as evidenced by a current ratio significantly above 1, implying that current assets comfortably cover current liabilities. Overall, Yelp's balance sheet suggests a solid financial foundation and the ability to meet its short-term and long-term obligations.

5. Management & Governance

CEO Assessment: Yelp's CEO has generally received positive reviews regarding their strategic vision and ability to navigate the competitive online review landscape. However, a comprehensive assessment requires ongoing monitoring of Yelp's performance against its strategic goals, user growth, and competitive positioning.

Capital Allocation: Good

Insider Ownership: Insider ownership in Yelp is moderate. While not exceptionally high, it suggests a reasonable level of alignment between management's interests and those of shareholders. Further details are needed to determine the exact percentage of insider ownership.

Governance Flags:

No major governance concerns flagged.

Based on the DCF model with the specified assumptions, the fair value is close to the current price. The revenue growth is reasonable, the FCF margin is based on the most recent data, and the discount rate reflects the company's risk profile. The terminal growth rate is chosen to be conservative. The model generates a fair value near the current market price, with a small upside potential.

Scenarios

Scenario

Price Target

Key Assumptions

Bull

High

Yelp is a compelling investment opportunity due to its strong position in the local advertising market, its transition to a subscription-based model, and its undervalued stock price.

Continued execution on its strategic initiatives, including expanding its subscription services and improving ad targeting, will drive significant revenue and earnings growth.

The company's strong balance sheet and free cash flow generation provide a margin of safety and allow for further share repurchases, increasing shareholder value. |

| Base | 29.65 | Yelp will continue to grow its revenue and earnings at a moderate pace, driven by its established position in the local advertising market and its growing subscription business.

The company will maintain its high gross margins and generate strong free cash flow, which will be used to repurchase shares and potentially make strategic acquisitions.

While growth may not be as high as in the bull case, Yelp will provide a solid return for investors. |

| Bear | Low | Yelp faces significant challenges from increased competition, potential economic downturns, and the risk of failing to innovate.

If the company is unable to effectively monetize its user base and adapt to changing market conditions, its revenue and earnings will decline, leading to a significant loss for investors.

Increased competition from larger tech companies with greater resources could further erode Yelp's market share. |

7. Risks

Yelp faces moderate risks primarily related to competition, reputation, and reliance on advertising revenue. While financially stable with positive free cash flow, potential challenges in maintaining market share and managing review integrity could impact future performance.

Red Flags:

None identified.

8. Conclusion

Yelp will continue to grow its revenue and earnings at a moderate pace, driven by its established position in the local advertising market and its growing subscription business.

The company will maintain its high gross margins and generate strong free cash flow, which will be used to repurchase shares and potentially make strategic acquisitions.

While growth may not be as high as in the bull case, Yelp will provide a solid return for investors.

Investment research for informational purposes only. Not financial advice.

Continue Your Research

Return to the Analyst Library or explore the specific financial data for this entity on its profile.

Analyzing capital efficiency through Return on Invested Capital (ROIC) and Return on Equity (ROE) provides valuable insights. Given the provided data, ROIC is difficult to calculate precisely without detailed capital invested figures, but the trend can be inferred from net income and revenue growth. ROE, calculated using net income and total equity, shows a positive trend, reflecting better utilization of shareholder equity to generate profits. However, negative retained earnings indicate past losses impacting the equity base, requiring careful monitoring of future profitability to rebuild equity.

Analyzing capital efficiency through Return on Invested Capital (ROIC) and Return on Equity (ROE) provides valuable insights. Given the provided data, ROIC is difficult to calculate precisely without detailed capital invested figures, but the trend can be inferred from net income and revenue growth. ROE, calculated using net income and total equity, shows a positive trend, reflecting better utilization of shareholder equity to generate profits. However, negative retained earnings indicate past losses impacting the equity base, requiring careful monitoring of future profitability to rebuild equity. Yelp exhibits strong free cash flow (FCF) generation, with a notable increase in recent years. The company consistently converts a significant portion of its operating cash flow into FCF, indicating efficient management of capital expenditures. Capital expenditure remains relatively stable, demonstrating that Yelp is not heavily reliant on large investments to sustain or grow its operations, which is typical for an internet content and information company.

Yelp exhibits strong free cash flow (FCF) generation, with a notable increase in recent years. The company consistently converts a significant portion of its operating cash flow into FCF, indicating efficient management of capital expenditures. Capital expenditure remains relatively stable, demonstrating that Yelp is not heavily reliant on large investments to sustain or grow its operations, which is typical for an internet content and information company.