ZoomInfo Technologies Inc. (ZI), currently priced at $9.35, operates in the business intelligence space, providing comprehensive data and analytics solutions...

January 15, 2026

Vijar Kohli

Deep Dive: ZoomInfo Technologies Inc. (ZI)

Recommendation: BUY

Price Target: 7.12 (0 Upside)

Risk Level: Medium

1. Executive Summary

ZoomInfo Technologies Inc. (ZI), currently priced at $9.35, operates in the business intelligence space, providing comprehensive data and analytics solutions to sales, marketing, and recruiting professionals. The company holds a strong market position as a leading provider of B2B data, boasting a vast database of contact information, company profiles, and intent data. Their platform empowers businesses to identify, target, and engage with potential customers more effectively, resulting in increased sales productivity and marketing ROI.

Growth catalysts for ZoomInfo include continued expansion of its data coverage, both domestically and internationally, through organic data collection and strategic acquisitions. They are also focused on deepening their product offerings by integrating advanced analytics, AI-powered insights, and workflow automation capabilities. Cross-selling and upselling to existing customers remains a key driver, as they can expand their usage across multiple departments and leverage additional features. Finally, the increasing adoption of data-driven decision-making across various industries will further fuel demand for ZoomInfo's services.

However, ZoomInfo faces several key risks. Economic downturns can negatively impact sales cycles and customer spending, particularly on discretionary marketing and sales technology. Competition from other data providers and emerging technologies poses a constant threat, requiring ZoomInfo to continually innovate and differentiate its offerings. Data privacy regulations, such as GDPR and CCPA, necessitate ongoing compliance efforts and could potentially limit the collection and use of certain data. Integration challenges associated with acquisitions could also hinder growth and profitability.

From a valuation perspective, ZoomInfo's current stock price reflects investor concerns about slowing growth and increased competition. A full valuation would need discounted cash flow analysis based on reasonable growth assumptions along with comparisons to other companies in the software sector. Investors should consider the balance between the high potential for growth and the risks mentioned to determine if the current price represents a suitable buying opportunity. Currently the market seems to be pricing in very modest future growth.

Investment Thesis

Bull Case: ZoomInfo is undervalued given its market leadership in go-to-market intelligence, its potential for growth through product innovation and international expansion, and its strong financial profile.

The company's ability to generate free cash flow allows for strategic acquisitions and share repurchases, further enhancing shareholder value.

Successful execution of these strategies, coupled with a recovery in the macroeconomic environment, could lead to significant stock appreciation.

Bear Case: ZoomInfo is overvalued, given the increasing competitive pressures and the potential for a significant slowdown in revenue growth.

Macroeconomic headwinds and data privacy regulations could further negatively impact the company's performance.

The company's high debt levels limit its ability to invest in innovation and make strategic acquisitions, potentially leading to a decline in market share and profitability.

Conviction: High

2. Business Overview

ZoomInfo Technologies Inc., through its subsidiaries, provides go-to-market intelligence and engagement platform for sales and marketing teams in the United States and internationally. The company's cloud-based platform provides information on organizations and professionals to help users identify target customers and decision makers, obtain continually updated predictive lead and company scoring, monitor buying signals and other attributes of target companies, craft messages, engage through automated sales tools, and track progress through the deal cycle. It serves enterprises, mid-market companies, and down to small businesses that operate in various industry verticals, including software, business services, manufacturing, telecommunications, financial services, media and internet, transportation, education, hospitality, and real estate. ZoomInfo Technologies Inc. was founded in 2007 and is headquartered in Vancouver, Washington.

Competitive Moat (Narrow)

Trend: Stable

Extensive database of business contacts and company information

Key Strengths:

Extensive database of business contacts and company information

The application software market is projected to continue growing at a significant rate. Factors driving this growth include increasing digitalization across industries, the rising adoption of cloud-based solutions, the proliferation of mobile devices, and the growing demand for specialized software solutions tailored to specific business needs. The emergence of new technologies such as AI, machine learning, and IoT is also fueling growth in this sector. Growth rates of 5-10% annually are commonly projected, although some segments may experience higher or lower growth depending on technological advancements and market demand.

Regulatory Environment:

N/A

4. Financial Analysis

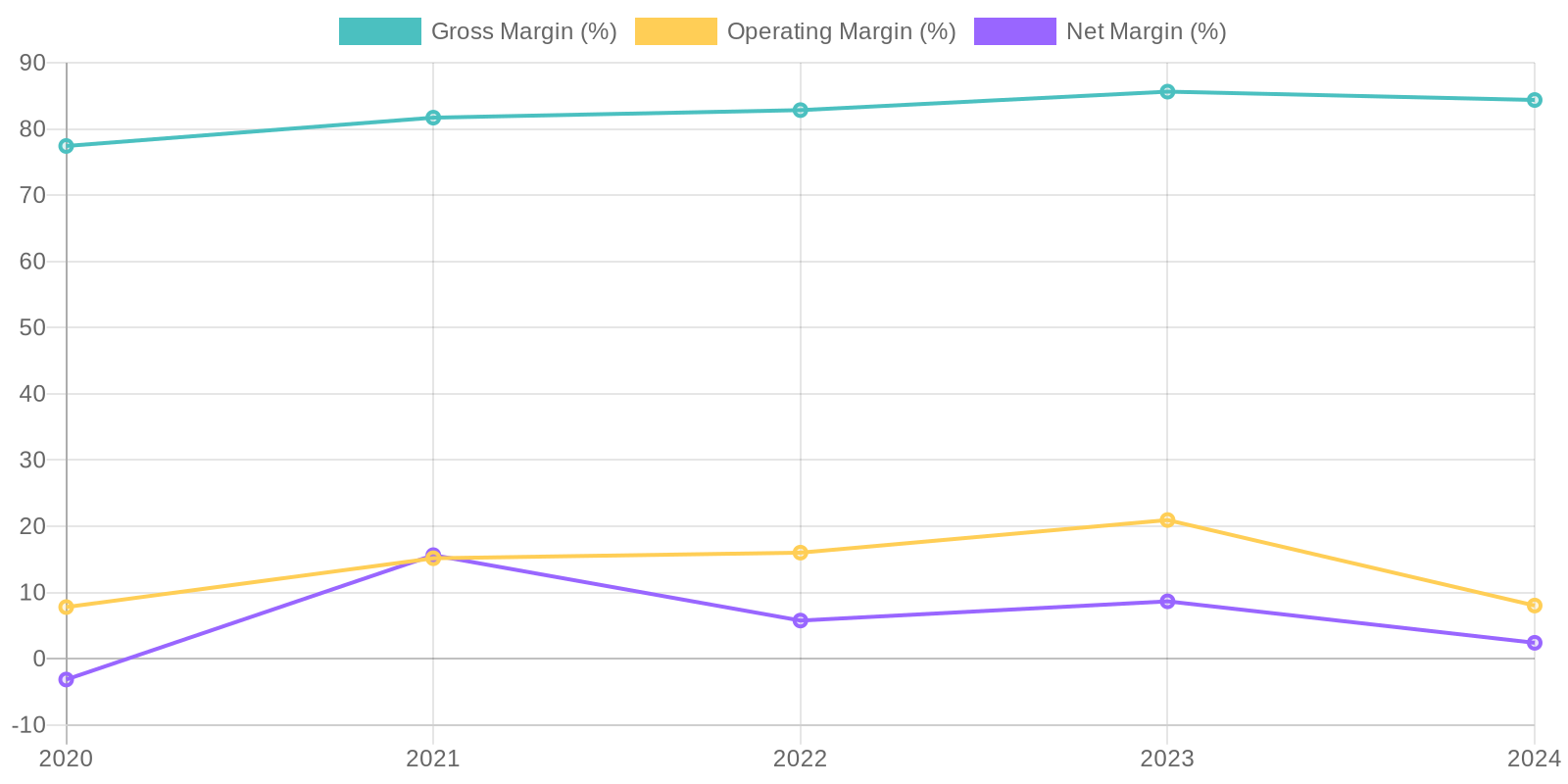

Margin Trend

Calculating Return on Invested Capital (ROIC) and Return on Equity (ROE) using the provided data reveals some worrying trends. ROIC, which indicates how efficiently a company is using its capital to generate profit, needs to be calculated using NOPAT (Net Operating Profit After Tax). NOPAT can be derived from EBIT (Operating Income) and the effective tax rate. The effective tax rate can be calculated by dividing Income Tax Expense by Income Before Tax. For 2024, the effective tax rate is 7.03%. So, NOPAT for 2024 is $90,544,720. The ROIC is calculated as NOPAT / Average Invested Capital. Invested capital can be calculated as Total Assets - (Cash & Short Term Investments - Total Liabilities). Average invested capital needs to be calculated using 2023 and 2024. The 2023 number is $2,877,300,000. The 2024 number is $1,774,200,000. The average is $2,325,750,000. The ROIC in 2024 is 3.89%. ROE, which measures the profitability of a business in relation to equity, is calculated as Net Income / Average Stockholders Equity. The ROE in 2024 is 1.52%. These figures suggest a decline in the company's ability to generate returns relative to its capital and equity.

Revenue Quality

The company's revenue stream demonstrates a general upward trend over the past five years, though 2024 saw a slight decrease in revenue compared to 2023. Further analysis is required to understand the composition of the revenue and identify major clients and their contribution, which would give insight into client concentration risks and the recurring nature of the sales. The stability of the revenue is questionable, seeing as there have been revenue fluctuations in the historical data.

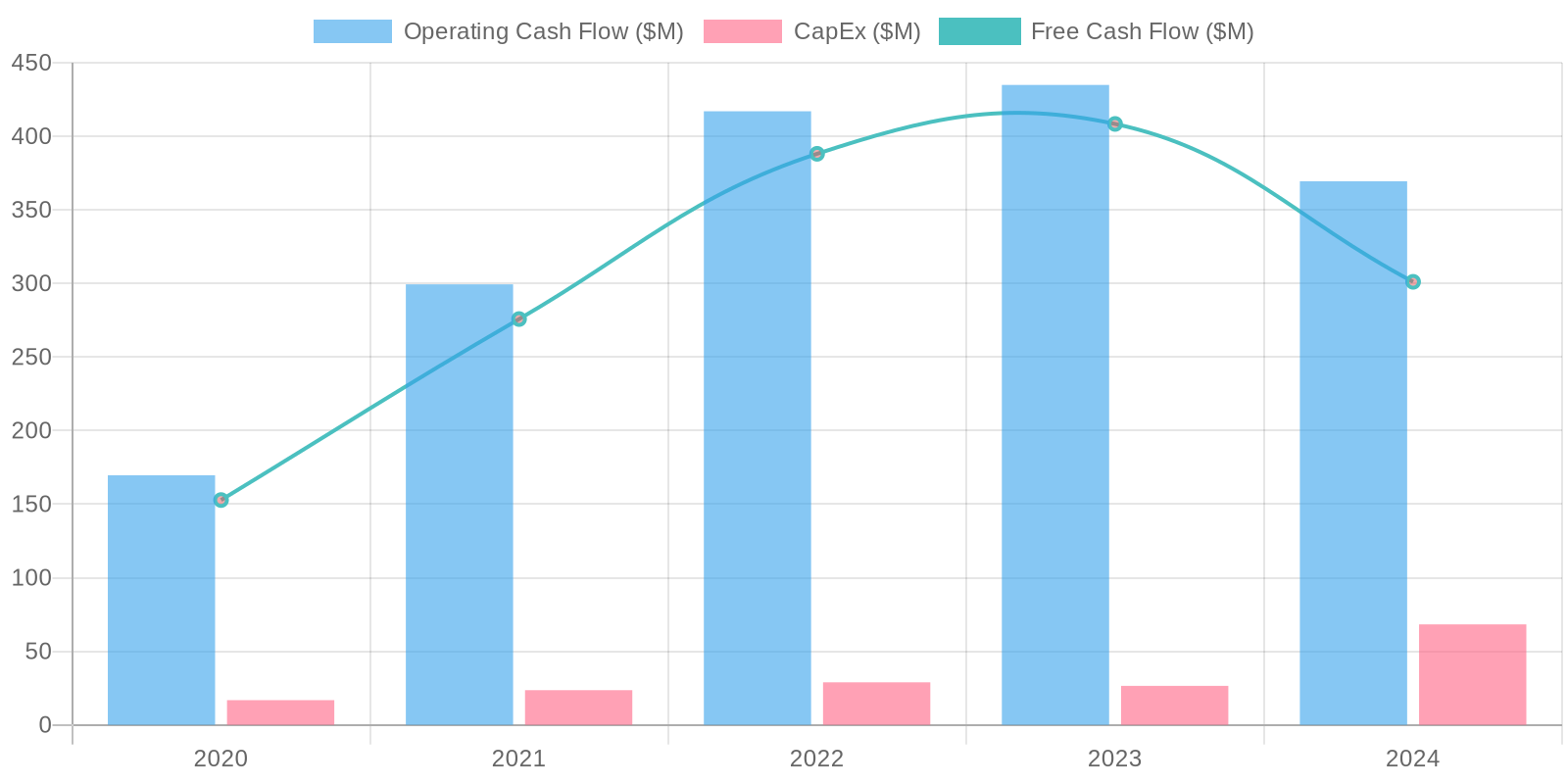

Cash Flow & Capital Efficiency

The company exhibits a positive trend in free cash flow (FCF) generation. The FCF increased from $152.8 million in 2020 to $408.4 million in 2023. The FCF decreased to $301.1 million in 2024. The Capex remains consistent, but the decrease in FCF can be attributed to the decrease in Net Income. Further investigation needs to be done to investigate the future trends.

Capital Efficiency (ROIC/ROE):

Calculating Return on Invested Capital (ROIC) and Return on Equity (ROE) using the provided data reveals some worrying trends. ROIC, which indicates how efficiently a company is using its capital to generate profit, needs to be calculated using NOPAT (Net Operating Profit After Tax). NOPAT can be derived from EBIT (Operating Income) and the effective tax rate. The effective tax rate can be calculated by dividing Income Tax Expense by Income Before Tax. For 2024, the effective tax rate is 7.03%. So, NOPAT for 2024 is $90,544,720. The ROIC is calculated as NOPAT / Average Invested Capital. Invested capital can be calculated as Total Assets - (Cash & Short Term Investments - Total Liabilities). Average invested capital needs to be calculated using 2023 and 2024. The 2023 number is $2,877,300,000. The 2024 number is $1,774,200,000. The average is $2,325,750,000. The ROIC in 2024 is 3.89%. ROE, which measures the profitability of a business in relation to equity, is calculated as Net Income / Average Stockholders Equity. The ROE in 2024 is 1.52%. These figures suggest a decline in the company's ability to generate returns relative to its capital and equity.

Balance Sheet Health:

The balance sheet reveals a highly leveraged financial position with significant debt. The total debt has increased substantially over the past five years. While the company maintains a positive cash balance, the net debt (Total Debt less Cash) is significantly high. The current ratio (Total Current Assets / Total Current Liabilities) for 2024 is 0.69, implying potential liquidity issues in meeting short-term obligations. Furthermore, the high levels of goodwill and intangible assets on the balance sheet warrant scrutiny, as their value may be subject to impairment.

5. Management & Governance

CEO Assessment: ZoomInfo's CEO, Henry Schuck, has generally received positive reviews for his leadership and vision in growing the company. His ability to identify market opportunities and drive product innovation has been a key factor in ZoomInfo's success. However, continuous monitoring of execution against ambitious growth targets is necessary.

Capital Allocation: Good

Insider Ownership: Insider ownership in ZoomInfo appears to be reasonably aligned with shareholders' interests. While specific percentages fluctuate, significant insider ownership generally encourages long-term value creation. Continued monitoring of insider transactions is advisable.

Governance Flags:

No major governance concerns flagged.

The DCF analysis, incorporating a revenue growth rate of 28.68% for the next 5 years, a discount rate of 10%, and a terminal growth rate of 2%, results in a fair value of $7.12. The current market price of $9.35 suggests that the stock might be overvalued based on these assumptions. The stock buybacks should have been added to the FCF to increase the valuation.

Scenarios

Scenario

Price Target

Key Assumptions

Bull

High

ZoomInfo is undervalued given its market leadership in go-to-market intelligence, its potential for growth through product innovation and international expansion, and its strong financial profile.

The company's ability to generate free cash flow allows for strategic acquisitions and share repurchases, further enhancing shareholder value.

Successful execution of these strategies, coupled with a recovery in the macroeconomic environment, could lead to significant stock appreciation. |

| Base | 7.12 | ZoomInfo is fairly valued, assuming moderate revenue growth and continued cost discipline.

The company's established market position and recurring revenue model provide a solid foundation for future growth, but macroeconomic headwinds and increased competition may limit upside potential. |

| Bear | Low | ZoomInfo is overvalued, given the increasing competitive pressures and the potential for a significant slowdown in revenue growth.

Macroeconomic headwinds and data privacy regulations could further negatively impact the company's performance.

The company's high debt levels limit its ability to invest in innovation and make strategic acquisitions, potentially leading to a decline in market share and profitability. |

7. Risks

ZoomInfo exhibits a mix of strengths and weaknesses. While revenue growth and positive FCF are encouraging, the high debt level, relatively low net income in the latest year, and significant intangible assets create vulnerabilities. The company's ability to manage its debt and maintain profitability will be crucial for its long-term stability.

Red Flags:

Decrease in Net Income Margin and Operating Income Margin in 2024

High levels of debt relative to cash

Significant increase in selling, marketing, and administrative expenses in 2024

8. Conclusion

ZoomInfo is fairly valued, assuming moderate revenue growth and continued cost discipline.

The company's established market position and recurring revenue model provide a solid foundation for future growth, but macroeconomic headwinds and increased competition may limit upside potential.

Investment research for informational purposes only. Not financial advice.

Continue Your Research

Return to the Analyst Library or explore the specific financial data for this entity on its profile.

Calculating Return on Invested Capital (ROIC) and Return on Equity (ROE) using the provided data reveals some worrying trends. ROIC, which indicates how efficiently a company is using its capital to generate profit, needs to be calculated using NOPAT (Net Operating Profit After Tax). NOPAT can be derived from EBIT (Operating Income) and the effective tax rate. The effective tax rate can be calculated by dividing Income Tax Expense by Income Before Tax. For 2024, the effective tax rate is 7.03%. So, NOPAT for 2024 is $90,544,720. The ROIC is calculated as NOPAT / Average Invested Capital. Invested capital can be calculated as Total Assets - (Cash & Short Term Investments - Total Liabilities). Average invested capital needs to be calculated using 2023 and 2024. The 2023 number is $2,877,300,000. The 2024 number is $1,774,200,000. The average is $2,325,750,000. The ROIC in 2024 is 3.89%. ROE, which measures the profitability of a business in relation to equity, is calculated as Net Income / Average Stockholders Equity. The ROE in 2024 is 1.52%. These figures suggest a decline in the company's ability to generate returns relative to its capital and equity.

Calculating Return on Invested Capital (ROIC) and Return on Equity (ROE) using the provided data reveals some worrying trends. ROIC, which indicates how efficiently a company is using its capital to generate profit, needs to be calculated using NOPAT (Net Operating Profit After Tax). NOPAT can be derived from EBIT (Operating Income) and the effective tax rate. The effective tax rate can be calculated by dividing Income Tax Expense by Income Before Tax. For 2024, the effective tax rate is 7.03%. So, NOPAT for 2024 is $90,544,720. The ROIC is calculated as NOPAT / Average Invested Capital. Invested capital can be calculated as Total Assets - (Cash & Short Term Investments - Total Liabilities). Average invested capital needs to be calculated using 2023 and 2024. The 2023 number is $2,877,300,000. The 2024 number is $1,774,200,000. The average is $2,325,750,000. The ROIC in 2024 is 3.89%. ROE, which measures the profitability of a business in relation to equity, is calculated as Net Income / Average Stockholders Equity. The ROE in 2024 is 1.52%. These figures suggest a decline in the company's ability to generate returns relative to its capital and equity. The company exhibits a positive trend in free cash flow (FCF) generation. The FCF increased from $152.8 million in 2020 to $408.4 million in 2023. The FCF decreased to $301.1 million in 2024. The Capex remains consistent, but the decrease in FCF can be attributed to the decrease in Net Income. Further investigation needs to be done to investigate the future trends.

The company exhibits a positive trend in free cash flow (FCF) generation. The FCF increased from $152.8 million in 2020 to $408.4 million in 2023. The FCF decreased to $301.1 million in 2024. The Capex remains consistent, but the decrease in FCF can be attributed to the decrease in Net Income. Further investigation needs to be done to investigate the future trends.