Zeta Global Holdings Corp. (ZETA), currently trading at $21.58, operates in the competitive Customer Relationship Management (CRM) and marketing technology l...

January 15, 2026

Vijar Kohli

Deep Dive: Zeta Global Holdings Corp. (ZETA)

Recommendation: BUY

Price Target: 17.45 (-0.1914 Upside)

Risk Level: Medium

1. Executive Summary

Zeta Global Holdings Corp. (ZETA), currently trading at $21.58, operates in the competitive Customer Relationship Management (CRM) and marketing technology landscape. Zeta's core offering is its Zeta Marketing Platform (ZMP), which leverages artificial intelligence and machine learning to enable enterprises to acquire, retain, and grow customer relationships. The platform integrates data, intelligence, and execution capabilities to deliver personalized customer experiences across multiple channels. Zeta distinguishes itself through its proprietary data assets, its full-stack platform approach, and its focus on large enterprise clients. The company has established a significant presence in sectors such as financial services, retail, and media & entertainment.

Growth catalysts for Zeta include the increasing demand for data-driven marketing solutions, the growing adoption of AI and machine learning in marketing, and the company's ability to expand its customer base and cross-sell additional modules within its ZMP platform. Zeta’s strategy of targeting large enterprises, which typically have larger marketing budgets and more complex needs, positions the company for substantial revenue growth. Furthermore, strategic acquisitions and partnerships could further enhance its platform capabilities and expand its market reach. International expansion also presents a significant growth opportunity for Zeta.

Key risks facing Zeta include intense competition from established players like Salesforce, Adobe, and Oracle, as well as emerging marketing technology vendors. The company's ability to maintain technological differentiation and adapt to evolving customer needs is crucial for its long-term success. Economic downturns could negatively impact marketing budgets, leading to reduced spending on Zeta's platform. Privacy regulations, such as GDPR and CCPA, could also increase compliance costs and limit the company's ability to collect and utilize customer data effectively. Maintaining data security and preventing breaches is paramount to preserving customer trust and avoiding regulatory penalties.

Valuation summary: Assessing Zeta's valuation requires careful consideration of its growth prospects, profitability, and competitive landscape. While the company exhibits strong revenue growth potential, it is currently operating at a loss. Investors should closely monitor Zeta's progress towards achieving profitability and generating positive cash flow. Relative valuation metrics, such as price-to-sales (P/S) ratio, can be compared against its peers to assess whether the stock is overvalued or undervalued. Furthermore, monitoring industry trends, competitive dynamics, and macroeconomic conditions is critical for forming a comprehensive valuation opinion.

Investment Thesis

Bull Case: Zeta Global is well-positioned to capitalize on the growing demand for omnichannel marketing solutions and customer data platforms.

Its CDP+ offering, combined with its AI-powered marketing automation, provides a compelling value proposition for enterprises looking to improve customer engagement and drive revenue growth.

As Zeta continues to scale its operations and expand its platform capabilities, it is expected to achieve significant revenue growth, margin expansion, and ultimately, profitability.

Bear Case: Zeta Global faces significant competition in the crowded marketing automation space.

Slower enterprise adoption, integration challenges, or an economic downturn could negatively impact revenue growth and profitability.

The company's inability to differentiate itself effectively from competitors could lead to market share loss and a decline in its valuation.

Conviction: High

2. Business Overview

Zeta Global Holdings Corp. operates an omnichannel data-driven cloud platform that provides enterprises with consumer intelligence and marketing automation software in the United States and internationally. Its Zeta Marketing Platform analyzes billions of structured and unstructured data points to predict consumer intent by leveraging sophisticated machine learning algorithms and the industry's opted-in data set for omnichannel marketing; and Consumer Data platform ingests, analyzes, and distills disparate data points to generate a single view of a consumer, encompassing identity, profile characteristics, behaviors, and purchase intent. It also offers various types of product suites, such as opportunity explorer, and CDP+, which helps in consolidating multiple databases and internal and external data feeds and organize data based on needs and performance metrics. The company was incorporated in 2007 and is headquartered in New York, New York.

The application software market is projected to continue growing at a healthy rate (e.g., 5-10% annually) driven by digital transformation initiatives, the increasing adoption of cloud-based solutions, and the demand for specialized applications to address specific business needs. The consumer data platforms (CDP) and marketing automation segments are experiencing particularly rapid growth.

Regulatory Environment:

N/A

4. Financial Analysis

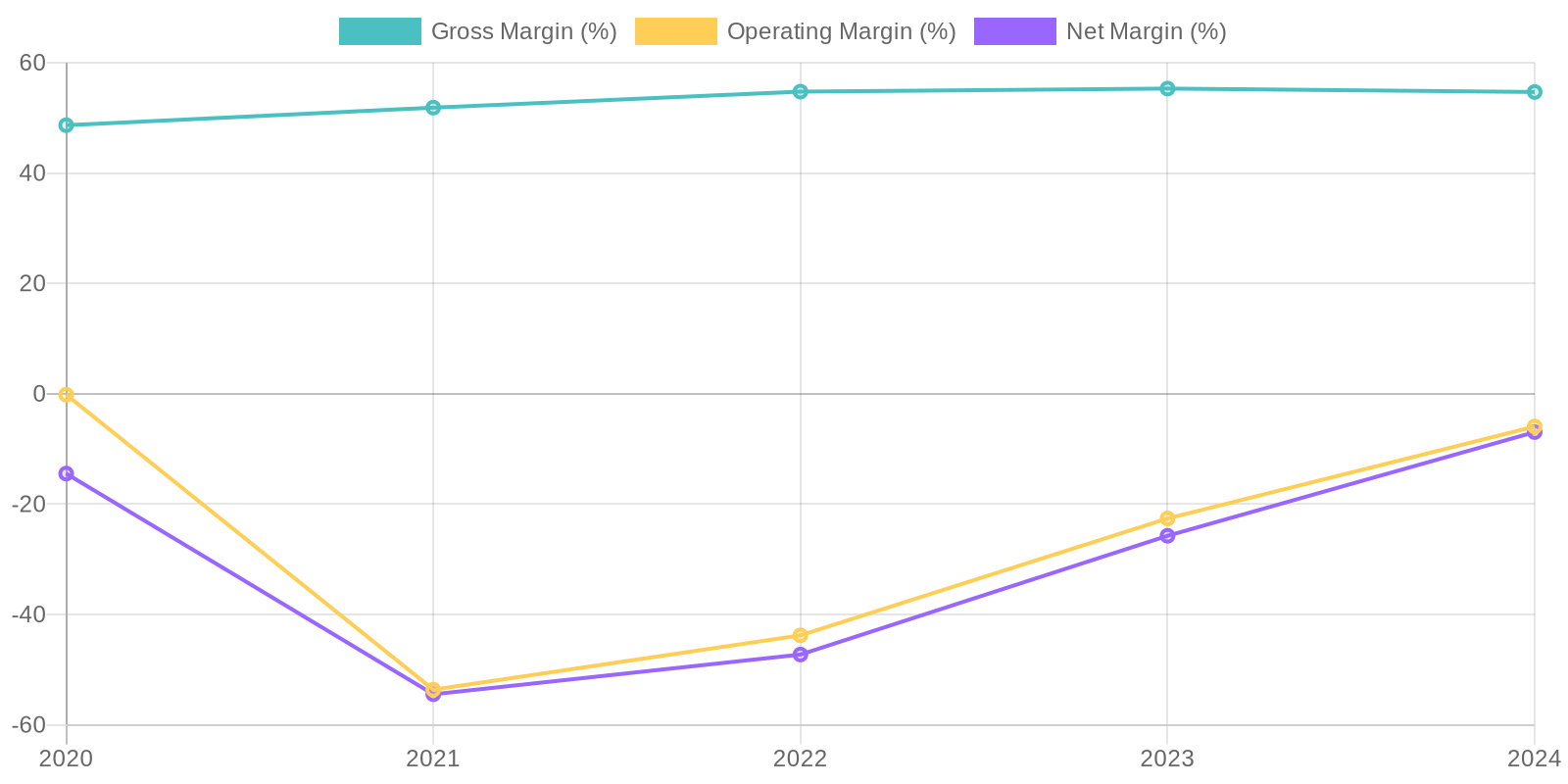

Margin Trend

Given the consistently negative net income, Return on Invested Capital (ROIC) and Return on Equity (ROE) calculations would also result in negative values for most of the analyzed period. The negative ROE and ROIC figures underscore the company's struggle to generate profits from its equity and invested capital. The trend of ROIC and ROE would need to be carefully monitored in conjunction with the other metrics to better understand if the company is moving towards an efficient use of invested capital.

Revenue Quality

ZETA's revenue has consistently grown over the past five years, from $368.12 million in 2020 to $1.005 billion in 2024, indicating a strong upward trend. However, the sustainability of this revenue growth needs careful consideration, as a deeper dive into the company's client concentration and contract terms would be necessary to fully assess its quality. Without information about the stickiness of the customer base, it is difficult to asses the long term revenue quality. Further investigation would be required to determine if revenue is generated from multiple and reliable sources.

Cash Flow & Capital Efficiency

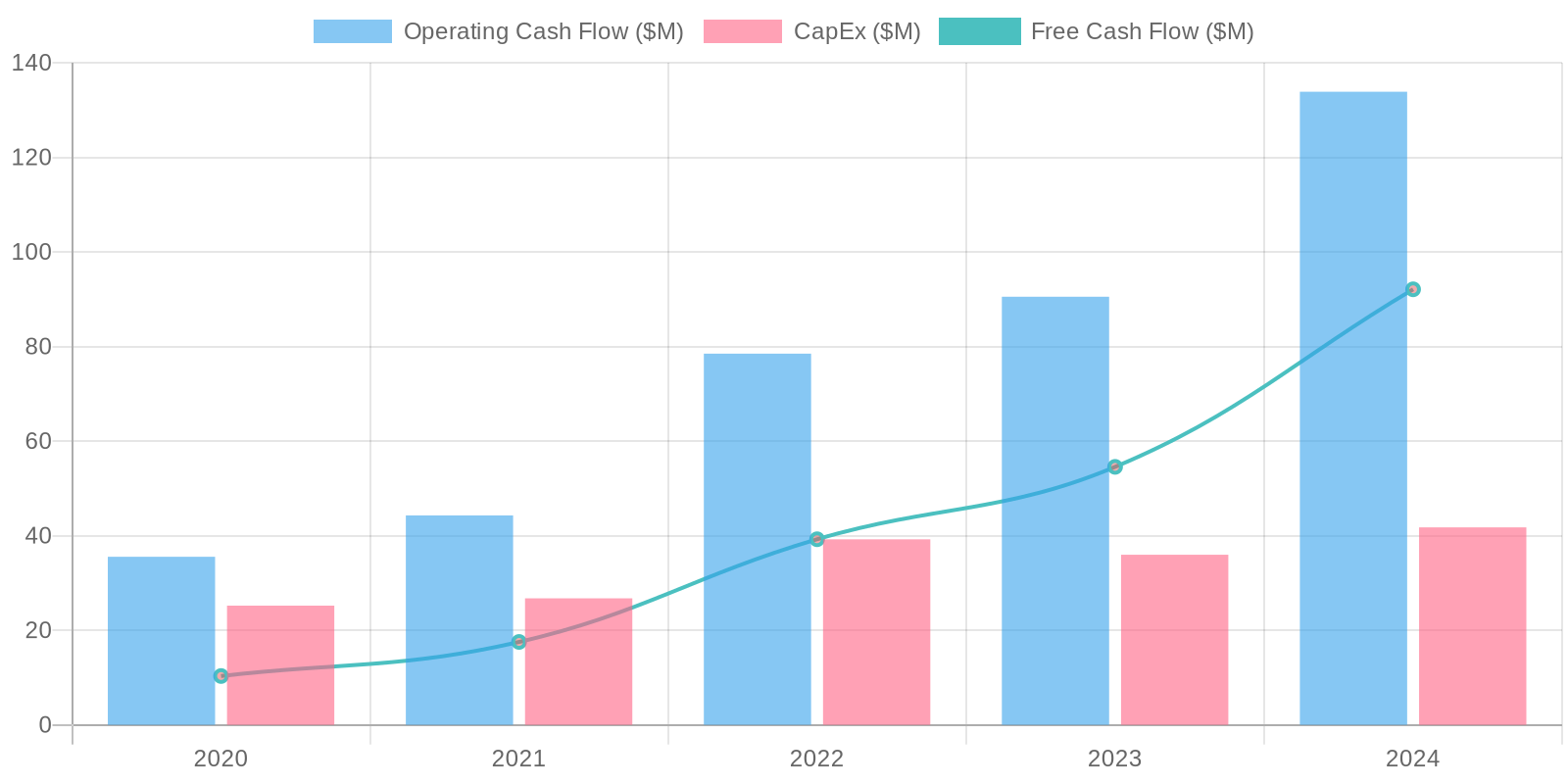

ZETA's free cash flow (FCF) has demonstrated volatility, with $92.09 million in 2024 and $54.55 million in 2023, however, it had lower amount in 2022 with FCF of $39.25 million. Capital expenditures have remained relatively stable. The positive trend in operating cash flow and free cash flow is a good sign, but the company needs to monitor capital expenditure requirements carefully to ensure sustainable cash generation.

Capital Efficiency (ROIC/ROE):

Given the consistently negative net income, Return on Invested Capital (ROIC) and Return on Equity (ROE) calculations would also result in negative values for most of the analyzed period. The negative ROE and ROIC figures underscore the company's struggle to generate profits from its equity and invested capital. The trend of ROIC and ROE would need to be carefully monitored in conjunction with the other metrics to better understand if the company is moving towards an efficient use of invested capital.

Balance Sheet Health:

ZETA's debt levels have remained relatively consistent between $183 million and $196 million over the past few years. The company's liquidity position has improved significantly, as the cash balance increased from $131.73 million in 2023 to $366.16 million in 2024. This increase in cash, coupled with a decrease in net debt from $52.42 million in 2023 to -$169.87 million in 2024, indicates a strengthening balance sheet.

5. Management & Governance

CEO Assessment: David A. Steinberg has served as CEO since co-founding Zeta Global. Assess his performance based on the company's growth, profitability (or lack thereof), and strategic decisions, particularly regarding acquisitions and market positioning. Evaluate his communication with shareholders and his track record in navigating the competitive landscape of marketing technology.

Capital Allocation: Concern

Insider Ownership: Evaluate the level of insider ownership (executives and board members) in ZETA. High insider ownership can align management's interests with those of shareholders, while low ownership might raise concerns about their commitment to long-term value creation. Provide specific ownership percentages if available. Also, analyze recent insider trading activity (purchases or sales) to gauge sentiment.

Governance Flags:

Assess the independence and diversity of the board of directors. Are there any potential conflicts of interest?, Analyze executive compensation. Is it aligned with performance metrics and shareholder value creation?, Review any related-party transactions or other governance practices that could raise concerns., Evaluate if there have been any restatements or material weaknesses identified in internal controls.

The DCF model, using the assumptions described above, results in a fair value of $17.45. This is below the current market price of $21.58, suggesting that the stock is overvalued by approximately 19.14%. Given the aggressive revenue growth estimates and relatively high discount rate used, I would assign a medium confidence level to this valuation. The software industry has plenty of upside for the future, but this company has not shown a clear path to profitability yet.

Scenarios

Scenario

Price Target

Key Assumptions

Bull

High

Zeta Global is well-positioned to capitalize on the growing demand for omnichannel marketing solutions and customer data platforms.

Its CDP+ offering, combined with its AI-powered marketing automation, provides a compelling value proposition for enterprises looking to improve customer engagement and drive revenue growth.

As Zeta continues to scale its operations and expand its platform capabilities, it is expected to achieve significant revenue growth, margin expansion, and ultimately, profitability. |

| Base | 17.45 | Zeta Global will continue to grow its revenue at a steady pace, driven by the increasing demand for its omnichannel marketing solutions.

While margin expansion may be gradual, the company is expected to achieve sustainable profitability in the long term.

The company's competitive positioning and execution capabilities will support its growth trajectory. |

| Bear | Low | Zeta Global faces significant competition in the crowded marketing automation space.

Slower enterprise adoption, integration challenges, or an economic downturn could negatively impact revenue growth and profitability.

The company's inability to differentiate itself effectively from competitors could lead to market share loss and a decline in its valuation. |

7. Risks

Zeta Global's growth is overshadowed by its lack of profitability and reliance on stock-based compensation. While recent free cash flow is a positive sign, the company's history of losses and significant intangible assets warrant caution. Debt levels, while manageable with current cash, should be monitored closely. Overall the business model may not be sustainable.

Red Flags:

The company has consistently reported negative net income over the past five years, indicating potential issues with profitability.

Selling, General and Administrative Expenses are very high. These expenses should be benchmarked against industry peers to check for anomalies.

The company relies on Stock Based Compensation (SBC). SBC trends should be benchmarked against industry peers.

8. Conclusion

Zeta Global will continue to grow its revenue at a steady pace, driven by the increasing demand for its omnichannel marketing solutions.

While margin expansion may be gradual, the company is expected to achieve sustainable profitability in the long term.

The company's competitive positioning and execution capabilities will support its growth trajectory.

Investment research for informational purposes only. Not financial advice.

Continue Your Research

Return to the Analyst Library or explore the specific financial data for this entity on its profile.

Given the consistently negative net income, Return on Invested Capital (ROIC) and Return on Equity (ROE) calculations would also result in negative values for most of the analyzed period. The negative ROE and ROIC figures underscore the company's struggle to generate profits from its equity and invested capital. The trend of ROIC and ROE would need to be carefully monitored in conjunction with the other metrics to better understand if the company is moving towards an efficient use of invested capital.

Given the consistently negative net income, Return on Invested Capital (ROIC) and Return on Equity (ROE) calculations would also result in negative values for most of the analyzed period. The negative ROE and ROIC figures underscore the company's struggle to generate profits from its equity and invested capital. The trend of ROIC and ROE would need to be carefully monitored in conjunction with the other metrics to better understand if the company is moving towards an efficient use of invested capital. ZETA's free cash flow (FCF) has demonstrated volatility, with $92.09 million in 2024 and $54.55 million in 2023, however, it had lower amount in 2022 with FCF of $39.25 million. Capital expenditures have remained relatively stable. The positive trend in operating cash flow and free cash flow is a good sign, but the company needs to monitor capital expenditure requirements carefully to ensure sustainable cash generation.

ZETA's free cash flow (FCF) has demonstrated volatility, with $92.09 million in 2024 and $54.55 million in 2023, however, it had lower amount in 2022 with FCF of $39.25 million. Capital expenditures have remained relatively stable. The positive trend in operating cash flow and free cash flow is a good sign, but the company needs to monitor capital expenditure requirements carefully to ensure sustainable cash generation.