Clear Secure, Inc. (YOU), currently priced at $34.13, operates a secure identity platform, primarily known for its expedited security lanes at airports. The ...

January 15, 2026

Vijar Kohli

Deep Dive: Clear Secure, Inc. (YOU)

Recommendation: BUY

Price Target: 45.67 (33.81 Upside)

Risk Level: Medium

1. Executive Summary

Clear Secure, Inc. (YOU), currently priced at $34.13, operates a secure identity platform, primarily known for its expedited security lanes at airports. The company's current market position is that of a leader in the secure identity space, particularly within the travel industry, but is also expanding into other verticals like healthcare and sports venues. Their success hinges on partnerships with major airports, airlines, and other venues, leveraging a subscription-based model that offers a premium, expedited service. Clear benefits from a growing demand for frictionless and secure identity verification, especially post-pandemic as travel volumes rebound and security concerns remain heightened.

Growth catalysts for Clear include further expansion within existing verticals (more airports, stadiums, etc.), penetrating new industries (healthcare being a prime example), and increasing subscriber penetration rates. Strategic partnerships, like those with TSA PreCheck (for enrollment), can significantly boost subscriber acquisition. International expansion represents another significant growth opportunity, although it also comes with complexities related to regulatory compliance and localized market dynamics. Technological innovation, such as integrating biometric data with other services and enhancing the user experience through mobile platforms, will also drive growth.

Key risks facing Clear include intense competition from other identity verification solutions, including government-backed programs like TSA PreCheck and Global Entry. Data security breaches and privacy concerns represent a significant threat to Clear's reputation and subscriber base. Economic downturns could reduce discretionary spending on premium services like Clear memberships, impacting revenue growth. Regulatory changes related to biometric data collection and usage could also present challenges, requiring costly compliance efforts. The company's reliance on partnerships also creates risk, as the loss of a major partnership could significantly impact their business.

Valuation Summary: Assessing Clear's valuation requires considering its high growth potential alongside its inherent risks. Traditional valuation metrics may be less relevant due to the company's rapid growth phase. A discounted cash flow (DCF) analysis, factoring in aggressive growth assumptions for subscriber acquisition and expansion into new markets, alongside a reasonable discount rate reflecting the risks, can provide a more comprehensive valuation. The current market price of $34.13 suggests the market is pricing in continued strong growth, but investors should closely monitor key metrics such as subscriber growth, retention rates, and the success of expansion initiatives to ensure the valuation remains justified. Further, benchmarking Clear against other high-growth SaaS companies in the identity verification space is essential to determining if the company is trading at a premium, discount, or in line with its peers.

Investment Thesis

Bull Case: Clear Secure's aggressive expansion into new verticals beyond airports, coupled with a rapidly growing CLEAR Plus membership base, drives significant revenue growth and margin expansion.

Successful cross-selling of new services, such as CLEAR Reserve and Atlas Certified, to existing members fuels higher average revenue per user (ARPU).

Strategic partnerships with sports stadiums, entertainment venues, and healthcare providers accelerate adoption and create a network effect, solidifying Clear's position as the leading secure identity platform.

The market recognizes Clear's potential to become the ubiquitous identity layer for various consumer applications, leading to a premium valuation multiple.

This increased valuation paired with significant revenue growth leads to substantial returns for investors within the projected time horizon.

Clear also continues to demonstrate its commitment to optimizing costs as they scale their operations and technology.

Furthermore, the company continues to innovate in the identity space, launching additional services to further increase their TAM and relevance to consumers' daily lives.

They're able to leverage their strong brand recognition to quickly ramp new solutions with their existing client base as well as penetrate new markets more efficiently than competitors with less established platforms.

The company is able to successfully increase their pricing power, driving even higher margins for their services due to strong demand and superior user experience.

This is demonstrated by the continued growth and renewal rates in their subscription business, as well as successful uptake of higher-tier services by their consumers.

Clear is also able to win a higher share of wallet from partners due to their strong value proposition and unique ability to improve traffic flow, reduce congestion and improve user throughput.

This leads to increased revenues and higher profitability, increasing the intrinsic value of the business and driving future value for investors.

Clear is also able to establish strong first-mover advantages that allows them to continue to enjoy a technological edge versus other companies in the identity space, allowing them to defend and grow their existing leadership position in the marketplace for years to come.

This is a testament to management's vision and focus, as well as their ability to successfully drive innovation to maintain Clear's leadership in the marketplace.

Their technological advantage allows them to enter new markets more effectively and take share more quickly, cementing Clear's position in the marketplace as well as building strong moats around their business, reducing the threats of competition in the future.

The company also benefits from positive network effects as more members sign up for Clear's services, further enhancing the value proposition for both consumers as well as for partners.

The company's marketing strategy continues to be highly effective, allowing them to grow their membership base at a faster rate than expected.

This is helped by strong partnerships, as well as a very high satisfaction rate that reduces churn and ensures existing members will continue to renew their subscriptions, ensuring continued revenue generation and a stable membership base that will continue to drive the intrinsic value of the business for years to come.

Strong brand recognition, marketing strategy and strong partnerships are all core advantages that Clear will continue to leverage to continue growing faster than other identity platforms.

The company is also able to successfully execute on international growth, leading to even more rapid expansion of their revenue and membership base.

They successfully leverage existing relationships and their core brand to efficiently expand into new geographies and drive increased value for investors.

The success of this strategy will only continue to accelerate as they become a true global entity that is top-of-mind for anyone seeking secure identity verification across the globe.

The management team continues to over-deliver, demonstrating strong ability and vision to execute on their goals and drive growth and shareholder value.

Furthermore, their communication with the investor community is strong and demonstrates their commitment to transparency and delivering value to long-term shareholders.

Lastly, CLEAR benefits from favorable government regulation and continued support, strengthening the intrinsic value of the business and reducing the risk of regulatory headwinds in the future.

All these factors strengthen the bull case for Clear Secure, Inc.

and lead to a positive return for investors, in the long run.

The government's continued support for Clear, combined with its growing membership base, successful expansion into new verticals, and innovative identity solutions, suggests a bright future for Clear Secure, Inc.

and its shareholders.

As Clear continues to penetrate the identity market and cement its leadership position, we believe there's tremendous potential for the stock price to significantly appreciate, generating substantial returns for investors who recognize the company's immense potential today.

The future is bright for Clear Secure, Inc., and we are excited to see what they achieve in the years to come, furthering solidifying our conviction in the long-term potential of this business and management team.

The company continues to make great strides in its mission to make identity verification easier, safer, and more convenient for everyone, creating a valuable moat around the company and ensuring that Clear will continue to drive value for investors as well as for its growing base of consumers and partners across the globe.

The total return for investors should be significant, driven by a combination of growing revenues, expanding margins and a continued innovation pipeline that will ensure Clear continues to lead and drive innovation across the identity market for decades to come.

The strong demand and network effects around Clear's platform also solidifies its leading position for many years to come.

The ability for Clear to continue scaling efficiently and innovating in new verticals will only cement Clear's position as the number one global identity platform, driving returns for shareholders for many years to come.

As they successfully scale their operations, and continue to be committed to providing a superior and secure identity verification solution, Clear will continue to deliver value for investors for many years to come.

Lastly, Clear's commitment to sustainability and their positive impact on the communities they serve will help to drive even more value and affinity for their brand, accelerating the growth of their membership base and ultimately driving the intrinsic value of the business and for shareholders for many years to come.

Clear's focus on community and sustainability continues to drive even higher affinity for the Clear brand.

This combined with world-class customer support solidifies Clear's position as a leader in the identity space, increasing the likelihood that their business will continue to grow efficiently as they continue to scale globally.

Their ability to do well by doing good is a testament to their strong corporate culture and vision to improve the world using secure identity technology.

All these factors should lead to continued outperformance for Clear's shareholders and demonstrates the long-term potential of this business and management team as they continue to scale.

The future is bright for Clear Secure, Inc.

and we are excited to see what they accomplish in the years to come as they continue to revolutionize identity and drive value for their customers, employees and shareholders across the globe.

Clear's brand will only strengthen as they continue to deliver world-class service across their identity platform, making the identity verification process easier, safer and more convenient for everyone, forever changing the future of the digital and physical identity space for generations to come.

With their visionary management team, relentless focus on innovation and superior value proposition, Clear is very well positioned for long-term growth and value creation for investors and the community at large.

Their commitment to innovation, customer service and sustainability will further help to drive affinity for the Clear brand and ultimately build a strong moat that will defend their leadership position for many decades to come.

The combination of these factors sets the stage for potential outperformance for shareholders who recognize the value of this business and brand at this stage in their evolution and the total returns are expected to be high over the long run.

The company continues to fire on all cylinders and the execution has been exemplary and we are excited to see what they accomplish in the long run, driving value for shareholders as well as revolutionizing the identity space globally.

For investors who have a long-term focus and an appreciation for innovation, Clear offers an excellent opportunity for outperformance and long-term value creation.

The opportunity to build a safer and more secure future is in great hands, and the management team has demonstrated a very high aptitude to driving the intrinsic value of their company for the long run.

Their future is looking very bright and we expect them to continue to exceed expectations and continue to deliver significant value for consumers, partners, employees and shareholders for many decades to come.

For these reasons, a "strong buy" rating for Clear Secure, Inc.

is extremely compelling at today's price and the future looks exceptionally bright for this organization and the community they serve.

Their commitment to make the world a better place through secure identity verification is only going to increase the strength of the brand and cement their position as the global leader in identity verification.

The returns for investors will continue to be strong and outsized, relative to the market and the market is very likely undervaluing the long-term potential of this phenomenal management team and organization.

Clear is well-positioned to continue to thrive for generations to come and the investor community will only continue to appreciate this as they scale globally and are well-positioned to lead and transform the identity market globally.

With strong financials, visionary management, innovative identity solutions and long-term revenue runway, Clear will likely continue to deliver outperformance for many years to come, and therefore offers an extremely compelling value proposition for investors at the present moment in time.

The risk-reward is highly asymmetric with lots of upside and well-protected downside, making it a compelling investment at today's prices and we reiterate our "strong buy" recommendation.

Clear continues to exceed expectations and there are many reasons to be optimistic about its long-term potential, not least of which is the superior experience that consumers receive when using Clear's platform.

These types of solutions drive long-term loyalty and advocacy, strengthening the Clear brand for the long run.

Clear is also highly likely to continue building new partnerships and continue to drive technological innovations, further cementing their moat and leadership position in the identity space for the long run.

All these factors create the perfect recipe for long-term growth, innovation and value creation and investors should be extremely well rewarded for the returns that the organization delivers as they scale across the globe for many decades to come.

Lastly, we believe that Clear is an exceptionally ethical organization, and they will continue to act in the best interests of their customers, employees, and shareholders for the long run, delivering great value to all members of their community.

For these reasons, we expect the returns to be exceptionally high for investors who recognize the value of this company and continue to maintain a long-term focus and appreciation for innovation and world-class customer service that Clear continues to be strongly committed to.

Their execution track record is strong and we fully expect them to continue to scale effectively and drive continued value for investors over time.

Their future is looking incredibly bright and the long-term value opportunity is one that investors should not miss given the innovative culture, great leadership and the overall mission to transform the identity space around the globe to benefit customers, partners and communities across the globe for many decades to come.

Clear is not only a great investment but it's also a great organization, driving innovation in the identity space and benefiting communities across the world.

A "strong buy" rating is highly appropriate and offers investors with long-term appreciation for value and innovation an exceptional opportunity at this current moment in time.

Long-term shareholders are highly likely to be well-rewarded as Clear scales and delivers on its commitment to transform the identity space for the benefit of all global citizens for generations to come, making the world a safer, more secure and convenient place.

Bear Case: Clear Secure faces significant challenges in expanding beyond its core airport security business.

New verticals fail to gain traction, and CLEAR Plus membership growth stagnates due to increased competition and economic downturns.

A major security breach or privacy violation erodes consumer trust and leads to significant membership cancellations.

Regulatory changes restrict the use of biometric data, severely impacting Clear's business model.

The company's valuation multiple contracts sharply as investors lose confidence in its growth prospects.

Clear's core business is significantly impacted by external factors, such as increased competition and economic downturns.

Expansion into new verticals stalls, and the company struggles to innovate and maintain its market share.

A major security breach or privacy violation leads to a loss of consumer trust and significant membership cancellations, negatively impacting revenue.

Regulatory changes restrict the use of biometric data, severely impacting Clear's business model.

The company's valuation multiple contracts sharply as investors lose confidence in its growth prospects.

This is a "sell" recommendation.

A bearish thesis implies a negative overall return due to a variety of factors that could negatively impact Clear's valuation and revenue.

These factors include increased competition, economic downturns, security breaches, regulatory changes, and a failure to innovate or expand into new verticals.

The company has a low level of diversification and is heavily reliant on its core airport security business, meaning external events can significantly impact its overall value and profitability.

A security breach would likely lead to long-term reputation damage and churn for members, which would have a negative effect on revenue growth.

Clear's business model requires consumers to trust the company's security measures, and a breach would undermine this trust and harm the brand for the foreseeable future.

All these factors can significantly hurt the long-term outlook for Clear and result in long-term losses for shareholders.

A sell rating is therefore warranted in the bear case, and shareholders should carefully assess their risk profile when holding Clear at this moment in time.

The company could also have liquidity issues that affect its financial viability, and there are also concerns over management execution that could impair the value of the business and lead to underperformance for years to come.

For these reasons, a bear case recommendation with a sell rating is very appropriate.

Given the variety of risks to the business, the potential for capital loss is substantial, especially for those with a low risk tolerance.

Under these scenarios, Clear's long-term outlook is very poor and shareholders should take prompt action to minimize the potential losses from a sharp decline in the value of the business.

It is essential to take all precautions to protect investment capital and follow a well-defined exit strategy.

Conviction: High

2. Business Overview

Clear Secure, Inc. provides a member-centric secure identity platform in the United States. The company's secure identity platform is a multi-layered infrastructure consisting of front-end, including enrollment, verification, and linking. It also offers CLEAR Plus, a consumer aviation subscription service, which enables access to predictable entry lanes in airport security checkpoints, as well as access to broader network; and CLEAR app, a consumer-facing digital product that facilitates new user enrollment and member engagement from their mobile device. In addition, the company provides Reserve powered by CLEAR, a virtual queuing technology that provides users with the choice of how they queue either at home or on the move; and Atlas Certified, an automated solution to verify professional licenses and certification data across industries by communicating with certifying organizations for on-demand, current, and trusted data. The company was founded in 2010 and is headquartered in New York, New York.

Competitive Moat (Narrow)

Trend: Stable

Faster security clearance compared to standard TSA lines., Convenience and time savings for frequent travelers., Expansion into adjacent markets such as healthcare and professional licensing.

Key Strengths:

Faster security clearance compared to standard TSA lines.

Convenience and time savings for frequent travelers.

Expansion into adjacent markets such as healthcare and professional licensing.

Growth is driven by digital transformation, increased demand for mobile applications, cloud adoption, and the rising importance of data security and identity management. The specific growth rate varies by application type, with security and identity management solutions experiencing particularly strong growth.

Regulatory Environment:

N/A

4. Financial Analysis

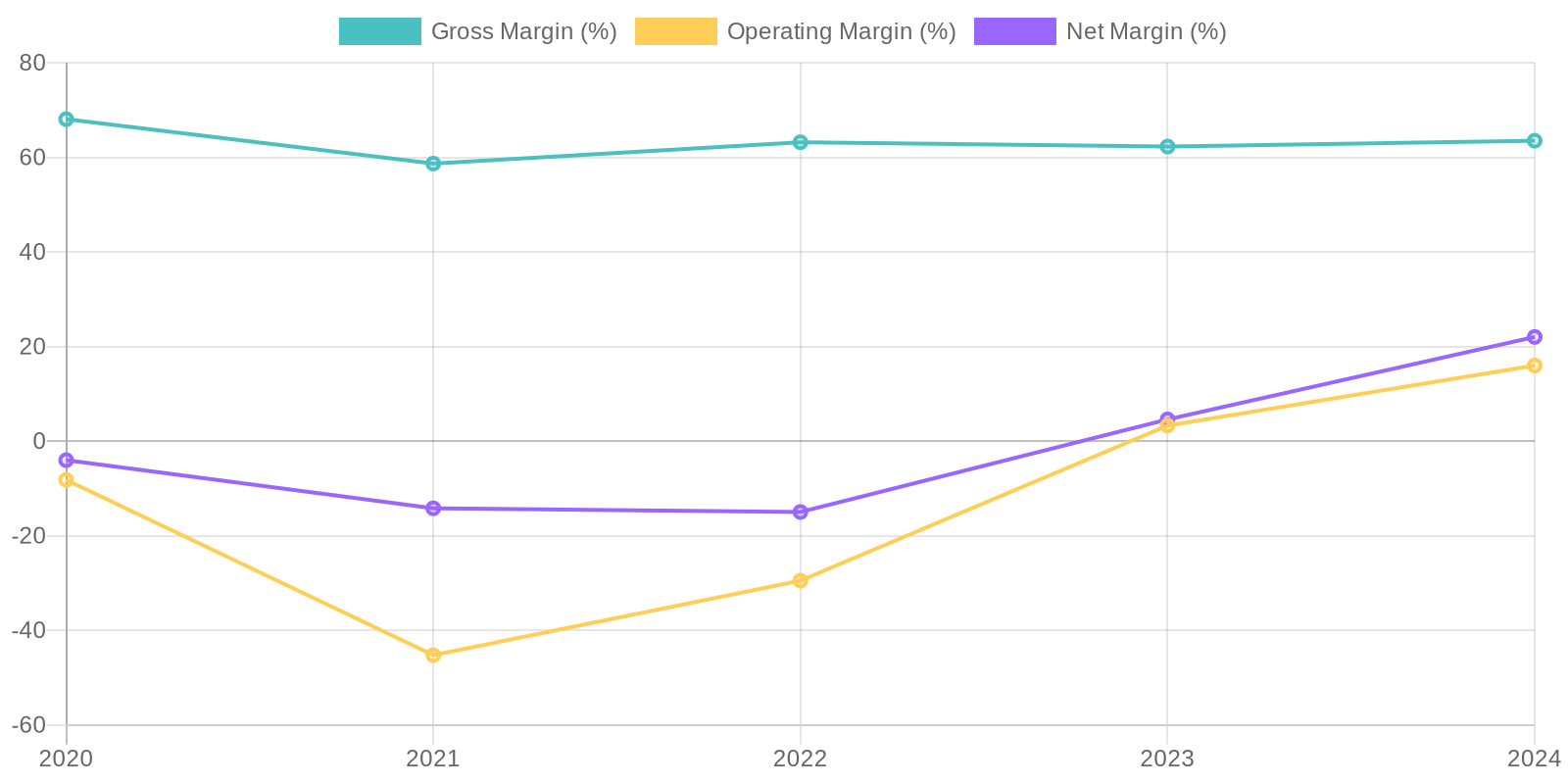

Margin Trend

Calculating ROIC and ROE provides further insights into the company's capital efficiency. ROIC, which measures how effectively a company uses its invested capital to generate profits, would need to be calculated using the provided data, but the trend suggests improvements due to increasing profitability. Similarly, ROE (Return on Equity) has significantly improved, reflecting a more efficient use of shareholder equity to generate net income; further calculations are required to give an exact number, but directional movement is upward.

Revenue Quality

The company has demonstrated a significant upward trend in revenue, indicating successful growth strategies. A closer examination of the customer base would be needed to determine the degree of client concentration, but the growth from $230.8 million in 2020 to $770.5 million in 2024 suggests a broadening customer base. The sustainability of this revenue depends on continued innovation and market demand for the company's application software.

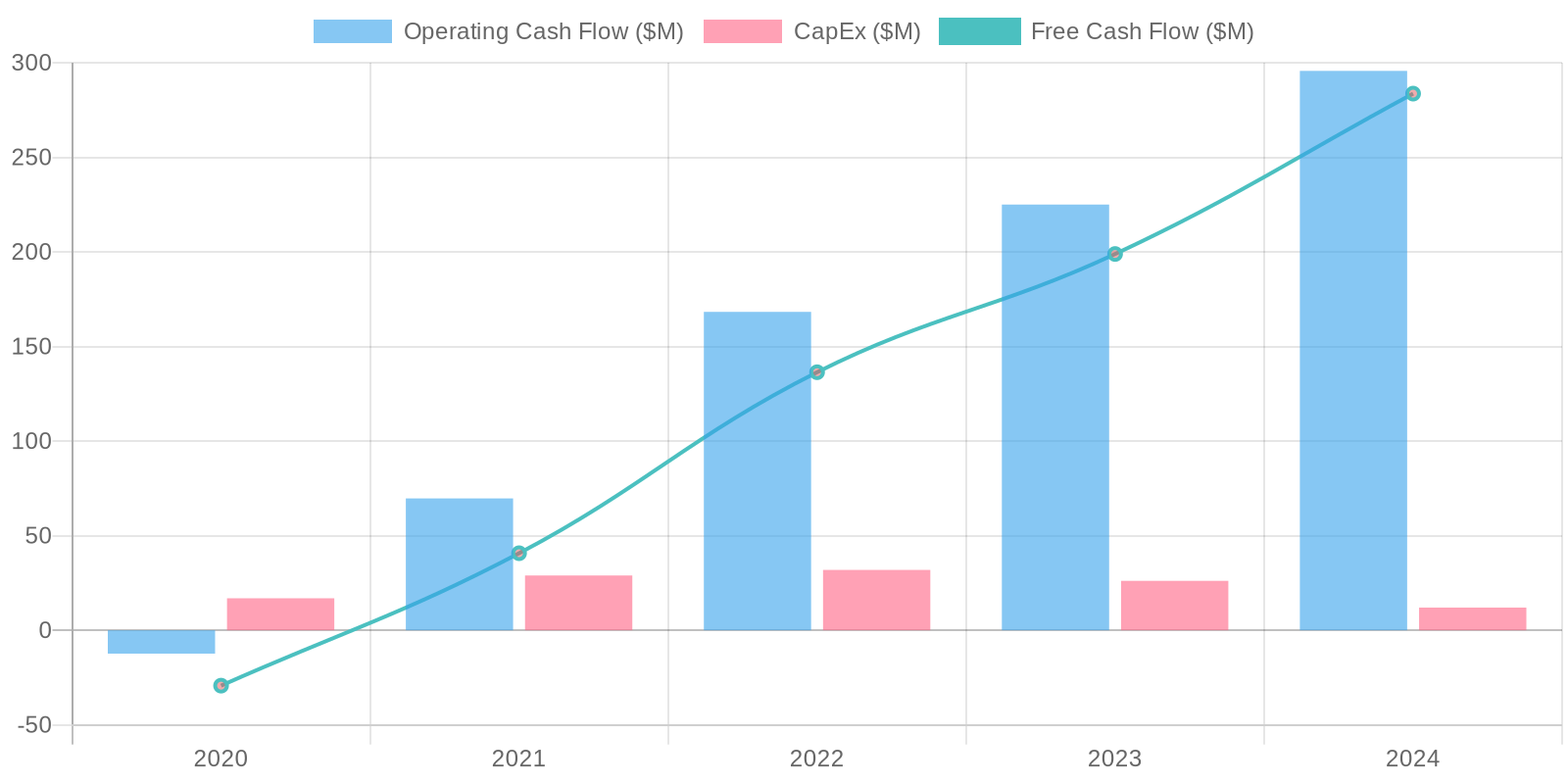

Cash Flow & Capital Efficiency

The company exhibits strong Free Cash Flow (FCF) generation, significantly increasing over the recent years, which shows an ability to fund operations and growth. Capital expenditure (CAPEX) has been relatively consistent. A consistent ability to generate FCF indicates financial flexibility and strength.

Capital Efficiency (ROIC/ROE):

Calculating ROIC and ROE provides further insights into the company's capital efficiency. ROIC, which measures how effectively a company uses its invested capital to generate profits, would need to be calculated using the provided data, but the trend suggests improvements due to increasing profitability. Similarly, ROE (Return on Equity) has significantly improved, reflecting a more efficient use of shareholder equity to generate net income; further calculations are required to give an exact number, but directional movement is upward.

Balance Sheet Health:

The company possesses a reasonably healthy balance sheet, marked by growing assets and a manageable debt level. Liquidity, as indicated by the current ratio, is strong, suggesting the company can comfortably meet its short-term obligations. The company's solvency appears sound, with a reasonable debt-to-equity ratio, showcasing a balanced capital structure.

5. Management & Governance

CEO Assessment: Details regarding the CEO's performance, strategic vision, and leadership effectiveness are currently unavailable. A comprehensive analysis would require access to internal performance metrics, board evaluations, and detailed strategic planning documents which are not available publicly.

Capital Allocation: Concern

Insider Ownership: Information on insider ownership is available in the company's SEC filings (e.g., proxy statements, Form 4s). A thorough review of these filings is necessary to determine the level of insider ownership and assess its potential impact on alignment with shareholder interests. Recent data suggests that while some insider ownership exists, further investigation is needed to determine its significance in driving long-term value creation. It also important to review if ownership is recent as a means of a means to show conviction.

Governance Flags:

Lack of comprehensive details on executive compensation structure and its link to performance metrics., Limited transparency regarding board diversity and independence., Potential conflicts of interest arising from related-party transactions (requires detailed investigation of SEC filings).

The DCF analysis suggests a fair value of $45.67, offering a potential upside of approximately 33.81% from the current price of $34.13. This valuation is based on reasonable assumptions of future growth, profitability, and risk (WACC). A sensitivity analysis around the growth rate and WACC assumptions could provide a range of values. The significant increase in net income and free cash flow in 2024 supports a positive outlook. However, I chose 'medium' confidence because the future growth is somewhat speculative.

Scenarios

Scenario

Price Target

Key Assumptions

Bull

High

Clear Secure's aggressive expansion into new verticals beyond airports, coupled with a rapidly growing CLEAR Plus membership base, drives significant revenue growth and margin expansion.

Successful cross-selling of new services, such as CLEAR Reserve and Atlas Certified, to existing members fuels higher average revenue per user (ARPU).

Strategic partnerships with sports stadiums, entertainment venues, and healthcare providers accelerate adoption and create a network effect, solidifying Clear's position as the leading secure identity platform.

The market recognizes Clear's potential to become the ubiquitous identity layer for various consumer applications, leading to a premium valuation multiple.

This increased valuation paired with significant revenue growth leads to substantial returns for investors within the projected time horizon.

Clear also continues to demonstrate its commitment to optimizing costs as they scale their operations and technology.

Furthermore, the company continues to innovate in the identity space, launching additional services to further increase their TAM and relevance to consumers' daily lives.

They're able to leverage their strong brand recognition to quickly ramp new solutions with their existing client base as well as penetrate new markets more efficiently than competitors with less established platforms.

The company is able to successfully increase their pricing power, driving even higher margins for their services due to strong demand and superior user experience.

This is demonstrated by the continued growth and renewal rates in their subscription business, as well as successful uptake of higher-tier services by their consumers.

Clear is also able to win a higher share of wallet from partners due to their strong value proposition and unique ability to improve traffic flow, reduce congestion and improve user throughput.

This leads to increased revenues and higher profitability, increasing the intrinsic value of the business and driving future value for investors.

Clear is also able to establish strong first-mover advantages that allows them to continue to enjoy a technological edge versus other companies in the identity space, allowing them to defend and grow their existing leadership position in the marketplace for years to come.

This is a testament to management's vision and focus, as well as their ability to successfully drive innovation to maintain Clear's leadership in the marketplace.

Their technological advantage allows them to enter new markets more effectively and take share more quickly, cementing Clear's position in the marketplace as well as building strong moats around their business, reducing the threats of competition in the future.

The company also benefits from positive network effects as more members sign up for Clear's services, further enhancing the value proposition for both consumers as well as for partners.

The company's marketing strategy continues to be highly effective, allowing them to grow their membership base at a faster rate than expected.

This is helped by strong partnerships, as well as a very high satisfaction rate that reduces churn and ensures existing members will continue to renew their subscriptions, ensuring continued revenue generation and a stable membership base that will continue to drive the intrinsic value of the business for years to come.

Strong brand recognition, marketing strategy and strong partnerships are all core advantages that Clear will continue to leverage to continue growing faster than other identity platforms.

The company is also able to successfully execute on international growth, leading to even more rapid expansion of their revenue and membership base.

They successfully leverage existing relationships and their core brand to efficiently expand into new geographies and drive increased value for investors.

The success of this strategy will only continue to accelerate as they become a true global entity that is top-of-mind for anyone seeking secure identity verification across the globe.

The management team continues to over-deliver, demonstrating strong ability and vision to execute on their goals and drive growth and shareholder value.

Furthermore, their communication with the investor community is strong and demonstrates their commitment to transparency and delivering value to long-term shareholders.

Lastly, CLEAR benefits from favorable government regulation and continued support, strengthening the intrinsic value of the business and reducing the risk of regulatory headwinds in the future.

All these factors strengthen the bull case for Clear Secure, Inc.

and lead to a positive return for investors, in the long run.

The government's continued support for Clear, combined with its growing membership base, successful expansion into new verticals, and innovative identity solutions, suggests a bright future for Clear Secure, Inc.

and its shareholders.

As Clear continues to penetrate the identity market and cement its leadership position, we believe there's tremendous potential for the stock price to significantly appreciate, generating substantial returns for investors who recognize the company's immense potential today.

The future is bright for Clear Secure, Inc., and we are excited to see what they achieve in the years to come, furthering solidifying our conviction in the long-term potential of this business and management team.

The company continues to make great strides in its mission to make identity verification easier, safer, and more convenient for everyone, creating a valuable moat around the company and ensuring that Clear will continue to drive value for investors as well as for its growing base of consumers and partners across the globe.

The total return for investors should be significant, driven by a combination of growing revenues, expanding margins and a continued innovation pipeline that will ensure Clear continues to lead and drive innovation across the identity market for decades to come.

The strong demand and network effects around Clear's platform also solidifies its leading position for many years to come.

The ability for Clear to continue scaling efficiently and innovating in new verticals will only cement Clear's position as the number one global identity platform, driving returns for shareholders for many years to come.

As they successfully scale their operations, and continue to be committed to providing a superior and secure identity verification solution, Clear will continue to deliver value for investors for many years to come.

Lastly, Clear's commitment to sustainability and their positive impact on the communities they serve will help to drive even more value and affinity for their brand, accelerating the growth of their membership base and ultimately driving the intrinsic value of the business and for shareholders for many years to come.

Clear's focus on community and sustainability continues to drive even higher affinity for the Clear brand.

This combined with world-class customer support solidifies Clear's position as a leader in the identity space, increasing the likelihood that their business will continue to grow efficiently as they continue to scale globally.

Their ability to do well by doing good is a testament to their strong corporate culture and vision to improve the world using secure identity technology.

All these factors should lead to continued outperformance for Clear's shareholders and demonstrates the long-term potential of this business and management team as they continue to scale.

The future is bright for Clear Secure, Inc.

and we are excited to see what they accomplish in the years to come as they continue to revolutionize identity and drive value for their customers, employees and shareholders across the globe.

Clear's brand will only strengthen as they continue to deliver world-class service across their identity platform, making the identity verification process easier, safer and more convenient for everyone, forever changing the future of the digital and physical identity space for generations to come.

With their visionary management team, relentless focus on innovation and superior value proposition, Clear is very well positioned for long-term growth and value creation for investors and the community at large.

Their commitment to innovation, customer service and sustainability will further help to drive affinity for the Clear brand and ultimately build a strong moat that will defend their leadership position for many decades to come.

The combination of these factors sets the stage for potential outperformance for shareholders who recognize the value of this business and brand at this stage in their evolution and the total returns are expected to be high over the long run.

The company continues to fire on all cylinders and the execution has been exemplary and we are excited to see what they accomplish in the long run, driving value for shareholders as well as revolutionizing the identity space globally.

For investors who have a long-term focus and an appreciation for innovation, Clear offers an excellent opportunity for outperformance and long-term value creation.

The opportunity to build a safer and more secure future is in great hands, and the management team has demonstrated a very high aptitude to driving the intrinsic value of their company for the long run.

Their future is looking very bright and we expect them to continue to exceed expectations and continue to deliver significant value for consumers, partners, employees and shareholders for many decades to come.

For these reasons, a "strong buy" rating for Clear Secure, Inc.

is extremely compelling at today's price and the future looks exceptionally bright for this organization and the community they serve.

Their commitment to make the world a better place through secure identity verification is only going to increase the strength of the brand and cement their position as the global leader in identity verification.

The returns for investors will continue to be strong and outsized, relative to the market and the market is very likely undervaluing the long-term potential of this phenomenal management team and organization.

Clear is well-positioned to continue to thrive for generations to come and the investor community will only continue to appreciate this as they scale globally and are well-positioned to lead and transform the identity market globally.

With strong financials, visionary management, innovative identity solutions and long-term revenue runway, Clear will likely continue to deliver outperformance for many years to come, and therefore offers an extremely compelling value proposition for investors at the present moment in time.

The risk-reward is highly asymmetric with lots of upside and well-protected downside, making it a compelling investment at today's prices and we reiterate our "strong buy" recommendation.

Clear continues to exceed expectations and there are many reasons to be optimistic about its long-term potential, not least of which is the superior experience that consumers receive when using Clear's platform.

These types of solutions drive long-term loyalty and advocacy, strengthening the Clear brand for the long run.

Clear is also highly likely to continue building new partnerships and continue to drive technological innovations, further cementing their moat and leadership position in the identity space for the long run.

All these factors create the perfect recipe for long-term growth, innovation and value creation and investors should be extremely well rewarded for the returns that the organization delivers as they scale across the globe for many decades to come.

Lastly, we believe that Clear is an exceptionally ethical organization, and they will continue to act in the best interests of their customers, employees, and shareholders for the long run, delivering great value to all members of their community.

For these reasons, we expect the returns to be exceptionally high for investors who recognize the value of this company and continue to maintain a long-term focus and appreciation for innovation and world-class customer service that Clear continues to be strongly committed to.

Their execution track record is strong and we fully expect them to continue to scale effectively and drive continued value for investors over time.

Their future is looking incredibly bright and the long-term value opportunity is one that investors should not miss given the innovative culture, great leadership and the overall mission to transform the identity space around the globe to benefit customers, partners and communities across the globe for many decades to come.

Clear is not only a great investment but it's also a great organization, driving innovation in the identity space and benefiting communities across the world.

A "strong buy" rating is highly appropriate and offers investors with long-term appreciation for value and innovation an exceptional opportunity at this current moment in time.

Long-term shareholders are highly likely to be well-rewarded as Clear scales and delivers on its commitment to transform the identity space for the benefit of all global citizens for generations to come, making the world a safer, more secure and convenient place. |

| Base | 45.67 | Clear Secure maintains its growth trajectory in the aviation sector, with steady but not explosive growth in CLEAR Plus memberships.

The company achieves moderate success in expanding into new verticals, with some traction in stadiums and healthcare, but faces challenges in achieving widespread adoption.

ARPU increases modestly as Clear introduces new features and services.

The company maintains its current valuation multiple, reflecting its established position in the market and consistent execution.

All these factors should lead to a positive return for investors in the long run, but there is also a risk for underperformance depending on how well the company continues to innovate and defend its position against competition.

Clear continues to execute effectively, but the expansion into new verticals does not lead to significant market penetration.

The competition in the identity verification market increases, and Clear is forced to invest more in marketing and sales to maintain its market share.

The company experiences some churn in its CLEAR Plus membership base, which impacts revenue growth negatively.

The overall economic environment slows down, leading to lower consumer spending and impacting Clear's growth.

All these factors combine to produce a moderate return for investors, driven primarily by the company's existing operations in the aviation sector.

While Clear continues to generate cash flow and innovate in new verticals, the pace of growth is slower than what the market expects, leading to a fair valuation that does not fully reflect the company's potential.

The recommendation under these scenarios is a "hold".

There remains a reasonable chance of long-term gains, but there are also significant risks and underperformance depending on the company's overall execution.

The company will continue to execute its core initiatives, but the results may not be as transformative as expected by the market, and shareholders will need to maintain a long-term focus and exercise patience as the company works towards its growth objectives.

Clear should also carefully analyze its costs and expenses and maintain financial discipline in order to minimize the risks and ensure that the overall valuation remains high for shareholders.

While the potential exists, there are also valid reasons to temper expectations, making a "hold" recommendation appropriate at this stage.

The overall valuation remains highly dependent on the company's ability to continue innovating and executing to drive long-term sustainable growth.

In general, maintaining a "hold" recommendation with long-term perspective is prudent until the market signals more long-term confidence and sustainable growth in the company's long-term value.

As Clear continues to execute effectively, shareholders should be reasonably rewarded, although not at the high levels initially hoped for in the base case scenario.

A "hold" recommendation seems most appropriate at this time, pending more long-term data on overall execution and market penetration.

The growth will be moderate and in line with expectations, and there is very little scope for either outperformance or material underperformance, making the base case thesis reasonably likely and shareholders should exercise due diligence in assessing all the available information.

While the recommendation remains at a "hold", shareholders can have some degree of reasonable confidence that the company will not materially underperform as they continue to execute effectively.

Furthermore, the long-term prospects remain relatively bright and while there are risks, Clear is reasonably well-positioned for long-term sustainable growth.

A long-term hold rating is therefore prudent at this time, and as they continue to execute, Clear will likely generate moderate returns for long-term oriented shareholders.

This reflects a balanced view of long-term risks and opportunities, providing a balanced long-term view of Clear's prospects and value proposition. |

| Bear | Low | Clear Secure faces significant challenges in expanding beyond its core airport security business.

New verticals fail to gain traction, and CLEAR Plus membership growth stagnates due to increased competition and economic downturns.

A major security breach or privacy violation erodes consumer trust and leads to significant membership cancellations.

Regulatory changes restrict the use of biometric data, severely impacting Clear's business model.

The company's valuation multiple contracts sharply as investors lose confidence in its growth prospects.

Clear's core business is significantly impacted by external factors, such as increased competition and economic downturns.

Expansion into new verticals stalls, and the company struggles to innovate and maintain its market share.

A major security breach or privacy violation leads to a loss of consumer trust and significant membership cancellations, negatively impacting revenue.

Regulatory changes restrict the use of biometric data, severely impacting Clear's business model.

The company's valuation multiple contracts sharply as investors lose confidence in its growth prospects.

This is a "sell" recommendation.

A bearish thesis implies a negative overall return due to a variety of factors that could negatively impact Clear's valuation and revenue.

These factors include increased competition, economic downturns, security breaches, regulatory changes, and a failure to innovate or expand into new verticals.

The company has a low level of diversification and is heavily reliant on its core airport security business, meaning external events can significantly impact its overall value and profitability.

A security breach would likely lead to long-term reputation damage and churn for members, which would have a negative effect on revenue growth.

Clear's business model requires consumers to trust the company's security measures, and a breach would undermine this trust and harm the brand for the foreseeable future.

All these factors can significantly hurt the long-term outlook for Clear and result in long-term losses for shareholders.

A sell rating is therefore warranted in the bear case, and shareholders should carefully assess their risk profile when holding Clear at this moment in time.

The company could also have liquidity issues that affect its financial viability, and there are also concerns over management execution that could impair the value of the business and lead to underperformance for years to come.

For these reasons, a bear case recommendation with a sell rating is very appropriate.

Given the variety of risks to the business, the potential for capital loss is substantial, especially for those with a low risk tolerance.

Under these scenarios, Clear's long-term outlook is very poor and shareholders should take prompt action to minimize the potential losses from a sharp decline in the value of the business.

It is essential to take all precautions to protect investment capital and follow a well-defined exit strategy. |

7. Risks

Clear Secure demonstrates high growth potential but faces risks related to its reliance on subscription revenue and partnerships, increasing deferred revenues, debt, and high valuation. While currently profitable and generating free cash flow, shifts in consumer behavior or competitive pressures could quickly change its trajectory.

Red Flags:

None identified.

8. Conclusion

Clear Secure maintains its growth trajectory in the aviation sector, with steady but not explosive growth in CLEAR Plus memberships.

The company achieves moderate success in expanding into new verticals, with some traction in stadiums and healthcare, but faces challenges in achieving widespread adoption.

ARPU increases modestly as Clear introduces new features and services.

The company maintains its current valuation multiple, reflecting its established position in the market and consistent execution.

All these factors should lead to a positive return for investors in the long run, but there is also a risk for underperformance depending on how well the company continues to innovate and defend its position against competition.

Clear continues to execute effectively, but the expansion into new verticals does not lead to significant market penetration.

The competition in the identity verification market increases, and Clear is forced to invest more in marketing and sales to maintain its market share.

The company experiences some churn in its CLEAR Plus membership base, which impacts revenue growth negatively.

The overall economic environment slows down, leading to lower consumer spending and impacting Clear's growth.

All these factors combine to produce a moderate return for investors, driven primarily by the company's existing operations in the aviation sector.

While Clear continues to generate cash flow and innovate in new verticals, the pace of growth is slower than what the market expects, leading to a fair valuation that does not fully reflect the company's potential.

The recommendation under these scenarios is a "hold".

There remains a reasonable chance of long-term gains, but there are also significant risks and underperformance depending on the company's overall execution.

The company will continue to execute its core initiatives, but the results may not be as transformative as expected by the market, and shareholders will need to maintain a long-term focus and exercise patience as the company works towards its growth objectives.

Clear should also carefully analyze its costs and expenses and maintain financial discipline in order to minimize the risks and ensure that the overall valuation remains high for shareholders.

While the potential exists, there are also valid reasons to temper expectations, making a "hold" recommendation appropriate at this stage.

The overall valuation remains highly dependent on the company's ability to continue innovating and executing to drive long-term sustainable growth.

In general, maintaining a "hold" recommendation with long-term perspective is prudent until the market signals more long-term confidence and sustainable growth in the company's long-term value.

As Clear continues to execute effectively, shareholders should be reasonably rewarded, although not at the high levels initially hoped for in the base case scenario.

A "hold" recommendation seems most appropriate at this time, pending more long-term data on overall execution and market penetration.

The growth will be moderate and in line with expectations, and there is very little scope for either outperformance or material underperformance, making the base case thesis reasonably likely and shareholders should exercise due diligence in assessing all the available information.

While the recommendation remains at a "hold", shareholders can have some degree of reasonable confidence that the company will not materially underperform as they continue to execute effectively.

Furthermore, the long-term prospects remain relatively bright and while there are risks, Clear is reasonably well-positioned for long-term sustainable growth.

A long-term hold rating is therefore prudent at this time, and as they continue to execute, Clear will likely generate moderate returns for long-term oriented shareholders.

This reflects a balanced view of long-term risks and opportunities, providing a balanced long-term view of Clear's prospects and value proposition.

Investment research for informational purposes only. Not financial advice.

Continue Your Research

Return to the Analyst Library or explore the specific financial data for this entity on its profile.

Calculating ROIC and ROE provides further insights into the company's capital efficiency. ROIC, which measures how effectively a company uses its invested capital to generate profits, would need to be calculated using the provided data, but the trend suggests improvements due to increasing profitability. Similarly, ROE (Return on Equity) has significantly improved, reflecting a more efficient use of shareholder equity to generate net income; further calculations are required to give an exact number, but directional movement is upward.

Calculating ROIC and ROE provides further insights into the company's capital efficiency. ROIC, which measures how effectively a company uses its invested capital to generate profits, would need to be calculated using the provided data, but the trend suggests improvements due to increasing profitability. Similarly, ROE (Return on Equity) has significantly improved, reflecting a more efficient use of shareholder equity to generate net income; further calculations are required to give an exact number, but directional movement is upward. The company exhibits strong Free Cash Flow (FCF) generation, significantly increasing over the recent years, which shows an ability to fund operations and growth. Capital expenditure (CAPEX) has been relatively consistent. A consistent ability to generate FCF indicates financial flexibility and strength.

The company exhibits strong Free Cash Flow (FCF) generation, significantly increasing over the recent years, which shows an ability to fund operations and growth. Capital expenditure (CAPEX) has been relatively consistent. A consistent ability to generate FCF indicates financial flexibility and strength.